Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

It's one of the most common questions we hear as financial advisers: "When can I finally access my super?" The short answer is that you can generally get your hands on your superannuation once you hit your preservation age and meet a condition of release, like retiring for good.

But of course, there's a bit more to it than that. This guide is designed to give you the clarity you need to move forward with confidence.

Your Guide to Accessing Australian Superannuation

Think of your super as a nest egg, carefully protected by the government to make sure it’s there for you in retirement. The rules around accessing it are designed to do just that—protect it. But they can feel a little complicated from the outside.

Our job at Wealth Collective is to cut through the jargon and make it simple. We want you to see your super not as a locked box, but as a powerful tool you can use to shape the future you want. Understanding the rules is the first step to taking control and building a clear path to your ideal retirement.

The Main Hurdles to Unlocking Your Super

When it comes to accessing your super, there are a few boxes you need to tick. It’s not just one thing, but a combination of factors that give you the green light.

Here’s what you need to have in place:

- Your Preservation Age: This isn't the same for everyone. It's a specific age set by the government, based on when you were born. It’s the first major milestone on your path to accessing your super.

- A Condition of Release: Hitting your preservation age is step one, but you also need a valid reason to access your funds. This is what's known as a condition of release, and the most common one is permanently retiring from the workforce.

- The Tax Consequences: This is a big one. How and when you withdraw your super can have significant tax implications. Knowing whether your money will be taxed or tax-free is crucial for smart planning.

It's about more than just getting your money out; it's about setting up a smart, sustainable income that lets you live the life you've worked so hard for. A solid plan ensures your super keeps working for you, long after you’ve stopped.

Navigating these rules is what we do best. At Wealth Collective, we help our clients turn these complex requirements into a clear, personalised strategy. This forms a core part of our Retirement Roadmap service, where we map out your path to and through retirement.

If you’d like to see how we can help you build that clarity, you can book a complimentary introductory call with our friendly team.

What Is Your Preservation Age?

So, you’re starting to think about retirement and wondering when you can finally get your hands on your super. The very first hurdle you need to clear is reaching what’s known as your preservation age.

Think of it as the government's official green light, a specific age you must hit before your super fund is allowed to release your money. It’s a rule designed to make sure your retirement savings are there for their true purpose: to support you when you've actually finished working.

It's easy to get this mixed up with the age you can apply for the Age Pension, or even the age you've personally pencilled in for retirement. But these are all different milestones. Knowing your preservation age is the essential first step to planning your future.

Finding Your Preservation Age

Your preservation age isn't the same for everyone; it’s tied directly to the year you were born. The government gradually increased this age from 55 to 60 over the years, so finding where you land is crucial.

Knowing this date gives you a solid anchor point for your retirement plan. Without it, you're just guessing.

Your Superannuation Preservation Age

Find your preservation age based on your date of birth. This is the first requirement you must meet before you can access your super.

| Date of Birth | Preservation Age |

|---|---|

| Before 1 July 1960 | 55 |

| 1 July 1960 – 30 June 1961 | 56 |

| 1 July 1961 – 30 June 1962 | 57 |

| 1 July 1962 – 30 June 1963 | 58 |

| 1 July 1963 – 30 June 1964 | 59 |

| From 1 July 1964 | 60 |

As you can see, for anyone born from 1 July 1964 onwards, the preservation age is now a standard 60. This means a whole lot of Australians will be reaching this important financial milestone at the same time.

Why It's More Than Just a Date

Here’s where a lot of people get tripped up. Hitting your preservation age doesn't mean your super is suddenly unlocked.

Think of it like this: reaching your preservation age gets you to the front door of your retirement savings, but the door is still locked.

You still need the key to open it. In the world of super, this ‘key’ is meeting a ‘condition of release’. Just turning 58, 59, or 60 isn’t enough on its own.

You must also satisfy one of several specific conditions set out by the Australian Taxation Office (ATO), which we'll explore in the next section.

Grasping this two-part test—your age plus a condition of release—is fundamental. It stops you from making plans that can't be put into action or, worse, making a costly mistake. This is the bedrock of understanding how to access your super.

Figuring out the right way to meet these conditions and manage the tax implications is where good advice can make a world of difference. This is exactly what our Retirement Roadmap service is for. We help pre-retirees get the clarity and strategy they need to make sure every move is the right one, setting them up for a secure and comfortable retirement.

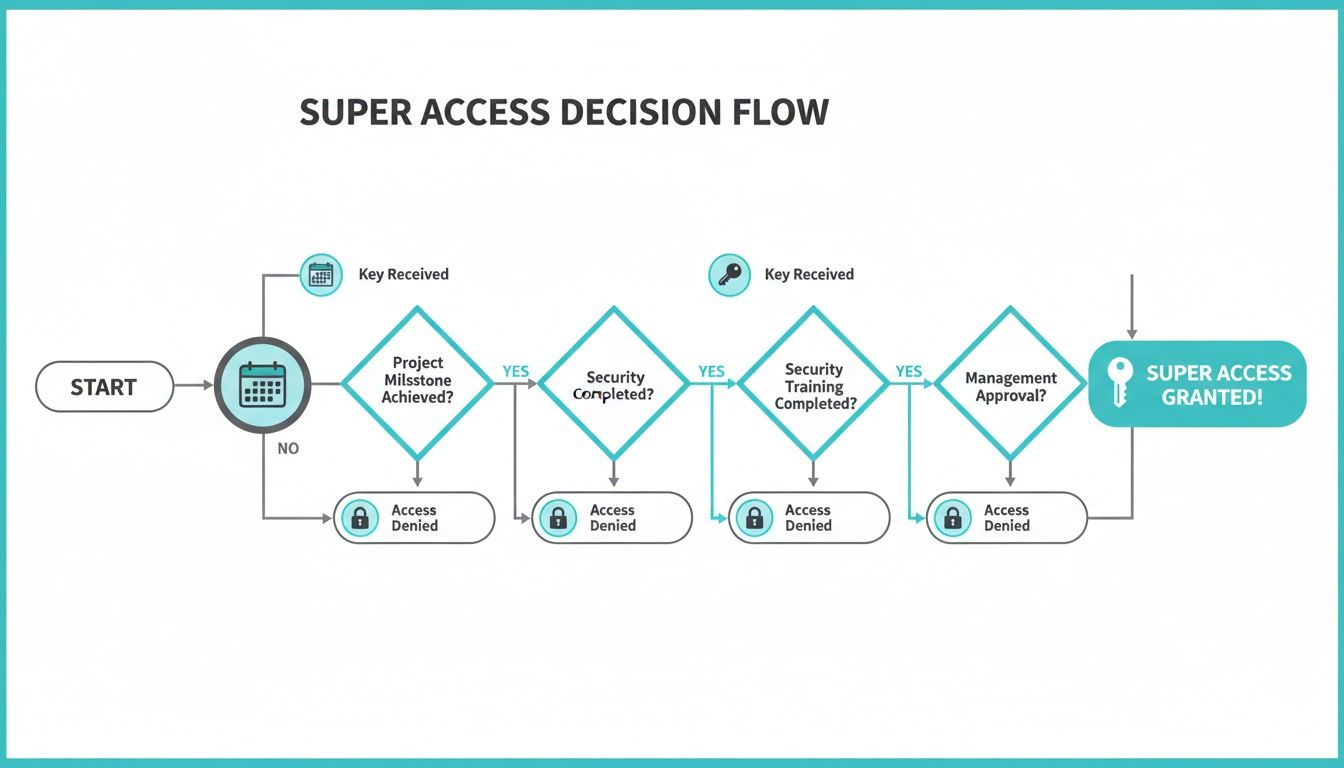

Meeting a Condition of Release to Unlock Your Super

Reaching your preservation age gets you to the front door of your super, but you’ll find that door is still locked. To actually turn the key, you need to meet what’s called a “condition of release”.

Think of these as official triggers, set by the tax office, that prove you’re accessing your nest egg for its intended purpose—funding your retirement. Simply hitting a certain age isn't enough on its own; you have to pair that milestone with a specific life event.

The Most Common Pathways to Your Super

For most Australians, getting your hands on your super will happen through one of three well-worn paths. These are the standard routes for people who are finishing up their working lives.

Retiring for good: This is the most straightforward trigger. Once you reach your preservation age (which is 60 for anyone born after 1 July 1964) and you permanently retire, you can access your super. This means you’ve stopped working and don't intend to work for more than 10 hours a week ever again.

Hitting age 65: This one is simple. The moment you turn 65, your super is yours for the taking, whether you’re still working full-time, part-time, or not at all. At this point, your age is the only thing that matters.

Easing into retirement with a TTR: If you’ve reached your preservation age but aren’t quite ready to stop working, a Transition to Retirement (TTR) pension could be a great option. It lets you draw a regular income from your super while you continue to work, making it easier to reduce your hours without taking a big financial hit.

A Real-World Example: Take David, a 62-year-old who just sold his business. He has met two conditions of release: he’s over his preservation age, and he has officially ceased a gainful employment arrangement. This combination gives him full, unrestricted access to his entire super balance.

Exceptions for Early Access Under Specific Circumstances

While super is designed for retirement, life doesn't always go to plan. The government acknowledges this by allowing early access in a few very specific situations, but the criteria are extremely strict and require a mountain of proof. This isn't a backdoor to paying off your credit card or funding a renovation.

This flowchart maps out the key decision points for getting into your super.

As you can see, reaching your preservation age is just the first step. You still need the "key"—a condition of release—to unlock the funds.

Here are some of the main reasons you might be granted early access:

Permanent Incapacity: If a physical or mental health condition will likely prevent you from ever working again in a job you're qualified for, you may be able to access your super. This has to be certified by at least two doctors.

Terminal Medical Condition: If two medical specialists certify that you have an illness that is likely to result in death within 24 months, you can access your super balance as a tax-free lump sum.

Severe Financial Hardship: This is probably the most misunderstood condition. To qualify, you must prove you've been on government income support payments for at least 26 consecutive weeks and genuinely can't cover immediate family living expenses. Access is usually limited to one payment between $1,000 and $10,000 in any 12-month period. For a deeper dive into these rules, you can check out our guide on how to withdraw super early.

Many people don't realise there can be a big gap between when they can access their super and when they can get the Age Pension. For instance, while you might be able to tap into your super from age 60, the Age Pension doesn't kick in until 67.

This creates a critical planning blind spot that needs to be managed carefully. If you're hoping to retire around 62, a popular age to exit the workforce, you'll need a solid plan to make sure your funds can bridge that multi-year gap comfortably.

Navigating these complex rules—whether for a standard retirement or under special circumstances—is where getting good advice becomes so important. It’s not just about meeting a condition; it's about making sure you do it in the most tax-effective way that supports your long-term goals. Our Retirement Roadmap service is designed to give you that clarity, helping you make the right moves at the right time.

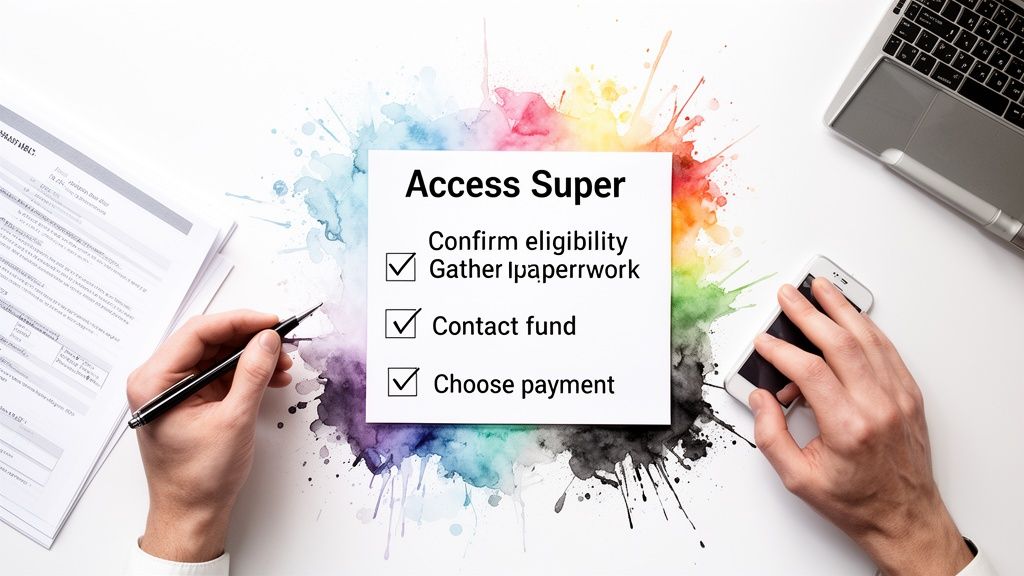

How to Access Your Super Step By Step

Alright, so you’ve hit your preservation age and met a condition of release. The big-picture rules are sorted, but what happens next? How do you actually get your money from your fund into your bank account?

Knowing when you can access your super is one thing, but knowing how is the practical part that matters most. Let’s walk through the practical, four-step journey. This is the admin side of things, and while it might seem a bit daunting, it's completely manageable when you know what to expect.

Step 1: Confirm Your Eligibility and Consolidate

Before you pick up the phone, just take a moment to be absolutely sure. Double-check that you’ve met both your preservation age and a genuine condition of release. Getting this wrong from the start can lead to frustrating delays and a lot of back-and-forth with your fund.

This is also the perfect opportunity to do a bit of housekeeping and track down any lost super. It's incredibly common to have multiple super accounts from different jobs over the years.

Pro-Tip: Your myGov account is your best friend here. You can use the ATO services linked to it to find all your super accounts in one place. Bringing them all together into one fund now will save you a huge amount of paperwork later.

Dealing with multiple funds means you have to repeat the withdrawal process for each and every one. Consolidating first simplifies everything and can even save you money on fees.

Step 2: Gather the Right Paperwork

Your super fund needs to verify who you are and that you’re legally allowed to access your money. It’s no different from a bank asking for ID before a big withdrawal. Having your documents ready to go will make the whole process much faster.

Typically, you'll need to provide certified copies of a few key documents.

- Proof of Identity: Usually a primary photo ID like a driver's licence or passport will do the trick.

- Proof of Age: A birth certificate is often requested to confirm you’ve reached your preservation age.

- Supporting Evidence: Depending on your situation, you might also need a letter from your last employer confirming your retirement date or medical certificates if you're applying for early access on specific grounds.

Rounding up these documents might feel like a hassle, but having them on hand makes the next step a breeze.

Step 3: Contact Your Super Fund

With your folder of documents ready, it’s time to officially apply. Every fund has its own specific forms and processes, but you can usually find everything you need on their website or by giving them a call.

When you get in touch, be crystal clear about which condition of release you’ve met. This is really important, as it dictates what you can withdraw and how. Be prepared to send in your certified documents along with your application forms.

This is the exact point where many people feel overwhelmed. Honestly, it's a key reason clients engage us at Wealth Collective. We take this entire burden off your shoulders, managing the paperwork and liaising directly with your fund to ensure every detail is spot on. It turns a stressful task into a smooth and simple process.

Step 4: Choose How You Want to Be Paid

This is the last, and arguably most important, decision. You've met the rules and filled out the forms—now, how do you want to receive your money? Your two main choices are a lump sum payment or a regular income stream.

- Lump Sum Withdrawal: You can take out some or all of your super balance in a single payment. This can be great for big goals like paying off the mortgage or buying a new car.

- Account-Based Pension: You can roll your super over into a retirement account that pays you a regular income, just like a salary.

Of course, you can also do a bit of both. The right strategy really comes down to your personal financial situation, your retirement goals, and the tax implications. It’s a decision that will shape your financial wellbeing for years to come.

As part of our Retirement Roadmap service, we help you model different scenarios to find the best withdrawal strategy for your life, ensuring your super works hard for you throughout retirement. Book a complimentary call to see how we can make this process simple and effective for you.

Understanding Tax, Drawdowns, and the Age Pension

Figuring out when you can get your hands on your super is only half the battle. The other, arguably more important, part is how you withdraw it. Getting this wrong can have serious consequences for your financial future, affecting everything from the tax you pay to your eligibility for government support.

Think of your super like a carefully filled water tank for your retirement. Once you turn on the tap, how you manage the flow will determine how long that water lasts. This is why getting your head around the rules for tax, compulsory withdrawals, and the Age Pension is so crucial.

The Magic Number for Tax-Free Super

When it comes to superannuation and tax, the most important number for most of us is 60. As soon as you hit this age and meet a condition of release (like retiring for good), any money you take out of your super fund is generally tax-free. That goes for both lump sums and regular income payments.

This is a massive milestone. It means the nest egg you’ve spent decades building can finally start flowing to you without the ATO taking a cut. Before you turn 60, withdrawals are usually taxed, so reaching this age gives you a huge advantage.

It's surprising, then, how many people miss out. Around 700,000 Australians over 65 are still leaving their money in accumulation accounts, where earnings are taxed. By not shifting to a tax-free retirement phase account, they're paying an extra $650 a year in tax on average. It’s a classic case of how indecision can quietly chip away at your savings.

Making Sense of Minimum Drawdown Rates

Once you do convert your super into a retirement income stream, you can’t just let the money sit there indefinitely. The government sets rules requiring you to withdraw a minimum amount each financial year. This is what’s known as the minimum drawdown rate.

These rates are simply a percentage of your account balance, and they increase as you get older. The idea is to ensure you’re actually using your super to fund your retirement, not just holding onto it as a nest egg for your kids.

Here’s what the standard minimum withdrawal percentages look like:

| Age | Minimum Annual Payment (% of balance) |

|---|---|

| Under 65 | 4% |

| 65–74 | 5% |

| 75–79 | 6% |

| 80–84 | 7% |

| 85–89 | 9% |

| 90–94 | 11% |

| 95 or more | 14% |

There's a persistent myth that retirees are overly cautious and don't spend enough of their savings. But recent 2024-25 research paints a very different picture. A significant 68% of retirees are actually taking out more than the mandatory minimums, showing most people are actively using their super to enjoy the retirement they worked for. Discover more insights from this myth-busting super research.

How Your Super Affects Age Pension Eligibility

Of course, your super doesn't exist in a vacuum. You also need to think about how it interacts with the Age Pension. Whether you’re eligible for government support comes down to two main tests run by Centrelink: the assets test and the income test. Your super balance has a big impact on both.

Key Takeaway: Once you reach the Age Pension age, your superannuation balance is counted under both the assets test and the income test. A larger super balance can reduce, or even cancel out, your Age Pension payments.

Here’s a quick rundown of how that works:

The Assets Test: This simply adds up the value of everything you own, including the balance of your super in a retirement account. If your total assets are over a certain threshold, your pension payment is reduced.

The Income Test: This test looks at the income your assets are expected to generate. For your super pension, Centrelink applies a 'deeming' rule—it assumes your investment earns a certain rate of income, no matter what it actually returns. This 'deemed' income is then tallied up as part of the test.

Centrelink will always apply the test that results in you receiving the lower pension payment. It’s this kind of complexity that makes having a smart, professional strategy so important. You’re not just drawing down super; you’re building an integrated, tax-effective income plan for the rest of your life. This is precisely where Wealth Collective’s Retirement Roadmap service can make a difference, helping you structure your finances to get the most from every source.

To get a starting point, feel free to use our handy Age Pension eligibility calculator to see where you might stand.

Build Your Retirement Plan with Wealth Collective

Figuring out when you can get your hands on your super is really just the first step. A great retirement doesn't just happen; it's built on a smart plan for how you’ll actually use that money. This is the point where general information stops and your personal strategy needs to begin.

We've walked through the key milestones: understanding your preservation age, meeting a condition of release, and getting your head around the tax implications. But think of these as individual puzzle pieces. The real magic happens when you fit them all together to create a picture that works for your life.

From Rules to a Real-World Strategy

Turning those complex rules into a solid, practical plan is what we live and breathe. It's the core of the Wealth Collective process. Whether you're a Perth professional looking to maximise contributions or a pre-retiree in Dunsborough mapping out a sustainable income stream, we build strategies tailored to you.

Our whole approach is grounded in two simple truths:

- Clarity is Power: We cut through the jargon so you can make decisions with complete confidence.

- Strategy is Everything: A good plan makes sure your money keeps working for you long after you’ve stopped working for it.

This is exactly why we created services like our Retirement Roadmap, which is all about designing a tax-effective income that’s built to last. Our process provides the structure and clarity needed to navigate this important life stage.

Bridging the Planning Gap

While the rules around super access set the timeline, the reality on the ground shows why planning ahead is so crucial. By the time they reach ages 65-69, men have an average super balance of $448,518, while women have $392,274. That’s a $56,244 difference, often stemming from different career paths and the persistent pay gap.

These numbers tell a powerful story. For younger professionals, it’s a clear signal to get proactive early with strategies like salary sacrificing. For those nearing the end of their careers, it highlights the urgency of having a clear strategy to close that gap and fund a long retirement, especially with the Age Pension eligibility kicking in at 67. If you're curious about how retirees are managing their funds, you can read the full research on superannuation trends.

Your Next Step Is Simple

For many people, a Transition to Retirement (TTR) pension is a fantastic way to ease into that next phase of life. It lets you draw an income from your super while you’re still working, giving you flexibility and options. It’s a strategy we often help our clients put in place, and you can learn more about how TTR pensions work in our article.

At the end of the day, our job is to help you build a financial life you're genuinely excited about. We’ll handle the complexity so you can focus on the future.

The next step is easy. Book a complimentary, no-obligation 10-minute introductory call to chat with our friendly team and see how our process can help you achieve your retirement goals.

Frequently Asked Questions About Accessing Super

We’ve covered a lot of ground on the main ways to get to your super, but it’s the tricky "what if" questions that often pop up. Let's walk through some of the most common ones we hear from our clients every day.

Can I Access My Super Early for Credit Card Debt?

This is a really common question, and the short answer is no. You generally can’t use your super to clear credit card debt or other personal loans. The rules around early access for severe financial hardship are incredibly strict, and for good reason.

They're designed to provide a last-resort safety net for essential living costs—things like rent or food. To even be considered, you usually need to have received government income support for at least 26 consecutive weeks and prove you can't cover your family's immediate needs. Unfortunately, paying down commercial debt just doesn't fall into this category.

Raiding your super to pay off debts might feel like a quick fix, but it can seriously jeopardise your retirement. A better approach is to work with a financial adviser to create a solid debt reduction strategy that doesn't sacrifice your future. This is a common focus for our clients, and one we can help you build a plan around.

What Is a Transition to Retirement Pension?

A Transition to Retirement (TTR) strategy is a great way to ease into your post-work life. It allows you to start drawing an income from your super once you hit your preservation age, even if you’re still working part-time or full-time. Many people use it to reduce their work hours without taking a big hit to their paycheque.

So, what's the catch? The main difference between a TTR and a full-blown retirement pension is how the investment earnings are taxed. Inside a TTR pension, those earnings are taxed at up to 15%. Once you properly retire and convert your super into an Account-Based Pension, those same earnings become completely tax-free.

Deciding if a TTR is the right move means balancing the need for more income now against the tax you’ll pay. It’s a nuanced decision, and it’s something we map out with clients in our Retirement Roadmap service to make sure it fits their bigger picture.

Should I Take My Super as a Lump Sum or an Income Stream?

This is probably one of the biggest financial crossroads you'll ever face. When you retire, you can take your super as a single lump sum, a regular income stream (often called a pension), or even a bit of both.

A lump sum gives you a big chunk of cash upfront—perfect for paying off the mortgage or finally buying that caravan. An income stream, on the other hand, acts like a regular salary, giving you reliable funds to cover your ongoing living expenses.

For most Australians over 60, both options are generally tax-free. The real kicker is how your choice impacts your eligibility for the Age Pension and, just as importantly, how long your own savings will actually last. There's no single right answer here.

At Wealth Collective, our process involves running the numbers for our clients, modelling what each scenario looks like ten, twenty, and thirty years down the track. Seeing the long-term impact makes it much easier to build a withdrawal strategy that gives you real security and peace of mind.

Knowing the rules for accessing your super is one thing, but building a smart strategy around them is what truly sets you up for a great retirement. At Wealth Collective, our job is to turn complexity into a clear, actionable plan for your future.

Book a complimentary 10-minute introductory call to see how we can help you build your ideal financial life.