Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You might be earning well, paying down a mortgage, building super, maybe holding a few investments, and still feel like you're making money decisions one at a time with no real map. One month the focus is cash flow. The next it's interest rates, school fees, insurance, or whether you should put extra money into super. It can feel busy without feeling clear.

That's usually the moment people realise they don't need more random tips. They need a strategy.

Beyond Budgeting What Is Strategic Financial Planning

Budgeting matters. It helps you control spending, avoid drift, and make sure your money lasts from one pay cycle to the next. But a budget on its own is like having a shopping list for materials without the house plans.

Strategic financial planning is the blueprint.

It looks across your whole financial life and asks a different set of questions. What are you trying to build? When do you want work to become optional? How should your mortgage, super, investments, tax position, and personal insurance work together? What trade-offs move you closer to the life you want?

Blueprint thinking changes the decisions you make

A tactical money decision usually solves one immediate issue. You move cash into savings. You make an extra loan repayment. You top up super. Each step might be sensible.

A strategic plan asks whether those actions are happening in the right order, for the right reason, and with a clear long-term outcome in mind.

| Aspect | Tactical Decision | Strategic Plan |

|---|---|---|

| Timeframe | Focused on the next bill, month, or short-term issue | Focused on the next stage of life and the years ahead |

| Scope | Looks at one account or decision at a time | Connects cash flow, debt, super, investments, tax, and protection |

| Trigger | Often reactive | Deliberate and goal-led |

| Confidence | Can feel like guesswork | Gives you a repeatable decision framework |

If you've ever watched a renovation go wrong, you've seen what happens when good trades work without one shared plan. The plumber, electrician, and builder may all be skilled, but the result can still be messy. Money works the same way.

A good plan doesn't remove uncertainty. It gives you a way to make decisions when life gets uncertain.

For people who want a business-style way to think about changing assumptions, it can help to understand rolling forecasts. The idea transfers well to personal finances because life rarely follows a static annual plan.

If you want a more detailed primer on the broader process, Wealth Collective also explains the foundations in its guide to financial planning in Australia.

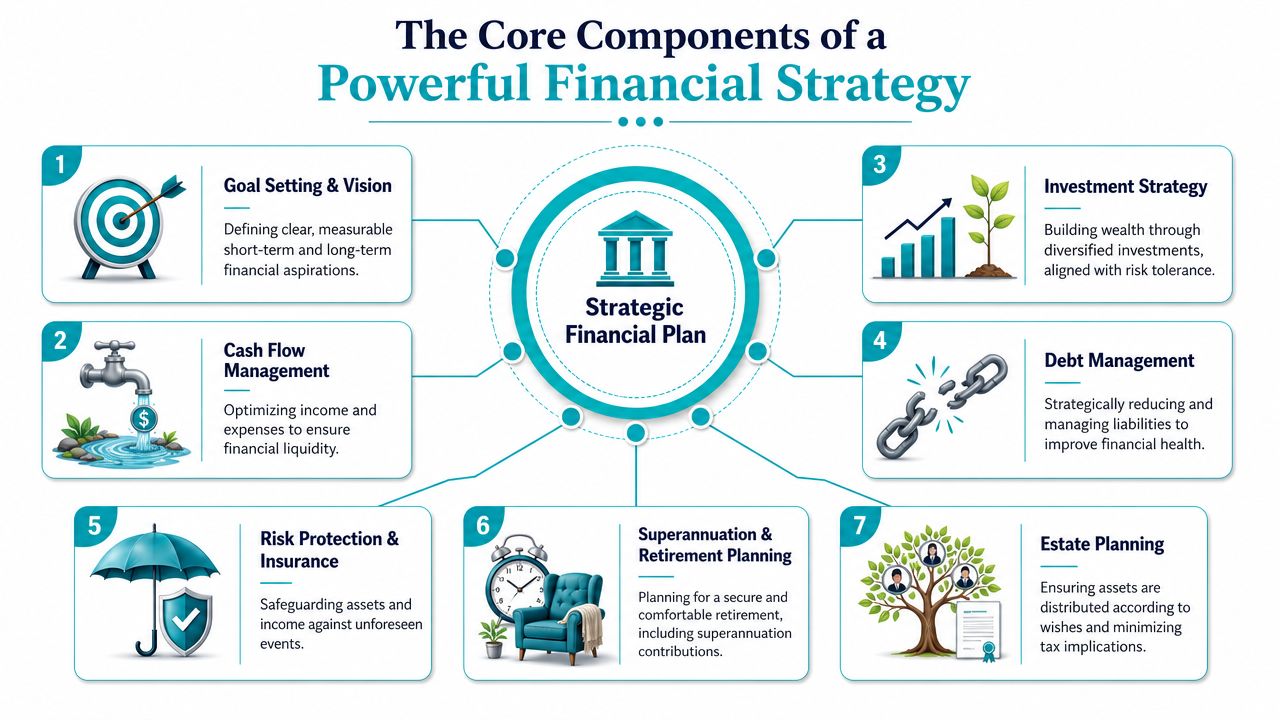

The Core Components of a Powerful Financial Strategy

A strong strategy isn't one product, one account, or one investment idea. It's a structure. In practice, most Australian households need a plan that coordinates four core areas at the same time.

Wealth creation

This covers the assets you're building for future freedom. For most Australians, superannuation sits at the centre of this. Strategic planning became especially important after the Superannuation Guarantee was introduced on 1 July 1992, and the compulsory SG rate later reached 12% on 1 July 2025, which materially changed how Australians build retirement wealth and made long-term contribution, tax, and cash-flow planning central to financial strategy, as outlined in this discussion of the importance of strategic finance.

That matters because super is no longer a side issue. It's one of the main engines of long-term wealth for employees, especially for pre-retirees, high-income earners, and dual-income households.

If you want to unpack how that system works, this explainer on superannuation in Australia is a useful starting point.

Debt and cash flow

A plan also needs to answer a practical question. How much of today's income should support today's life, and how much should build tomorrow's options?

For some households, the strategic move is accelerating a mortgage. For others, it's preserving flexibility with cash buffers. For people with uneven income, it may be less about maximising every spare dollar and more about making the whole structure resilient.

Risk protection

This is the pillar people often ignore until something goes wrong.

Insurance doesn't create wealth directly. It protects the ability to create it. If a household depends on one or two incomes, then income protection, life cover, or other personal risk cover can act like the structural beams in a home. You don't admire them every day, but you definitely notice when they're missing.

Estate and legacy planning

Many view estate planning as something to sort out later. In reality, it belongs inside a strategic plan much earlier.

Here, the central issue is coordination. You want ownership structures, beneficiaries, legal documents, and family intentions moving in the same direction. That's how wealth gets transferred with less confusion and less stress.

Practical rule: If one financial decision weakens another part of your structure, it isn't strategic. It's just activity.

These pillars don't sit in separate boxes. Extra super contributions affect cash flow. Faster debt reduction affects liquidity. Insurance premiums affect how much you can invest. Estate decisions influence how assets should be held. The power comes from integration.

Your 5-Step Strategic Financial Planning Framework

A sense of calm often arises once the process becomes visible. A good plan isn't magic. It's method.

Step 1 Assessment

Start by getting the facts into one place. Income. Spending. Debts. Super balances. Investments. Insurance. Ownership structures. Existing goals.

This sounds simple, but it's where many people first see their financial life clearly. Until then, they're often making decisions from memory, habit, or whatever feels urgent.

A snapshot gives you a base camp. Without that, every recommendation sits on shaky ground.

Step 2 Goal setting

“Be better with money” isn't a strategy. Neither is “retire comfortably.”

Useful goals have shape. They connect to timing, lifestyle, and trade-offs. A household might want to reduce debt while preserving flexibility for children's costs. A business owner might want optionality rather than a hard retirement date. A pre-retiree might want confidence that work can become part-time instead of full-time.

Step 3 Strategy design

At this point, the plan becomes selective.

Not every decent financial move deserves equal priority. One of the most useful planning concepts here is benchmark-driven allocation of scarce capital. In plain English, that means comparing your options instead of assuming every spare dollar should go to the same place. Strategic planning literature frames this as ranking debt reduction, super optimisation, insurance funding, and investment contributions against explicit criteria such as return thresholds, payback periods, and risk assessments, then revisiting assumptions regularly so capital doesn't get trapped in low-value uses, as discussed in this article on critical financial data points in strategic business planning.

That's a long sentence for a simple idea. Compare before you commit.

A useful design discussion might sound like this:

- Super question Which contribution level improves retirement readiness without straining near-term cash flow?

- Debt question Does paying extra into the mortgage create more value than building liquid reserves?

- Protection question Is the household exposed if one income stops unexpectedly?

- Investment question Are new contributions aligned with time horizon and tolerance for volatility?

Step 4 Implementation

A plan only becomes real when the accounts, policies, contributions, and structures change.

This step often includes practical tasks such as adjusting contribution settings, redirecting surplus cash flow, updating insurance, consolidating old arrangements, or changing investment settings. The work can feel administrative, but it's through these actions that strategy becomes effective.

For clients who want support carrying out that work, firms such as Wealth Collective can assist with implementation across superannuation optimisation, investment strategy, debt reduction, and protection planning.

Step 5 Monitoring and review

Life changes. Rates change. Work changes. Families change.

That means the plan should be reviewed, not admired. A review isn't just a check on investment performance. It's a check on whether the current structure still suits the life you're now living.

Review your plan when your life changes, not only when markets do.

A working framework creates calm because decisions stop being random. You know where you are, where you're going, and what deserves attention next.

Strategic Planning in Action Real-World Examples

A framework becomes useful when you can see yourself inside it. Here are three situations that come up often for Australians trying to make strategic decisions, not just isolated money moves.

Young professionals with competing priorities

A couple in WA are both earning, both busy, and both trying to do the right thing. They've got a mortgage, childcare costs on the horizon, and a rough sense that they should invest more. One income is stable. The other varies because of contract work.

Their problem isn't lack of motivation. It's sequencing.

Mainstream advice often assumes tidy monthly income, but that doesn't reflect many real households. A major underserved angle in strategic financial planning is how it should change for Australians with irregular or gig-style income, because non-standard work remains material and many households need planning around buffer sizing, super contributions, debt reduction, and insurance decisions in years when income is uneven rather than linear, as discussed in this piece on strategic financial capital planning.

For this couple, the strategic answer might be to build a stronger cash buffer first, automate a baseline super or investment amount that feels sustainable even in softer income months, and use high-income periods for targeted debt reduction. That's very different from forcing a rigid monthly plan that breaks every quarter.

Pre-retirees trying to get the order right

Another couple are approaching retirement and asking the question many people ask too late. What should happen first?

They can make extra mortgage repayments. They can direct more into super. They can hold more cash. They can reduce investment risk. All of those sound sensible, but not all at once and not in equal amounts.

What usually helps here is a decision framework rather than a checklist. The right sequencing depends on liquidity needs, tax position, comfort with market swings, and how close paid work is to ending. For some, reducing debt creates peace of mind. For others, building retirement assets inside the right structure is more valuable. For others again, the key move is reducing the risk of a badly timed market drawdown.

Small business owners with blurred lines

A business owner often has a more complex version of the same challenge. Personal and business finances leak into each other. Cash flow can be strong one quarter and tight the next. Planning gets pushed aside because operations feel more urgent.

The five-step framework works especially well here because it creates separation. First, get a clear picture of what belongs to the household and what belongs to the business. Then define what the personal end goal is. Is it passive income? A future sale? More flexibility? Less stress?

From there, strategic choices become clearer. The owner might prioritise a larger buffer, cleaner debt structures, a super contribution rhythm that fits uneven income, and protection arrangements that don't leave the family exposed if the business hits a rough patch.

Good strategy often feels less dramatic than people expect. It replaces financial noise with a clear order of operations.

The Unexpected Benefits of a Strategic Plan

People usually begin planning because they want better financial outcomes. More clarity around retirement. Smarter use of surplus cash. A cleaner path through debt, investing, and super. Those are important.

The surprise is that the biggest benefit often isn't numerical. It's emotional.

Clarity reduces background stress

Money stress rarely comes from one bill. It comes from unresolved questions sitting in the background. Are we doing enough? Should we be paying off debt faster? Are we behind on retirement? What happens if work changes?

A strategic plan turns those vague worries into specific decisions. Once priorities are visible, people stop carrying so much low-grade uncertainty.

Confidence improves decision-making

Australia's retirement system shows why this matters. A comfortable retirement in 2024 was estimated to require $73,077 a year for a single person and $103,456 a year for a couple, and life expectancy at age 67 is roughly another 20 to 25 years, meaning retirement savings may need to support income for decades, according to this overview of strategic financial planning and retirement context.

When the stakes are that high, confidence isn't a luxury. It's functional. You need a way to judge whether a decision helps or hurts the long-term plan.

Resilience matters when conditions change

A strategic plan also gives households a framework for rough periods. That might mean a market downturn, a pause in work, a health event, or a sharp rise in costs.

For business owners, this kind of thinking overlaps with broader contingency planning. If that's relevant to you, these strategies for business in recession can be a useful companion read because they reinforce the same principle. Build resilience before you need it.

Better conversations at home

Couples often argue less about money once they're no longer arguing from different assumptions.

One person may value security and cash reserves. The other may want faster growth. Neither is necessarily wrong. The problem is the absence of a shared framework. A plan gives both people a reference point, which makes decisions feel less personal and more practical.

When a couple agrees on the destination, the trade-offs feel less like conflict and more like coordination.

That shift alone can change how money feels day to day.

Common Mistakes to Avoid in Your Financial Plan

Most financial mistakes aren't caused by laziness. They happen because people make understandable decisions without a clear framework.

Mistaking motion for progress

It's easy to feel productive when you're doing something. Opening an investment account, making extra repayments, chasing a better rate, switching funds. Action feels reassuring.

But activity isn't the same as progress. A strategic plan asks whether each action fits the bigger picture. Without that filter, people can end up pulling in opposite directions.

Setting goals that are too vague

“Build wealth” sounds sensible but doesn't help with actual choices.

Clear goals create constraints, and constraints are useful. If you know what the money is for, by when, and what flexibility you need along the way, then your decisions become sharper. Without that, almost any option can be justified in the moment.

Confusing products with planning

A product can play a role in a plan. It is not the plan.

This is one of the most common traps. People ask which fund, which investment, which loan structure, or which policy is best before they've settled the strategic question underneath. That's like choosing tiles before you know the house design.

Letting emotions take the wheel

Money decisions become erratic when fear and excitement run the process.

People can panic when markets fall, become overconfident when things rise, or make rushed choices after hearing what a friend is doing. A strategic plan gives you pre-agreed rules so you don't have to invent a philosophy during stressful moments.

Treating the plan as fixed

The opposite of reactive money management isn't rigid money management.

A good plan should adapt. New jobs, children, inheritance, health events, business changes, and retirement timing all affect priorities. If you never revisit the strategy, it slowly becomes a history document.

A practical way to stay out of trouble is to ask three questions before any major move:

- Does this support my main goal?

- What trade-off am I making elsewhere?

- Will this still make sense if circumstances change?

Those questions won't answer everything, but they'll stop many expensive detours.

Your Path to a Wildly Successful Financial Life

Strategic financial planning gives you something far more useful than a pile of disconnected recommendations. It gives you a way to think. A way to prioritise. A way to make decisions with more calm and less second-guessing.

That matters whether you're building momentum, protecting a growing family, preparing for retirement, or trying to make sense of uneven income. The process is the same at heart. Understand your position. Define what matters. Build the right sequence. Put it into action. Review as life changes.

If you're comparing different advice approaches, it can also help to see how other firms describe strategic financial solutions. The language varies, but the common thread is clear. Better outcomes usually come from coordination, not isolated decisions.

Choosing the right adviser matters as much as choosing the right strategy. If you're weighing up what to look for, this guide on how to choose a financial advisor can help you assess fit, communication style, and scope of advice.

The first step doesn't need to be dramatic. It just needs to be clear. Sometimes a short conversation is enough to turn a vague sense of financial pressure into a practical next move.

If you'd like to explore what a customized strategy could look like, book a conversation with Wealth Collective. Their free, no-obligation 10-minute introductory call is a simple way to see whether the process fits your goals, your stage of life, and the kind of support you want to create your own wildly successful financial life.