Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You're probably in one of two positions right now. You're either running a business in WA and paying someone through invoices because that felt simpler than payroll, or you're a professional weighing up a contract offer and wondering whether the extra hourly rate is worth it.

Both situations look straightforward on paper. They're not.

The contractor vs employee ATO question has become one of the easiest places to make an expensive mistake. The problem isn't only about tax. It's that the ATO and Fair Work don't always look at the same relationship in the same way. A worker can sit in one bucket for tax and a different bucket for employment rights. If you rely on the label in the contract and stop there, you can end up exposed on multiple fronts.

The High Stakes Decision Every Business Faces

A Perth business owner hires a long-term “contractor” with an ABN. They work set days, use the business systems, report to a manager, and do the work personally. Everyone calls them a contractor. The invoices come in monthly. It feels organised.

Then the arrangement gets tested.

That's where people discover the trap. The contractor vs employee ATO issue isn't just about whether someone has an ABN or sends invoices. It's about what the relationship really is for tax, super, and related obligations. On top of that, Fair Work can apply a different lens to employment rights. That gap catches people because most guidance collapses both tests into one simplified answer.

The practical risk is bigger than most owners realise. A 2025 Fair Work Ombudsman report indicates that 34% of misclassified workers in Australia are incorrectly labeled as contractors for tax but are legally employees for other rights. That's the exact compliance blind spot many WA businesses are operating in right now.

A useful external reference on the broader issue is this guide to worker classification, which helps frame why classification can't be treated as a paperwork exercise.

The label on the agreement matters less than the rights, duties, and day-to-day reality behind it.

If you're a business owner, the stakes are obvious. Get it wrong and you may have to unwind tax and super obligations after the fact. If you're an individual, the stakes are personal. A contract role that looks lucrative can leave you funding your own super, leave, and protection without pricing that cost properly.

Here's the blunt view. If you haven't reviewed contractor arrangements recently, you're trusting assumptions that may already be out of date.

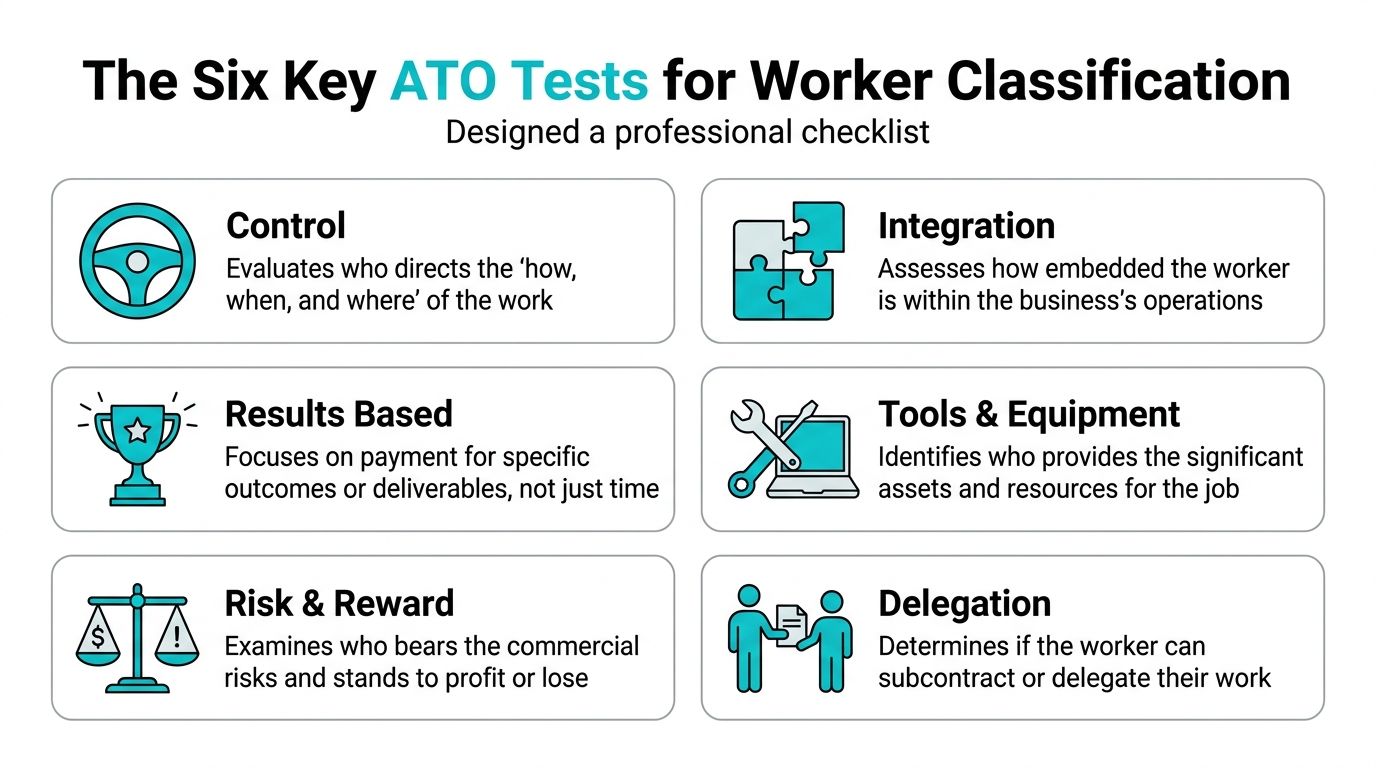

The Six Key ATO Tests for Worker Classification

The ATO doesn't decide status based on one magic clause. It looks at six key factors: delegation, payment, equipment, commercial risk, control, and integration, as outlined in the ATO's employee or independent contractor guidance.

Control over the work

Control asks a simple question. Who decides how, when, and where the work gets done?

If your business tells someone their hours, location, and method, that points towards employee status. If you engage someone to produce an outcome and they choose how to deliver it, that points towards contractor status.

Practical rule: If you're directing the process, not just the result, you're moving closer to employment.

A receptionist rostered into your front desk is different from a web developer engaged to deliver a finished site by a deadline.

Ability to delegate

Delegation is one of the clearest dividing lines. A genuine contractor can usually subcontract or delegate the work, and they pay that substitute themselves. An employee usually has to do the job personally.

This aspect is significant, as personal service under your direct oversight looks much more like employment.

If the person can't legally send someone else in their place, that's a warning sign.

Basis of payment

The ATO also looks at how payment is structured.

An employee is usually paid for time, activity, or attendance. A contractor is more often paid for a quoted result, milestone, or completed deliverable. That doesn't mean hourly billing automatically makes someone an employee, but time-based pay is one factor that can push the relationship that way.

Tools and equipment

Who provides the essential tools?

A contractor typically brings and pays for their own equipment. An employee usually uses business-supplied tools, software, systems, or vehicles. If the worker relies almost entirely on your setup, it weakens the contractor argument.

Commercial risk

A real contractor bears commercial risk. They can profit from efficient work, but they also wear the cost of fixing defects or mistakes.

An employee usually doesn't absorb that risk personally. If something goes wrong, the employer wears it.

Integration into the business

This is the “are they part of your business or running their own?” test.

A worker who appears on your org chart, uses your internal processes, works under your brand, and functions as part of the team may be integrated into the business. A contractor should look more like an external operator running an independent enterprise.

A quick working summary helps:

| ATO factor | Leans employee | Leans contractor |

|---|---|---|

| Control | Business directs hours, place, method | Worker controls delivery |

| Delegation | Must perform work personally | Can subcontract or delegate |

| Payment | Paid for time or activity | Paid for result or quote |

| Tools | Business provides key tools | Worker supplies own tools |

| Risk | Business absorbs mistakes | Worker fixes errors at own cost |

| Integration | Part of internal operations | Operates independently |

One more point people miss. An ABN and an invoice don't decide anything on their own. They're administrative details, not proof of contractor status.

Employee vs Contractor A Side-by-Side Financial Comparison

Legal classification matters because it changes the money. Not just tax withholding. The whole economics of the role.

For an employee, part of total remuneration sits outside the hourly or salary figure. For a contractor, those costs often land on the individual instead. That's why many people underestimate the true break-even point.

Financial obligations employee vs contractor

| Financial Aspect | Employee Responsibility | Contractor Responsibility |

|---|---|---|

| PAYG tax withholding | Employer generally manages withholding through payroll | Worker typically manages own tax position unless a specific withholding arrangement applies |

| Superannuation | Employer funds compulsory super where required | Worker often funds their own super, unless super obligations still apply to the arrangement |

| Annual leave | Employee receives paid annual leave | Contractor usually gets no paid annual leave |

| Personal or carer's leave | Employee receives paid personal or carer's leave | Contractor usually gets no paid personal or carer's leave |

| Workers' compensation coverage | Employer generally maintains coverage for employees | Contractor may need to arrange their own protection depending on the arrangement |

| Equipment and business costs | Employer often provides core tools and systems | Contractor often pays for tools, software, insurance, and overheads |

| Income stability | Regular pay cycle | Payment can depend on invoices, milestones, and collection timing |

The key benchmark is this: a contractor must charge at least 30% to 50% more per hour than the equivalent employee rate to achieve an identical net financial position, after accounting for self-funded superannuation, leave, and other entitlements, including the 12% Superannuation Guarantee in FY2025-26 according to this contractor vs employee pay comparison.

Why the headline hourly rate misleads people

A contract offer can look better on first glance because the hourly figure is higher. But that premium isn't a bonus if it's merely replacing things an employee receives automatically.

Those include:

- Super contributions: Employees receive employer-funded super under the applicable rules. Contractors often have to build this into their pricing.

- Leave entitlements: Employees are paid during annual leave and personal leave. Contractors usually aren't.

- Risk costs: Contractors may need to absorb gaps between projects, unpaid admin time, and self-funded protections.

That's why I tell clients to stop comparing hourly rate to hourly rate. Compare net position to net position.

A contract role only wins financially if the rate covers what you're giving up.

For readers who want a non-Australian comparison of how people frame this trade-off in freelance markets, this informed choice for UK freelancers is useful as a mindset piece. The tax systems differ, but the commercial logic is similar.

What business owners should do with this

If you're engaging contractors, don't assume you're saving money just because you're not running payroll. The cost depends on whether the arrangement is independent and whether the rate reflects what the contractor is expected to fund themselves.

If you're the worker, price from the bottom up. Include super, unpaid leave, and downtime. If the premium isn't there, the deal may be worse than employment dressed up as flexibility.

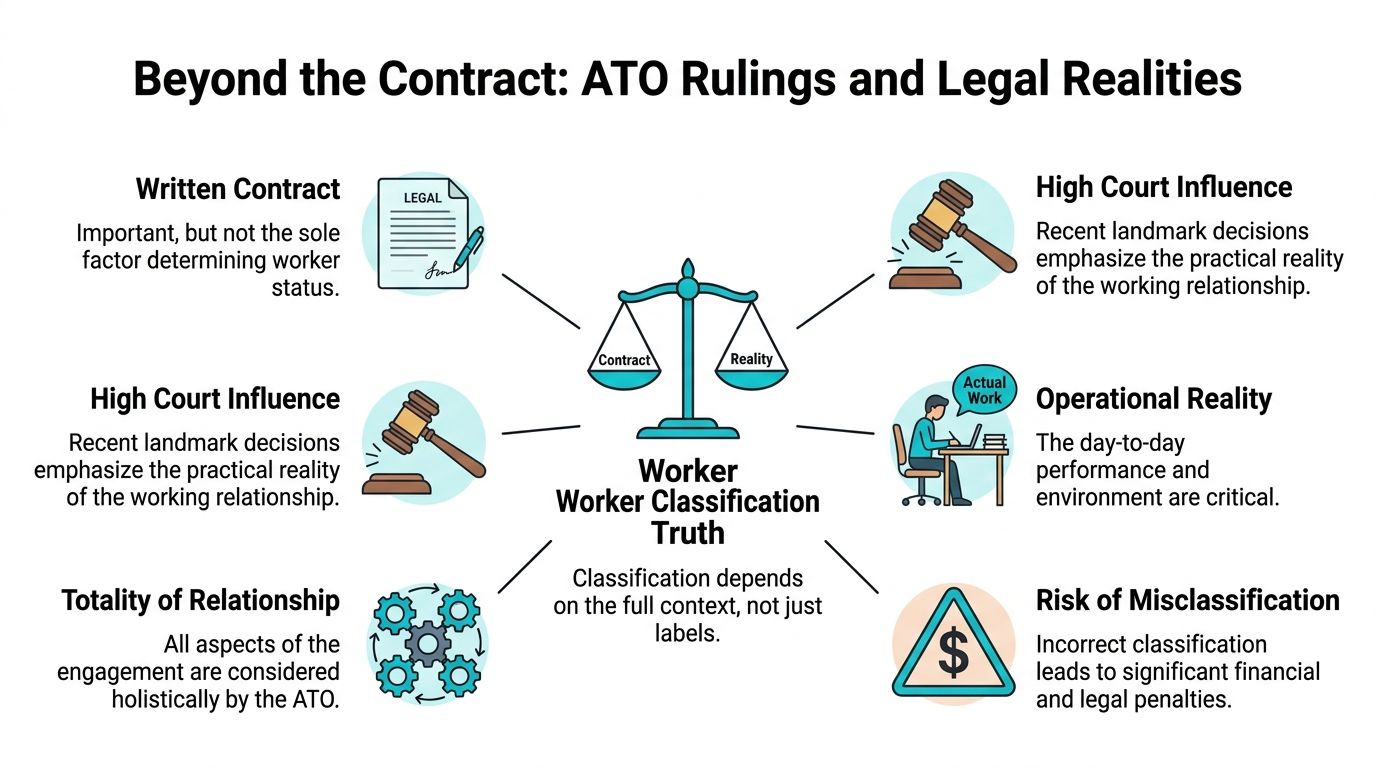

Beyond the Contract ATO Rulings and Legal Realities

A lot of older advice on contractor vs employee ATO treatment is stale. The legal position shifted after two High Court decisions in February 2022, and the ATO updated its approach in TR 2022/D3. The core message is clear in KPMG's summary of the High Court decisions and ATO guidance update. Where a written contract explicitly sets out the rights and duties, and it isn't a sham, those legal terms are decisive in classification.

That has led some businesses to overcorrect. They assume a polished contract solves the problem. It doesn't.

A strong contract helps, but only if it reflects the real arrangement

If your agreement says the worker controls their hours, can delegate, and runs an independent business, but your managers roster them like staff and require personal attendance, you've created a mismatch. That mismatch is where disputes start.

The ATO also uses a four-zone risk assessment model to allocate compliance resources, from very low to high risk. That means some arrangements are much more likely to attract attention than others. If your setup has obvious employee indicators dressed up in contractor language, you're taking on preventable risk.

Where WA business owners often get caught

The biggest practical mistake is treating this as a tax-document exercise rather than an operational design issue. The contract, onboarding process, approval workflows, equipment access, and supervision model all need to line up.

For businesses already reviewing tax exposure, it's worth looking at broader planning opportunities through a small business tax reduction approach at the same time. Classification errors often sit beside other avoidable structural issues.

If a matter is already moving towards a disagreement, external help can be useful. These ATO dispute resolution services outline the kind of support businesses often need once the issue escalates.

The best contract in the world won't rescue a working arrangement that operates like employment.

The practical takeaway is simple. Get the legal drafting right, then make sure the business behaves that way.

Implications for Small Businesses and High Income Earners

The same classification issue hits different people in different ways. For small businesses, it's mostly about downside risk. For high-income professionals, it's often about structuring income, super, and flexibility without tripping over technical rules.

Small businesses need to think beyond convenience

Many owners use contractors because it feels faster. Less payroll. Less admin. More flexibility. That convenience disappears fast if the worker should have been treated differently from the start.

The most common pattern is long-term engagement drift. Someone starts as a genuine project contractor. Over time, they become embedded. They work regular hours, rely on internal systems, and stop looking like an external operator. The paperwork stays the same, but the reality changes.

That's the point where a periodic review matters. If you're already tightening your business systems, this is exactly the sort of issue that should sit inside a broader accounting for small business near me review rather than being left to guesswork.

High-income earners have a specific super rule to watch

There's also a very specific issue for executives and high-income contractors. A new legislative provision allows high-income contractors earning above $183,000 from July 1, 2025 to formally opt out of superannuation guarantee obligations, but only if they provide a written notice before the work commences.

That timing matters. Miss it, and you can't assume the opt-out works.

Here's the practical summary:

- Income threshold matters: The opt-out only applies if earnings are above $183,000 from 1 July 2025.

- Paperwork matters: The notice must be in writing.

- Timing matters most: It must be provided before the engagement starts.

This is one of those rules that sounds simple and gets mishandled because people focus on income level and forget procedure.

The decision point for both groups

For business owners, the question is whether the arrangement has been designed properly.

For high-income individuals, the question is whether the contract rate, super position, and overall wealth strategy still stack up once you strip away the headline numbers.

Those are different questions, but they need the same discipline. Don't rely on assumptions. Review the arrangement before the first invoice goes out.

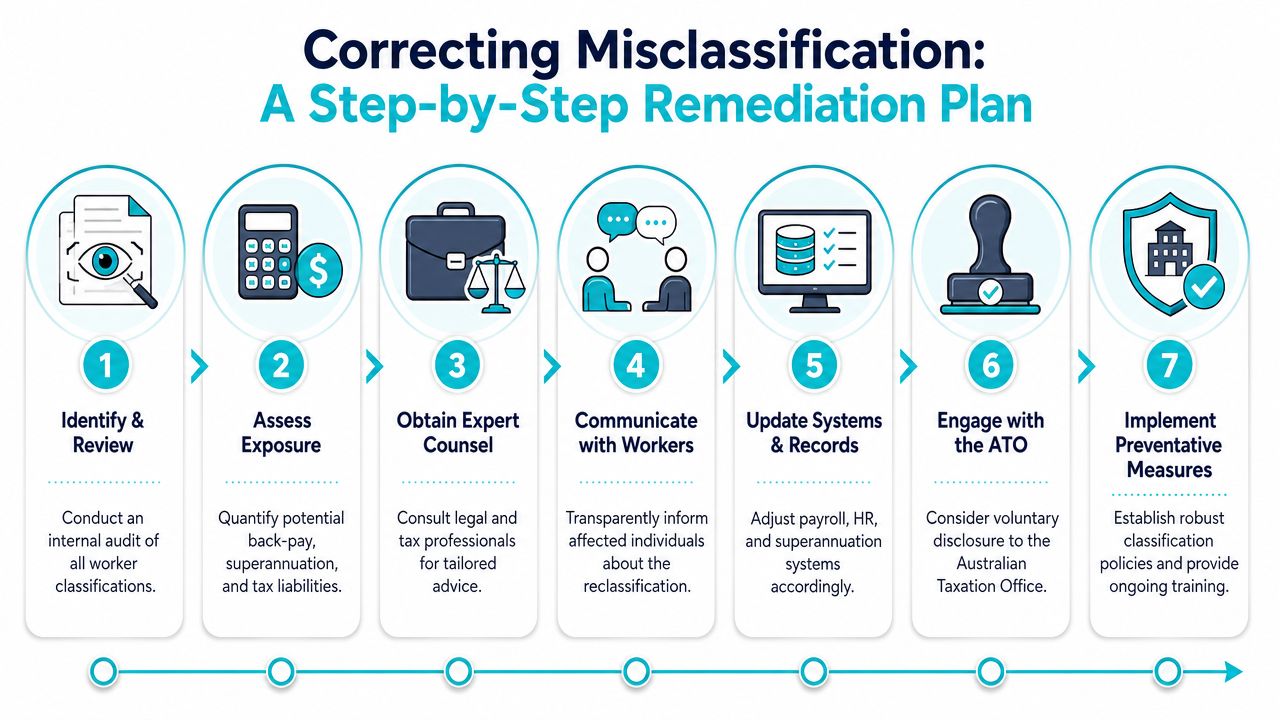

Correcting Misclassification A Step-by-Step Remediation Plan

If you think you've misclassified a worker, don't freeze and don't try to bury it in a new contract. The ATO's position is clear in Pitcher Partners' summary of the tax perspective on contractor versus employee status. If the worker is an employee, a contract calling them a contractor doesn't override tax and super obligations.

Start with a clean review

Pull the contract, invoices, onboarding documents, payment records, and any internal instructions that show how the relationship operated.

Then test the arrangement against the indicators already covered. Focus on control, delegation, payment structure, tools, risk, and integration. Don't let titles like “consultant” or “contractor” distort the assessment.

Work through remediation in order

Review each current contractor arrangement. Don't isolate the one that triggered concern. Classification problems often repeat across similar roles.

Estimate the exposure. Work out where tax, super, and related obligations may have been missed. You need a realistic number before you decide how to respond.

Fix the status going forward. Either redesign the engagement so it functions as an actual contractor arrangement, or move the worker to employment if that reflects reality.

Correct payroll and records. If someone should be on payroll, systems need to be updated properly. For some businesses, old reporting issues also create confusion. If you're sorting historical payroll documents, guidance on items like a PAYG summary process can help clean up the admin side.

Take advice before contacting regulators. Voluntary correction is often better than waiting to be challenged, but timing and wording matter.

Fixing misclassification is a financial decision, not just a legal one. Handle it with numbers, records, and a clear sequence.

Don't treat remediation as DIY if the facts are messy

Simple cases can look simple until you test the details. Mixed indicators, old contracts, long-running arrangements, and inconsistent payment methods all make the analysis harder.

If the relationship changed over time, you may also need to identify when it changed. That's where many owners go wrong. They assume status is fixed forever from the start date. It isn't. The risk can increase gradually as the role becomes more embedded.

The best move is to deal with it early, document everything, and avoid casual fixes that create a second problem later.

Navigate Your Financial Future with Confidence

The contractor vs employee ATO question isn't admin trivia. It affects tax, super, leave economics, business risk, and personal wealth outcomes. For WA business owners, the hidden danger is the split between ATO tax treatment and Fair Work employment rights. For professionals, the danger is accepting a contractor label without pricing the role properly or understanding the super consequences.

That's why this issue deserves a proper review, not a guess.

A good decision here protects more than compliance. It protects cash flow, margins, retirement savings, and the strength of your broader financial plan. It also creates opportunity. When the structure is right, business owners can engage talent with confidence, and individuals can assess whether a contract role advances their long-term position.

If you're unsure whether a current arrangement is safe, don't wait for a dispute, an audit, or a super problem to force the issue. Review it while you still have options.

The right advice should make this simpler, not more confusing. You want a clear answer on where you stand, what the exposure is, and what to do next.

If you want clarity on contractor arrangements, super, business risk, or how this fits into your broader wealth strategy, book an initial call with Wealth Collective. It's a practical first step to get clear advice and a plan that protects both your finances and your future.