Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You're probably searching accounting for small business near me because something already feels messy.

Maybe it's a late-night Xero catch-up. Maybe your BAS is coming up and the bank feed still doesn't match. Maybe payroll is running, money is coming in, invoices are going out, and you're wondering whether the business is paying you properly or just keeping you busy.

That's the point where most WA owners make the same mistake. They look for someone to “do the tax”.

Fair enough. But it's too small a brief.

If you run a business in Perth, Dunsborough, or anywhere across WA, the right accountant shouldn't just lodge forms and clean up the books after the fact. They should help you understand what the numbers are saying now, where cash is getting stuck, what obligations can hurt you if ignored, and how the business fits into your personal wealth plan.

Your Guide to Finding the Right Local Accountant

It's 7:30 at night. You've finished a full day on the tools, at the desk, or in the shop. Then you open the books and realise the numbers still don't answer the only questions that matter. What can I safely draw? What do I owe? Is this business actually building wealth, or just producing work?

That's when a lot of WA owners type “accounting for small business near me” into Google and pick the closest firm.

Convenient, yes. Smart, not always.

A local accountant should understand Australian business obligations and the basics that keep a business under control, including cash flow, bank reconciliations, payroll, receivables, and payables. The Australian Government's business finance guide covers those fundamentals well. But proximity is not the standard you should hire on. You're not buying a postcode. You're choosing someone who will influence your decisions, your tax position, and, if they're any good, your personal wealth outside the business as well.

That last part gets missed all the time.

Plenty of accountants can keep records tidy and lodge on time. Fewer can show you how business profit, tax planning, super, debt reduction, and personal investing fit together. If your accountant never asks what you want the business to do for your life, they're working too narrowly.

If you want a quick example of how local service pages frame nearby support, have a look at these Northern Beaches accounting services. It shows the standard “near me” pitch clearly. Location, convenience, service list. Useful, but incomplete. The real question is whether the adviser can turn compliance into better cash control, better tax decisions, and a clearer path to wealth.

Practical rule: Hire the accountant who helps you make decisions during the year, not just explain the result after year-end.

Good accountants keep you compliant. Strong accountants improve how you operate. The right one also helps you connect the business to the bigger picture, because there's no point building turnover if it never turns into personal financial progress.

If you want a sharper filter before you start calling firms, read this guide on how to find a good accountant.

Defining Your Business Accounting Needs

A WA business owner can look profitable on paper and still feel broke every month. That usually isn't a sales problem. It's an accounting setup problem.

Before you compare firms, define the job properly. If you don't, you'll hire for data entry when you need advice, or pay for tax lodgements while missing the bigger issue, which is turning business profit into personal progress.

Know the difference between the roles

Owners often throw bookkeeping, tax, and advisory into one bucket. That creates bad hiring decisions.

Here's the practical split.

| Role | Core Function | Best For |

|---|---|---|

| Bookkeeper | Records day-to-day transactions, categorises spending, reconciles accounts | Owners who need reliable books and clean records |

| Tax agent | Handles tax compliance, lodgements, and tax reporting obligations | Businesses focused on staying compliant |

| Strategic accountant | Interprets reports, advises on cash flow, forecasting, structure, and decisions | Owners who want forward-looking guidance |

Many small businesses need all three functions. They do not always need three separate providers.

What matters is whether someone on your team can do more than keep the ATO happy. A good local accountant should connect business numbers to owner outcomes. Tax, drawings, super, debt, and personal wealth do not sit in separate boxes in real life. If you're comparing providers, this is the standard to use when reviewing a Perth tax agent for small business support.

Understand cash and accrual before you hire anyone

If your accountant can't explain your reporting basis clearly, don't hire them.

The two common methods are cash and accrual accounting. Cash accounting records money when it hits the bank. Accrual accounting records income and expenses when they're earned or incurred. That choice changes how you read profit, when tax pressure shows up, and whether your reports reflect the actual trading position of the business.

A simple filter:

- Cash accounting gives a straightforward view of money in and money out.

- Accrual accounting gives a better picture once you have invoices, supplier terms, stock, or work in progress.

- Your profit number means different things depending on the method, so review it with context.

If you want to get sharper at reading operating performance, spend time mastering profit and loss statements.

What Good Bookkeeping Looks Like

Poor bookkeeping usually looks harmless at first. A few mixed transactions. Reconciliations pushed back another month. Contractor payments dumped into the wrong category. Then BAS gets harder, tax advice gets weaker, and decisions get made off numbers you shouldn't trust.

Good bookkeeping is boring in the right way. It is consistent, clean, and easy to review.

A sound workflow for an Australian small business includes:

- Separate banking first: keep business and personal spending apart

- Code transactions properly: use a chart of accounts that reflects how the business runs

- Reconcile on a set rhythm: weekly or monthly is fine, as long as it gets done properly

- Keep GST and payroll records current: don't leave compliance support to year-end cleanup

- Store the backup: invoices, receipts, loan records, and contractor details should be easy to produce

Clean books do more than reduce admin. They give you usable reports. Usable reports lead to better pricing, cleaner wage control, clearer tax planning, and better decisions about what the business can afford to pay you.

That's the point. You're not defining accounting needs so someone can tick compliance boxes. You're deciding whether your finance function will only record the past or help build wealth from the business.

How to Find and Shortlist Local WA Accountants

Once you know what you need, the search gets easier. You're no longer looking for “someone nearby”. You're looking for a shortlist of people who fit the business.

Start with sharper search terms

Don't just search accounting for small business near me and hope Google reads your mind.

Use terms that reflect your actual problem. Think “small business accountant Perth payroll”, “BAS and bookkeeping Dunsborough”, “Xero accountant WA trades”, or “tax agent for family business WA”. That filters out generic firms and brings up providers who speak to your issue directly.

Then read their websites with a sceptical eye.

Look for:

- Service clarity: Can you tell what they do beyond tax returns?

- Client fit: Do they mention businesses like yours?

- Local relevance: Do they understand WA owner-operator realities?

- Systems fluency: Are they comfortable with Xero, payroll software, and cloud workflows?

If the website is vague, the service usually is too.

Build a shortlist, not a spreadsheet of ten firms

You don't need endless options. You need two or three serious contenders.

A practical process looks like this:

- Search locally and by specialty.

- Check credentials and service mix.

- Read the language on the site. Reactive firms talk about forms. Better firms talk about decisions.

- Ask business contacts who they trust. Especially owners in a similar size or industry.

- Keep the shortlist tight. Too many options creates confusion, not quality.

If your current finance stack is messy, it can also help to review tools before you talk to firms. You can browse expense tracking solutions to get a feel for what modern workflows look like and what integrations your accountant should be comfortable with.

Read between the lines

A polished website means nothing on its own. You need signals that the firm can support a small business with moving parts.

Watch for signs of a proactive tax and compliance service, especially if you're comparing local options around Perth. If you want an example of what a more specific service page looks like, review this Perth tax agent resource and compare the level of clarity against other providers you're considering.

The right shortlist is small, specific, and based on fit. Not on who happened to rank first.

If a firm can't explain who they help, how they work, and where they add value, they probably won't become clearer after you sign up.

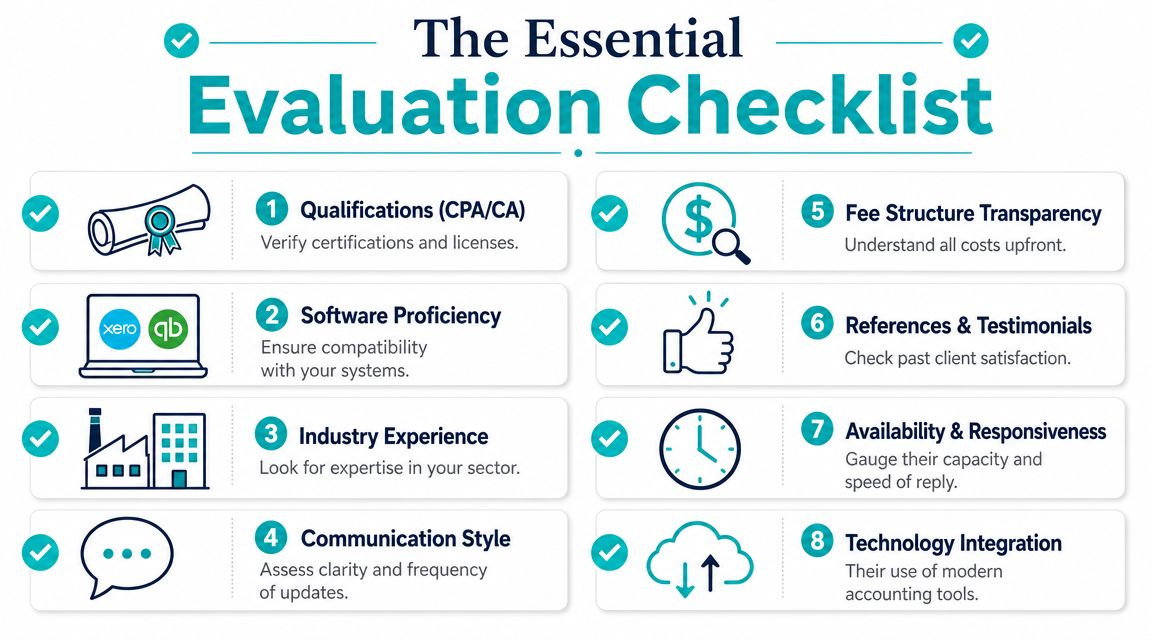

The Essential Evaluation Checklist

A WA business owner usually notices the wrong accountant too late. The BAS is lodged. The tax return is filed. Then cash gets tight, super has been underpaid, drawings are messy, and nobody has connected the business numbers to the owner's personal financial position.

That is the standard you should judge against. You are not hiring someone to keep the ATO quiet. You are choosing a financial operator who can keep the business clean, show you what the numbers mean, and help you turn business profit into personal wealth.

The Checklist That Matters

Use this checklist to separate processors from advisers.

- Check qualifications and registration: Confirm the lead adviser is a CPA or CA, and confirm the firm is properly registered to provide the tax services you need.

- Check software competence: If your business runs on Xero, MYOB, or QuickBooks, your accountant should use it well, not tolerate it.

- Check industry fit: Hospitality, construction, professional services, and retail each create different margin pressure, payroll issues, and reporting needs.

- Check communication standards: Slow replies before engagement usually become slower once you are a client.

- Check fee clarity: You should know what is included, what triggers extra fees, and how project work is priced.

- Check relevant client experience: Ask whether they work with businesses at your stage, size, and level of complexity.

- Check capacity: A good firm with no bandwidth will still give you late answers and rushed work.

- Check systems and workflow: Bank feeds, payroll platforms, digital document collection, and clear monthly processes should already be part of how they operate.

- Check strategic scope: Ask whether they only handle compliance, or whether they also advise on cash flow, entity structure, owner pay, and the gap between business profit and personal wealth.

Compliance discipline is the baseline

Payroll is one of the fastest ways for a small business to get into trouble. The ATO sets clear obligations around PAYG withholding, Single Touch Payroll, and super guarantee, and those obligations need consistent systems, not last-minute fixes, as outlined by the Australian Taxation Office guidance for employers.

A capable accountant raises those issues early. They ask who runs payroll, how super is checked, when lodgements are reviewed, and what controls are in place if someone is away.

That matters because compliance work should feed decision-making. If payroll, super, and tax are being handled properly each month, your numbers become reliable enough to use for hiring decisions, pricing, debt management, and owner distributions.

A strong accountant keeps the records clean enough to protect the business and useful enough to build wealth.

Watch what they focus on in the meeting

The best sign is where their attention goes.

A strategic accountant asks about cash movement, debt, margins, payroll process, owner drawings, GST pressure, and whether the balance sheet reflects reality. They want to know if the business is producing usable profit or just revenue with stress attached. They also ask where the business is trying to go, because structure and reporting should support that outcome.

A basic provider stays narrow. They quote on tax returns, BAS, and year-end accounts, then stop there.

For a WA owner, that is not enough. You need someone who can connect business compliance to broader financial progress. If your accountant cannot explain how the business supports your own wealth position, they are doing bookkeeping with a tax licence attached.

Key Questions to Ask in the First Meeting

You sit down with a local accountant expecting a practical conversation about your business. Ten minutes later, you have heard about software badges, turnaround times, and fixed-fee packages, but nothing about your cash pressure, your structure, or how the business is meant to build your own wealth. That meeting has already told you a lot.

Your first meeting should test judgment. You are not there to collect a brochure in human form.

Ask questions that show whether they can think beyond compliance

Skip the soft questions. Ask the ones that force a real answer.

- What do you look at first when you assess a business like mine?

- How do you help clients improve cash flow visibility and spot pressure early?

- What reports will I receive each month or quarter, and how do you explain what matters?

- How do you handle payroll, super, BAS, and year-round lodgement control?

- What problems do you see repeatedly in WA businesses at my stage?

- If you spot an issue in the numbers, what happens next?

- How do you help an owner turn business profit into personal wealth, not just taxable income?

That last question matters more than many owners realise. A decent accountant can keep you compliant. A strategic one can connect tax decisions, structure, drawings, super, and retained profits to the bigger picture. If you want that level of support, ask how they approach business advisory services for growing WA owners rather than stopping at tax returns.

Ask about the balance sheet

Profit gets attention. The balance sheet tells you whether the business is getting stronger.

The U.S. Chamber of Commerce small business finance guidance notes that a balance sheet shows assets, liabilities, and equity. That matters because those figures shape decisions around debt, working capital, and financial stability, as outlined in this small-business finance reference.

Ask it plainly:

“How do you use the balance sheet to help clients make decisions before problems show up in the P&L?”

A sharp accountant will talk about debtor blowouts, stock that is tying up cash, tax liabilities building in the background, loans that need attention, and whether retained earnings are real or just paper profit. A weak one will drift straight back to year-end tax work.

That is your signal.

Ask how they work with you as the owner

Your business numbers and your personal position are linked. Any accountant who treats them as separate conversations is leaving value on the table.

Ask how they deal with owner drawings, super contributions, trust distributions, and the line between business spending and private spending. Ask whether they help clients plan for borrowing, investment, or an eventual exit. You want someone who can explain the trade-offs clearly and tell you what to do next, not someone who waits for June and starts talking deductions.

Fees matter. Judgment matters more.

You still need to understand the pricing model. Ask what is included, what triggers extra fees, how often you will meet, and who does the work.

Then make the call. Are they giving you clean answers, commercial insight, and a clear link between compliance and wealth creation? Or are they selling low-friction admin with a tax return attached?

The wrong accountant can look affordable for a year and expensive for the next five.

Beyond the Books When to Engage a Financial Adviser

You can run a solid business for years and still end up with a weak personal balance sheet.

That happens all the time in WA. The BAS gets lodged, the tax gets managed, and the business keeps trading, but no one has tied those decisions to your super, your family protection, your debt position, or your exit plan. Profit alone does not build wealth. A joined-up plan does.

Where accounting ends and broader advice starts

Your accountant should keep the business clean, compliant, and tax-aware. A financial adviser should help you turn the results of that business into personal financial progress.

The line matters because the decisions overlap. Business structure affects how profits come out. Super contributions affect tax and retirement outcomes. Insurance affects whether your family can hold the line if you are out of action. Exit planning affects what the business is worth and what you keep. The Australian Securities and Investments Commission makes the distinction clear through its guidance on what financial advisers do and when advice moves into regulated personal financial advice.

A good owner asks sharper questions than “Is the tax sorted?”

Ask these instead:

- How much of this year's profit should stay in the business, and how much should come out?

- Am I building retirement wealth on purpose, or leaving it to chance?

- If I get sick or die, what happens to the business, the debt, and my family's income?

- Am I creating a business someone can buy, or just a job that depends on me?

Bring in advice before the pressure hits

Owners usually wait too long. They call for advice when cash is tight, a partner wants out, a lender wants answers, or they are two years from wanting to sell and have done no preparation.

That is backwards.

Bring in broader business advisory services while the business is stable enough to give you options. That is when you can set profit distribution rules, build super properly, review ownership structures, protect key risks, and shape an exit on your terms instead of under pressure.

A business can produce good income and still leave the owner exposed, underfunded for retirement, and too dependent on future sale proceeds.

If your accountant is handling compliance well, keep them. Then add advice that connects the business to your personal wealth plan. That is how a WA business owner stops treating accounting as a yearly obligation and starts using it to build long-term financial control.

If you want help connecting business performance to your personal financial future, book an introductory call with Wealth Collective. We help WA business owners turn compliance, cash flow, super, protection, and long-term planning into one clear strategy.