Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Division 293 tax is an extra 15% tax on super contributions for high-income earners. Many successful Australians get caught by surprise because the income calculation is broader than they expect, and the tax can apply once your combined Division 293 income and concessional contributions go over $250,000.

You might be in that group right now. Your salary looks straightforward, your super contributions seem sensible, and then the ATO issues a notice for a tax you didn't know existed. That surprise usually isn't caused by reckless planning. It's caused by a rule that looks simple from a distance and turns out to have a few expensive traps once real life gets involved.

The Surprise Tax Bill You Did Not Expect

You finish a strong financial year. Salary is up, employer super has been paid, and you may have added salary sacrifice contributions because that seemed like the sensible long-term move. Months later, an ATO notice arrives for a tax you never factored in.

That moment catches high-income professionals off guard for a simple reason. Division 293 is often discovered after the year has ended, when the choices that triggered it have already been made.

The questions come quickly. Why is there extra tax on super? Weren't concessional contributions already taxed? Why did this only show up now?

Why the bill feels so unexpected

Part of the surprise is timing. Part of it is visibility.

The ATO works out Division 293 after it pulls together your tax return information and the reporting from your super fund, then issues an assessment under that process, as explained on the ATO's Division 293 overview. By then, the financial year is over and your opportunity to reshape contributions, manage cash flow, or prepare for the liability is much smaller.

That delay matters. A tax is easier to handle when you can see it forming in advance. It feels far more confronting when it arrives as a retrospective bill tied to decisions that looked harmless at the time.

Discovery of Division 293 often happens reactively, not during planning. That is one of the reasons it creates so much frustration.

Why smart earners still get caught

This is rarely about careless behaviour. It is usually about hidden inputs.

A person may look only at salary and conclude they are safely under the threshold. Then a broader income item, an extra concessional contribution, or a one-off event changes the result. The trap is not the idea of paying more tax. The trap is misunderstanding what the ATO counts and when the bill will appear.

That is also why the shock can feel similar to other delayed tax obligations. If you have ever seen how tax can be assessed after a profitable period, Action Accountants' payments on account guide shows the same broader pattern. Income is earned first, and the cash flow impact can follow later.

For readers also trying to make sense of how super is taxed at different stages, our guide on whether you get taxed on superannuation helps place Division 293 in the bigger picture.

Beyond the notice itself

The dollar amount matters. The more useful question is what the notice says about your planning.

In practice, it often points to one of four blind spots:

- Income that was broader than you expected

- A salary sacrifice strategy that changed the tax outcome

- A one-off event that pushed you over the line

- A payment decision that could affect long-term retirement savings

That last point is easy to underestimate. Paying the assessment from super may preserve personal cash flow today, but it can also leave less money invested for your future. Paying it personally may protect your super balance, but it changes your short-term cash position. Small decisions here can have a long tail.

That is why Division 293 deserves more than a quick reaction once the notice arrives. With the right advice, it becomes a rule to plan around. Without that guidance, it remains one of those taxes that catches capable, organised people because the costly parts were never explained clearly enough.

What Is Division 293 Tax and Who Pays It

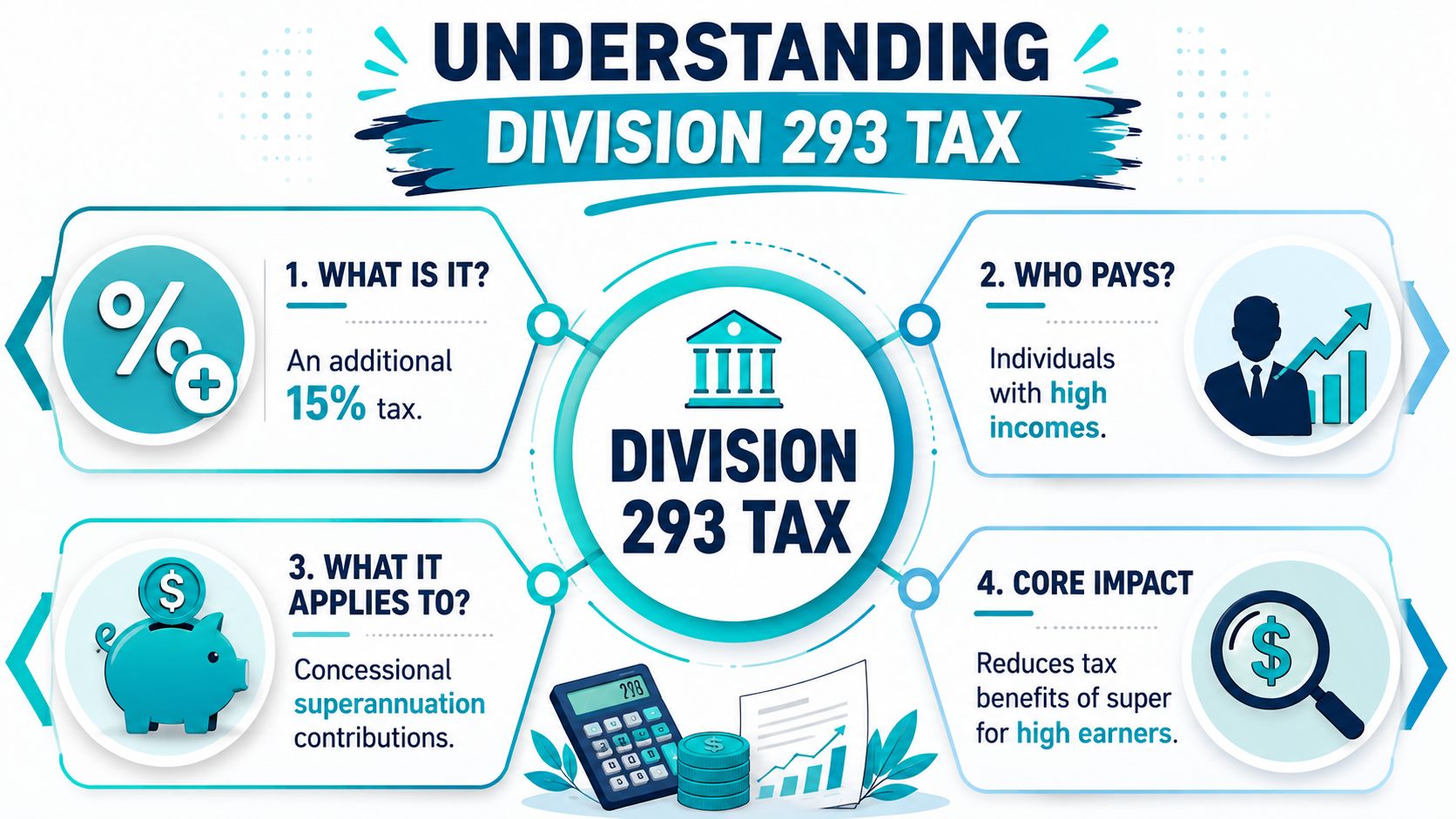

Division 293 is an extra tax on concessional super contributions for higher-income earners. The purpose is to trim back the tax advantage of super once your income reaches a certain level.

If your combined Division 293 income and concessional contributions are more than $250,000 for the financial year, an additional 15% tax can apply to some or all of those concessional contributions. In practical terms, contributions that were already taxed at 15% inside super can end up taxed at 30% overall.

The threshold is only part of the story

A common and costly misunderstanding is treating the $250,000 threshold as a salary test.

It is broader than that. The ATO uses a wider income measure for Division 293, so your base pay is only one part of the picture. Reportable fringe benefits, net investment losses, and some trust distribution amounts can all affect the result. The ATO sets out that broader definition in its Division 293 tax guide for high-income earners.

That catches people off guard. Someone can look comfortably under the line based on salary alone, then find that other items in their tax return push them into Division 293 territory.

What counts in the income mix

A useful way to view Division 293 income is as a wider lens than your payslip. Your employment income matters, but the tax rule also looks at other amounts that affect your overall financial position.

These amounts commonly matter:

- Taxable income. Salary, wages, bonuses, and other taxable earnings.

- Reportable fringe benefits. Salary packaging arrangements can increase your Division 293 income even if they do not feel like take-home pay.

- Net investment losses. Losses from a rental property or other investments can still change the calculation.

- Some trust-related amounts. Family or discretionary trust distributions can be relevant.

If you want the broader context first, our guide to how superannuation is taxed in Australia can help place Division 293 in the bigger super tax picture.

Practical rule: If your finances include salary packaging, an investment property, trust distributions, or personal deductible super contributions, do not estimate Division 293 using salary alone.

Who usually gets caught

Division 293 does not only affect someone on a very high fixed salary.

It often shows up for people whose income moves around or whose tax position is more layered than it first appears.

Employees with bonuses or variable remuneration

A strong year, deferred payment, or one-off bonus can tip the combined figure over the threshold.Professionals with investment income or losses

Property losses and trust distributions often create the gap between what someone thinks counts and what the ATO counts.People making concessional contributions strategically

Salary sacrifice or deductible personal contributions can still be worthwhile, but they can also increase the amount exposed to Division 293.

The important point is not just who pays it. It is why the bill often feels unexpected. The misunderstanding usually starts with the income definition, then gets more expensive if no one steps back and considers the longer-term effect of the payment choices that follow. That is where good advice earns its keep. It helps you spot the trigger early, weigh the trade-offs properly, and avoid treating Division 293 as a surprise instead of a planning issue.

How Your Division 293 Tax Is Calculated

The calculation is more mechanical than many people expect. The surprise usually comes from what gets counted, not from complicated maths.

Division 293 adds an extra 15% tax to the lower of these two amounts:

- the amount by which your Division 293 income plus concessional contributions exceeds $250,000

- your total concessional contributions

That lower-amount rule matters. It is why two people can both cross the threshold and still end up with very different tax bills.

A practical way to work it out

Start with the full combined figure, not just your salary. That is one of the most expensive misunderstandings people make.

- Add your Division 293 income and your concessional contributions.

- Calculate how much that total is above $250,000.

- Compare that excess amount with your concessional contributions.

- Apply 15% to whichever figure is lower.

If part of your strategy includes salary sacrifice, it helps to know exactly which amounts flow into concessional contributions. Our guide to salary sacrifice super contributions explains how those payments are treated.

Division 293 Tax Calculation Example 2026

| Metric | Scenario A High Income | Scenario B Borderline Income |

|---|---|---|

| Division 293 income | $260,000 | $240,000 |

| Concessional contributions | $20,000 | $20,000 |

| Combined total | $280,000 | $260,000 |

| Amount above $250,000 | $30,000 | $10,000 |

| Lesser amount | $20,000 | $10,000 |

| Division 293 tax at 15% | $3,000 | $1,500 |

What Scenario A tells you

In Scenario A, the person is already above the threshold before contributions are added. Once their concessional contributions are included, the excess over $250,000 is $30,000.

Their concessional contributions are $20,000, which is the lower of the two figures. So the extra tax applies to the full $20,000, producing a $3,000 Division 293 liability.

This is the version people usually expect. Higher income means all concessional contributions can be exposed to the extra 15%.

What Scenario B tells you

Scenario B is where people often get caught.

A Division 293 income of $240,000 can look comfortably under the line if you focus on taxable income alone. But after adding $20,000 of concessional contributions, the combined figure becomes $260,000. That is $10,000 over the threshold.

Because the tax applies to the lower amount, only $10,000 is taxed at the extra 15%. The result is a $1,500 bill, not tax on the full $20,000 of contributions.

That small detail changes the result materially.

Where people get the maths wrong

The same mistakes come up again and again:

- Using salary instead of the broader income test. Bonuses, investment-related amounts, reportable fringe benefits, and some other items can change the result.

- Assuming all concessional contributions are taxed every time. That only happens if the excess above $250,000 is greater than your concessional contributions.

- Treating the threshold as a cliff. Going slightly over does not automatically expose every concessional dollar.

- Stopping at the calculation itself. How you respond to the assessment can affect your super balance over time, which is why advice often matters more than the formula.

The formula itself is straightforward. The trap is that many people apply it to the wrong income figure, or they treat a one-year tax bill as a minor annoyance without considering the long-term cost of how they choose to pay it.

Handled properly, Division 293 is usually a planning issue. Handled casually, it becomes an avoidable drag on your retirement savings.

Your Assessment Arrived What Happens Next

You open an ATO letter expecting routine paperwork and find an extra tax bill instead. For many high-income earners, that is the first time Division 293 feels real.

The next decision matters more than the envelope suggests. You are not only dealing with an amount owing. You are deciding whether to pay it from cash outside super or have money released from super, and that choice can shape your retirement balance long after this year's bill is forgotten.

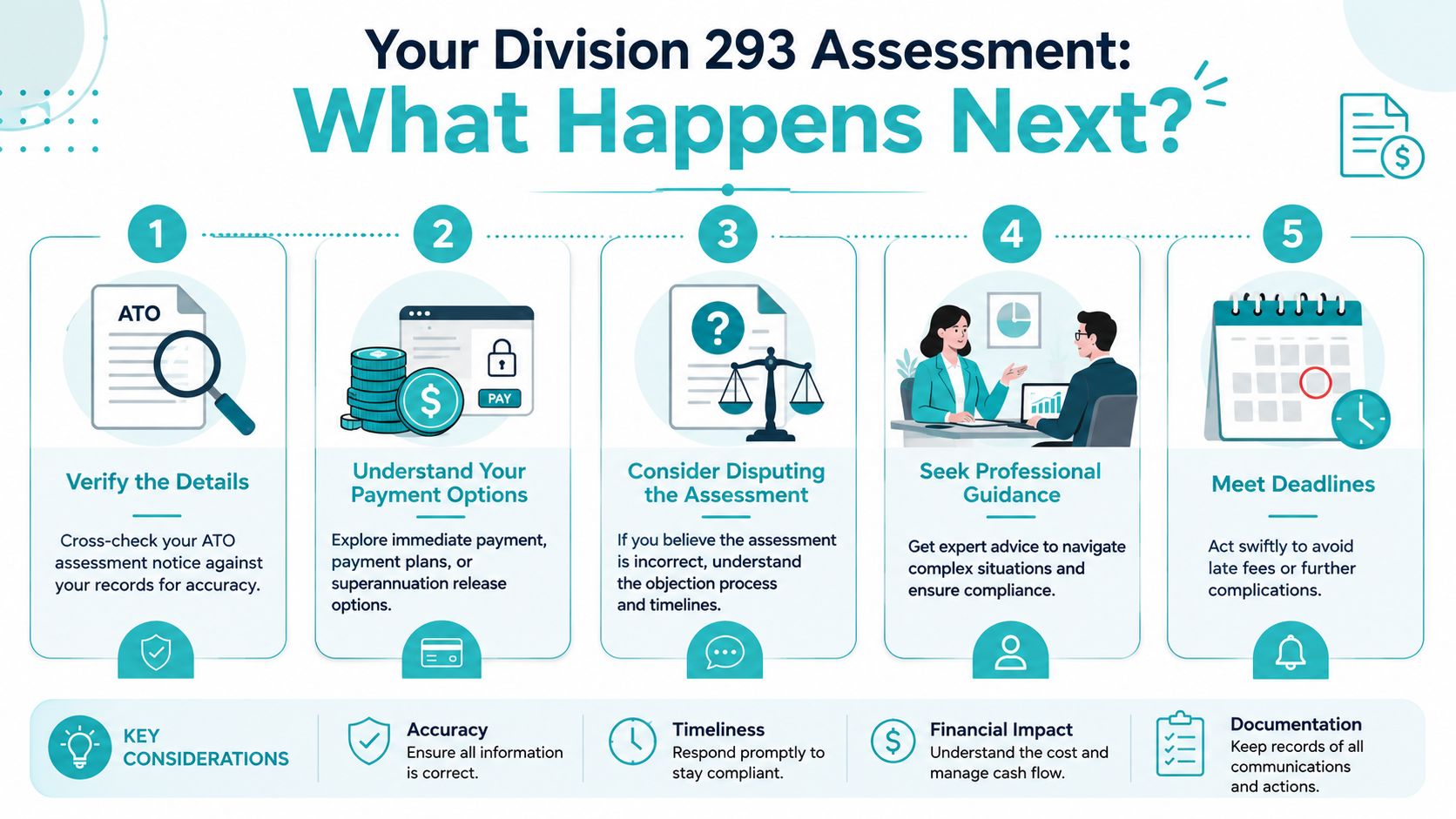

Start with the assessment itself

Before choosing how to pay, check what the ATO has assessed.

A Division 293 assessment is based on your lodged tax return and the contribution information reported by your super fund. If you want the ATO to release money from super to cover the liability, there is generally a 60-day window from the date on the notice to make that election through the ATO process.

That sounds administrative. It is really a review point.

Go through the notice with three questions in mind:

- Does the income figure match what you expected? The broad income definition catches people who only focused on salary.

- Do the concessional contributions line up with your records? Employer contributions, salary sacrifice amounts, and other concessional contributions need to match fund reporting.

- Was there a one-off event this year? A capital gain, bonus, or other irregular amount can explain why the assessment appeared in a year that otherwise looked ordinary.

This is one of the costliest misunderstandings with Division 293. People often assume the bill means something has gone wrong. Often, the rule has worked exactly as designed, but against a broader income figure than they had in mind.

Your two payment options

Once the assessment is correct, the practical choice is straightforward. The long-term effect is less obvious.

Pay it from personal cash

Paying from your bank account leaves your super balance intact. Your cash flow takes the hit now, but the money inside super stays invested.

For many people, this is the cleaner long-term option, especially if preserving retirement savings is a priority.

Release the money from super

You can elect to have the liability paid from your super. That can feel easier because it protects cash on hand today.

The trade-off is that the released amount stops compounding inside the concessionally taxed super environment. A smaller super balance today can mean a noticeably smaller balance years later, even when the original tax bill looked manageable.

A small withdrawal now can work like removing a brick from the base of a wall. One brick does not look dramatic on its own, but everything built on top of it is now smaller.

Why the election window deserves more thought

The 60-day period is enough time to choose. It is not much time to think clearly if the letter catches you off guard.

That is why this step is often underestimated. The common mistake is treating the assessment as a payment task instead of a planning decision. If cash flow is tight this year, releasing funds from super may still be the right move. But it should be a conscious trade-off, not an automatic reaction.

This is also a good point to review whether your broader contribution strategy still fits. In some cases, future years may be managed better by reviewing timing, income spikes, and the use of tools such as carry-forward concessional contribution rules.

A practical way to compare the two

| Consideration | Pay personally | Release from super |

|---|---|---|

| Immediate cash flow | Reduces cash on hand | Preserves cash on hand |

| Impact on super balance | Keeps balance invested | Lowers the amount invested |

| Long-term retirement effect | Usually lower | Can be higher because future earnings are lost |

| Behavioural risk | Feels painful now | Can feel easier than it really is |

The right answer depends on your income, liquidity, mortgage position, investment structure, and retirement time horizon.

Good advice earns its place. A Division 293 assessment can look like a simple tax notice, but the expensive mistakes usually come from misunderstanding the income test or underestimating what one payment choice does to long-term wealth.

Proactive Strategies for Managing Division 293 Tax

The most efficient way to deal with Division 293 is to treat it as a planning variable before the financial year closes.

For many high-income earners, the expensive mistake is not the tax itself. It is misreading what counts toward the threshold, or making contribution decisions in isolation and only discovering the full picture after the year has ended.

Start with the right dashboard

A good review brings the moving parts onto one page. Salary is only one dial.

You also need to look at taxable income, reportable fringe benefits, net investment losses, and concessional contributions together. If those items sit in separate conversations with payroll, your accountant, and your super fund, Division 293 can arrive like a problem that appeared out of nowhere. In reality, the signals were there. They just were not being read together.

That broader view matters most for people who assume they are safely under the line based on base salary alone.

Four planning moves that reduce expensive surprises

Watch one-off income before it lands

A capital gain, bonus, employment termination amount, or other unusual income event can change the result quickly.

Sometimes Division 293 will still apply. The benefit of planning is not always avoiding it. The benefit is knowing early enough to adjust contributions, prepare cash flow, and avoid making rushed decisions later.

Review salary sacrifice with the full tax picture in view

Salary sacrifice can still make sense. But near the threshold, an extra concessional contribution should be tested against the likely after-tax outcome, not judged on the contribution tax rate alone.

Many individuals often overlook this point. They focus on the first tax saving and miss the second layer that follows. That does not make concessional contributions wrong. It means the strategy needs context.

Use the right contribution mix for the year you are actually having

Some high-income earners keep adding to concessional contributions because that strategy has worked well in prior years. But a year with a gain, bonus, or other spike may call for a different mix.

If unused cap amounts might be part of that decision, our guide to carry forward concessional contributions explains when using earlier cap space may help and when it can create a larger-than-expected tax outcome.

Decide how you would pay before the notice arrives

Paying personally versus releasing money from super is not just an admin choice. It is a trade-off between today's cash flow and tomorrow's retirement balance.

Super works like a long-term compounding engine. Money left inside it has more time to earn on itself. Pulling funds out to cover a tax bill may feel easier in the moment, but the true cost is the future growth that money no longer gets to earn. For someone with many years to retirement, that gap can matter more than the notice itself.

Good tax planning is not only about reducing tax. It is about avoiding poor decisions made under time pressure.

What proactive planning actually improves

Handled well, this kind of planning changes three things:

- Fewer surprises: You are more likely to spot risk before the ATO assessment arrives.

- Better contribution decisions: You can judge concessional contributions with the full income picture in view.

- Stronger long-term outcomes: You are less likely to solve a short-term cash issue by weakening a long-term retirement asset.

The goal is rarely to avoid Division 293 at all costs. The better goal is to stop it from distorting the rest of your strategy.

That is usually where professional advice pays for itself. The rule is not hard because the formula is mysterious. It is hard because income is defined more broadly than many people expect, and because the way you choose to pay can affect your wealth long after the tax year is over.

Turn Tax Complexity into Financial Clarity

A lot of Division 293 mistakes happen to capable, high-income professionals who assume they already understand the rule. Then a tax notice lands, and they realise the actual trap was never the formula. It was the gaps in how they defined income, timed contributions, or judged the long-term cost of paying the bill the wrong way.

Division 293 often works like a second layer of interpretation sitting on top of your normal tax thinking. What looks straightforward on a payslip can look very different once salary sacrifice, reportable fringe benefits, investment income, and super contributions are viewed together. That is why smart people still get caught. They are using the wrong map.

Good advice helps before the mistake gets expensive. An adviser can pressure-test the assumptions that usually cause trouble. Which income items are easy to overlook. Whether extra concessional contributions still make sense in your position. Whether paying personally protects your retirement balance better than releasing money from super, or whether cash flow points the other way.

Those choices shape more than one tax year.

Handled well, Division 293 becomes a planning issue you can account for early, rather than a surprise that pushes you into a rushed decision. That shift matters because the costly part is often not the tax itself. It is the knock-on effect on contribution strategy, cash reserves, and long-term compounding inside super.

If you want help making sense of how Division 293 fits into your broader super, tax and retirement strategy, book an introductory call with Wealth Collective. A short conversation can help you understand where the traps are, what needs reviewing, and how to turn a reactive tax issue into a clear financial plan.