Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Your fixed rate is ending. Or you've spotted lenders advertising rates that look far better than the one you're paying now. You're wondering if you should refinance, but you're also thinking about paperwork, fees, timing, and whether it's even worth the hassle.

That's the right question.

Refinancing isn't something you do because a bank ad tells you to. You do it when the numbers, your life stage, and your longer-term plan all line up. Get it right, and the upside can be meaningful. According to the ACCC, refinancing a $250,000 home loan can save a borrower up to $1,400 in the first year and over $17,000 over the loan's lifetime (ACCC figure cited here).

The mistake I see most often is simple. People wait too long because they assume their current lender will “look after them”, or they jump too quickly because they've seen a lower headline rate without checking costs, structure, or whether the loan still suits the way they use money.

If you're trying to work out when to refinance mortgage debt in Australia, don't treat it like a rate-shopping exercise only. Treat it like a strategy decision.

Is Now the Right Time to Refinance Your Mortgage

A common scenario goes like this. A couple has been on a fixed rate for a while. The fixed term is about to expire, the repayment shock is staring them in the face, and they've started comparing their current loan with what new customers are getting. They're not in financial trouble, but they can see the gap widening and they don't want to keep paying a premium out of habit.

That's often the moment a proper mortgage review should happen.

The best refinance decisions usually don't come from panic. They come from noticing a trigger early, checking the numbers, and choosing the option that supports the rest of your financial life. If you're weighing up whether your next structure should prioritise certainty or flexibility, it also helps to understand the trade-offs between fixed and variable rates.

The question to ask first

Don't start with “Can I get a lower rate?”

Start with this. “Is my current loan still competitive and still fit for purpose?”

Those are different questions. A loan can have a decent rate and still be wrong for you because it lacks features you need. It can also have the features you want while charging more than it should.

Practical rule: A mortgage review makes sense when your current loan no longer matches both your cash flow needs and the market available to someone in your position.

What makes this decision urgent

If your fixed rate is ending, you're approaching a natural decision point. If you've had the same lender for years without a review, that's another. If your income has changed, your equity has improved, or your goals have shifted from “get into the market” to “reduce debt faster”, your mortgage should change with you.

The point isn't to refinance for the sake of movement. The point is to stop overpaying or carrying the wrong structure just because you've been busy.

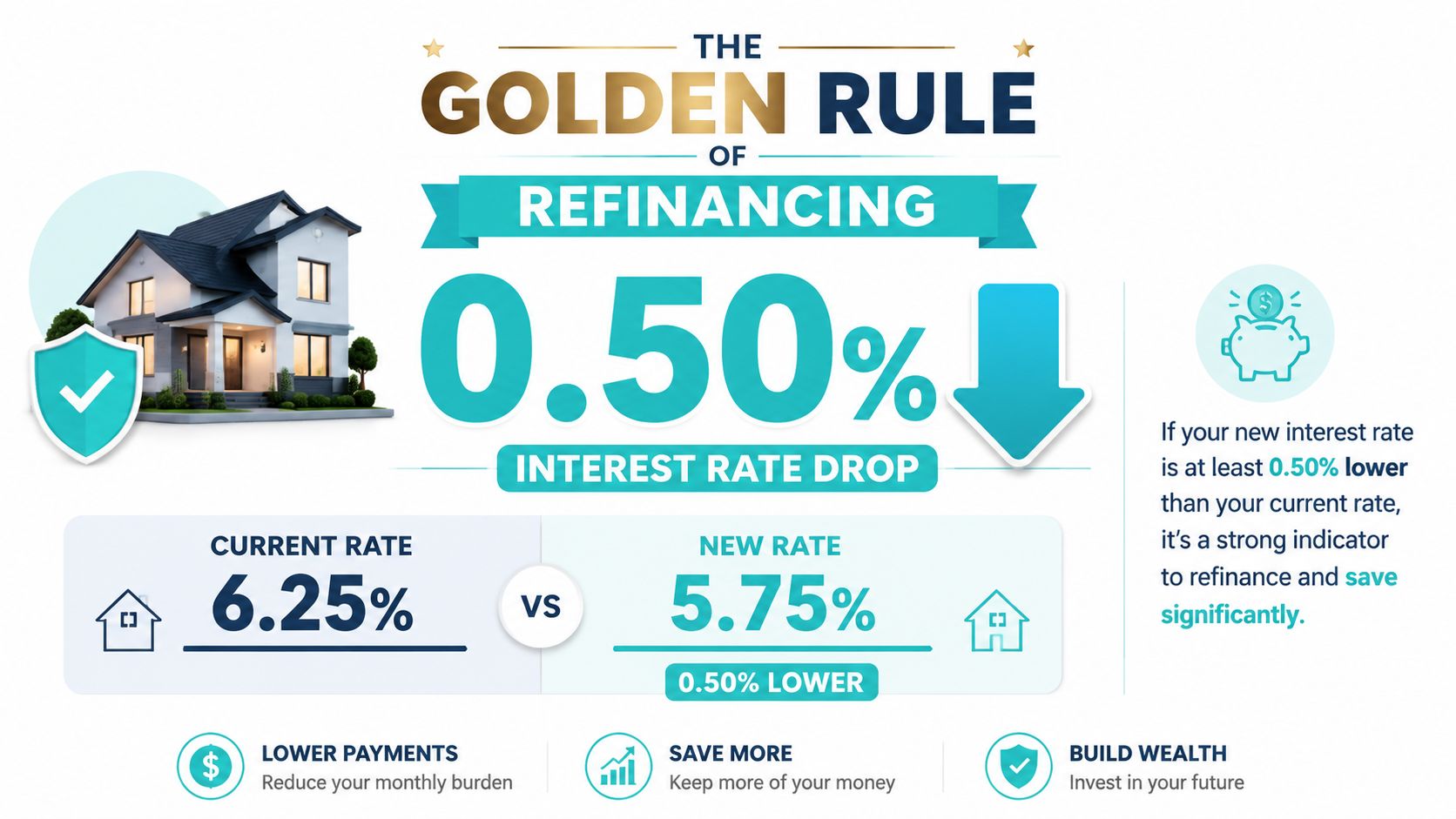

The Golden Rule of Refinancing

There's one benchmark I want most borrowers to remember. If the new rate is at least 0.50% lower than your current rate, refinancing is often worth serious attention.

In Australia, refinancing is typically financially justified when the interest rate differential is at least 0.50% or more, because that level usually means the savings outweigh switching costs. One example often used is that a 0.50% reduction on a $700,000 loan saves about $3,500 per year (Australian refinance guide reference).

Why the 0.50% rule matters

Think about it like changing electricity providers. You don't switch because the bill is a tiny bit lower. You switch when the savings are clear enough to justify the effort.

Mortgages work the same way. A very small rate difference can disappear once you factor in discharge fees, registration costs, legal fees, and your time. A meaningful rate gap usually gives you room to absorb the switching costs and still come out ahead.

How to use the rule properly

Use the 0.50% rule as a filter, not as the final answer.

Ask yourself:

- Current gap: Is the rate you can qualify for at least 0.50% lower than what you're paying now?

- Loan size: Is your balance large enough for that gap to produce real savings?

- Time horizon: Will you stay with the property and loan long enough to benefit?

- Structure fit: Does the new loan improve more than just the headline rate?

A cheap loan that traps your cash flow or removes useful features isn't automatically a better loan.

Many people stumble here. They chase the advertised rate, then realise the product doesn't suit their repayment habits, offset strategy, or broader debt reduction plan. The right move isn't just a cheaper loan. It's a loan that improves your position in a way you will use.

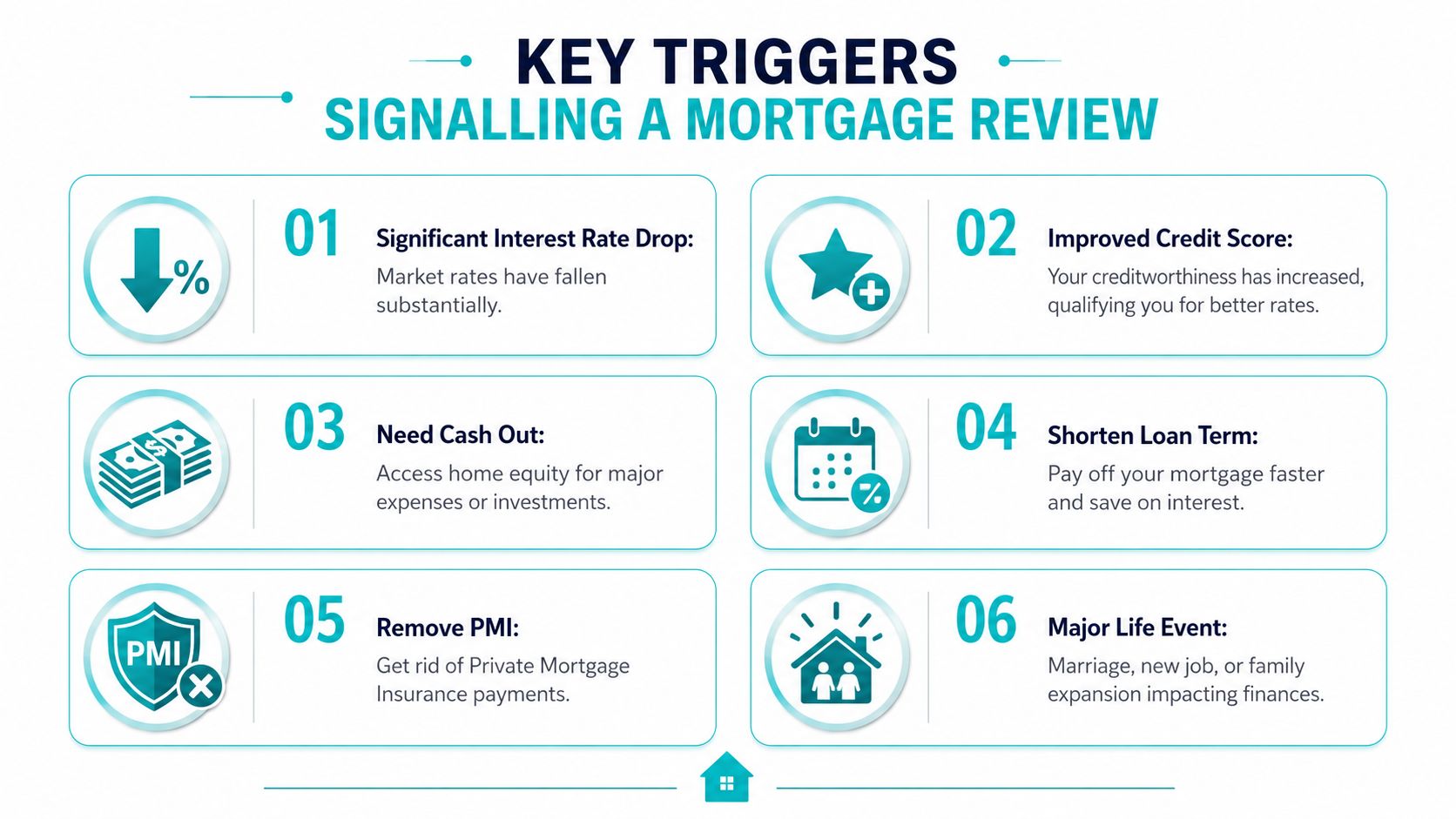

Key Triggers Signalling a Mortgage Review

Borrowers rarely refinance because they wake up feeling inspired to compare lenders. They refinance because something changes. The trigger can come from the market, from the loan itself, or from your own life.

The market trigger is obvious. Australian Bureau of Statistics data showed refinancing between lenders reached a record $20.2 billion in June 2023, which was a 12.6% increase compared with the previous year as borrowers responded to rate volatility (ABS media release). When rates move sharply, borrowers who review their loan early usually have more options than those who wait until repayments are already hurting.

Loan events that should put you on alert

Some mortgage moments should always trigger a review.

- Fixed rate ending: This is the classic one. Many borrowers roll straight onto a higher variable rate and do nothing for months.

- Interest-only period finishing: Your repayment structure changes, which can alter cash flow fast.

- You've had the same loan for years: Familiarity isn't a strategy. A stale loan often costs more than people realise.

- Your lender won't budge: If you ask for a review and get a weak response, that tells you something.

Life changes matter just as much

The right time to refinance mortgage debt often has less to do with lenders and more to do with your own circumstances.

A few examples:

- Income has improved: A promotion, a new role, or stronger household income can improve borrowing strength and flexibility.

- You want to consolidate debt: Folding expensive non-mortgage debt into a better-structured home loan can improve cash flow, but only if it's done with discipline.

- You want to renovate or invest: Accessing equity can be sensible when it serves a defined plan, not impulse spending.

- You're focused on retirement: If your goal has shifted to clearing debt faster, your loan should support that.

Review your mortgage when your life changes, not only when the Reserve Bank gets the headlines.

Service and features are valid reasons too

A mortgage isn't only an interest rate. It's a working tool. If your loan lacks an offset account, has clunky online access, poor redraw rules, or a lender that's hard to deal with, those frictions matter. They affect how well the loan performs in real life.

If your finances have become more complex than the loan you took out years ago, that's your signal.

The Refinancing Eligibility Checklist

Before you spend time comparing rates, check whether you're in a strong refinancing position. Lenders don't assess your loan the way you do. They look at risk, equity, repayment capacity, and conduct.

The big checkpoint is equity. Most Australian lenders prefer borrowers to have at least 20% equity in their home, which means an LVR of 80% or less, because that usually opens the door to stronger refinance options and helps avoid Lenders Mortgage Insurance (Australian refinancing eligibility guide).

Your lender-readiness checklist

Run through this thoroughly.

- Equity position: If your LVR is at or below 80%, you're generally in a better position. If it's higher, refinancing may still be possible, but your choices can narrow.

- Income stability: Lenders want to see that your income is reliable and supports the new repayments.

- Credit conduct: Clean repayment history matters. Missed payments make lenders nervous fast.

- Existing debts: Credit cards, car loans, and personal debt affect serviceability.

- Property suitability: Some properties are easier for lenders to assess than others.

What to do if you're not ready yet

Not every borrower should refinance right now. That's not failure. It just means the sequencing matters.

If your equity is thin, focus on reducing the balance and letting time do some work. If your credit file has issues, clean up conduct before you apply. If your income is in transition, it may be smarter to wait until your position is easier to verify.

Reality check: The best refinance deal on the market is irrelevant if you can't qualify for it.

Borrowers waste energy comparing products before confirming they meet lender expectations. Start with your position first. Then compare options.

How to Calculate Your Break-Even Point

This is the step that stops emotional decision-making.

Refinancing only makes sense when the savings recover the costs in a reasonable timeframe. In Australia, typical refinancing costs range from $650 to $1,450, and one worked example shows that a $1,650 total cost divided by $405 monthly savings gives a break-even point of just over 4 months (break-even refinance guide). The same source notes that valuation fees are often waived for refinances.

The formula

The formula is simple:

Break-even months = Total refinance costs ÷ Monthly savings

If the break-even point is short and you expect to keep the property and loan beyond that point, refinancing is usually worth a closer look.

What goes into the cost side

Start by adding up the switching costs. Common items include:

- Discharge fee: Charged by your current lender

- Settlement or legal fees: Administrative costs for the new loan

- Government registration fees: Costs attached to mortgage and title registration

- Other lender charges: Depending on the product and lender

- Fixed-rate break costs: If you're leaving a fixed loan early, this can change the entire decision

If you use an offset account heavily, also compare how the new loan handles that feature. You can test the impact with an offset account calculator.

Sample Break-Even Calculation

| Item | Cost/Saving |

|---|---|

| Total refinance costs | $1,650 |

| Monthly savings | $405 |

| Break-even point | Just over 4 months |

How to judge the result

The calculation is only useful if you interpret it properly.

A short break-even period is attractive. But if you plan to sell soon, restructure again, or your goals are shifting rapidly, even a mathematically sound refinance might not be the best move. On the other hand, if you expect to stay put and the break-even point is reached quickly, every month after that improves your position.

The smartest borrowers don't stop at “Will I save?” They ask, “Will this saving still matter after costs, over time, and in the context of what I'm trying to do next?”

Strategic Scenarios Tailored to Your Life Stage

The right answer changes with your stage of life. A young professional trying to free up cash flow has different priorities from a pre-retiree who wants debt gone before work income stops.

Young professionals and dual-income households

If you're earlier in the wealth-building phase, refinancing can be a lever. Not just a cost-cutting move.

You might be looking to simplify debt, improve monthly cash flow, or build a structure that helps you get ahead rather than just stay afloat. In that situation, the key question isn't “What's the cheapest rate?” It's “Does this loan help me direct more money to the right places?” For some borrowers, that means a sharper repayment plan. For others, it means flexibility and a clear route for how to pay off your mortgage early.

A practical checklist for this group:

- Cash flow pressure: Will the refinance make your monthly budget easier to manage?

- Debt clean-up: Are you using the change to become more disciplined, or just to reshuffle debt?

- Feature use: Will you utilize redraw or offset features if they're included?

- Next goal: Does this help with investing, family planning, or buying your next property?

Pre-retirees who need a cleaner path

Pre-retirees need to be more careful. Closing costs, timing, and loan structure matter more when you're focused on retirement readiness than when you're chasing a lower repayment.

I'm opinionated here: Don't switch lenders first. Negotiate first.

Government guidance from MoneySmart says borrowers should “Ask your current lender for a better deal first” before switching (MoneySmart guidance on switching home loans). That advice is better than most generic refinance content because it acknowledges something practical. If your current lender will sharpen your rate enough, you may avoid unnecessary switching costs and paperwork.

Ask your current lender for a better deal before you do anything else.

That's especially useful if your equity is tighter than you'd like, you want minimal disruption, or you're close enough to retirement that preserving simplicity matters. If your broader objective includes reducing housing costs later in life, it's also worth understanding resources on making the most of property through downsizing, because refinancing and downsizing often sit inside the same retirement planning conversation.

A pre-retiree checklist should focus on different issues:

- Debt runway: Will this move help you reach retirement with less mortgage stress?

- Switching friction: Can the existing lender solve the problem without a full refinance?

- Equity access: Are you trying to access equity for a clear purpose, or reacting to pressure?

- Simplicity: Will the new arrangement be easier to manage in later years?

Your Next Step A Smarter Mortgage Strategy

When to refinance mortgage debt comes down to four things. A real trigger. A solid eligibility position. A break-even point that makes sense. A loan structure that supports where your life is heading.

Miss one of those, and the decision can still be wrong even if the headline rate looks good.

This is why I don't like blanket advice. “Always refinance when rates drop” is lazy. “Never refinance because fees are too high” is just as bad. Good mortgage decisions are specific. They depend on your equity, your income, your plans for the property, your debt habits, and whether your current lender is willing to compete for your business.

If you're nearing the end of a fixed rate, carrying a loan you haven't reviewed in years, or trying to line up your mortgage with a bigger goal like debt reduction or retirement, don't guess. Check the numbers. Push your current lender first. Then compare alternatives with a clear head.

The best loan isn't the one with the loudest marketing. It's the one that subtly improves your financial life for years.

If you want help turning this into a personalized strategy, speak with Wealth Collective. A free, no-obligation 10-minute call can help you decide whether to negotiate with your lender, refinance, or leave your current loan alone. It's a simple way to get clarity before making a decision that can affect your cash flow, debt timeline, and retirement plans.