Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You've got money sitting in savings, a home loan ticking along, and a nagging sense that those two things should be working together better than they are. That's where a Mortgage Offset Account Calculator becomes useful. It gives shape to a question many borrowers in Perth, Dunsborough, and across Australia ask at some point: if I keep cash available instead of tipping it straight into the loan, am I still making progress?

For a lot of households, the answer is yes, but only if the structure matches the way money actually moves through the month. A calculator helps you test that before you make changes. More importantly, it helps you move from vague optimism to a practical decision.

Is Your Money Working as Hard as You Are

A common situation looks like this. A couple has built a solid savings buffer. Their mortgage repayments are under control. One salary lands regularly, the other varies a bit, and they're trying to decide whether to leave cash in savings, make extra repayments, or link their day-to-day banking more closely to the home loan.

That's the moment an offset account usually enters the conversation.

An offset account can be powerful, but it's often misunderstood because people treat it like a generic savings feature. It isn't. Used well, it becomes part of how you manage income, bills, buffers, and debt reduction together. Used poorly, it's just another account with money drifting in and out and no clear purpose.

Why the calculator matters early

A Mortgage Offset Account Calculator is a good first filter because it answers the practical question many borrowers have: what difference could this make if used properly?

It also helps expose gaps in the plan. If your result looks underwhelming, that doesn't always mean the strategy is poor. Sometimes it means your offset balance won't stay high for long enough, or your cash flow setup needs work first. That's why getting the basics of cash flow management right often matters just as much as having the offset itself.

Practical rule: An offset account works best when your everyday banking habits support it. The account structure and the spending pattern need to match.

We've seen borrowers get the biggest benefit when they stop treating the offset as a passive feature and start treating it as an active money hub. Salary goes in. Bills come out intentionally. Spare cash stays parked as long as possible. The calculator gives you the first hint of what that discipline could achieve.

By the end of the process, the true value isn't just the estimate. It's knowing whether the offset fits your financial life, not just your loan product.

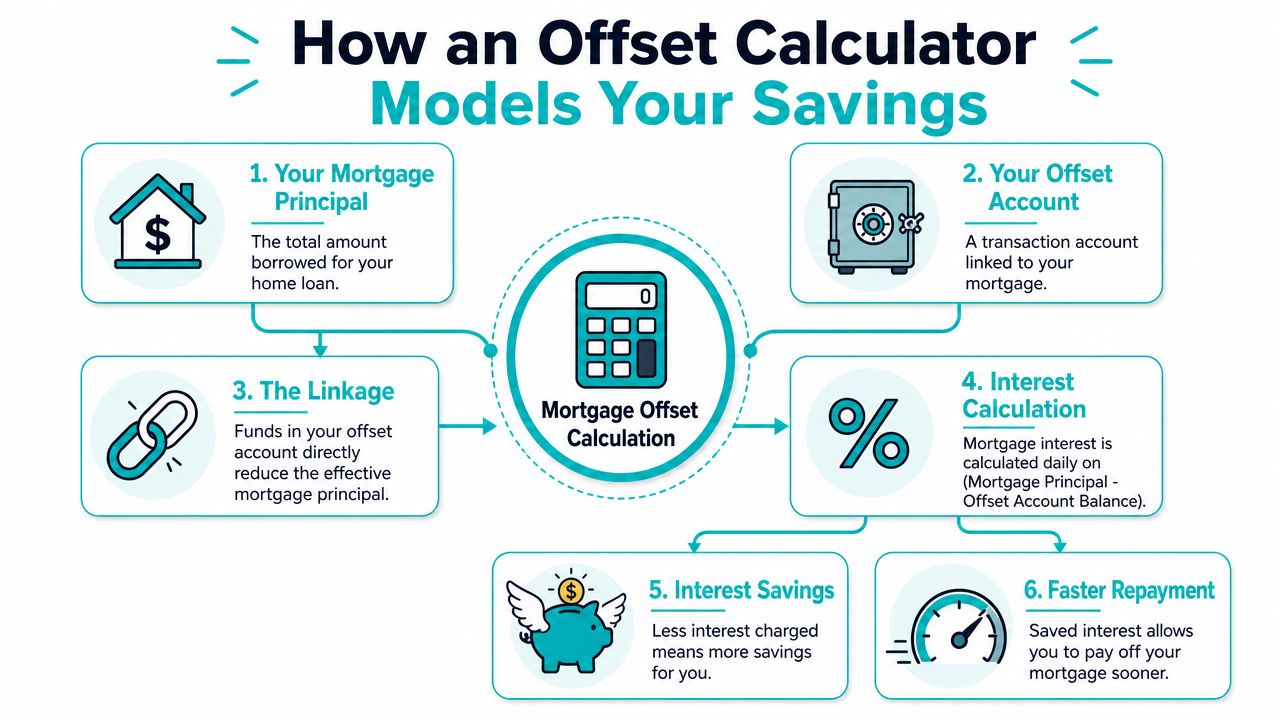

How an Offset Calculator Models Your Savings

Before you enter any figures, it helps to know what the calculator is doing.

In Australia, a mortgage offset account is a transaction account linked to a home loan that reduces the loan balance used to calculate interest. ASIC's Moneysmart gives a simple example. With a $500,000 home loan and $20,000 in offset savings, interest is charged on $480,000, not the full loan balance, as outlined by ASIC Moneysmart's mortgage offset account guide.

What the calculator is really measuring

The calculator compares two moving parts:

- Your loan balance becomes the starting point for interest.

- Your offset balance reduces the amount the lender uses for that interest calculation.

That's why the result changes so quickly when cash moves in or out. This isn't a once-a-month snapshot. It's a model of how your available cash interacts with your mortgage over time.

If you want a broader explainer to calculate mortgage interest savings in different payoff scenarios, that resource can help frame the offset result alongside other repayment strategies.

Why daily timing matters

Many borrowers focus only on the average balance. That helps, but it doesn't tell the full story. Timing matters because home loan structures with offset features are commonly tied to variable rate lending, so you also need to understand how your broader loan setup behaves. If you're weighing loan structure choices, fixed or variable rates are part of the same decision.

A simple way to think about the calculator is this:

- Start with the current loan balance

- Subtract the amount likely to sit in offset

- Apply the rate and remaining term

- Compare the outcome with and without offset funds

The best calculators don't just estimate savings. They show whether your money is sitting in the right place often enough to change the long-term result.

That's why a small balance held consistently can sometimes outperform a larger balance that disappears quickly each month.

Gathering Your Inputs for an Accurate Forecast

A calculator is only as useful as the figures you give it. If the inputs are rough guesses, the output will be too.

Australian lenders structure these tools around the same basic mechanism. The balance in the offset account is deducted from the mortgage balance, borrowers pay interest only on the net amount, and with an offset account linked to a standard variable home loan, 100% of the transaction account balance offsets interest, with interest calculated daily and charged monthly, as described by BankSA's offset calculator guide.

The figures to pull together

Most mortgage offset account calculator tools ask for the same core inputs.

Remaining loan balance

Use the current figure from your latest loan statement or banking app. Don't rely on what the balance was a few months ago.Interest rate

Enter the current rate attached to the relevant loan split. If part of your debt is fixed and part is variable, make sure you model only the portion linked to the offset.Remaining loan term

Check how long is left on the loan, not the original term. That difference changes the forecast meaningfully.Offset balance

The offset balance is a frequent source of errors. Borrowers often enter the amount they hope to keep in offset, not the amount that will remain there.

How to estimate the offset balance properly

The most reliable approach is to review your recent transaction history and work from what your banking behaviour already shows.

A simple checklist helps:

Review statements

Look at several months of account activity and note the balance pattern, not just the high point after payday.Track salary timing

If income lands in the offset and sits there before bills are paid, that improves the result more than a balance that arrives late and leaves quickly.Include real spending habits

Groceries, school fees, insurance, travel, and annual expenses all affect how long money stays parked.Separate emergency savings from everyday cash

If part of the balance is untouchable, model that as stable offset money. If it's likely to be spent soon, be conservative.

Common mistakes that skew the result

Some forecasts look fantastic on screen and disappointing in real life because the assumptions were too optimistic.

A few traps show up regularly:

| Input issue | What goes wrong |

|---|---|

| Using the original loan size | The calculator overstates the effect |

| Guessing the offset balance from memory | The result doesn't reflect real cash flow |

| Ignoring irregular expenses | The model assumes money stays longer than it will |

| Combining multiple loan portions carelessly | The estimate stops matching the actual structure |

Useful test: If the number in the calculator feels ambitious, cut it back and run the scenario again. Conservative inputs usually lead to better decisions.

Running Scenarios for Different Life Stages

The most useful way to use a calculator isn't once. It's several times, with different assumptions.

For practical use, the method is straightforward. Enter the loan balance, offset balance, rate, and remaining term, then test how long funds stay in offset because the longer the balance remains there, the more interest you save. The output is highly sensitive to cash-flow timing, not just the average offset balance, as noted by Teachers Mutual Bank's mortgage offset calculator overview.

A young professional building momentum

A borrower early in their career usually starts with a modest but growing cash buffer. Their main question isn't whether offset works. It's whether smaller, steady balances are worth the effort.

In this case, the calculator is best used as a habit-testing tool. Run one scenario with current savings behaviour. Then run another where salary lands in offset and surplus cash stays there longer before spending. The difference shows whether the main opportunity lies in saving more, or in improving timing.

For borrowers who follow international market commentary and wonder how rate settings can affect borrower behaviour more broadly, this discussion of Bank of Canada rate cut impact is a useful reminder that mortgage decisions are often tied to wider interest-rate conditions, even when your own plan should stay grounded in local lending terms.

A dual-income family using offset as a household hub

Families often get more from an offset because there are more cash flows running through the same structure. Salaries, childcare, school costs, insurance, and annual bills all create a strong reason to centralise money movement.

The calculator becomes more realistic when the family tests multiple balance levels across the month instead of one neat average. If one partner is paid fortnightly and the other monthly, the balance pattern can look very different from a standard salary cycle.

What tends to work:

- Income directed into offset first

- Bills planned rather than scattered

- A clear emergency buffer left untouched

- Separate budgeting decisions from the loan strategy

What usually doesn't work is leaving the offset open but continuing to keep meaningful cash elsewhere out of habit.

A business owner with uneven cash flow

Small business owners often have the most to gain from modelling scenarios carefully because their balances can be lumpy. Tax provisions, GST allocations, seasonal revenue, and supplier payments can all create periods where substantial funds sit in the account, followed by sharp reductions.

That makes the time-based testing especially important. One scenario might assume funds remain parked until BAS or tax payments are due. Another might reflect a leaner trading period.

Temporary balances can still be useful in offset. What matters is how often they appear and how long they stay before they're needed elsewhere.

A business owner shouldn't treat the highest bank balance of the quarter as the calculator input. The better approach is to model realistic holding periods and see whether the structure remains beneficial across both strong and quieter months.

Interpreting Results and Comparing Offset vs Redraw

Once the calculator gives you an estimate, the next step is judgment.

Most borrowers focus on two outcomes. The first is how much interest the structure could save over time. The second is whether the loan could be paid off sooner if repayments stay on track. Both matter, but neither should be viewed in isolation. A good result on paper still needs to fit your access needs, tax position, and future plans.

How to read the result properly

If the calculator shows a meaningful benefit, ask why. Usually it comes down to one of three things:

- Cash sits in the account consistently

- The account is used as a central transaction hub

- The borrower keeps repayments unchanged while reducing interest

If the result is weaker than expected, don't assume offset isn't worthwhile. It may mean your money doesn't stay parked long enough, or the balance is too variable to create a strong effect.

For people focused on debt reduction, it also helps to compare the offset result with broader strategies to pay off your mortgage early. The calculator gives one lens. The right structure often involves more than one habit change.

Mortgage Offset vs Redraw Facility at a Glance

A redraw facility often comes up in the same conversation because both options can reduce interest in practice. But they aren't interchangeable.

| Feature | Offset Account | Redraw Facility |

|---|---|---|

| Access to funds | Money usually remains in a linked transaction account and is available for day-to-day use | Access depends on the lender's redraw rules and loan setup |

| How it operates | Reduces the loan balance used to calculate interest while keeping funds separate from the loan | Involves extra repayments made into the loan, which may later be withdrawn if redraw is available |

| Daily banking use | Suits salary deposits, bill payments, and cash buffers | Not designed as an everyday transaction account |

| Repayment experience | Can support flexibility while maintaining the loan structure | Often better suited to borrowers focused on pushing extra money directly into the loan |

| Future tax considerations | Can be useful where borrowers want to preserve clearer separation between savings and loan principal, especially if future property use may change | Can become more complex where funds are repaid into and withdrawn from the loan over time |

Which one tends to suit which borrower

Offset often suits borrowers who value flexibility. Families, professionals with strong savings habits, and business owners with fluctuating balances usually like having instant access to cash while still reducing interest.

Redraw can suit someone with a simpler goal: put extra money into the loan and leave it there unless there's a clear need to pull it back.

If access, flexibility, and future planning matter, offset usually deserves a closer look. If simplicity matters most, redraw may still be the better fit.

The calculator result gives you the starting point. The structure choice determines whether the strategy will keep working once real life gets involved.

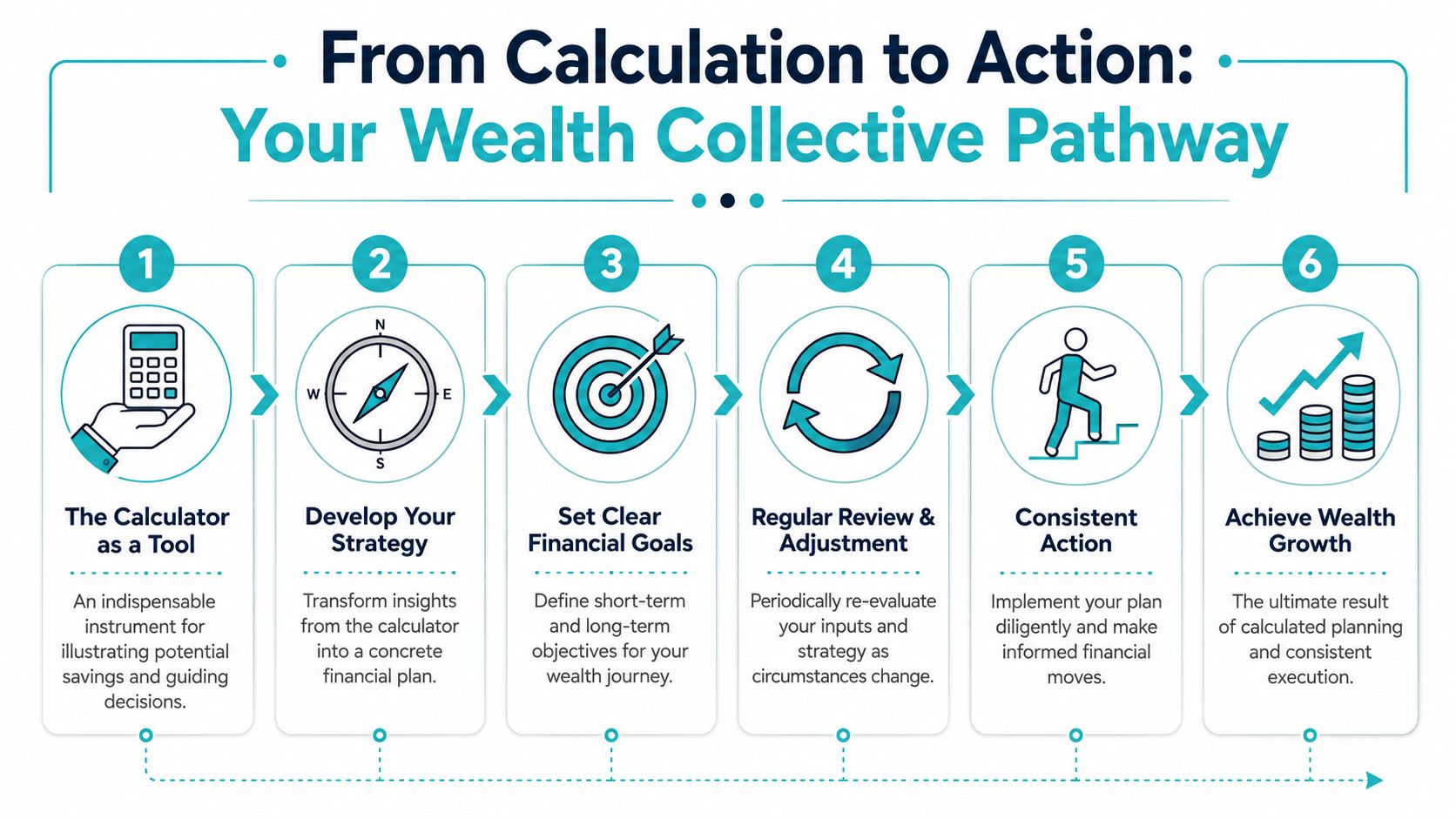

From Calculation to Action Your Wealth Collective Pathway

A mortgage offset account calculator gives you direction, not a complete plan.

That distinction matters. The tool can show potential savings and a possible reduction in loan term, but it can't tell you how to balance mortgage reduction against super contributions, investment goals, insurance needs, future school fees, or a possible move into business or retirement. Those decisions sit above the calculator.

Turning the estimate into a strategy

The most effective next step is to treat the calculator result as a working draft, then pressure-test it against your actual goals.

That usually means asking:

- Is the offset balance realistic year-round

- Does the loan structure still suit your stage of life

- Would the same cash be better used elsewhere

- How often should the plan be reviewed as income and expenses change

A good strategy keeps the benefits of the offset without creating friction in the rest of your financial life. If the setup is too rigid, people stop using it well. If it's too loose, the savings never build.

Wealth creation rarely comes from one tool alone. It comes from aligning debt, cash flow, risk management, and long-term investing so each part supports the others.

If you want help turning your calculator result into a practical financial plan, Wealth Collective can help. Our Guided Growth approach is built for Australians who want their money working with purpose, not just sitting in the right account by accident. Book a complimentary 10-minute initial call and we'll help you assess whether an offset strategy fits your broader goals, your cash flow, and the kind of wildly successful financial life you're building.