Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You've probably felt it already.

You've built real wealth the sensible way. A solid income. Maybe an investment property or two. A decent share portfolio. Super that's no longer an afterthought. On paper, things look organised. But every time listed markets lurch, or property headlines turn noisy, you're reminded that being “diversified” in Australia often just means owning different versions of the same risk.

That's usually the point successful investors start asking a better question. Not “What's hot?” but “What else belongs in this portfolio?”

That's where alternative investments enter the conversation. Not as exotic toys for thrill-seekers. As a practical next layer for people who've outgrown a basic mix of shares, cash and residential property. If you're trying to build resilience, create different income streams, or protect future retirement spending from inflation and market mood swings, alternatives deserve a serious look.

They also get oversimplified. Most articles give you a glossy list of asset types and move on. They don't spend enough time on the part that matters in real life: when you can get your money back, how the structure works, and whether the investment fits your stage of life. That matters a lot in Perth, where many clients I meet are balancing business income, property exposure, family commitments and a retirement timeline that's suddenly not that far away.

Beyond Shares and Property

A common pattern shows up in advice meetings.

A couple in their late forties or fifties has done well. One is in a senior role, the other runs a business or has built a strong career. They've accumulated wealth through the ASX, super and property. They're not reckless. They're not chasing fads. They're just tired of feeling overexposed to listed market swings and the same domestic property narrative.

They want a portfolio that behaves differently.

Not wildly differently. Sensibly differently. They want assets tied to essential services, private businesses, contractual income or specialist strategies that don't rise and fall purely because public markets had a bad quarter. That instinct is right. Mature portfolios usually need more than “more of the same”.

A resilient portfolio doesn't come from owning more line items. It comes from owning different return drivers.

That's the core appeal of alternative investments in Australia. They can add assets that sit outside the standard retail menu and broaden where returns might come from. For some investors, that means access to infrastructure or private credit. For others, it means selective exposure to private equity, specialist funds or real assets that offer a different mix of income, growth and inflation protection.

Still, sophistication cuts both ways. Plenty of investors step into alternatives because they want less volatility, then discover they've bought complexity, lock-ups and structures they don't properly understand. That's not smarter investing. That's just upgrading your confusion.

The right approach is simple. Start with the role the investment needs to play. Then test whether the structure, liquidity and risk profile match that job.

What Are Alternative Investments Really

Alternative investments are assets outside the standard trio of shares, bonds and cash. Think of traditional investments as the meat and potatoes of a portfolio. They're familiar, useful and foundational. Alternative investments are everything that expands the menu beyond that.

That doesn't make them better by default. It makes them different.

Why investors add them

The point of alternatives isn't novelty. The point is diversification with purpose. You're adding assets that may respond to different forces than listed shares or term deposits. A toll road, private loan portfolio, unlisted property trust or hedge fund strategy doesn't necessarily move for the same reasons the ASX does.

For high-income earners and pre-retirees, that matters because concentration risk tends to build subtly. You can own a home, an investment property, Australian shares and super, and still be heavily tied to the same economic cycle.

A better investment diet includes assets that can contribute in different ways:

- Income sources: Some alternatives focus on regular distributions or contracted cash flow.

- Growth exposure: Others target long-term capital growth through private businesses or specialist themes.

- Inflation support: Certain real assets can hold up better when living costs rise.

- Portfolio behaviour: Some strategies aim to smooth the ride when listed markets get messy.

What this looks like in practice

In plain English, alternatives often sit in one of these buckets:

- Private assets: Investments in businesses or loans that aren't listed on a public exchange.

- Real assets: Infrastructure, unlisted real estate, commodities or other tangible assets.

- Strategy-based funds: Vehicles such as hedge funds that use broader tools than a plain share fund.

- Emerging areas: Digital assets and tokenised structures, which need a much tighter risk filter.

If you're moving into property-related alternatives, it helps to understand the language before reading an offer document. A practical primer on real estate investing terms can save you from signing up to something you only half understand.

Practical rule: If you can't explain where the return comes from, what can go wrong, and when you can exit, you're not ready to invest.

That rule cuts through the noise fast.

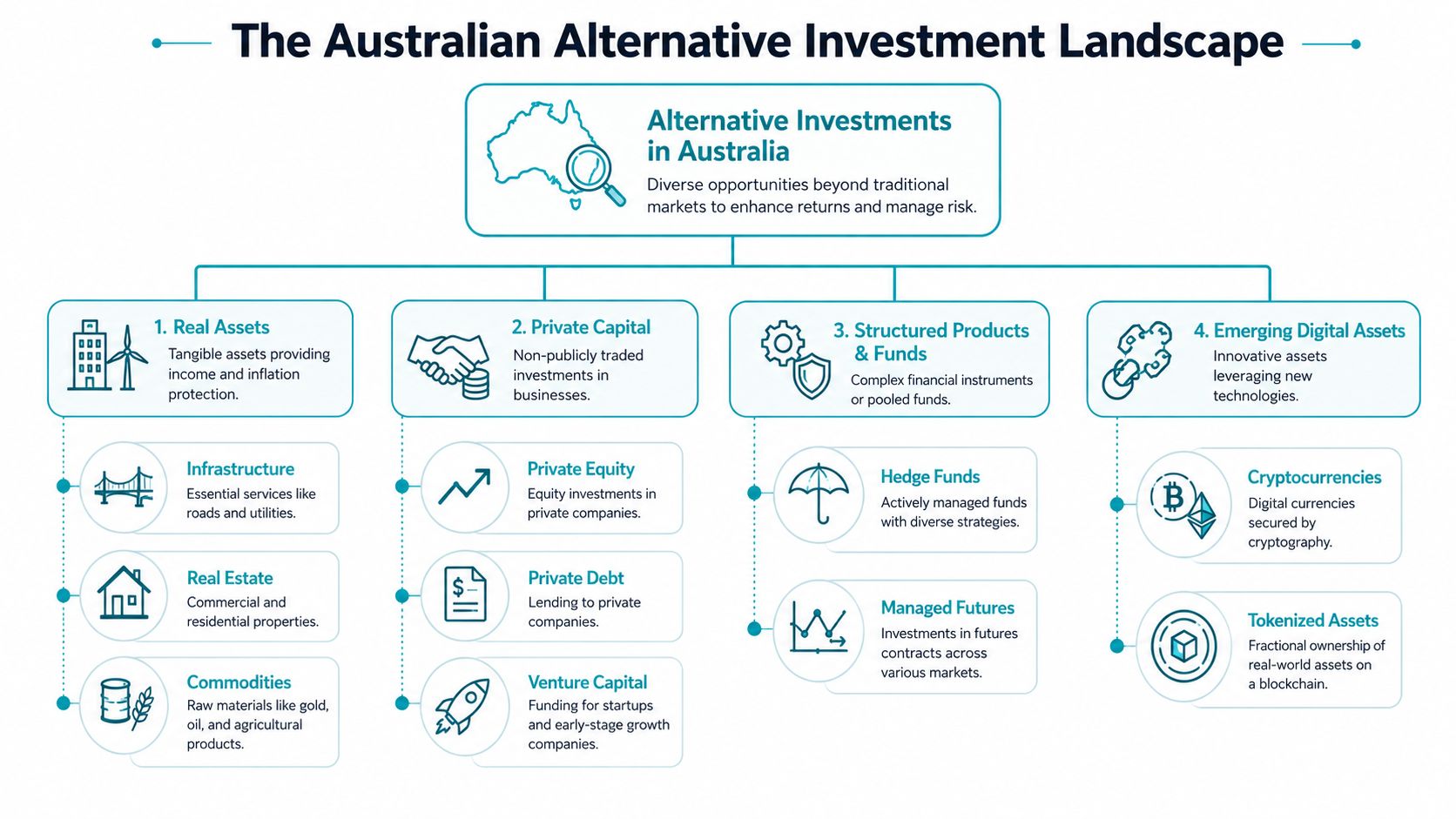

The Australian Alternative Investment Landscape

Australia's alternatives market is no sideshow. It's established, broad and increasingly relevant for private investors who want more than listed shares and standard property exposure. According to Chambers and Partners' Australia trends and developments guide, Australian-focused private capital assets under management totalled AUD 139 billion as of September 2024, with real estate at AUD 54 billion, and AUD 65 billion allocated specifically to private equity, venture capital and private credit funds. The same source notes that fundraising for Australia-focused funds dropped to AUD 5.7 billion in 2025, the lowest level in a decade, while family offices now make up 40% of active private capital investors by number.

That tells you two things. First, alternatives are a serious element within the local investment sector. Second, access to capital has tightened, which makes manager selection and structure even more important.

Growth engines

Private equity and venture capital sit here. These strategies back private businesses rather than listed companies. Private equity usually focuses on more established businesses with a pathway to operational improvement, expansion or eventual sale. Venture capital targets earlier-stage companies and carries more uncertainty.

These aren't “set and forget” assets. They require patience, manager skill and a stomach for delayed outcomes. They can suit investors who already have a strong base portfolio and want selective growth exposure outside public markets.

Real assets

Many Australians feel more comfortable with investments where the assets are easier to picture. Real estate, infrastructure and sometimes commodities fall into this bucket.

BlackRock's Australian alternatives overview notes that the local alternatives market is valued at approximately AUD100 billion, and identifies infrastructure and unlisted real estate as core parts of the unlisted asset class. It also highlights infrastructure equity across energy, transport, water, waste and digital or social infrastructure, with income characteristics linked to contracted cash flows and inflation protection for long-term investors.

For many investors, this is the most intuitive corner of alternative investments Australia has to offer. You can see the asset, understand the service it provides, and assess whether the income story stacks up.

Private credit

Private credit deserves its own lane because investor interest has lifted sharply. Again, the Chambers guide reports 51 Australia-focused open-ended private credit funds tracking over AUD 25 billion in total net asset value. That's significant.

Private credit can include lending to businesses, property-backed loans and other non-bank financing arrangements. The attraction is straightforward: income, contractual lending terms and diversification away from listed equities. The danger is equally straightforward: investors often treat it like enhanced cash when it plainly isn't. If you want a deeper look at how the asset class works, this overview of private credit investing is a useful starting point.

Strategy funds and emerging assets

Hedge funds and managed futures sit in the “strategy” category. They're defined less by what they own and more by how they invest. They may use long-short approaches, derivatives or macro views that differ sharply from a plain vanilla managed fund.

Then you have digital assets and tokenised structures. They attract attention quickly and due diligence slowly. That's backwards. For most investors, these belong in the “small, speculative, fully-understood-only” bucket, if they belong anywhere at all.

A practical comparison

| Category | Main role in a portfolio | Liquidity profile | Typical investor fit | Key caution |

|---|---|---|---|---|

| Private equity and venture capital | Long-term growth | Usually low | Investors with time and strong risk capacity | Returns can take years to realise |

| Infrastructure and unlisted real estate | Income and inflation support | Often low to moderate | Pre-retirees and long-term wealth builders | Access terms matter more than brochures |

| Private credit | Income and diversification | Varies by fund structure | Investors seeking non-bank lending exposure | Don't confuse it with cash |

| Hedge funds and managed futures | Diversification through strategy | Varies | Sophisticated investors wanting a different return profile | Complexity and manager risk |

| Digital assets and tokenised assets | Speculative growth or thematic exposure | Varies widely | Investors who can tolerate sharp volatility | High due diligence burden |

The best category isn't the one with the best story. It's the one that solves a real portfolio problem without creating a bigger one.

Weighing the Rewards Against the Risks

Alternative investments can improve a portfolio. They can also trap a portfolio. Both statements are true.

The upside is easy to sell. The downside is usually hidden in the application form, the withdrawal terms or the sentence investors skipped on page forty-three of the information memorandum. That's why this part matters more than the glossy marketing.

Why the rewards are real

Some alternatives can deliver benefits traditional portfolios struggle to provide on their own.

- Different return drivers: Private markets, infrastructure and specialist strategies may be influenced by contracts, project cash flow, lending margins or manager skill rather than daily sharemarket sentiment.

- Inflation support: Certain real assets, especially infrastructure, can offer revenue characteristics linked to inflation. That's useful if you're trying to protect future spending power.

- Access to parts of the economy public markets miss: Some opportunities aren't available through listed shares.

- Potentially steadier income: Contracted or asset-backed cash flows can appeal to investors who want more than dividend uncertainty.

That's the case for alternatives at their best. They broaden your opportunity set and can make a portfolio less reliant on one narrow set of economic outcomes.

The risk most investors still get wrong

Liquidity is the issue. Not volatility. Not fees. Liquidity.

Mercer points to the blind spot directly. In its Australian alternatives material, 68% of retail investors underestimate their inability to access capital for 5 to 10 years in private credit or infrastructure funds, leaving them exposed to what Mercer describes as liquidity cliffs when retirement spending needs arrive. You can review that finding in Mercer's discussion of alternatives and liquidity budgeting.

A liquidity cliff is simple. You need money. The investment won't release it. Or it will, but not on your timeline.

That's manageable for a younger accumulator with strong cash flow and years to wait. It's a much bigger problem for a WA pre-retiree who expects an unlisted fund to help fund a renovation, bridge an income gap, support adult children or top up retirement spending.

Other risks that deserve blunt treatment

Complexity and transparency

Many alternative structures are harder to analyse than listed assets. Reporting can be slower. Valuations can be less visible. Fund terms can be dense. If you need a glossary beside the product disclosure document, pause.

Higher fees

Specialised access usually costs more. Sometimes the extra fee is justified by specialist sourcing, active management or complexity. Sometimes it just isn't. You need to know which is which.

Structure risk

A strong underlying asset can still sit inside a poor structure. Withdrawal gates, mismatched liquidity, gearing and manager discretion all matter. Investors often focus on the asset and ignore the vehicle. That's a mistake.

If an investment promises stable income but limits your ability to exit, treat it as an illiquid asset first and an income asset second.

My view

Alternatives belong in many portfolios. They do not belong there by default. If you're still carrying expensive debt, lack emergency liquidity, or expect to draw on capital in the medium term, your first job isn't chasing alternatives. It's fixing the basics and ringfencing liquidity.

For pre-retirees especially, liquidity budgeting isn't optional. It's one of the main decision filters.

Navigating Australian Tax SMSFs and Regulations

The legal wrapper matters almost as much as the investment itself. Many capable investors often get sloppy in this area. They research the asset, like the pitch, and ignore the compliance framework. That's how sensible ideas turn into administrative headaches.

SMSFs need discipline, not improvisation

An SMSF can invest in alternatives, but the bar is higher than many people realise. The fund's investment strategy has to support the decision. The asset must fit the sole purpose of providing retirement benefits. Documentation has to be clean. Valuation, related-party issues and liquidity all need attention.

That's especially important if the fund is considering less familiar assets or private structures. Just because an SMSF can technically access something doesn't mean it should.

If you want a grounded explanation of the structure itself before looking at alternatives, this guide on what is a SMSF is a useful primer.

CCIVs are worth knowing

Australia added a newer investment structure with the Corporate Collective Investment Vehicle, or CCIV, introduced on 1 July 2022. According to PwC's explanation of Australia's new alternative investment structure, all CCIVs, whether retail or wholesale, must be registered with ASIC, and a retail CCIV must lodge a compliance plan with ASIC.

That's a meaningful due diligence point. It doesn't make a CCIV automatically superior. It does mean the regulatory architecture is distinct from a traditional Managed Investment Scheme, particularly where wholesale structures may not carry the same registration requirement.

Tax and property-linked alternatives

The tax treatment of alternative assets depends heavily on the vehicle, the underlying investment, and whether you're investing personally, through a company, trust or super. There's no universal shortcut.

That's also why investors need to separate broad tax ideas from specific deductions. If you're comparing property-linked alternatives with direct property ownership, practical issues such as Australian property conveyancing tax can affect how you assess direct property costs versus a fund structure.

Due diligence questions that actually matter

Before you sign anything, get direct answers to these:

- What is the legal structure? Trust, company, CCIV or something else.

- Who can redeem and when? Monthly, quarterly, at manager discretion, or not until maturity.

- How is the asset valued? Independent valuation process matters.

- Does the investment fit the SMSF strategy? If not, don't force it.

- What happens in stressed markets? In stressed markets, fine print becomes real.

Regulation won't save you from a poor decision. It just gives you a better framework to evaluate one.

How You Can Access Alternative Investments

Access has improved, but that doesn't mean all access points are equal. In practice, most investors enter alternatives through one of three paths. Each has trade-offs. The right choice depends less on excitement and more on your balance sheet, experience and tolerance for complexity.

Specialised funds and unlisted trusts

This is the most common route for private investors. You invest through a managed fund, unit trust or similar vehicle run by a specialist manager.

The appeal is obvious. You get professional management, diversification within the strategy, and easier administration than sourcing deals yourself. The downside is that you inherit the manager's fees, liquidity terms and portfolio construction decisions. If the fund is mediocre, you own a well-packaged mediocre investment.

This path usually suits busy professionals and families who want access without becoming part-time analysts.

Modern investment platforms

Some platforms now give investors curated exposure to private assets, specialist managers or niche opportunities that used to be harder to reach. That can simplify administration and broaden the menu.

Still, convenience can blur judgement. A polished dashboard doesn't remove underlying risk. It just makes it easier to buy. Investors need to read past the platform interface and into the actual fund terms, redemption rights and manager track record.

Access is not the same as suitability. The fact you can click into an alternative investment doesn't mean it belongs in your portfolio.

Direct deals

Direct deals are where confidence can outpace competence. These include private loans, direct business investments, syndicated property deals or bespoke opportunities from personal networks.

The upside is control and sometimes sharper economics. The downside is concentration, due diligence burden and a much higher chance of making an expensive mistake. Direct deals usually make sense only for experienced investors who understand the asset, the counterparties and the legal documentation.

A side-by-side view

| Access path | What you get | Where it works well | Main downside |

|---|---|---|---|

| Specialised funds | Professional management and pooled exposure | Investors who want cleaner access to a strategy | Less control and manager dependence |

| Investment platforms | Convenience and broad menu access | Organised investors who compare options carefully | Easy to mistake convenience for quality |

| Direct deals | Control and customised exposure | Sophisticated investors with expertise and strong due diligence support | Concentration and execution risk |

Where an adviser fits

An adviser isn't a fourth access path. An adviser is the filter that helps you use the other three properly.

That matters because alternatives don't fail only on returns. They fail on fit. The wrong holding period, the wrong structure, the wrong amount invested, or the wrong asset inside an SMSF can undo what looked like a smart idea.

For niche areas especially, perspective matters. A collector looking at tangible assets, for example, might browse a specialist wine investment guide, but that still doesn't answer whether the asset belongs alongside super, property and core investments. The portfolio context is the key question.

If the alternative sits inside super, the structure matters again. Investors considering direct property exposure through super should understand the mechanics before acting. This explainer on buying property in an SMSF is helpful for that specific pathway.

Your Next Step Toward a Resilient Portfolio

Alternative investments can play a valuable role in a serious portfolio. They can add income diversity, inflation support, access to private markets and a different return profile than standard listed assets. For the right investor, that's useful.

But the overlooked part is still the decisive part. Liquidity, structure and life-stage fit matter more than the headline return target. A pre-retiree with upcoming cash flow needs should assess an unlisted infrastructure or private credit fund very differently from a younger professional with strong income and a long runway. The same asset can be sensible for one person and a problem for another.

That's why this area rewards discipline, not enthusiasm.

If you're exploring alternative investments in Australia, start with a blunt audit:

- What role does this investment play?

- How long can the capital stay locked up?

- What happens if I need liquidity earlier than planned?

- Does this improve my total portfolio, or just add complexity?

Get those answers right and alternatives can strengthen your plan. Get them wrong and they can subtly create the exact stress you were trying to avoid.

If you want clear advice on whether alternative investments fit your stage of life, cash flow and long-term goals, talk to Wealth Collective. Their Guided Growth process is built for Australians who want smart, structured investment decisions without the noise. Book a complimentary 10-minute introductory call and have a straightforward, no-obligation chat about what belongs in your portfolio, what doesn't, and what to do next.