Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You’ve built a career, grown your income, and probably made sharper decisions in business than many others ever will. Then you look at your super and it feels generic. A few managed options. A fee structure you don’t control. Limited visibility over what’s being bought and sold on your behalf.

That mismatch frustrates a lot of successful WA professionals.

If you’re a business owner in Perth, a medical specialist, a senior executive, or a couple with strong combined incomes, you may already be asking the right question. Is your super set up to support your actual goals, or is it just sitting in a default structure because that’s where it landed years ago?

That’s where the benefits of SMSF become worth serious attention. An SMSF gives you control, broader investment choice, and far more room for strategic tax planning than is typically available in a standard fund. It also gives you responsibility. That trade-off matters, and I’ll be direct about it.

This isn’t a strategy for everyone. But for the right person, it can be one of the most useful wealth structures available in Australia.

Is Your Super Working as Hard as You Are?

A common WA scenario goes like this. You’ve got solid income, your mortgage is under control or nearly there, and your super balance has grown into something meaningful. But every time you log in to your fund, you feel like a spectator.

You can choose between menu options, but you can’t shape the strategy in a way that reflects your real priorities. You might want direct exposure to a specific asset, tighter tax management, or a long-term plan to buy business premises. Your fund usually won’t give you that level of control.

That’s why more Australians are choosing to take the wheel themselves. As of September 2025, the SMSF sector had 661,384 funds holding an estimated $1.07 trillion in assets for more than 1.2 million members, according to SMSF quarterly statistics for September 2025. That isn’t fringe behaviour. It’s a mainstream decision made by people who want their retirement capital treated with the same care they apply to their careers and businesses.

Most people don’t need more super options. They need a structure that lets them act on the options that already suit them.

An SMSF isn’t a magic trick. It won’t fix weak saving habits or poor investment judgement. But if you already think strategically and want your super to reflect that, it can be a far better fit than an off-the-shelf fund.

What Exactly Is a Self-Managed Super Fund?

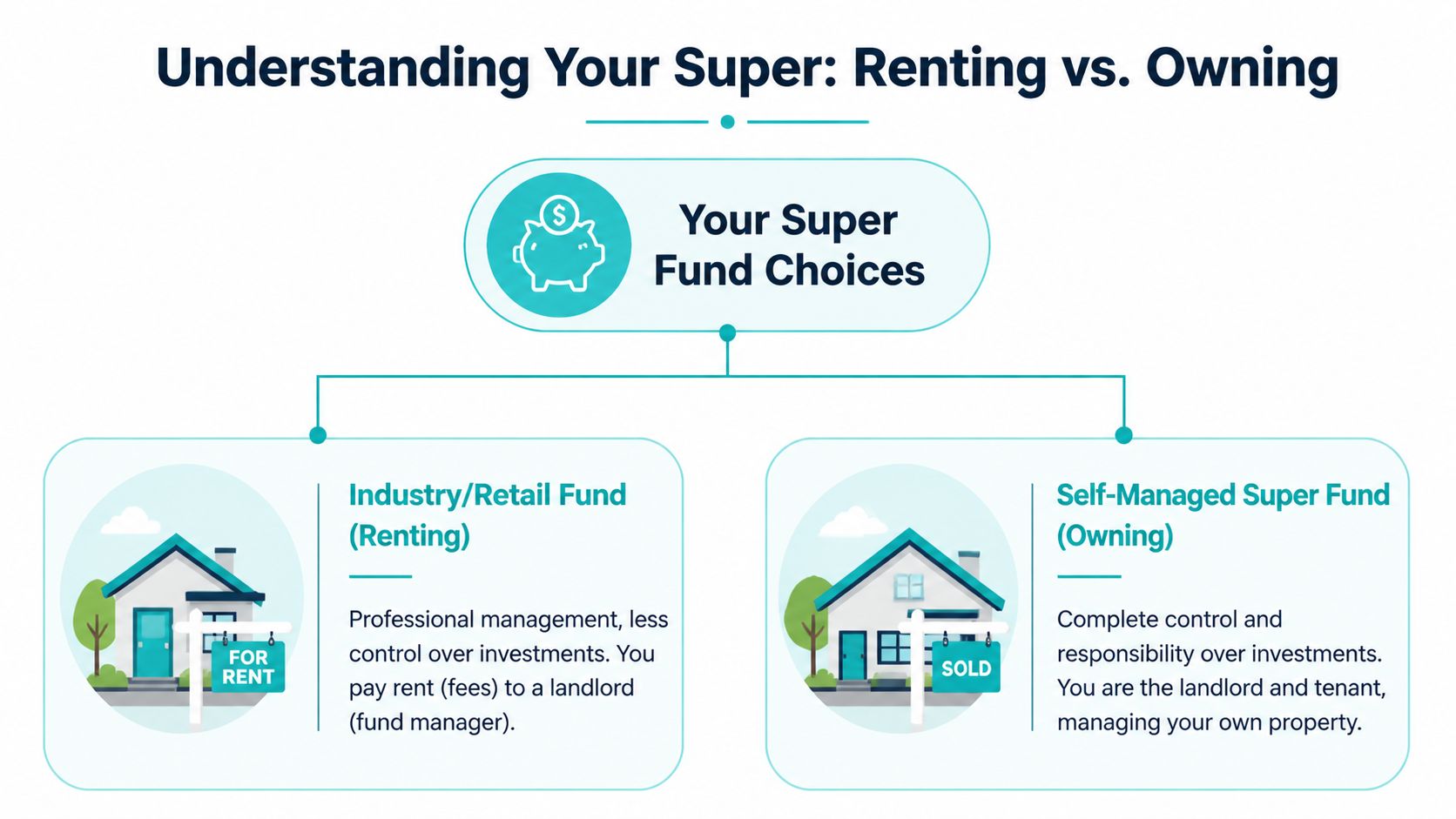

Think of a retail or industry fund like renting in a large apartment complex. The building is professionally managed, the rules are already set, and you get convenience. But you don’t decide the design, you don’t choose the exact assets, and you work within someone else’s framework.

An SMSF is closer to owning the property yourself. You decide how it’s structured, what goes inside it, and how it’s run. You also carry the responsibility.

If you want a basic primer before going further, this guide on what an SMSF is is a useful starting point.

Who actually runs it

The members of the SMSF are usually also the trustees, or directors of a corporate trustee. That means the people benefiting from the fund are also the people legally responsible for it.

That responsibility includes:

- Investment decisions. Trustees choose the assets and make sure the strategy is documented and appropriate.

- Compliance. Trustees must follow super laws, maintain records, and ensure the fund meets its legal obligations.

- Administration oversight. Even if professionals handle the work, trustees remain accountable for the outcome.

That last point matters. You can outsource tasks. You can’t outsource responsibility.

Self-managed doesn’t mean alone

A lot of people hear “self-managed” and assume it means doing everything yourself. That’s a mistake.

In practice, most serious SMSF trustees use a support team. That can include an accountant, an administrator, an auditor, and a financial adviser. The trustees still make decisions, but they do so with technical support and strategic advice around them.

Practical rule: If you want full control but no responsibility, an SMSF is the wrong structure.

The right mindset is this. You are the decision-maker. Professionals help you implement, document, and monitor the strategy properly.

Why people choose this structure

People don’t usually set up an SMSF because they want more paperwork. They do it because the structure solves a specific problem.

A few common examples:

- They want direct control over investments instead of choosing from a menu.

- They want to buy a specific asset inside super, such as commercial property.

- They want better tax planning flexibility around contributions, disposals, and pension transitions.

- They want family-level strategy rather than scattered accounts across multiple funds.

That’s the key point. An SMSF is not a product. It’s a legal and strategic structure. Used properly, it gives you room to build a super strategy that matches your life.

The Five Core Benefits of an SMSF

The benefits of SMSF aren’t theoretical. They’re practical. They matter when you want your super to do a specific job, not just drift along in a default setting.

Control that actually means something

This is the big one.

With an SMSF, you decide what the fund owns and why it owns it. You’re not picking from a shortlist designed by someone else. You can build a portfolio that matches your risk tolerance, cash flow needs, time horizon, and broader wealth plan.

For a Perth business owner, that might mean prioritising liquidity while the business scales. For a pre-retiree in Dunsborough, it might mean shifting the portfolio toward income-producing assets and simpler management.

That control also changes behaviour. People tend to engage more seriously when they know the decisions are theirs.

Broader investment choice

Mainstream funds give you packaged access. SMSFs can give you direct ownership.

That matters if you want to invest in assets that don’t fit neatly inside a standard menu. A business owner may want their fund to hold commercial premises. An investor with specific investment preferences may want selected shares, term deposits, ETFs, or carefully chosen alternatives. The structure can be designed around the asset mix you want, subject to super rules and a proper investment strategy.

This is one area where Australian trustees often look internationally for ideas. If you want to understand how other retirement systems approach investor control, this piece on self-directed IRA investing is useful context. Different jurisdiction, same underlying principle. Control attracts people who want their retirement capital aligned with their own judgement.

Better tax planning flexibility

At this point, SMSFs become truly powerful.

Trustees can control the timing of asset sales, manage gains more deliberately, and structure the fund so that investment income and capital gains can be taxed at zero when assets are wholly supporting an income stream in pension phase, as explained in Pitcher’s discussion of SMSF tax planning and pension phase strategy.

That flexibility matters in real life. If you’re selling a lumpy asset, managing a transition to retirement, or coordinating contributions in a high-income year, timing can materially change the tax outcome.

Here’s the practical point. In a retail fund, you live with fund-level decisions. In an SMSF, your fund can plan around your circumstances.

Estate planning with more precision

Super doesn’t automatically go where people assume it will. That’s one reason high-balance members often outgrow generic structures.

An SMSF can give you more control over how benefits are handled, how assets are positioned, and how family wealth transitions are managed. That doesn’t remove complexity. It gives you more tools to deal with it properly.

For blended families, business owners, or couples with very different balances and retirement timelines, that control can be far more valuable than people realise at first.

If your estate planning is vague, your super strategy is incomplete.

Cost efficiency when the balance is right

The cost discussion around SMSFs is often poorly handled. People either oversell the savings or ignore them.

SMSFs can be cost-effective because many of the running costs are fixed rather than charged as an ongoing percentage of assets. For larger balances, that can work in your favour. Prime Financial notes that SMSFs often become cost-effective for balances typically over $200,000, depending on complexity and providers, and also highlights the concessional 15% tax treatment during accumulation phase and the tax-free treatment on assets wholly supporting an income stream in pension phase in its article on why investors choose an SMSF over a retail fund.

That doesn’t mean every SMSF is cheaper. It means the fee structure can become more efficient as the balance grows and the strategy gets more specific.

The five benefits in plain English

| Benefit | What it means in practice |

|---|---|

| Control | You decide what the fund invests in and when changes happen |

| Choice | You can build around specific assets and strategies, not just packaged options |

| Tax flexibility | You can manage timing and pension phase transitions more deliberately |

| Estate planning | You get more control over how super wealth is directed and administered |

| Cost efficiency | Fixed costs can become attractive when balances are high enough |

The strongest reason to consider an SMSF isn’t ego or novelty. It’s strategic fit. If you want your super to support a clear plan, and you’re prepared to govern it properly, the benefits are real.

Understanding the Costs and Responsibilities

To be blunt, plenty of people like the upside of an SMSF. Fewer people respect the workload and discipline that comes with it.

That’s a problem, because the structure only works well when it’s run properly.

The cost side

An SMSF has setup work and ongoing annual costs. Those usually include administration, accounting, audit, regulatory obligations, and any advice you choose to use.

The important issue isn’t whether there are costs. Of course there are. The question is whether the strategy justifies them.

You should be sceptical of anyone telling you an SMSF automatically saves money. Sometimes it does. Sometimes it doesn’t. Balance size, asset mix, family structure, and complexity all matter.

The break-even issue is real

Low-balance SMSFs often struggle. That’s not opinion. The ATO has found that SMSFs with balances under $200,000 often have higher running costs and lower returns than APRA-regulated funds. As of 2024, 16% of funds are under $100,000, which increases the risk of underperformance and compliance problems, as noted in this summary of ATO findings on when SMSFs may not stack up.

If your balance is modest and you mainly want convenience, an industry or retail fund is often the better answer. There’s nothing wrong with that.

The responsibility side

Trustees have legal duties. They need to keep records, maintain a current investment strategy, make sure assets are held correctly, and ensure the fund follows super law.

That means you need to be comfortable with:

- Decision-making. You can’t switch off and blame the fund manager later.

- Documentation. Good strategy with poor records is still a problem.

- Ongoing oversight. You need to review what the fund is doing and why.

- Professional coordination. Accountants, auditors, and advisers all need clean information and timely responses.

An SMSF is not a hobby account. It’s a regulated trust structure holding retirement money.

What goes wrong most often

In my experience, the people who struggle with SMSFs usually fall into one of three camps:

- They started too early with an insufficient balance.

- They wanted control without governance.

- They bought a strategy they didn’t understand.

That’s why proper upfront advice matters. Good advice won’t just tell you the benefits of SMSF. It will tell you when not to proceed.

A simple filter

Before you even think about setup, ask yourself:

- Do I want real control, or do I just dislike my current fund?

- Am I prepared to act like a trustee, not just an investor?

- Does my balance and strategy justify the work and cost?

- Will I use specialist support where needed?

If those answers are weak, don’t force it. If they’re strong, an SMSF may be worth serious modelling.

SMSF vs Industry and Retail Funds a Direct Comparison

This comparison is where the noise usually clears.

An SMSF is not “better” in every way. It’s better for people who value control, flexibility, and strategic tailoring enough to accept the added responsibility. For everyone else, an APRA-regulated fund can be the smarter choice.

SMSF vs APRA-Regulated Funds (Industry/Retail)

| Feature | Self-Managed Super Fund (SMSF) | APRA-Regulated Fund (Industry/Retail) |

|---|---|---|

| Investment control | Trustees choose and manage the investment strategy directly | Members choose from menu options set by the fund |

| Asset choice | Broader direct investment capability, subject to rules and strategy | Mostly limited to pre-selected investment menus and packaged options |

| Fee structure | Often built around fixed running costs | Usually percentage-based fees linked to balance |

| Tax strategy | Greater ability to manage timing of sales and pension transitions | Less individual control over tax outcomes |

| Compliance burden | Trustees carry legal responsibility | Fund provider handles compliance and administration |

| Ideal member profile | Engaged investor, business owner, or pre-retiree wanting control | Member who values simplicity and a hands-off approach |

The cost difference in one practical example

For larger balances, the fee structure can tilt in favour of an SMSF. Stake notes that for balances over $500,000, SMSFs can become highly cost-efficient because costs are typically fixed. Its example compares a retail fund charging 1%, or $5,000 on a $500k balance, with a well-run SMSF whose fixed costs could be around $3,000, in its article on how SMSF costs can compare with retail funds.

That doesn’t settle the question by itself. But it does show why high-balance members should at least run the numbers instead of assuming the default fund is cheaper.

Which side do you actually fit?

If you want to choose a specific commercial property, direct shares, or manage tax timing around retirement, an SMSF is usually the relevant structure to consider.

If you want someone else to handle everything and you’re happy with packaged options, stay with an APRA-regulated fund. That’s not settling. That’s matching the structure to your preferences.

The mistake is using the wrong vehicle for the job.

Advanced Strategies for WA Business Owners and Investors

SMSFs are particularly relevant for successful WA business owners. A standard super fund can hold your money. An SMSF can become part of a wider business and retirement strategy.

Buying business premises through super

For many business owners, one of the most compelling strategies is owning commercial premises through an SMSF. That can mean your business pays rent to the fund at market terms, rather than paying a landlord forever.

This can be powerful when the premises are central to the business and you want more long-term control over occupancy and retirement wealth building. If you’re considering that path, this guide on buying property with super is worth reading.

A proper decision here starts with valuation discipline. Before you structure anything around your business or premises, you need a clear handle on enterprise value and commercial viability. This article on determining your business’s value gives helpful context for that thinking.

Why this matters in WA

WA business owners often operate in industries where premises are more than just office space. They’re operational assets. Warehouses, workshops, consulting rooms, logistics sites, and mixed-use commercial property can all be strategically important.

If the property is something your business needs long term, using super as part of the ownership strategy can align retirement planning with business planning. That’s a far more intelligent use of capital than treating super as a separate bucket no one thinks about.

The strongest SMSF strategies usually solve two problems at once.

Beyond property and into alternatives

Property still matters, but discerning trustees are increasingly looking beyond it. According to the SMSF Association discussion of non-traditional asset classes, private markets have returned 12.4% p.a. compared with 9.2% for listed equities, in the context of trustees exploring broader diversification through non-traditional SMSF assets.

That doesn’t mean you should chase illiquid assets just because they sound advanced. It means an SMSF can give you access to opportunities that are difficult to hold effectively inside a standard fund structure.

Examples may include:

- Private market exposure that suits a long-term horizon

- Infrastructure-style assets where cash flow and diversification matter

- Specialised allocations that sit alongside listed equities and property

The discipline matters more than the idea

Advanced strategy is where bad advice gets expensive fast.

A commercial property purchase, an LRBA, or an allocation to alternatives should only happen when the fund has enough scale, liquidity, and governance to support it. That includes a proper investment strategy, attention to cash flow, and a clear understanding of what happens if circumstances change.

This is also the one point in the process where using a specialist advice framework helps. Wealth Collective’s service model includes retirement planning, superannuation strategy, and SMSF guidance as part of broader wealth planning for WA clients. That’s relevant when the SMSF is not a standalone idea, but one piece of a larger plan involving the business, family balance sheet, and retirement income.

Is an SMSF Right for You? A Decision Framework

Forget the marketing. Use a filter.

If you answer yes to most of the questions below, an SMSF is worth proper investigation. If you answer no to most of them, don’t force it.

The right-fit checklist

- You want control over what your super owns.

- You have a meaningful balance, or a combined family balance that can justify the structure.

- You’re a business owner who wants to explore owning commercial premises through super.

- You care about tax planning and want more flexibility around timing, pension phase, and asset sales.

- You’re comfortable with governance and you won’t ignore trustee responsibilities.

- You want customized strategy, not just a menu of pre-built options.

If you’re still weighing trade-offs, this article on self-managed super fund pros and cons adds another useful lens.

The wrong-fit signals

An SMSF is usually the wrong fit if:

- You want set-and-forget convenience above all else.

- You have a relatively small balance and no specific strategic use case.

- You dislike paperwork, oversight, and decision-making.

- You’re mainly reacting to frustration with your current fund rather than moving toward a clear plan.

Wanting more control is a good reason to review an SMSF. Wanting to copy someone else is not.

A good consultation should confirm or reject the idea quickly. You don’t need a sales pitch. You need a suitability decision.

Build Your Roadmap with Wealth Collective

Starting an SMSF is a strategic decision, not an admin exercise. If it’s the right move, it should fit into a bigger plan around retirement timing, tax position, investment structure, and family wealth.

That’s why the first step should be simple. Clarify whether the structure suits you before you spend time on setup, providers, and implementation.

If you’re in Perth, Dunsborough, or elsewhere in WA, book a short introductory conversation and bring your most pressing questions. Is your balance high enough? Is buying business premises through super realistic? Would you be better off improving your current fund instead? Those are the questions worth answering first.

A good process should feel clear and orderly. Quick initial discussion. Proper fact-finding. Strategy before paperwork. Then implementation only if the numbers and the purpose stack up.

If you want clear advice on whether an SMSF suits your situation, book an initial conversation with Wealth Collective. It’s a practical first step for WA professionals and business owners who want their super to work with their broader wealth plan, not sit off to the side.