Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A decent windfall can create a strange kind of stress. You sell an investment property, your business throws off surplus cash, or an inheritance lands in your account, and suddenly the question isn't how to get money. It's where to put it so it improves your life later.

For a lot of people in Perth, Dunsborough, and across WA, the smartest answer is super. Not by dribbling money in slowly, but by using the Bring Forward Rule properly and moving a larger amount at the right time. That's where this rule stops being a technical ATO detail and starts becoming a serious planning opportunity.

Used well, it can help you get more money into the super system sooner. Used badly, it can lock you into the wrong move, trigger avoidable mistakes, or leave you thinking you had more room than you did. If you need a refresher on the basics of super before tackling the strategy side, this guide on superannuation in Australia is a useful starting point.

A Super Way to Boost Your Retirement Savings

A common WA scenario looks like this. You're in your late 50s or early 60s, you've sold an asset, and cash has hit your bank account. It might be a beach house, a commercial property, a parcel of shares, or the final proceeds from winding down a business interest.

Leaving that money sitting in cash usually isn't the answer. Nor is making a rushed investment decision because the balance suddenly looks too large in your everyday account. The more practical question is whether some of that money belongs inside super, where it can support your retirement instead of drifting into ad hoc spending or poorly timed investments.

That's why the bring forward rule matters. It exists to let eligible Australians make larger after-tax contributions in one year, rather than waiting and spreading them out over future years. As Passive Investing Australia explains in its bring-forward rule guide, the bring-forward rule is designed to help Australians with lower super balances accelerate their retirement savings by making larger contributions in a single year without incurring additional tax penalties.

Why this matters in real life

For pre-retirees, this can be the difference between entering retirement with a stronger super balance or missing the window while balances rise and eligibility narrows.

For business owners, it can be even more useful. A profitable year, an asset sale, or a business exit often creates a rare funding opportunity. You might not get many chances to move a meaningful lump sum into super. When that chance appears, timing matters.

Practical rule: If a large sum has arrived and retirement is getting closer, don't treat super as an afterthought. Review your contribution options before you invest, gift, or spend the money elsewhere.

The rule isn't complicated once you strip out the jargon. But it does demand precision. Age, balance thresholds, and contribution timing all matter. Get those right, and this becomes one of the cleaner ways to strengthen your retirement position.

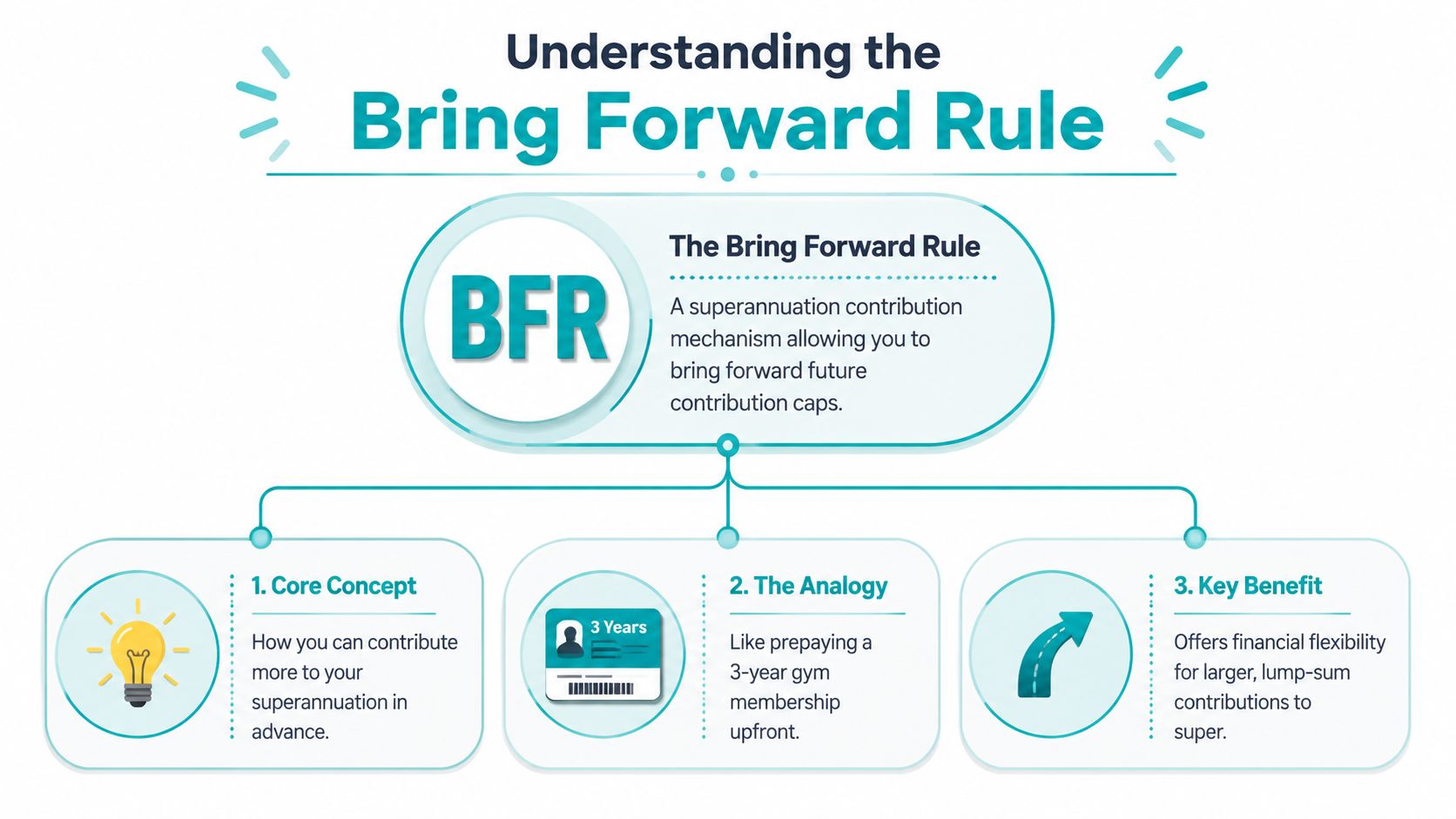

What Is the Bring Forward Rule

The simplest way to think about the bring forward rule is this. You're effectively prepaying future contribution caps, much like paying for a multi-year membership upfront instead of one year at a time.

Normally, non-concessional contributions are limited by an annual cap. Under the bring forward rule, eligible people can use more than one year's cap in the current financial year. That's what makes a lump-sum contribution possible.

The core mechanism

For the 2026 to 2027 financial year, the annual non-concessional contribution cap is $130,000, and the bring forward arrangement is automatically triggered if an eligible person under 75 contributes more than that amount in a single financial year, as outlined by SuperGuide's explanation of the bring-forward rule.

That automatic trigger is important. You don't fill out a special form to switch it on. If you're eligible and your contribution goes over the annual cap, the rule is activated.

In plain English, that means you can't casually go a little over and assume you'll sort it out later. The system treats that as a deliberate event.

What the rule lets you do

The attraction is simple. If you have the capacity and you're eligible, you can move a much larger after-tax amount into super in one hit instead of waiting year by year.

That can suit people who:

- Receive a lump sum from an inheritance, bonus, property sale, or business proceeds

- Want to act before retirement so more assets sit inside super sooner

- Prefer decisive action rather than stretching a contribution plan across multiple years

- Need to use a narrow window before age or balance limits reduce flexibility

The bring forward rule isn't about making super more exciting. It's about making a one-off opportunity count.

What it doesn't mean

It doesn't mean everyone should contribute the maximum possible amount. It doesn't mean every windfall belongs in super. And it definitely doesn't mean the tax result is the only thing that matters.

Super is powerful, but it's also a long-term structure. Once money goes in, access rules apply. That's why the best use of the rule sits inside a broader plan, not a last-minute transfer done because someone at a barbecue mentioned “you can put three years in at once”.

Who Can Use the Rule in 2026

A lot can change with one date on the calendar.

A Perth business owner might sell part of the business in May 2027 and expect to tip a large amount into super before 30 June. A pre-retiree might downsize, free up cash, and assume the full bring forward amount is still available. Both can be wrong if they ignore the two tests that matter. Your age, and your Total Super Balance on 30 June 2026.

Get either one wrong and the strategy changes fast.

The age test

For 2026 to 2027, the bring forward rule is generally available if you are under 75 in the year the contribution is made. There is also a strict deadline if you are turning 75. Contributions must be made no later than 28 days after the end of the month in which you turn 75, as noted earlier.

That deadline matters most for people near retirement who are acting on a narrow window. If you are 74 and planning to contribute after a property sale, business sale, or inheritance, timing is not an admin detail. It is the strategy.

The balance test

Your Total Super Balance on 30 June 2026 decides how much bring forward capacity you have for 2026 to 2027. If you want a clearer explanation of the contribution type involved, read our guide to non-concessional contributions.

Here is the practical reference point for 2026 to 2027:

| Total Super Balance (on 30 June 2026) | Bring-Forward Period | Maximum Contribution (2026-27) |

|---|---|---|

| Less than $1.84 million | 3 years | $390,000 |

| $1.84 million to less than $1.97 million | 2 years | $260,000 |

| $1.97 million or more | No bring-forward period | $130,000 |

These tiers are not academic. They directly affect what you can do with a lump sum.

If your balance is below $1.84 million, you have the full three-year capacity. That is the strongest position for a WA pre-retiree who wants to move sale proceeds or surplus cash into super while access to the contribution still exists.

If your balance sits in the middle range, you still have room, but less of it. That often matters for established business owners who have built super steadily over time and assume they still have the full amount available. They often do not.

If your balance is $1.97 million or more, the full bring forward strategy is off the table. You are limited to the standard annual non-concessional cap, assuming you are still otherwise eligible to contribute.

What this means in real life

This rule rewards people who plan before the money arrives.

If you are a pre-retiree in WA and expect a property sale, redundancy payment, or inheritance, check your 30 June balance before you commit to a contribution plan. If you are a business owner preparing for a sale or a strong profit year, review your cap position early, not after the funds hit your account.

The people who get the best result from the bring forward rule are usually not the people with the most cash. They are the people who checked eligibility early enough to use it properly.

How the Bring Forward Rule Works in Practice

Theory is easy. Real life is messier. The bring forward rule only becomes useful when you apply it to an actual person with an actual decision to make.

The pre-retiree with a property sale

Sam is 62 and has sold an investment property. He wants to move a significant portion of the proceeds into super before fully retiring.

If Sam's Total Super Balance on the relevant balance date is below the lower threshold, he may have access to the full three-year bring-forward amount. That makes the rule a strong fit because he has a one-off influx of cash, he's close to retirement, and he wants more money inside the super environment before he stops work.

In this context, the strategy excels. The asset sale creates liquidity. Retirement creates urgency. The bring forward rule can connect the two.

The high-income earner with a bonus

Rachel is 45, works in a senior executive role, and has received a large bonus. She doesn't need that money for day-to-day living, and she wants to push part of it toward long-term wealth.

The bring forward rule can work here, but only if the contribution suits her wider plan. A high income doesn't automatically mean a large non-concessional contribution is smart. She still needs to weigh cash reserves, mortgage strategy, investment goals, and upcoming tax commitments.

For someone like Rachel, the rule is often most useful when she has surplus capital and wants to make a decisive move rather than drip-feed contributions.

The young professional with an inheritance

Liam is 35 and has inherited money earlier than expected. He wants to “do something sensible” with it, which is usually how people phrase the moment before they either make a smart move or a regrettable one.

For a younger client, the bring forward rule can be powerful because time does the heavy lifting once the money is inside super. But that doesn't mean he should tip every available dollar into it. He may still need funds outside super for a home, family plans, or business opportunities.

A younger client needs balance more than maximum contribution. The right move is usually the one that strengthens future retirement without starving present flexibility.

The business owner after a sale

Nina is 55 and has sold her business. She now has a rare window where personal wealth planning matters more than business structuring.

If her balance leaves room under the relevant threshold, the bring forward rule can help her shift a meaningful amount into super while she still has age-based eligibility and clear capital to work with. Business owners often delay this conversation too long because they're focused on the deal itself. That's a mistake. The sale is only half the job. What happens after settlement matters just as much.

A lump sum creates options, but options decay when you leave them untested. The best contribution window is often the one right in front of you.

The practical takeaway from these examples

Different people use the rule for different reasons, but the pattern is consistent:

- Pre-retirees use it to improve retirement readiness while time still allows.

- Executives use it when a bonus or surplus income creates excess capital.

- Younger professionals use it selectively to get ahead without overcommitting.

- Business owners use it when a sale or profit event opens a short, valuable window.

The key point isn't the client profile. It's the timing of the cash event and whether the contribution fits the person's bigger plan.

Strategic Timing and Tax Implications

The usual focus is on the cap. Smart planning focuses on timing.

The bring forward rule rewards people who act before their options narrow. Delay can cost flexibility. That's not theory. It's built into how the balance thresholds work.

Why timing matters so much

As noted in this discussion of carry-forward concessional contributions, contribution strategies often work best when they're coordinated rather than considered in isolation.

The same applies here. The tiered eligibility of the bring forward rule creates a direct cause-effect: higher super balances progressively restrict access to the mechanism, incentivising earlier contributions before balance thresholds are breached, as explained in this bring-forward rule discussion.

That's the central planning point. If your balance is likely to rise, waiting may reduce what you can do later.

Good timing usually looks like this

Some contribution decisions are obvious in hindsight. The problem is that clients only get one chance to make them in real time.

Consider using the rule when:

- A lump sum has just arrived from a sale, inheritance, or bonus and you already know part of it is long-term capital.

- Retirement is approaching and you want more assets positioned inside super before you stop working.

- Your balance is still below a threshold but may not stay there.

- You're coordinating with a spouse and want to decide which balance, owner, and timing makes the most sense.

- You want cleaner planning instead of revisiting the same question every financial year.

The tax side in plain English

These are after-tax contributions. That matters because the money has generally already been taxed before it enters super.

The strategic attraction isn't an instant deduction from this contribution type. It's the long-term value of getting money into the super system in a deliberate way, especially for clients who are tightening their retirement structure and want more of their wealth organised efficiently.

Don't confuse “after-tax contribution” with “no tax planning value”. The value often sits in where the money lives next, not in a same-day deduction.

What I'd recommend

If you're clearly eligible and sitting on a genuine lump sum, don't leave this to the last week of June. Confirm your balance position, check contribution room, and decide whether acting now is better than waiting.

If your balance is near a threshold, be even more decisive. In practice, the bring forward rule is often less about squeezing out the absolute maximum and more about acting while the door is still open.

Common Pitfalls to Avoid

The bring forward rule is simple enough to understand and easy enough to mishandle. Most errors don't happen because the rule is obscure. They happen because people assume “close enough” is good enough.

It isn't.

The most common mistakes

Accidentally triggering the rule

A contribution just over the annual cap can trigger the arrangement automatically. People sometimes think a small overpayment is harmless. It's not. Once triggered, you're operating under bring-forward rules whether that was your plan or not.Ignoring the lock-in effect

When you trigger the rule, you're not just making a bigger contribution. You're using future cap space. If you don't think ahead, you can leave yourself with less flexibility in later years than you expected.Using the wrong Total Super Balance

Clients often estimate from memory, or they focus on one fund and forget another. That's dangerous. Eligibility depends on Total Super Balance, not the balance of the fund you happen to log into most often.Missing the age timing

If you're close to the age limit, the calendar matters. Delay can turn a valid strategy into a missed opportunity.

What to do instead

A better process is boring, which is exactly why it works:

- Confirm the exact balance position using full super records, not a rough guess.

- Check contribution history before moving money.

- Model the next few years, not just the current one.

- Review access needs so you don't push too much into a structure you can't tap easily.

The mistake I see most often

People treat super contributions as an admin task. They're not. They're a strategy decision.

A rushed contribution made because “the accountant mentioned it” or “someone said I could do three years at once” is how otherwise sensible people create preventable problems. The bring forward rule is useful precisely because it's powerful. Power without context is what gets people into trouble.

If your contribution plan depends on rough numbers, memory, or assumptions, stop. Verify first, contribute second.

Build Your Retirement Roadmap with Wealth Collective

A good bring forward strategy can change the trajectory of retirement planning. I see that most often with Perth pre-retirees who have just sold an investment property, and with WA business owners coming off a sale, dividend, or unusually strong year. The opportunity is real, but the window can be short, and poor timing can cost you flexibility you will want later.

The rule matters less than the decision around it. The key question is whether this is the right year to contribute, how much should go in, and what that does to your tax position, cash reserves, and future contribution options.

That is the job of advice.

Wealth Collective provides practical advice that connects super strategy with the bigger picture. For clients nearing retirement, the Retirement Roadmap process maps contribution timing, pension planning, asset structure, and retirement income so each decision supports the next one. For clients still building wealth, Guided Growth brings super, investing, debt reduction, and cash flow into one plan instead of treating them as separate tasks.

If you have recently sold a WA business, received an inheritance, or are weighing up whether to contribute proceeds from a property sale, get the numbers checked before you move money. The right plan can help you use the bring forward rule at the right time. The wrong move can leave too much capital locked away, trigger avoidable mistakes, or waste a one-off contribution window.

If you want clear advice on whether the bring forward rule fits your situation, book a free initial call with Wealth Collective. We will pressure-test the strategy against your actual balance, timing, tax position, and retirement goals, then show you what to do next.