Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A lot of WA business owners hit the same point. Revenue is solid, the team is growing, and the business looks successful from the outside. But behind the scenes, cash flow feels tighter than it should, tax decisions keep getting deferred, super sits in the background, and there’s no clear line between building the business and building personal wealth.

That tension is common in Perth, Dunsborough, and across regional WA. A business owner in professional services might be drawing well but still not know whether their structure is helping or hurting them. A trades business owner may be reinvesting heavily without a proper plan for debt reduction or retirement. An executive with equity or bonus income may have strong earnings and weak integration between tax, super, insurance, and long-term planning.

That’s where business advisory services matter. Done properly, they’re not a nicer label for compliance work. They’re a working relationship that connects your business decisions to your personal financial life, so growth doesn’t stay trapped inside the business.

Navigating Your Business Beyond the Balance Sheet

A WA owner can be doing almost everything right and still feel uncertain. You might know your numbers well enough to run the month, approve wages, chase receivables, and make payroll. What often gets missed is the bigger question. Is the business taking you where you want to go personally?

In Western Australia, that gap shows up in practical ways. A mining services contractor has lumpy income and wants more stability at home. A retail operator has built a valuable business but hasn’t sorted succession. A dual-income family has decent earnings and rising complexity, yet no clear retirement roadmap. Generic advice doesn’t usually solve that, because generic advice treats the business, the family balance sheet, and the future exit as separate files.

The WA context matters here. Total superannuation assets in Australia reached AUD 3.9 trillion, with Western Australia contributing about AUD 331.5 billion, which underlines why integrated super and retirement advice matters locally. The same data notes that small business owners make up 25% of advisory clients in this space, reflecting how often business and personal planning overlap in practice, as outlined in this WA advisory market overview.

What owners usually need

Most business owners who seek advice aren’t looking for theory. They want help with decisions such as:

- How much to draw versus reinvest so the business grows without starving personal wealth.

- Whether the current structure still fits as profit, staff count, and family goals change.

- How to reduce risk exposure if illness, death, or a major interruption affects income.

- What retirement looks like if a large share of net worth sits inside the business.

Practical rule: If your business is growing but your personal financial position still feels vague, your issue usually isn’t effort. It’s lack of integration.

Strong business advisory services give owners a way to manage that integration. The balance sheet still matters. So do tax returns, BAS, lending, and forecasting. But the core value comes from connecting those moving parts to choices about super, debt, succession, protection, and retirement timing.

What good advice changes

The best advisers don’t just tell you whether the business is profitable. They help you decide what to do next, what trade-offs you’re making, and what those trade-offs mean for your family over time.

That’s the shift. Business advisory stops being a cost line and starts becoming a decision-making framework. For many WA owners, that’s the difference between running a successful business and converting that success into lasting wealth.

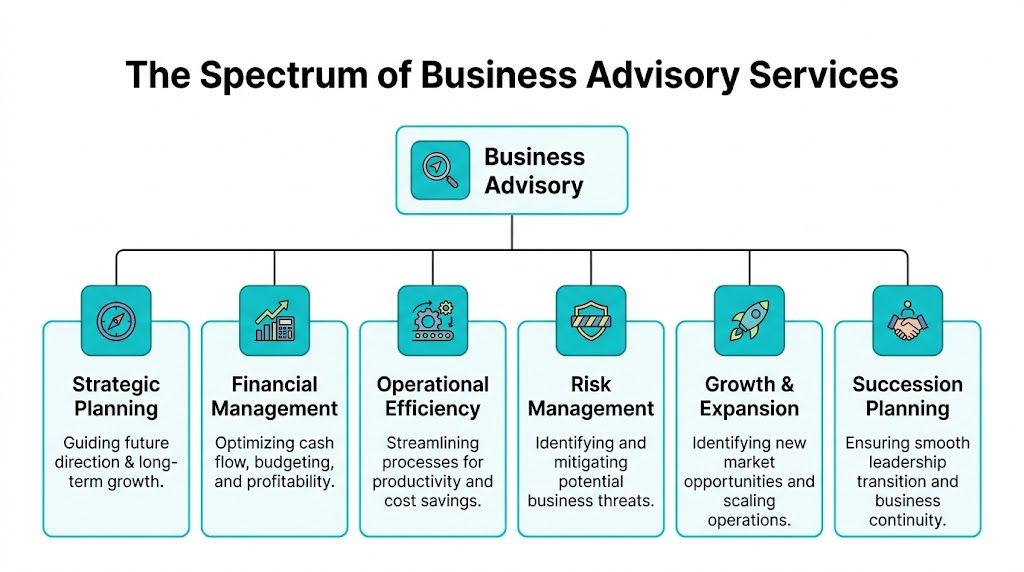

The Spectrum of Business Advisory Services Explained

Business advisory services cover far more than year-end tax work. At their best, they bring structure to decisions that would otherwise stay reactive. That includes strategy, cash flow, tax, super, risk, and succession.

A simple way to think about it is this. Compliance tells you where you’ve been. Advisory helps decide where you’re going, and what needs to happen in the business and outside it to get there.

Strategic and financial advisory

This is the operating core. It deals with cash flow, margins, debt pressure, reinvestment, working capital, and growth choices. For a Perth consultancy, that may mean deciding when to hire. For a Dunsborough hospitality business, it may mean building buffers for seasonal revenue swings.

A good adviser doesn’t just produce forecasts. They pressure-test assumptions. If revenue softens, what gives first. If you buy equipment, what does that do to available cash. If owners keep drawing at the current level, does that weaken the balance sheet or reflect a healthy business.

For owners who want a practical starting point, this guide to small business cash flow management is useful because it focuses on the day-to-day mechanics that often trigger the need for broader advice.

Tax and superannuation integration

Standard advice often falls short. Plenty of firms can lodge returns and explain deductions. Fewer can connect business structure, profit extraction, concessional contributions, SMSF suitability, and retirement timing into one strategy.

That gap matters in WA. A key gap in standard advice is integrating business succession with superannuation. ATO data shows that 15% of WA small business owners use SMSFs for retirement, yet only 25% receive customized advice on structuring a business exit in a tax-efficient way that optimises super, as noted in this piece on integrated succession and super advice.

If succession is the bridge to retirement, super is often the foundation underneath it. You need both designed together.

Risk and protection

Most business owners understand risk in theory and underinsure in practice. They cover the obvious assets, then leave major exposure sitting around key people, income interruption, debt servicing, or family cash flow if something goes wrong.

This part of advisory asks harder questions. If one owner can’t work, does the business keep trading. If revenue drops suddenly, what expenses become dangerous. If the owner dies or is disabled, does the family inherit clarity or chaos.

The businesses that hold up under pressure usually made their protection decisions before they felt urgent.

The trade-off here is straightforward. Premiums and policy design can feel like a drag on cash flow. But no owner wants to discover, during a claim event, that cover was thin, outdated, or disconnected from the actual structure of the business.

Succession and exit planning

Many owners treat succession as a future issue. In practice, it affects decisions now. Entity structure, debt levels, retained earnings, ownership records, and super planning all shape what an exit will look like later.

This isn’t only about selling. It also includes family transition, management handover, staged retirement, or winding down in a way that protects accumulated wealth.

A useful cross-industry perspective comes from broader business consulting services, especially where operational strategy and long-term planning intersect. The key difference in Australia is that business owners also need the tax and super rules built into that advice from the start.

Operational efficiency and growth

Some firms also pull in process improvement, technology, reporting cadence, and decision dashboards. That’s worthwhile when the business is growing faster than the owner’s current systems.

What works is simple reporting tied to real choices. What doesn’t work is a beautiful dashboard no one uses. Advisory only adds value when it changes decisions, habits, or timing.

The Advisory Process From Initial Call to Action Plan

One reason business owners delay getting advice is uncertainty about what the engagement looks like. They assume it will be slow, jargon-heavy, or overly theoretical. Good advisory should be the opposite. Clear, structured, and directly tied to decisions.

The first conversation

The opening call should be short and practical. Its job isn’t to solve everything. It’s to establish fit.

A capable adviser will ask where the pressure is showing up. That could be inconsistent cash flow, uncertainty around super, business debt, family protection, or no credible retirement path. They should also be honest if the issue is compliance, not advisory.

The deep dive

Once there’s a fit, the main work starts. This stage gathers the documents and context that matter, financial statements, debt details, super balances, ownership structures, insurance, family commitments, and goals that often never make it into spreadsheets.

This is also where assumptions get challenged. Owners often say they want growth when what they really want is more freedom. They say they want to retire at a certain age when they haven’t calculated what that would require. A proper discovery process surfaces those mismatches early.

The strategy blueprint

The output here should be specific. Not generic goals, and not a long report filled with technical language that no one acts on.

A useful advisory plan usually covers:

- Immediate priorities such as cash flow pressure, debt concerns, or protection gaps.

- Structural decisions around entities, tax position, super contributions, and profit extraction.

- Medium-term actions such as investment planning, succession design, or debt reduction.

- Review points so the strategy adjusts as business conditions and family circumstances change.

What to look for: If the adviser can’t explain the plan in plain English, the strategy probably isn’t ready for implementation.

Implementation

At this stage, many plans fail. The advice may be sound, but nobody owns the sequence. Documents sit unsigned. Super changes don’t happen. Insurance applications stall. Debt restructuring gets delayed by day-to-day business demands.

Strong advisers narrow the action list and set an order. They coordinate with accountants, lenders, solicitors, and platform providers where needed. They also know when not to do too much at once. Owners don’t need ten simultaneous changes. They need the right first three.

Ongoing review

Business conditions change. So do tax rules, profit levels, debt profiles, and family priorities. Advisory should operate as a live process, not a one-off event.

A review meeting should answer practical questions. Did cash flow improve. Are contributions happening as planned. Has risk reduced. Is the owner closer to the desired exit position. If the plan isn’t moving behaviour or outcomes, it needs adjusting.

The best process feels steady, not dramatic. It gives owners a way to act with less friction and more confidence.

The Real ROI of Strategic Advice for WA Businesses

The return from business advisory services isn’t just higher profit. That can happen, but it’s too narrow a test. The deeper return is better survival, stronger decision quality, cleaner risk management, and a clearer path from business effort to personal wealth.

That matters in WA because many owners carry concentrated risk. Their income comes from the business. Their future wealth depends on the business. Their retirement may depend on selling, transferring, or drawing from the business. When all those roles sit in one asset, advice has to do more than tidy up reporting.

What the numbers support

There’s a strong case for advice when you look at business resilience and long-term outcomes. SMEs that engage professional advisers are 35% more likely to survive five years, and their revenue growth is 15% higher than non-advised peers. For high-income earners in WA, personalized advisory has been shown to boost net worth by an average of 22% over a decade, according to this Australian advisory market report.

Those figures don’t mean every adviser creates the same outcome. They do show the pattern. Businesses and households that make structured decisions, with outside perspective and proper implementation, tend to perform better than those that stay reactive.

Where ROI actually shows up

Owners often expect ROI to arrive as one visible win. In practice, it usually appears across several areas at once.

- Cash preserved: Better timing on tax, debt, and drawings leaves more room in the business.

- Risk reduced: The family and the business aren’t carrying silent exposures that could undo years of work.

- Super used properly: Contributions, structure, and investment settings become intentional rather than incidental.

- Exit value protected: Succession planning starts early enough to avoid rushed decisions later.

A practical tax angle often forms part of that return. This overview of small business tax reduction is a reminder that tax strategy works best when it’s linked to broader business and personal planning, not treated as a stand-alone exercise.

What works and what doesn’t

What works is disciplined advice tied to actual decisions. Monthly reporting that informs owner drawings. Super planning that matches business profitability. Insurance that reflects debt obligations and family reliance. Succession planning before fatigue or health forces the issue.

What doesn’t work is fragmented advice. One professional handles tax. Another handles investments. Insurance sits somewhere else. No one coordinates the trade-offs. The owner gets plenty of documents and very little alignment.

Owners don’t need more opinions. They need one integrated strategy that holds together under pressure.

That’s also why generic entrepreneurial content has limits. There’s value in broad perspectives like these best advice for entrepreneurs, especially around mindset and leadership. But once an owner is making real money, carrying debt, building super, and thinking about succession, the work becomes technical and local.

The practical business case

If an adviser helps a business owner avoid poor drawings, tighten debt strategy, improve super settings, and build a workable retirement plan, the return isn’t abstract. It changes the owner’s options.

They can invest with more confidence. They can decide whether to expand or consolidate. They can protect the family balance sheet. They can stop hoping the business will somehow become the retirement plan and start designing a path that works.

That’s the actual ROI. Better numbers matter. Better choices matter more.

Key Signs It Is Time to Hire a Business Adviser

Many owners wait too long because they think advice is only for distressed businesses or very wealthy families. Usually, the right time is earlier. The trigger isn’t failure. It’s complexity.

Your business and personal finances are too intertwined

If your household decisions depend on irregular business cash, you need structure. That doesn’t automatically mean the business is unhealthy. It often means the owner has outgrown a simple approach.

The warning sign is when you can’t clearly answer basic questions. How much can I draw. What should stay in the business. Am I using super properly. If the answer to each is some version of “it depends” but nobody has modelled it, that’s advisory territory.

Debt is following you toward retirement

For pre-retirees in WA, debt is a major trigger for getting help. WA households aged 55 to 64 carry average non-housing debt of AUD 42,500, which is 17% above the national average. Without an advisory-led debt reduction strategy, this can erode retirement nest eggs by up to 18%, according to this analysis on WA debt pressure and retirement planning.

That’s not a small planning issue. It changes retirement timing, investment flexibility, and how much pressure remains on the business to keep funding lifestyle needs.

Growth is creating strain rather than confidence

Growth can hide problems for a while. Revenue improves, but systems lag behind. Owner decisions stay trapped in their head. Tax and super planning don’t keep pace. The business gets larger and less controlled at the same time.

Common signs include:

- Cash flow surprises: Profit looks acceptable, but cash is regularly tight.

- Slow decisions: You delay hires, purchases, or structure changes because the consequences aren’t clear.

- No risk framework: Insurance and protection have been set once and then ignored.

- Owner fatigue: You’re making too many financial calls without a clear model.

You have no genuine exit plan

A vague idea that you’ll “sell one day” isn’t a succession plan. Neither is assuming the kids will take over or that the business will fund retirement because it always has.

If your business is meant to finance retirement, then retirement planning has to begin while the business is still healthy and under your control.

You’re earning well but still feel disorganised

This is common with executives, professionals, and dual-income households. Income is strong. The problem is coordination.

If your super, tax, debt, investments, and protection are all moving separately, you may be doing fine on paper while wasting opportunities in practice. That’s often the point where business advisory services become less about fixing a problem and more about creating order before small inefficiencies turn into expensive ones.

Choosing the Right Adviser in Western Australia

Not all advisers work the same way. Some are excellent at compliance and weak on strategy. Some can discuss investment markets but can’t connect that advice to business structures, succession, or super. Others rely on broad recommendations that don’t reflect how WA business owners operate.

The right adviser should be able to sit in the overlap between your business and your personal financial life. This is the critical test.

Start with integration, not personality

A good relationship matters, but chemistry alone isn’t enough. You need someone who can explain how they connect business cash flow, tax, debt, super, insurance, and retirement planning.

That’s especially important if a large portion of your wealth is tied to the business. Many owners have one adviser for the company and another for personal planning. That can work, but only if someone is taking responsibility for integration. If nobody is, things fall through the gaps.

A practical due-diligence resource is this guide on how to choose a financial advisor. It helps clarify the questions owners should ask before committing.

Ask how they handle super optimisation

This is one of the clearest ways to separate generic advice from specialist advice. A top-quartile adviser can demonstrate how they reduce superannuation fees from an average of 1.05% p.a. to below 0.50% using strategies like SMSFs, boosting net returns by 22-35% over 5 years, as described in this piece on super fee reduction and business owner advice.

The important part isn’t the headline result. It’s whether the adviser can explain their method clearly. You want to hear how they assess suitability, fee trade-offs, compliance burden, investment governance, and the circumstances where an SMSF is a poor fit.

Look for transparency on fees and scope

Owners should understand what they’re paying for, how advice is delivered, and what happens after implementation. Vague fee explanations are a warning sign.

Ask whether the engagement is project-based, ongoing, or both. Ask what gets reviewed regularly. Ask whether the adviser coordinates with your accountant and solicitor or expects you to join the dots. Good advisers won’t avoid these questions.

Questions worth asking in the first meeting

Use the first meeting to test clarity, not to be impressed by jargon.

| Question Category | Specific Question to Ask |

|---|---|

| Business integration | How do you connect business performance with my personal wealth plan? |

| Cash flow | What would you want to review first in my business to assess cash pressure and owner drawings? |

| Superannuation | How do you decide whether an SMSF or another super structure is appropriate for a business owner? |

| Tax strategy | How do you coordinate tax planning with super contributions and profit extraction? |

| Risk management | What risks do you usually see overlooked by owner-managed businesses in WA? |

| Succession | How early should I start planning for exit, sale, or family transition? |

| Implementation | Who helps execute the strategy once the advice is agreed? |

| Review process | How often do you review plans, and what would cause you to change course? |

| Client fit | What type of clients are not a good fit for your process? |

What strong answers sound like

Strong answers are direct. They acknowledge trade-offs. They don’t promise a universal fix.

For example, a serious adviser won’t say every business owner should use an SMSF. They’ll explain when it helps, when costs outweigh benefits, and what responsibilities come with control. They’ll also recognise that succession planning can conflict with short-term tax minimisation, and they’ll tell you which objective they’d prioritise and why.

The right adviser makes complexity easier to act on. The wrong adviser makes simple decisions sound complicated.

Local knowledge still matters

Western Australia isn’t one market. Perth professionals, regional operators, family businesses, mining-linked contractors, and pre-retirees all face different planning realities. A capable adviser should understand those differences and adjust accordingly.

That local judgement is often what turns a technically correct recommendation into one that works in practice.

Build Your Wildly Successful Financial Life Today

Business success on its own doesn’t guarantee financial freedom. Plenty of owners generate strong income and still feel exposed, overextended, or unclear about the future. The missing piece is usually integration.

That means treating the business as part of your broader financial life, not as a separate world. Cash flow decisions affect your household. Tax choices affect your investment capacity. Super strategy affects retirement timing. Protection decisions affect whether your family keeps options if something goes wrong. Succession planning affects whether years of effort turn into usable wealth.

Business advisory services are most valuable when they solve that whole problem. Not by adding more paperwork, but by helping you make better decisions in the right order. Some owners need to start with protection. Others need a tighter growth strategy, cleaner debt reduction, or a realistic retirement roadmap. The exact starting point changes. The principle doesn’t.

If you’re a WA business owner, executive, or pre-retiree and your finances feel more complicated than they should, that’s a signal worth acting on. The right advice can help you protect what you’ve built, grow with more confidence, and move toward retirement with a plan that makes sense.

Wealth planning works best when it’s practical. Clear actions. Clear trade-offs. Clear accountability. That’s what turns a good income or a good business into a financial life that feels organised, durable, and under your control.

If you want help turning business momentum into personal wealth, speak with Wealth Collective. Their Perth and Dunsborough team helps clients across Protection Plus, Guided Growth, and Retirement Roadmap, with a simple process that starts with a complimentary 10-minute call.