Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Most Australian business owners will leave their business only once. They do not get a practice run. That is why your exit strategy deserves attention years before a sale, handover, or health event forces the issue.

Your business exit strategy is not a formality to park in a drawer. It is a core part of your personal retirement plan. For many owners in Perth and across WA, the business will fund the lifestyle they want after work stops, top up super, clear debt, and support family goals. If that exit is poorly planned, retirement carries the cost.

Too many owners focus on revenue, staff, tax, and day-to-day pressure, then treat the exit as a transaction at the end. That approach leaves money on the table and creates avoidable stress at the point when the stakes are highest. A sale price matters, but it is only one part of the outcome. The structure of the deal, the tax position, the timing, and your plan for life after ownership matter just as much.

At Wealth Collective, we see business exit planning through a broader retirement lens. The sale is one event. Your Retirement Roadmap is the bigger job. It needs to answer two questions clearly. How will this business convert into lasting financial security, and who are you when you are no longer the owner making every decision?

A practical exit strategy for small business starts with options, timing, and transferability. It also depends on the financial habits inside the business today, especially small business cash flow management systems that support transfer value.

Get this right, and your exit can fund freedom with confidence. Get it wrong, and a strong business can still produce a disappointing personal result.

Why Your Business Exit Strategy Needs to Be a Priority Now

That lack of planning has real-world consequences. Owners who delay exit planning usually accept weaker terms, pay more tax than necessary, and realise too late that the business is too dependent on them to transfer cleanly.

This is not just a business issue. It is a retirement issue.

For many owners in Perth and across WA, the business is the largest asset outside the family home. It is expected to fund income in retirement, clear debt, top up super, and give the family options. If that asset is not prepared well in advance, the shortfall shows up in your personal life, not just in the sale process.

That is why I treat exit planning as part of a broader Retirement Roadmap, not a standalone transaction. The sale matters, but the bigger question is what the proceeds need to do for the next 20 or 30 years. Your exit strategy should answer that clearly. How much do you need after tax? What level of risk can you afford to take after the sale? What does life look like when the business no longer sets your identity, routine, and income?

A practical exit strategy for small business starts with timing, transferability, and realistic options. It also starts earlier than owners think. Clean reporting, reliable margins, and disciplined small business cash flow management systems that support transfer value make a direct difference to buyer confidence and deal quality.

Here is the blunt truth. A profitable business is not automatically sale-ready.

Buyers pay well for a business that can perform without the owner, produce clean numbers, and survive proper due diligence. If your business relies on your relationships, your judgement, and your daily intervention, the value is lower than you think. In many cases, the owner has built themselves a job with staff, not an asset that can be transferred at a premium.

Priority matters because time gives you choices. It gives you time to strengthen systems, reduce owner dependence, sort out shareholder issues, clean up the balance sheet, and structure the exit around your tax and retirement goals. It also gives you space to prepare for the human side of the sale, which many generic guides ignore. Owners often underestimate how hard it is to step away from the role that has defined them for decades.

Start early and you stay in control. Leave it late and the market, a health event, burnout, or a dispute can set the timetable for you.

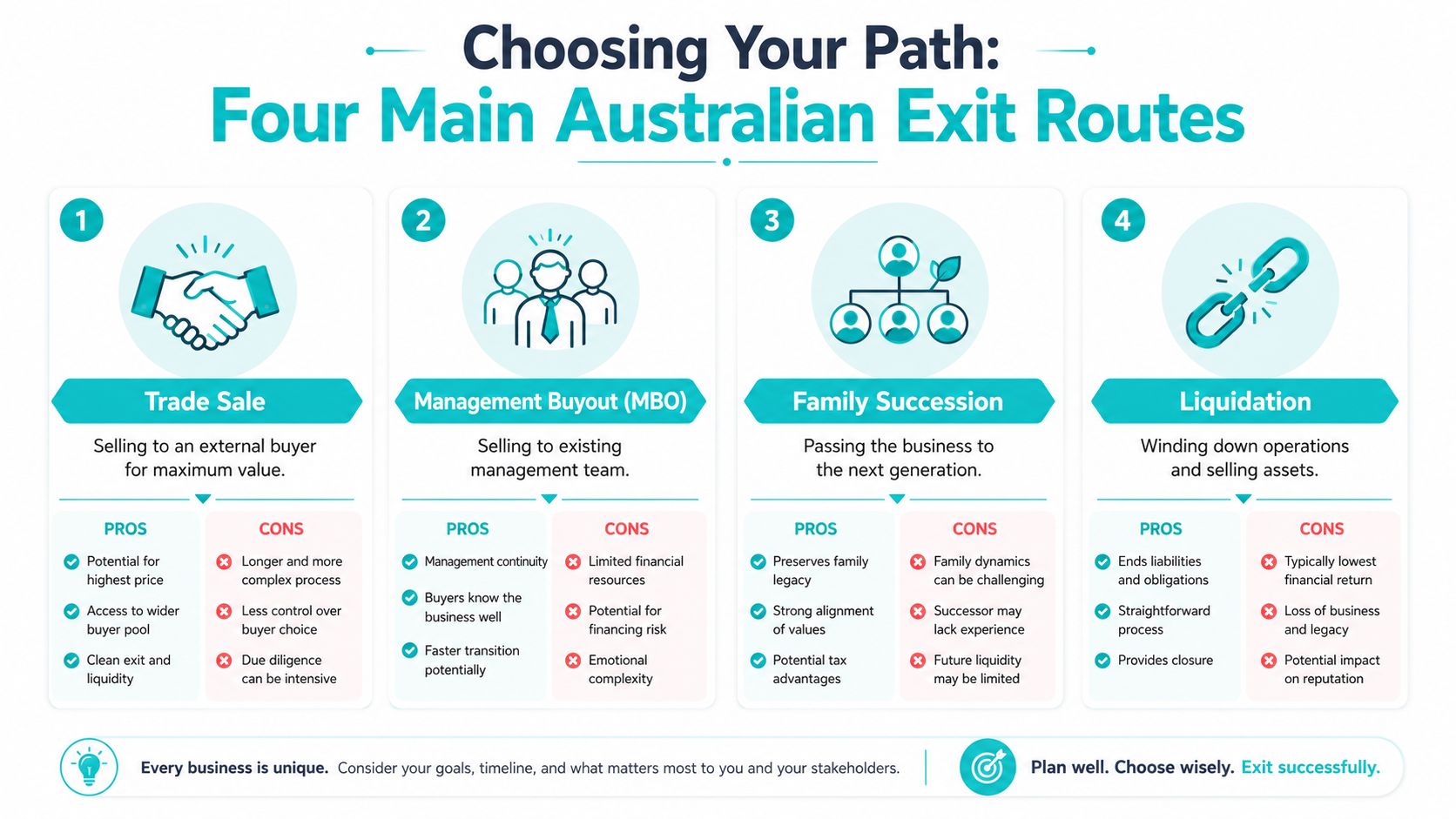

Choosing Your Path The Four Main Australian Exit Routes

Not every owner should sell to the highest bidder. Some want maximum value. Others want continuity for staff, a family legacy, or a clean break. The right route depends on what you value most.

The four routes in plain English

A trade sale means selling to an external buyer. That could be a competitor, a strategic acquirer, or an investor. This route usually appeals to owners focused on value and liquidity.

A management buyout means the existing leadership team acquires the business. This often suits firms with capable operators already inside the business and owners who care about continuity.

Family succession keeps the business in the family. It can preserve legacy, but it only works when the next generation is willing, capable, and aligned. Sentiment doesn't run a company.

Liquidation is the final route. You close operations and sell assets. This is usually the least attractive option if your aim is to preserve goodwill, staff continuity, or enterprise value, but sometimes it's the cleanest path when the business isn't effectively transferable.

Comparison of Business Exit Strategies

| Exit Option | Potential Value | Timeline | Control Retained | Ideal For |

|---|---|---|---|---|

| Trade Sale | Often strongest where a buyer sees strategic value | Usually longer and more demanding | Lower after completion | Owners focused on maximum sale proceeds |

| Management Buyout (MBO) | Can be solid, depending on funding and team capability | Moderate | Often more influence during transition | Owners wanting continuity with existing leaders |

| Family Succession | Financial outcome varies widely | Often longer due to family and structural issues | Higher during staged handover | Owners prioritising legacy over immediate liquidity |

| Liquidation | Usually limited to asset realisation | Can be quicker | High during wind-down | Owners wanting a clean exit where transfer value is low |

How to choose without fooling yourself

Ask yourself four blunt questions:

- What matters more, price or legacy: If maximum after-tax wealth is the priority, don't pretend family succession is automatically the best answer.

- Can the business survive without you: If not, the path narrows quickly.

- Do you want a staged transition or a sharp break: Some owners need time to hand over relationships and responsibilities.

- Are you protecting employees, family, or your own retirement first: You can care about all three, but one goal usually leads.

The wrong exit route often starts with an emotional preference and ends with a financial compromise.

The route must fit the business you actually have

Many owners say they want a management buyout, but their team can't lead commercially. Others assume the kids will take over, but no one has asked whether the kids even want it. Some expect a premium third-party sale while carrying untidy accounts, concentrated revenue, and undocumented systems.

Your business exit strategy has to match reality, not hope. Clarity now saves disappointment later.

How to Prepare Your Business for a High-Value Sale

If you want a premium outcome, preparation starts early. A buyer isn't purchasing your effort. They're purchasing future cash flow, reliable systems, transferable relationships, and manageable risk.

Start earlier than feels comfortable

The most effective preparation window is 3 to 5 years before exit. That gives you time to clean up financials, tighten operations, formalise contracts, and reduce dependence on the founder. If you start too late, buyers will still find the problems. You'll just have less time to fix them.

If you want outside perspective on the commercial side of exit planning, this guide on how to maximize your final sale is a useful companion to the deeper personal and retirement planning work every owner should also be doing.

Pass the transferability test

The first question buyers ask is rarely “How hard did the founder work?” It's “What breaks when the founder leaves?”

According to this Australian SME exit planning framework shared by Chris Herbert, a business should pass the “30-day test”, meaning it runs without the founder for a month with no performance degradation. The same source notes that no single client should account for more than 15-25% of revenue.

That gives you two clear benchmarks.

- Founder independence: If sales stall, staff freeze, or decisions pile up when you step away, the business is still too dependent on you.

- Client diversification: If one customer carries too much of the revenue base, buyers see concentration risk immediately.

- Documented systems: If key knowledge lives in your head or in scattered conversations, the business isn't ready.

A saleable business has systems. A valuable business has systems that still work when you're absent.

Clean up the numbers

You don't need perfect accounts. You do need credible, organised, consistent financial information.

Focus on the basics first:

- Reliable profit and loss reporting: Buyers want clarity, not reconstruction.

- Clean balance sheet items: Old loans, private expenses, and murky inter-entity transactions complicate trust.

- Defensible earnings: If profitability relies on add-backs that can't be explained cleanly, value suffers.

- Working capital discipline: Poor debt collection and erratic stock management make future cash flow harder to trust.

Turn goodwill into contracts

Many small business owners rely on strong personal relationships. That's useful while you own the business, but dangerous at sale time. Buyers don't pay top dollar for handshake arrangements they can't enforce.

Strengthen the business buyers can inherit

Work through the business like a buyer would.

- Formalise key customer agreements: Multi-year contracts are stronger than verbal understandings.

- Lock in staff capability: Identify who carries operational knowledge and protect retention where possible.

- Remove noise from the structure: Related-party arrangements, unclear ownership lines, and loose governance slow transactions.

- Show future upside: Buyers want a stable base and a believable growth story.

Focus on operational independence

If the business only works because you chase every issue personally, you don't own an asset yet. You own a demanding job with some transferable elements.

Here's what I'd want fixed before going to market:

| Area | What a buyer wants to see |

|---|---|

| Leadership | Managers who can make decisions without constant owner approval |

| Sales | A repeatable process, not a founder-only rainmaking model |

| Finance | Timely reporting and clear commercial drivers |

| Operations | Standard procedures staff can follow consistently |

| Customers | Broad spread of revenue and sticky relationships |

The best exits don't happen because the owner finally got tired. They happen because the business became durable, readable, and transferable.

Minimising Tax and Boosting Super on Your Business Exit

A good sale price can still produce a disappointing personal result if the structure is wrong. Consequently, many owners lose money they didn't need to lose.

Your business exit strategy should be built through exit contemplation, exit planning, and exit execution, not improvised after a letter of offer arrives. That three-stage Australian framework is outlined in this Victoria University research on successful SME exits. The same source highlights the role of a special purpose insurance trust to hold buy-sell insurance proceeds so they're distributed correctly on an owner's exit.

Tax planning starts before the deal

Owners often call the accountant when the sale is imminent. That's late. Structure affects outcomes, and structure takes time.

The big issues usually include:

- Entity structure: The way ownership sits today may not be the best shape for a future buyer or for your personal tax position.

- Sale structure: Asset sale versus share sale can change the outcome materially.

- Eligibility and documentation: Concessions, exemptions, and rollover opportunities often depend on facts that need to be prepared and evidenced.

- Timing: The order in which you do things matters.

Super is not an afterthought

A business sale can be a rare chance to move capital from an active, concentrated asset into a more controlled retirement structure. That's why exit planning and retirement planning need to sit in the same room.

If you're looking at ways to legally keep more of what you've built, this overview of small business tax reduction is a sensible starting point before any transaction is locked in.

Key point: The sale price is only half the story. What matters is what lands in your hands, what moves into super effectively, and what income that pool can support for the rest of your life.

Buy-sell arrangements matter more than most owners think

Where there are multiple owners, risk protection can't be loose. Death, disability, disagreement, or forced exit can derail succession and cash flow quickly. A properly structured buy-sell arrangement backed by the right insurance mechanism helps avoid confusion at exactly the wrong moment.

This is especially relevant when the business is part of a family's retirement funding plan. If ownership transfer, insurance proceeds, and personal planning aren't coordinated, the business can become a financial problem instead of a financial solution.

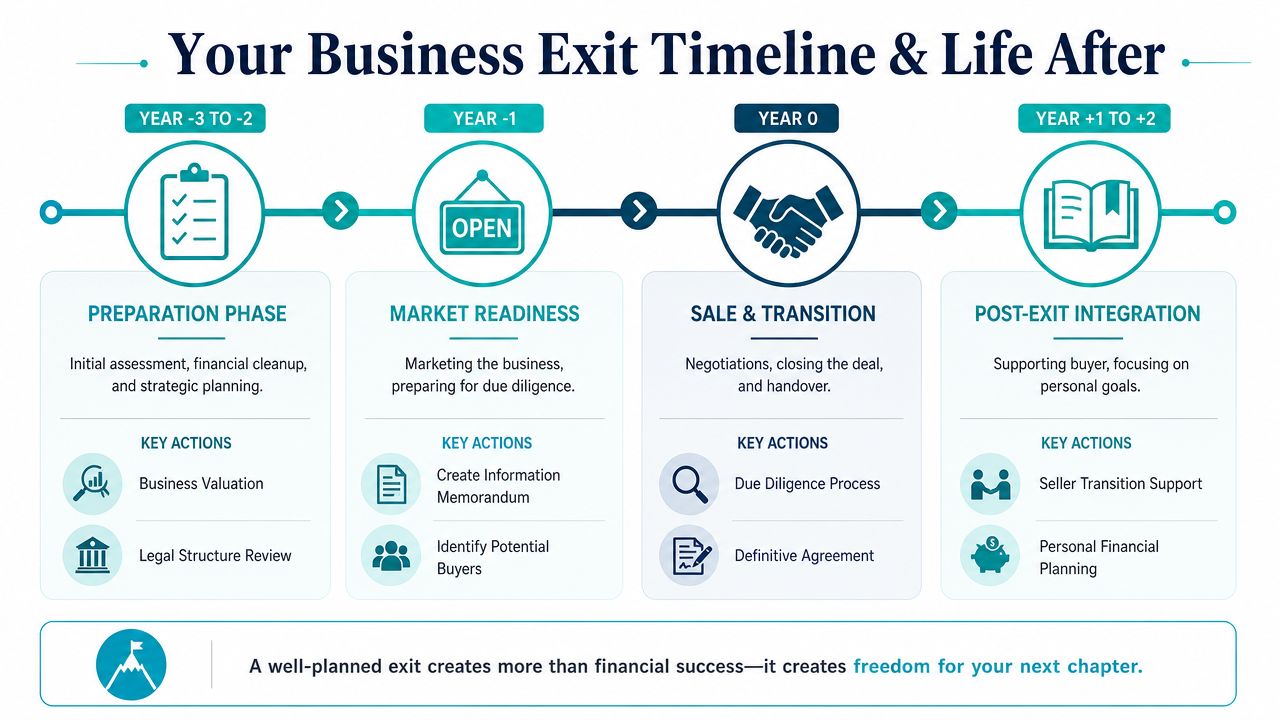

Your Exit Timeline and Life After the Sale

A sale date in the diary doesn't create readiness. What matters is what you do in the years before, and what you're walking into after settlement.

The years before the sale

Three to five years out, the owner usually still feels busy and indispensable. That's exactly why the work begins there. Financial records need attention. Leadership gaps need closing. Client relationships need to move beyond the founder. The owner also needs to decide what a successful outcome looks like.

Around the year before sale, the tone changes. Buyers, due diligence, negotiation strategy, and transition planning start to matter more. The business has to stand up to scrutiny. So does the owner's own plan for what comes next.

The year after is where many owners get caught

A surprising number of business owners are far less prepared for life after the sale than they are for the deal itself. According to this article on post-exit planning for Australian founders, many exit guides ignore the “Post-Exit Identity” issue, and 80% of SME exits fail to achieve the founder's personal goals because planning focused on financial mechanics instead of the psychological and cultural transition.

That rings true in practice. Owners who've spent decades being needed often struggle when the phone stops ringing. The title disappears. The routine changes. The urgency goes. Even a successful sale can feel disorienting if there's no purpose on the other side.

Don't just plan the exit from the business. Plan the entry into the next version of your life.

A better timeline for the person, not just the company

Here's how I'd think about the human side of a business exit strategy.

- Years before exit: Start defining what retirement or semi-retirement means for you. Work, travel, mentoring, board roles, investing, family support, community involvement. Be specific.

- Approaching sale: Decide whether you want a clean break, an earn-out period, an advisory role, or a phased handover.

- Immediately after sale: Give yourself structure. Many owners need a planned rhythm, not an empty calendar.

- Later on: Shift from operator mindset to investor mindset. Your capital now needs governance, not hustle.

Protect the next chapter

The strongest exits preserve two things. Financial security and personal direction.

If you sell well but drift afterward, the result still feels thin. If you preserve meaning, protect your capital, and build a clear retirement roadmap, the exit becomes what it should be: a transition into freedom, not a loss of identity.

Assembling Your Team and Planning Your Next Move

No owner should handle this alone. A serious business exit strategy is a team sport.

Who should be in the room

Your accountant handles tax structure, financial clarity, and transaction implications. Your lawyer manages contracts, terms, risk allocation, and legal transfer. If there are multiple owners, they'll also be central to shareholder arrangements and contingency planning.

Your financial adviser should do a different job. They should connect the business transaction to your personal future. That includes retirement income, investment structure, super strategy, protection needs, estate planning coordination, and the question most other advisers ignore: what life is this sale supposed to fund?

Why coordination matters

Problems usually don't come from one adviser doing poor work. They come from each adviser doing good work in isolation.

A lawyer can close a sound deal that doesn't fit your retirement needs. An accountant can minimise tax without addressing your long-term income plan. A broker can secure a buyer without helping you think through succession risk, family expectations, or whether your life after sale measures up.

If you're a business owner already thinking beyond the transaction, this guide to succession planning for business owners is worth reading alongside your exit planning.

The transaction ends on settlement day. The consequences of that transaction can last the rest of your life.

The right next move

If you're within a few years of stepping back, don't wait for the perfect moment. Start with clarity. Work out what the business needs to look like, what your after-tax target needs to be, and what sort of life you want on the other side.

That's how a business exit strategy should work. Not as a sale checklist, but as a plan to convert years of effort into lasting financial security and a life you want to live.

If you want help turning your business exit into a practical retirement plan, Wealth Collective offers a clear, low-pressure starting point. A brief introductory call can help you assess where you stand, what risks need attention, and what your next steps should be.