Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You're probably doing what most Perth locals do first. Open a few tabs, search for financial advisor Perth fees, click through adviser websites, and end up with more questions than answers.

One firm talks about custom solutions. Another mentions ongoing service. A third says fees depend on complexity. Very few spell out what you'll pay, what's included, or how to compare one model against another without guessing.

That confusion is reasonable. Advice pricing isn't usually one neat sticker price. It can involve the cost of producing advice, implementing it, reviewing it over time, and separate product-level costs sitting underneath the strategy. If you're trying to decide whether advice is worth it for your stage of life, that lack of clarity makes the decision harder than it should be.

This guide is designed to make the fee environment easier to read. Not from the angle of sales copy, but from the practical side of how advisers usually structure charges, what those structures suit, and what a sensible fee conversation should sound like before you commit.

Navigating the Fog Around Financial Advisor Fees

A common scenario looks like this. A couple in their thirties in Mount Lawley want help sorting out super, insurance, and whether to start investing outside the mortgage. They search around, see words like “detailed advice”, “wealth strategy”, and “ongoing guidance”, but they still can't tell whether they're looking at a one-off cost, a yearly cost, or both.

A pre-retiree in Applecross often hits a different version of the same problem. They've built decent super, retirement isn't far away, and now the questions are more technical. Pension structure, drawdown strategy, tax position, estate planning, and whether the adviser will stay involved after the initial work is done. Price matters, but so does knowing what the fee is buying.

That's where people often get stuck. They're not resisting advice. They're resisting ambiguity.

The real issue usually isn't the fee itself. It's not knowing how the fee is built, what it covers, and whether it matches the decisions you actually need help making.

In practice, fee confusion tends to come from three things:

- Mixed pricing language. Some advisers quote a plan fee, others focus on an ongoing service fee, and others lead with a percentage.

- Hidden second-layer costs. Even when the advice fee is clear, product costs can still sit underneath the strategy.

- Mismatch between life stage and service model. A young professional might need focused strategic help. A pre-retiree might need regular oversight and adjustment.

Why Perth clients need a clearer lens

The right question isn't “What does a financial adviser cost?”

It's “What fee model makes sense for my stage of life, complexity, and need for ongoing support?”

If you're early in your accumulation years, the best value might come from a defined piece of advice that helps you avoid bad set-up decisions. If you're approaching retirement, value often comes from getting the moving parts aligned and then reviewed as circumstances change.

A clear fee discussion should leave you knowing three things:

- What you're paying the adviser for

- What other costs sit outside the adviser's fee

- How long the arrangement is meant to last

Once those are clear, comparing advisers becomes much easier.

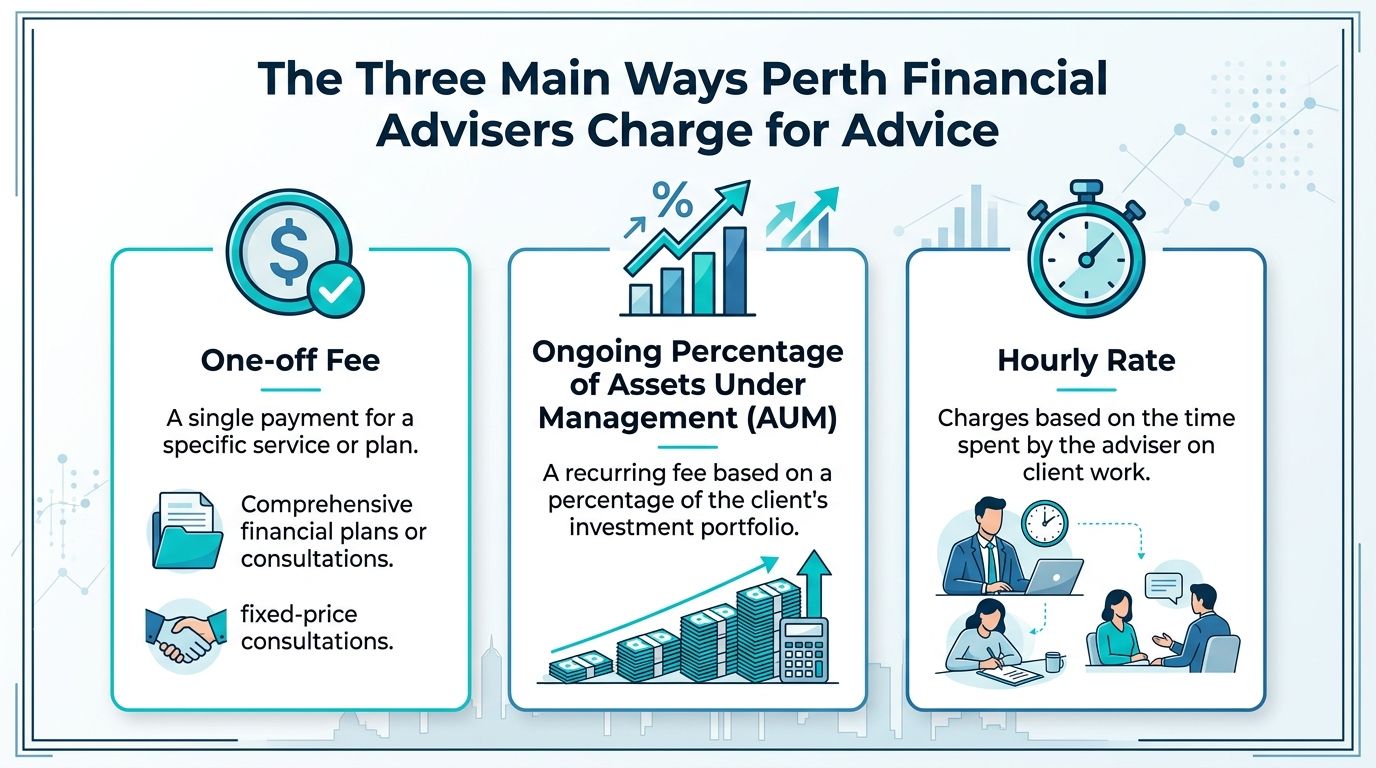

The Three Main Ways Perth Advisers Charge for Advice

A Perth couple in their early 30s usually needs help with a few specific decisions. Super setup, insurance gaps, cash flow, maybe whether to invest outside super. A Perth client five years from retirement usually needs something different. Pension timing, tax position, portfolio drawdown, Centrelink, and whether the current strategy will hold up when salary stops. The fee model should reflect that difference.

In practice, Perth advisers usually charge in one of three ways. One-off project fees, percentage-based ongoing fees, or hourly and retainer pricing. Each can be reasonable. The right fit depends on whether you need a single piece of advice, ongoing oversight, or access to an adviser across the year.

One-off fee

A one-off fee works like a paid strategy project. You are paying for analysis, recommendations, and the formal advice document, with implementation sometimes quoted separately.

This often suits younger professionals and families who need a clear decision made well at the start. Common examples are structuring super contributions, reviewing personal insurance, setting up an investment approach, or pressure-testing a debt reduction plan. The value is usually strongest when one good decision now can prevent years of drift or expensive mistakes.

What works well:

- Clear scope. You know what advice problem is being addressed.

- Good fit for focused questions. Useful where the need is specific rather than ongoing.

- Easier budgeting. The cost is agreed upfront for a defined piece of work.

What to watch:

- Implementation may sit outside the advice fee. Ask whether execution, product setup, and paperwork are included.

- Reviews are not automatic. If your income, family, or retirement timing changes, the advice may need updating.

Ongoing percentage fee

This is usually an assets-under-management arrangement. The adviser charges a percentage of the portfolio they oversee.

This model is more common for clients who want continuing investment management and regular review work. It can make sense for pre-retirees and retirees with a larger super balance, multiple accounts, and a need for ongoing decisions around asset allocation, pension payments, tax, and sequencing risk. In that setting, the fee is paying for ongoing judgement, not just the initial recommendation.

The trade-off is simple. As the portfolio grows, the fee usually rises as well. Some clients are comfortable with that because the adviser remains engaged and the work continues. Others prefer a flat annual fee because they want the cost tied to service scope rather than account balance alone.

Hourly or retainer pricing

Hourly pricing charges for time spent. A retainer or subscription charges for access and agreed service across the year.

Hourly advice can suit clients with narrow questions. Examples include checking whether to salary sacrifice more into super, getting a second opinion on insurance, or reviewing a proposed investment move. A retainer is often better for households or business owners who want regular contact, quick answers between meetings, and accountability as decisions arise.

The main trade-off is predictability. Hourly pricing can be efficient for contained work, but costs can become harder to estimate if issues expand. A retainer gives steadier access and clearer budgeting, but only makes sense if you will use that ongoing support.

A practical test helps here. If you need one good decision, a one-off fee often fits. If you need someone involved as your position changes, an ongoing fee model is usually easier to justify.

For a broader explanation of how these pricing approaches work nationally, see this overview of financial advice fees in Australia.

Typical Fee Ranges You Can Expect in Perth for 2026

Fee benchmarks are useful, but only if you treat them as a starting point rather than a universal rule. A straightforward super and insurance review won't be priced the same way as advice involving retirement income planning, trusts, business cash flow, or multiple entities.

For current market context, Envestnet's planning-and-fees study reports an average fixed percentage fee of 1.05%, an average flat fee of $2,554, an average hourly rate of $268, an average annual or retainer fee of $4,484, and an average subscription fee of $215 per month, as outlined in its review of different advisory fee models.

How to read those numbers properly

Those figures are most useful when you use them as comparison markers.

If an adviser quotes below them, that doesn't automatically mean better value. It may mean the scope is narrower, implementation is separate, or ongoing service is light. If an adviser quotes above them, that doesn't automatically mean overcharging. It may reflect more complexity, broader strategic work, more meetings, or hands-on implementation.

A practical way to compare fees is to ask what decisions the adviser is helping with. In Perth, the biggest drivers of variation are usually:

- Complexity of your structure. Personal name investing is simpler than layered super, trusts, companies, or business advice needs.

- Breadth of advice. Super alone is different from super, insurance, debt strategy, estate planning coordination, and retirement income planning.

- Implementation workload. Some advice is mostly strategic. Some requires application work, rollovers, policy changes, and product setup.

- Ongoing involvement. Annual reviews, regular contact, and proactive adjustments change the service equation.

A simple comparison lens

| Fee model | Best fit | Main caution |

|---|---|---|

| Flat fee | Defined advice project | Scope needs to be tightly clear |

| Hourly rate | Limited questions or second opinions | Cost can drift if scope expands |

| Percentage fee | Ongoing portfolio oversight | Fee rises with asset balance |

| Retainer or subscription | Ongoing strategic support | You need to use the service to get value |

Perth clients often make the mistake of comparing fee types as if they're interchangeable. They're not. A percentage fee and a one-off plan fee can both be reasonable, but only if they're attached to the right kind of work.

A good proposal should make it obvious whether you're paying for strategy, implementation, ongoing oversight, or a mix of all three.

What Services Are Included in the Fees

A young couple in Leederville might need one strong advice project to sort super, cash flow, insurance, and the right order for investing. A pre-retiree in Applecross may need ongoing reviews, pension drawdown planning, tax-aware withdrawal strategy, and coordination with an accountant and estate lawyer. Both can receive fair value. The fee only makes sense once the service matches the stage of life.

That is the question to press on. What work is included, who is doing it, and what decisions does it help you make?

What a one-off advice fee usually includes

A one-off engagement usually covers discovery, analysis, strategy, recommendations, and a formal advice document. It often suits younger professionals, growing families, or anyone with a defined set of decisions in front of them.

The value is clarity and sequencing. Which debt to clear first. How much emergency cash to keep. Whether to add to super or invest outside super. How much insurance is sensible without overpaying.

Typical inclusions may include:

- Initial discovery and goal setting. Understanding your income, assets, liabilities, priorities, and timeframes.

- Strategy analysis. Reviewing super, cash flow, debt, insurance, and investment options relevant to your position.

- Written recommendations. Setting out the recommended course of action, the trade-offs, and why one path may suit better than another.

- Implementation support. This may include forms, rollovers, account changes, and product applications, or it may be quoted separately.

- A presentation or follow-up meeting. Giving you a chance to test the recommendations and decide what to act on first.

For a younger household, that can be enough for now. If the main benefit is getting organised and avoiding expensive mistakes early, a one-off fee can be money well spent.

What an ongoing fee should cover

An ongoing fee should buy ongoing work. If the adviser is charging every month or every year, there should be regular monitoring, review, and adjustment behind it.

For pre-retirees, that often means more than investment oversight. It can include retirement timing analysis, super contribution changes, transition-to-retirement strategy, pension drawdown reviews, insurance reductions where appropriate, and keeping the broader plan aligned as legislation or family circumstances shift.

For established professionals or business owners, ongoing service may also include accountability. Regular check-ins, contribution discipline, investment rebalancing, and help making decisions in the right order instead of reacting case by case.

Service packages can help make this clearer. At Wealth Collective, the service lines are framed as Protection Plus, Guided Growth, and Retirement Roadmap. That sort of structure is useful because it shows whether the fee is tied to risk management, wealth accumulation, or retirement planning, rather than a vague promise of broad advice.

Where outside resources can still be useful

Some questions sit next to financial advice rather than inside it. A property decision is a good example.

Someone weighing up home ownership against long-term retirement savings may benefit from broad background reading before getting personal advice. The Home Ready guide for 401k home buyers is US-based, so it is not a guide to Australian rules, but it is a useful prompt for thinking through the trade-off between using retirement savings and preserving long-term wealth.

Good advisers are clear about that boundary. Personal advice should deal with your numbers, your structure, and your options in Perth. General education can help you ask better questions before that conversation.

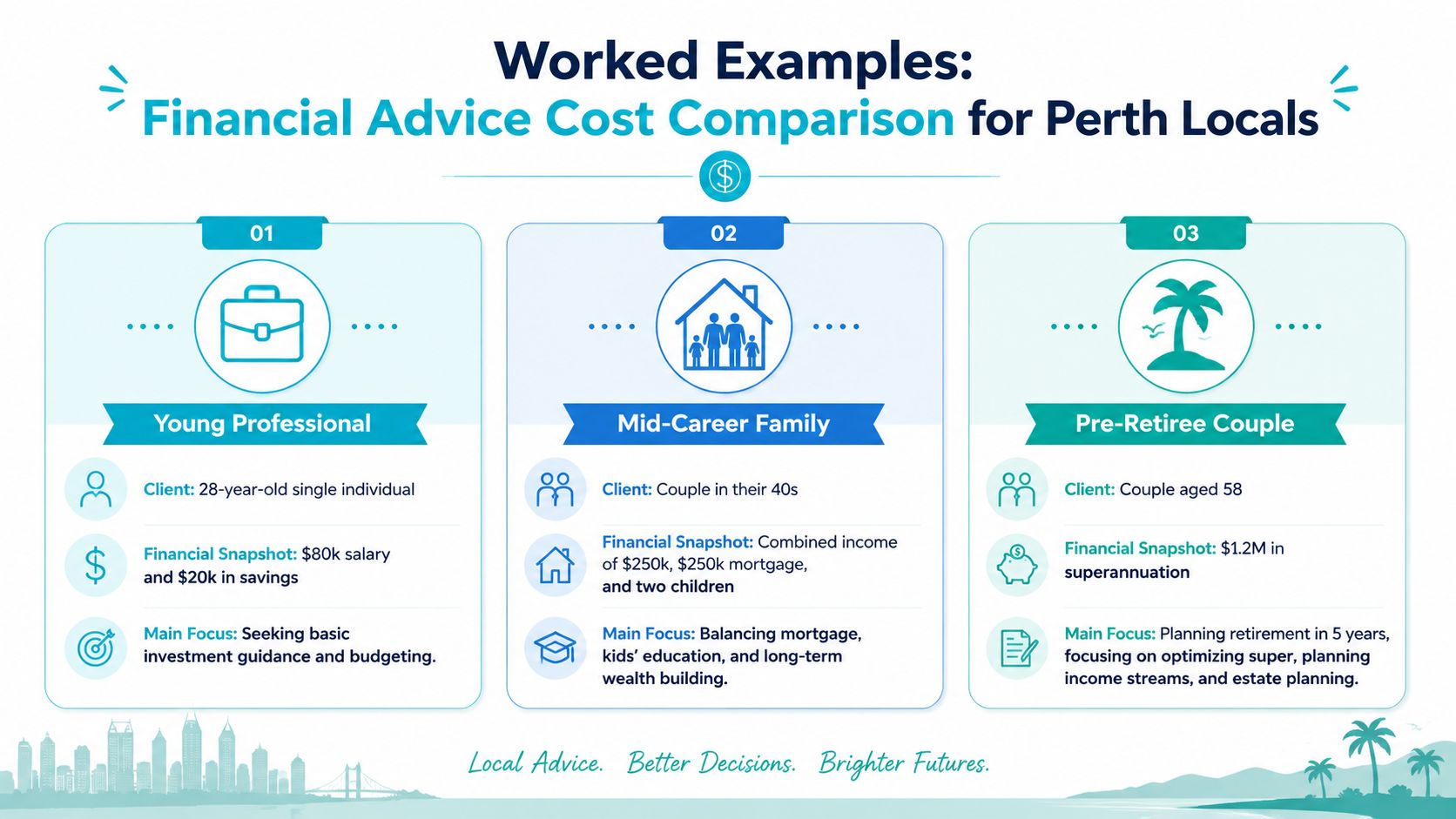

Worked Examples Cost Comparison for Perth Locals

Abstract fee models make more sense when you attach them to real life situations.

Young professional couple in Subiaco

They're earning well, carrying a mortgage, trying to clean up surplus cash flow, and have started asking the right questions about super, investing, and insurance. Their main risk isn't complexity. It's delay, scattered accounts, and making piecemeal decisions.

A one-off advice arrangement often makes sense here. They may need a focused plan covering debt strategy, emergency cash, super settings, insurance gaps, and the right order for beginning to invest.

An hourly model can also work if they're organised and only need a few key questions answered. What tends not to work well is jumping straight into an expensive long-term arrangement before they've even sorted the basics.

Good fit:

- one-off strategic advice

- limited implementation support

- occasional review as circumstances change

Less effective fit:

- a broad ongoing service they won't use consistently

- an asset-based model when investable assets are still modest

Pre-retiree couple in Dunsborough

They're within sight of retirement and their decisions are more interlinked. Super access, timing of retirement, income needs, tax position, and estate planning all need to work together.

For couples in this stage, a one-off plan can still be valuable, but many prefer an ongoing arrangement because the plan often needs refinement. Dates move. Work patterns change. Market conditions shift. Pension and cash flow decisions need monitoring.

The fee question here isn't just about preparation of advice. It's about whether the adviser stays close enough to the strategy to adjust it when needed.

If retirement is near, the cost of getting sequencing wrong can matter more than the discomfort of paying for proper oversight.

High-income business owner in the CBD

This client often has several moving parts at once. Personal and business cash flow, tax structuring discussions with an accountant, investment decisions, insurance, and family protection all interact.

A simple hourly arrangement usually becomes awkward because the work spills across multiple issues and rarely stays contained. A flat project fee may suit the initial strategy phase, but if the financial structure is active and changing, many business owners prefer a retainer or ongoing arrangement that gives them continuity.

What usually works:

- clearly defined initial strategy work

- implementation support across multiple items

- ongoing access for updates and coordination

What usually fails:

- trying to solve a layered financial situation with ad hoc one-hour meetings

- comparing adviser cost without considering the cost of fragmented decision-making

Comparing the examples

| Client type | Likely suitable fee style | Why |

|---|---|---|

| Young professional couple | One-off or limited hourly | Focused strategy, lower complexity |

| Pre-retiree couple | One-off plus ongoing review, or retainer | Decisions need active refinement |

| Business owner | Initial project plus ongoing arrangement | Multi-layered, changing needs |

These examples aren't about putting everyone into a template. They're about showing that the right fee model depends less on income alone and more on the shape of the decisions in front of you.

How to Assess Value Beyond the Price Tag

People naturally compare prices first. That's normal. It's also where many poor advice decisions begin.

A cheap arrangement can end up expensive if it leaves major decisions unmade, product choices poorly matched, or key risks uncovered. A higher fee can be good value if it helps you avoid costly mistakes and gives you a structure you'll follow.

Value looks different at different life stages

For early-career households, the math can feel uncomfortable because advice can take a bigger bite relative to assets. SmartAsset notes that a detailed standalone financial plan may cost about $3,000, subscription-style advice about $4,500 annually, and that advice can still make sense for smaller-balance households if it prevents poor product selection, duplicate insurance, or inefficient debt and super choices, as discussed in its overview of financial advisor costs.

That's the key point. Value doesn't belong only to wealthy clients. It often shows up first in avoided mistakes.

For pre-retirees, value often sits in sequencing and coordination. It's making sure retirement income, super access, tax position, and family goals fit together cleanly. For business owners, value often comes from having one strategic framework instead of a string of disconnected decisions.

What to test in an adviser conversation

If you want to assess value, ask questions that reveal how the adviser thinks, not just how they charge.

- Ask how they define scope. If they can't explain what's included and what isn't, the fee won't stay clear for long.

- Ask how often they expect to review the strategy. Ongoing fees need ongoing work behind them.

- Ask what kind of client the model suits. A good adviser should be able to say when a cheaper or simpler structure is enough.

- Ask how they coordinate with other professionals. Good advice rarely exists in isolation from accounting, lending, legal, or insurance decisions.

A useful comparison is moving house. The cheapest quote isn't always the best if timing, care, and reliability matter. If relocation is part of your planning year, these Perth removalists hiring tips are a good reminder that service value usually comes down to fit, transparency, and execution, not just sticker price.

Some clients need a plan. Others need a partner who helps them act on it. Price only makes sense once you know which of those you are buying.

For a practical framework on evaluating fit, service style, and fee alignment, this guide on how to choose a financial advisor is a useful starting point.

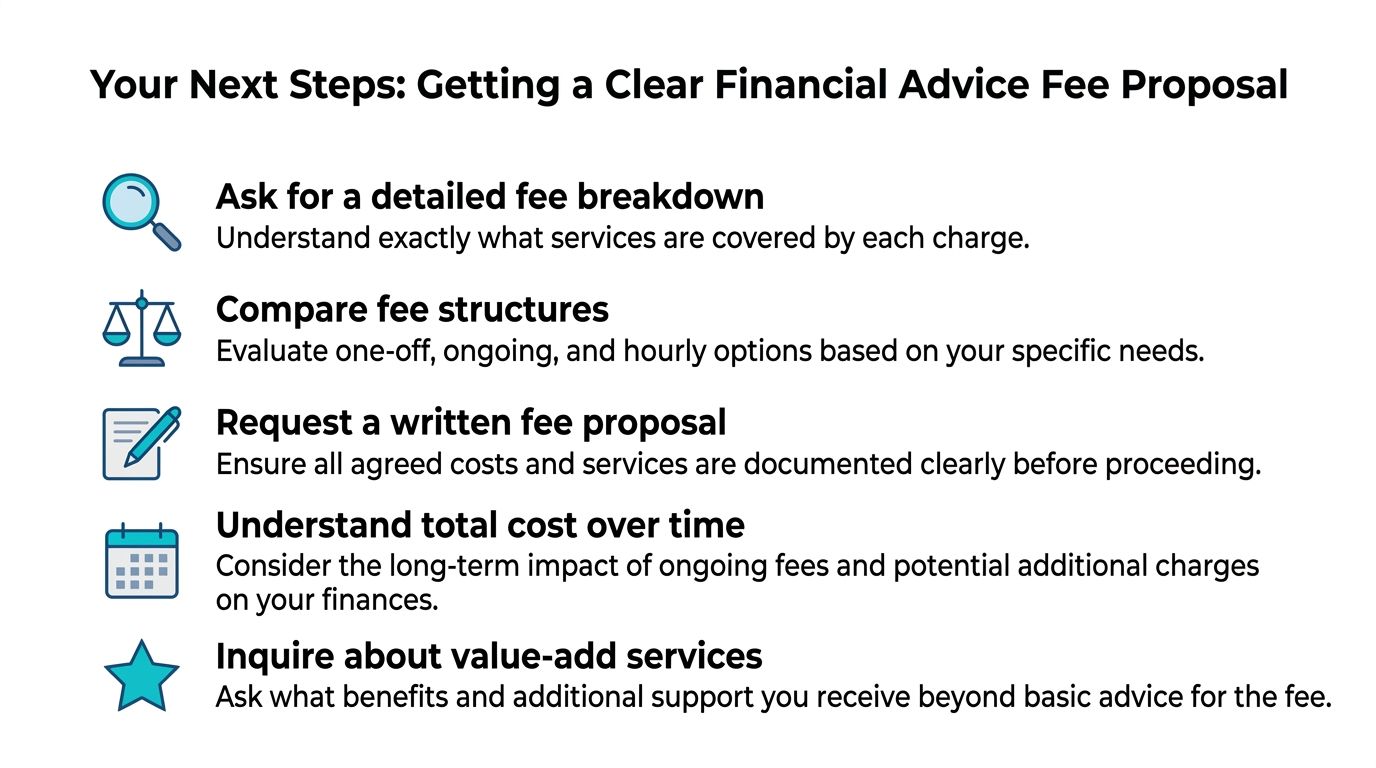

Your Next Steps Getting a Clear Fee Proposal

A Perth couple in their early 30s might need a one-off plan to sort cash flow, super, and a first investment strategy. A pre-retiree may need retirement income modelling, Centrelink planning, and regular reviews for years. The right fee proposal should make that difference obvious. It should show what you are buying, why it fits your stage of life, and what the adviser will do.

Questions worth asking

Advice fees should be clear before you agree to anything. If a proposal is hard to follow, that usually becomes a problem later when scope changes, reviews are missed, or extra work appears on the invoice.

Use the first meeting to get specific answers:

- Ask for each fee to be shown separately. Advice preparation, implementation, ongoing service, and product or platform costs should not be blended into one figure.

- Ask what happens in the first 12 months. That is where young professionals and pre-retirees often have very different needs, and the fee should reflect that.

- Ask what ongoing service includes. Reviews, adviser access, rebalancing, pension adjustments, insurance updates, and liaison with your accountant should be listed in plain language.

- Ask what falls outside scope. Estate planning work, complex super changes, aged care advice, or major restructuring can carry extra fees.

- Ask how fees stop or change. You should know how to end an ongoing arrangement and what happens if your circumstances become simpler or more complex.

What a usable proposal should do

A strong proposal answers three practical questions quickly:

- What am I paying at the start?

- What could I pay later if the relationship continues?

- What decisions, actions, and support am I getting for that cost?

That matters because the cheapest proposal can still be poor value. A young professional may be better served by a focused piece of advice with no ongoing retainer. A pre-retiree may pay more and still get better value if the work covers tax position, super pension timing, withdrawal strategy, and regular adjustments through retirement.

If you are comparing firms, this list of best financial advisors in Perth can help you build a shortlist before you request proposals.

A short conversation often clears up more than another round of online research. Wealth Collective offers a complimentary 10-minute introductory call where you can explain your situation, ask how the fee structure works, and decide whether it is worth taking the next step.