Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You've been doing the “right” thing. Money goes into a savings account each payday. You skip a few holidays, say no to a few dinners out, and keep checking property listings anyway. Then you look at your deposit balance and it still feels small compared with the homes you'd actually want to buy.

That's the point where a lot of first home buyers start asking a better question. Not “How do I save harder?” but “Is there a smarter way to save?”

For some people, the First Home Super Saver Scheme can be that smarter way. It isn't magic, and it isn't right for everyone. But it can make your deposit strategy more tax-effective by letting you use your super as a dedicated savings channel for part of your first home deposit.

The catch is that the rules are wrapped in government language, tax jargon, and timing traps. If you've ever read about the scheme and thought, “I sort of get it, but I'm not confident enough to use it,” you're not alone.

Struggling to Save a Deposit? There Might Be a Better Way

A common first-home story goes like this. You've built a decent routine, maybe an automatic transfer into savings every payday, maybe a separate “house deposit” account so you're not tempted to spend it. But the money sits there earning modest interest, while the total you need still feels far away.

That's where the first home super saver often enters the conversation. Not as a shortcut in the flashy sense, but as a more efficient route for part of your savings plan. Instead of saving every deposit dollar in a regular bank account, you can make eligible voluntary contributions into super and later apply to release them for a first home purchase.

If you're still tightening up the basics, practical guides like Koru App's house-saving walkthrough can help you organise cash flow before you add anything more advanced. The FHSS works best when it sits inside a broader savings system, not when it's treated as a standalone fix.

Why a bank account can feel slow

A savings account is simple. That's its strength.

It's also fully exposed to your normal spending habits and your normal tax position. You get easy access, but you don't get the specific tax treatment that can make super-based saving more efficient for some earners.

Practical rule: If your deposit plan feels disciplined but sluggish, the problem may not be your effort. It may be the structure you're using.

Where the FHSS can help

Think of the FHSS as a tax-advantaged deposit bucket inside super. You still have to contribute the money. The government isn't handing you a free deposit. What changes is the path your savings take and the tax treatment attached to that path.

That's why it can be useful to compare it with other approaches before you commit. If you want a broader look at different ways to save for a house, it helps to see FHSS as one option among several, not the default answer for every buyer.

For the right person, it can speed things up. For the wrong person, it can add complexity without enough upside. The key is knowing which camp you're in.

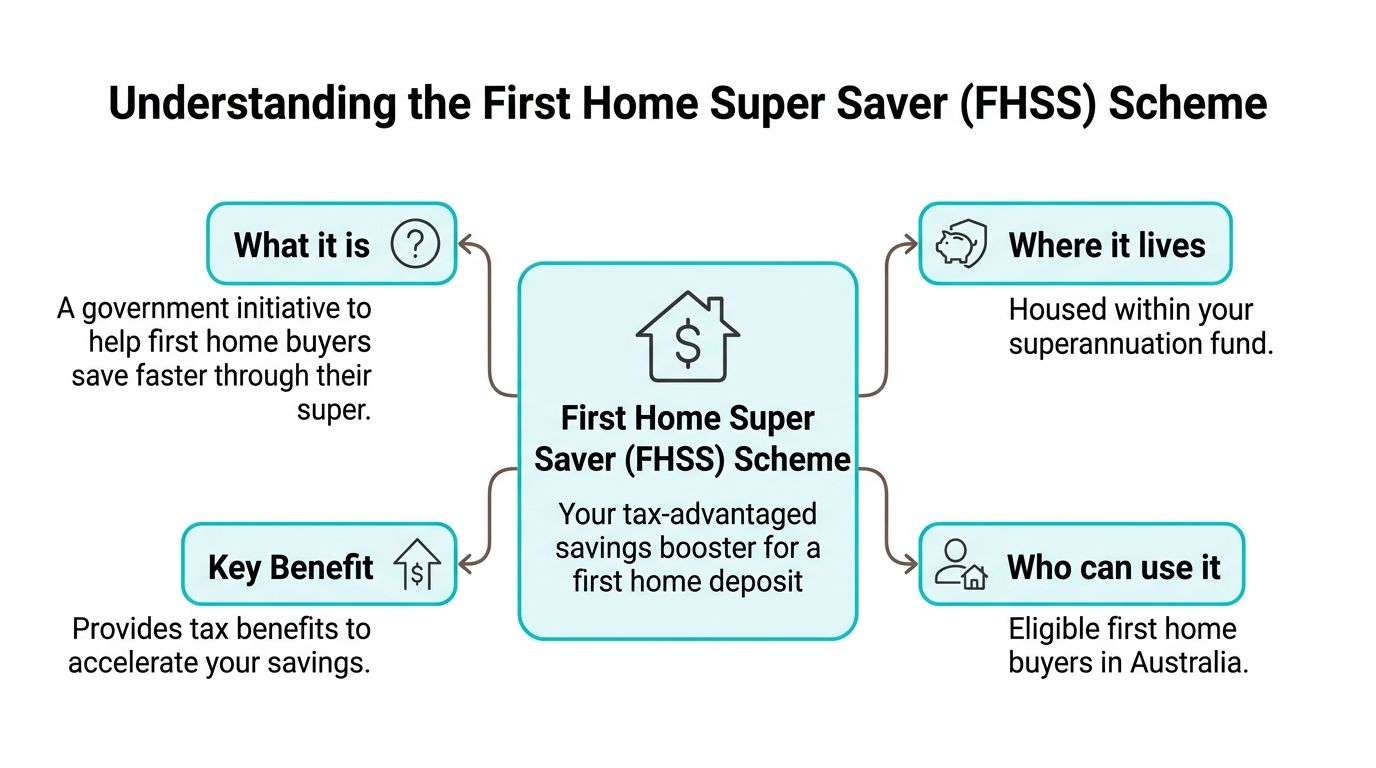

What Is the First Home Super Saver Scheme

The easiest way to understand the FHSS is to picture super as a locked toolbox. Most of what's in that toolbox is for retirement. The FHSS creates a narrow exception. It lets eligible first home buyers put certain extra contributions into super, then later ask to release an allowed amount to help buy their first home.

It's not your whole super balance. It's not compulsory employer super. It's a specific slice of voluntary contributions, handled under specific rules.

The simple version

You make voluntary contributions to super. Those contributions are tracked for FHSS purposes if they're the right type. When you're ready to buy, you apply through the ATO to release the amount you're allowed to access.

The attraction is simple. Super has tax rules that can be more favourable than saving from fully taxed income in a standard account.

What the FHSS is not

People often get tripped up here, so it helps to clear away a few myths.

- It's not a general early release of super. You can't dip into your retirement savings whenever you like.

- It's not based on employer compulsory contributions. Regular employer super payments don't count for FHSS release.

- It's not for an investment-only purchase. The home has to be one you genuinely intend to live in.

- It's not automatically better than every other strategy. If your timeline is short, your income is uneven, or flexibility matters more than tax efficiency, another approach may suit you better.

A quick eligibility checklist

You may be able to use the FHSS if the following apply to you:

- You're an adult. You need to be at least 18 when you request an FHSS determination.

- You haven't owned Australian property before. This generally includes a house, apartment, investment property, or vacant land.

- You intend to live in the property. This is aimed at first homes, not purely investment purchases.

- You'll hold an ownership interest. Your name needs to be part of the ownership arrangement.

- You meet the scheme rules at the time you apply. Eligibility is assessed individually.

A good way to think about eligibility is this. The FHSS is about helping a genuine first home buyer buy a home to live in, using their own voluntary super contributions.

Why this matters before you do anything else

The biggest mistake at this stage is getting excited about the tax angle before checking the basic fit. If you're not eligible, or if your planned property purchase doesn't match the occupancy rules, the scheme can create confusion rather than progress.

That's why I always suggest starting with a plain-English question. “Am I the kind of buyer this scheme was designed for?” If the answer is yes, then it's worth moving to contribution strategy.

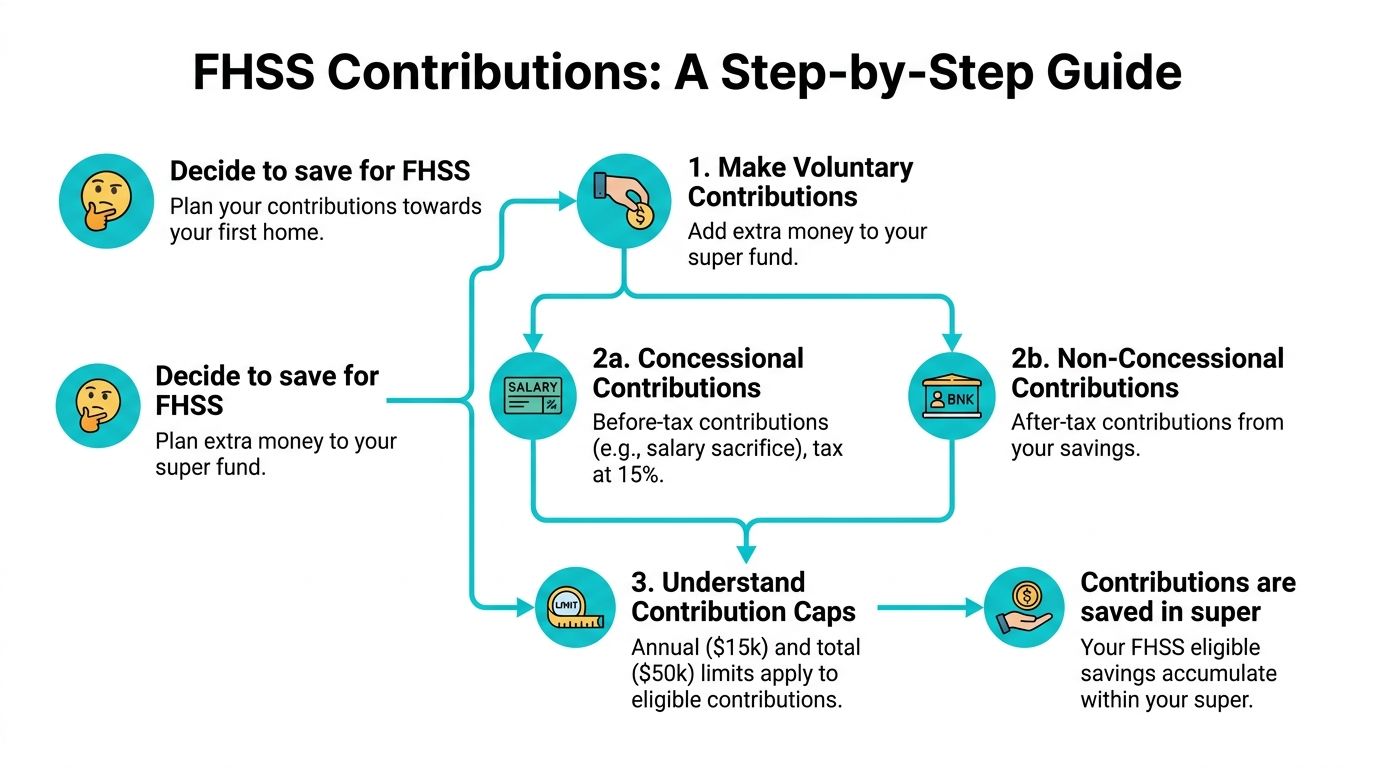

How to Make Contributions and Understand the Caps

This is the part that usually causes the most confusion. The FHSS doesn't involve a special FHSS account. You make contributions into your normal super fund, but only certain voluntary contributions count.

There are two broad paths. One uses before-tax money. The other uses after-tax money. Both can have a place, depending on your cash flow, tax position, and how organised you want the paperwork to be.

The two main contribution types

Concessional contributions

These are before-tax contributions. The common example is salary sacrifice through your employer. If you're self-employed or making personal contributions, you may also claim a tax deduction, which can make the contribution concessional.

Why people like this route is straightforward. It can create an immediate tax advantage because the money goes into super before it's taxed at your normal marginal rate.

Non-concessional contributions

These are after-tax contributions. The money has already been taxed before it lands in super.

This can still work for FHSS purposes. It just doesn't carry the same immediate tax benefit as salary sacrifice or deductible personal contributions.

The caps that matter

The scheme has two contribution limits built into it:

- Annual FHSS limit of $15,000 per financial year

- Total FHSS limit of $50,000 across all years

These figures are part of the required scheme rules for eligible contributions. They matter because not every voluntary dollar you put into super can later be counted for FHSS release.

If you remember only one thing from this section, remember this. FHSS limits sit inside the broader super contribution system. They don't replace it.

How FHSS caps interact with normal super limits

People sometimes make mistakes in this area. FHSS isn't a separate universe. Your contributions still sit inside the usual super rules.

That means:

- Concessional FHSS contributions still count toward your concessional contribution cap.

- Non-concessional FHSS contributions still count toward your non-concessional cap.

- Employer contributions can affect your room for concessional strategy, even though employer contributions themselves aren't released under FHSS.

If you're using salary sacrifice, you need to look at the whole super picture, not just the FHSS piece. A contribution that makes sense in isolation can be messy once employer payments and other super strategies are added in.

For a refresher on the broader framework, this guide to concessional contribution limits is useful background before setting up salary sacrifice.

A practical way to choose

Here's the plain-language version.

- Use concessional contributions if tax efficiency is the priority and your income structure supports it.

- Use non-concessional contributions if flexibility and simplicity matter more, or if you don't have room to add more concessional contributions comfortably.

- Use a mix if that gives you the best balance of tax outcomes and cash flow.

The right answer depends on your income, your employer setup, your timeline to buy, and what else you're already doing in super.

The Tax Benefits and Release Process Explained

The reason people pay attention to the FHSS is the tax treatment. Without that, most buyers wouldn't bother with the extra administration.

The scheme offers assistance because concessional contributions are taxed at 15% in super. That's often lower than the tax rate someone would otherwise pay on employment income before saving for a deposit. The release side has its own tax treatment too, which is why the strategy needs to be looked at from start to finish rather than in isolated pieces.

Where the tax benefit comes from

Start with salary sacrifice. If you divert part of your pay into super as a concessional contribution, that contribution is generally taxed in super at 15%.

That can be attractive because the money doesn't first pass through your full personal tax rate before being saved. In simple terms, more of each contributed dollar may stay in play for your deposit strategy.

There's another layer. When the amount is released, the assessable amount is taxed at your marginal tax rate, but there is a 30% tax offset applied. That's the part people often miss. The release isn't merely “tax free”, and it shouldn't be treated that way in your planning.

Why earnings confuse people

Many buyers assume they'll receive exactly what their super fund investment return delivered. That isn't the best way to think about it.

The ATO works with the FHSS rules to calculate the releasable amount, including associated earnings under the scheme. So when you're modelling outcomes, you need to be careful not to treat your super fund's visible balance movements as a direct one-for-one forecast of your final release amount.

The value of the FHSS is usually clearest for people who focus on the tax treatment of contributions first, then treat the release calculation as an administrative process to be planned carefully.

The release process in plain English

A lot of stress comes from timing. Buyers often assume they can sort the paperwork out once they've found a property. That's risky.

A clean process usually looks like this:

- Check your eligible contributions. Make sure the amounts and contribution types are correct.

- Request an FHSS determination from the ATO. This tells you what amount may be available to release.

- Wait for the determination before moving too far ahead. Don't assume. Confirm.

- Request the actual release. This is a separate action.

- Receive the funds into your bank account once processed.

- Use the released amount as part of your home purchase under the scheme rules.

A useful companion read if you want more context on super access rules generally is when you can access your super. It helps frame why FHSS is a narrow exception rather than a broad withdrawal right.

Timing matters more than people expect

The release process isn't instant. Administration takes time, and that matters when you're negotiating, bidding, or trying to line up funds before a purchase deadline. Buyers who leave FHSS paperwork until the last minute can end up creating pressure for themselves.

The safest approach is to treat FHSS like any other moving part in a property plan. Build in time. Confirm the order of steps. Don't rely on “we'll sort it after the offer is accepted”.

FHSS in Action A Worked Example and Comparison

Let's make this real without pretending there's one universal outcome.

Say Ella is buying her first home. She has stable employment, she's comfortable with salary sacrifice, and she doesn't need every dollar of her deposit savings to stay instantly accessible. She decides to use the FHSS for part of her deposit and keeps the rest in a regular savings account for flexibility.

Her logic is sensible. She wants some of her savings to benefit from the super tax environment, but she also wants cash outside super for costs that can pop up around a purchase, such as inspections, moving costs, or a buffer after settlement.

A practical worked example

Ella sets up a recurring contribution strategy rather than trying to dump in money irregularly. That does two things. It makes the plan easier to stick to, and it reduces the chance that she'll accidentally lose track of contribution limits.

Her process might look like this:

- She directs part of her savings effort into salary sacrifice because that's where the tax edge is usually most noticeable.

- She tracks each year's voluntary contributions carefully so she doesn't assume everything will count automatically.

- She keeps a separate cash reserve outside super so she isn't forced to rely on FHSS money for every purchase cost.

- Before house hunting gets serious, she checks her records and prepares for the ATO determination process.

That's a strong example of how FHSS should work in real life. It's not just “save in super instead of a bank account”. It's a split strategy with clear roles for each pool of money.

“The best FHSS plans aren't aggressive. They're organised.”

How it compares with other deposit strategies

FHSS is often compared with two alternatives. A high-interest savings account and investing in ETFs. Each can make sense. Each also solves a different problem.

| Strategy | Tax Efficiency | Risk Level | Accessibility | Best For |

|---|---|---|---|---|

| FHSS | Often stronger for eligible voluntary super contributions, especially concessional ones | Usually depends on your super investment option, but access rules add complexity | Restricted. Funds are tied to scheme rules and release process | Buyers who want tax efficiency and have a clear first-home timeline |

| HISA | Simple but usually less tax-effective than concessional super contributions | Low | High. Money is generally easy to access | Buyers who prioritise flexibility, certainty, and clean cash management |

| ETFs | Tax treatment depends on structure and personal circumstances | Higher short-term market risk | Accessible if sold, but value can fluctuate when you need the money | Buyers with a longer timeline and higher tolerance for volatility |

The honest comparison

A HISA is easier to understand and easier to access. That matters if your timeline is uncertain, your emergency fund is thin, or you hate administrative complexity.

ETFs can offer growth potential, but they're usually the least comfortable option for a near-term deposit because markets don't care when you want to buy. If prices fall at the wrong moment, your deposit plan can shrink just when you need it.

The FHSS sits in the middle. It can be more efficient than cash for the right person, but the money is less flexible and the rules matter. If you're the sort of saver who likes automation, stable employment, and planning ahead, it can fit well. If your life is changing quickly, a plain savings account can still be the better answer.

Common Pitfalls and Getting Personalised Advice

The FHSS can work well. It can also go wrong in very ordinary ways.

The first trap is treating it like a casual add-on. People make contributions without checking caps, assume employer super counts when it doesn't, or forget that contribution type affects how the strategy works. None of those mistakes sound dramatic, but they can create tax issues or reduce the benefit you expected.

Mistakes that catch buyers out

- Cap confusion: People focus on FHSS limits and forget the broader super contribution limits still apply.

- Timing errors: They leave the determination or release steps too late and then try to rush a property purchase.

- Access assumptions: They think FHSS money is as available as savings account cash. It isn't.

- One-bucket planning: They put too much emphasis on FHSS and too little on keeping cash outside super for real-life expenses.

Another common issue is what happens if plans change. A purchase can fall through. A couple can change direction. Work income can shift. FHSS doesn't become useless in those moments, but it does become more technical.

Watch-out: A good FHSS strategy should make your path to a first home calmer, not more fragile.

Why personal advice matters

Generic articles often fall short. While the scheme rules might be public, your decision still depends on your income, your tax position, your super setup, your purchase timing, your risk tolerance, and what else you're juggling financially.

A personalised plan matters because FHSS is only one moving piece. It needs to fit alongside your cash reserve, debt reduction, borrowing strategy, insurance needs, and longer-term super goals. That's why the best outcomes usually come from advice that looks at the whole picture instead of trying to optimise one rule in isolation.

FHSS Frequently Asked Questions

Can a couple both use the FHSS for the same property

Yes, potentially. Eligibility is assessed individually, not as a single combined application. If both people qualify, each person can use their own eligible FHSS amounts toward the same purchase. That can make the scheme more powerful for couples, but each side still needs its own contribution and release planning.

What if the property purchase falls through after release

This is one of the reasons timing and paperwork matter. If the purchase doesn't proceed, you'll need to follow the scheme rules for what happens next. Depending on the situation, that may involve recontributing the amount to super or dealing with the tax consequences set out under the FHSS framework. This isn't the sort of detail to leave fuzzy. It's worth checking before you request release.

Does FHSS usually affect state-based first home buyer support

In general, FHSS is a separate federal mechanism for deposit saving. State-based grants and concessions are governed by their own eligibility rules. That means FHSS can often sit alongside other first home buyer support, but you should always confirm the exact rules that apply in your state and for the property you want to buy.

Can self-employed buyers use the FHSS

They can, but the contribution method usually looks different from a standard employee salary sacrifice setup. The planning can still work well. It just requires closer attention to timing, deductions, and record-keeping.

Is the FHSS always worth it

No. If your income is low, your purchase timeline is uncertain, or you need maximum flexibility, the extra complexity may not justify the benefit. The FHSS tends to work best when it's part of a deliberate, personalised deposit plan rather than a rushed attempt to squeeze out a last-minute advantage.

If you're weighing up whether the FHSS fits your situation, a personalized plan can save a lot of second-guessing. Wealth Collective helps Australians turn complex rules into clear next steps through a simple advice process, starting with a free introductory call and building toward a strategy that fits your goals, cash flow, super, and home-buying timeline. If you want to know whether the first home super saver is the right move for you, booking that initial conversation is a smart place to start.