Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A lot of people start searching for an accountant at the same moment they realise their finances have crossed a line. The tax return used to be straightforward, then shares, property, a family trust, a new business, retirement income, or an SMSF entered the picture. Suddenly the question isn't whether you need help. It's how do you find a good accountant who fits the job in front of you.

That question matters more than is commonly assumed. An accountant can become part of your decision-making circle for years. The wrong one creates confusion, reactive tax work, weak communication, and blind spots between your tax position and your broader financial plan. The right one helps you stay organised, compliant, and better positioned for the next decision.

When Your Finances Outgrow Your Expertise

In Australia, the challenge usually isn't finding an accountant. It's filtering the field properly. The Australian Bureau of Statistics reports that accountants are among the country's largest professional groups, with well over 100,000 employed nationally, which means clients need to screen for fit, experience, and specialisation rather than assume any available practitioner will do the job, as noted in this discussion of qualified and experienced accountants.

That size cuts both ways. You have options, but volume makes lazy selection dangerous. Choosing the first person a friend mentions, or the cheapest quote in your inbox, often leads to a mismatch between what you need and what the accountant does well.

The real decision is strategic fit

A good accountant isn't just someone who can prepare a return. The better question is whether they fit your life stage, complexity, and decision style.

For a business owner, that might mean someone who can work comfortably with Xero or MYOB, review payroll and BAS processes, and speak plainly about reporting. If you're still sorting your systems, Wistec's review of accounting software options is a useful starting point before you even shortlist advisers, because software choice shapes how smoothly your accountant can work with your records.

For a retiree or pre-retiree, the issues are different. You may need someone who can coordinate with superannuation, pension drawings, estate considerations, and reporting obligations without treating each piece in isolation.

Practical rule: Don't ask, “Who's a good accountant?” Ask, “Who regularly handles situations like mine?”

Price matters, but not first

Low fees can look attractive when you're comparing names online. But if the work has to be redone, if deadlines are missed, or if the accountant doesn't communicate clearly with your adviser and lender, the cheaper option can become expensive quickly.

Business owners often see this first in reporting gaps and cash pressure. If that's already a problem area, it helps to understand small business cash flow management before you appoint anyone, because cash flow pressure often exposes whether you need compliance help, strategic help, or both.

A strong selection process protects more than your tax return. It protects your financial judgement.

Define What You Actually Need from an Accountant

The word “accountant” is often used as a catch-all term. In practice, that's where the search often goes wrong.

The Tax Practitioners Board regulates different roles in Australia, and many people asking for a “good accountant” need a registered tax agent, BAS agent, or strategic adviser, as explained in this overview of choosing the right accounting help. If you don't define the role first, you can end up hiring someone competent, but not competent for your task.

Match the role to the task

Use a simple filter before you contact anyone.

- Tax return and tax advice. You're looking for a registered tax agent if the work involves preparing returns, giving tax advice for a fee, or lodging on your behalf.

- BAS and routine bookkeeping support. A BAS agent may be the right fit if your main need is BAS preparation, GST, and related lodgement support.

- Financial statements and business reporting. A general accountant may help with reporting, management accounts, and compliance support, depending on the work involved.

- Big-picture decision support. A strategic adviser is useful when your questions involve structure, retirement cash flow, wealth planning, debt, investments, or coordination across multiple professionals.

What different clients usually need

The right appointment depends heavily on where you are financially.

Small business owners

A business owner often needs more than annual tax work. The shortlist should be able to discuss:

- Entity structure and whether your current setup still suits the business

- Payroll and BAS workflows so reporting doesn't become a scramble

- Software compatibility with platforms such as Xero or MYOB

- Owner drawings and tax planning, especially if personal and business cash flow keep blurring together

If your accountant can only talk about last year's numbers, but not how your systems support this year's decisions, that's a sign you may need broader advice alongside compliance. For clients weighing that bigger picture, guidance on how to choose a financial advisor helps clarify where accounting ends and financial strategy begins.

Retirees and pre-retirees

This group often needs someone who understands the interaction between:

- superannuation withdrawals

- retirement income planning

- SMSF reporting support if relevant

- estate and family coordination

- taxable income from investments

A retiree doesn't need an accountant who is brilliant with trade businesses but unfamiliar with retirement structures.

High-income earners and executives

These clients usually need clean tax compliance, but also someone who can work around complexity such as investments, bonuses, equity arrangements, trusts, and debt recycling discussions with advisers.

The right accountant for a salary-and-wages tax return may be the wrong accountant for a household with investments, entities, and long-term structuring decisions.

How to Verify an Accountant's Credentials in Australia

Once you know the job, verification becomes far simpler. This is the part many people rush. They read testimonials, skim a website, and assume professional language equals professional standing. It doesn't.

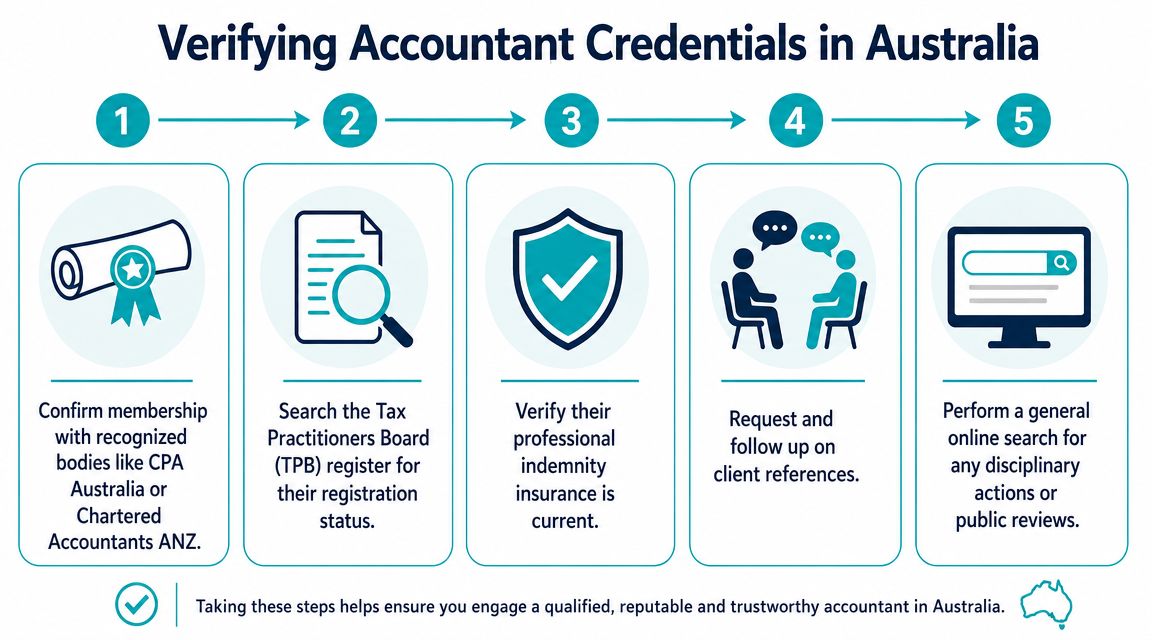

A mandatory first check in Australia is registration. The Tax Practitioners Board requires anyone providing tax agent services for a fee to be registered, and verifying their status on the public register is the government-recommended first step before engagement, as outlined in this explanation of the TPB register and why it matters.

Start with registration, not branding

Plenty of firms present well online. That has almost no value if the person providing tax agent services isn't properly registered.

Use this order:

- Search the TPB register and confirm the practitioner appears there.

- Check the registration status shown on the register.

- Confirm who will be doing the work. In some firms, the person you meet isn't the person handling your file.

- Ask whether your matter will be reviewed by a registered tax agent if junior staff prepare parts of it.

This step protects you from a basic but costly mistake. It also helps distinguish between someone doing bookkeeping support and someone legally authorised to provide tax agent services.

Then look at professional depth

Registration answers the legal threshold. It does not answer whether the accountant is right for you.

Look for signs of depth such as:

- Professional body membership like CPA Australia or Chartered Accountants ANZ

- Relevant client mix, meaning they regularly deal with people in your position

- Clear scope of work, so you know whether they do compliance only or broader advisory work

- Experience with your tools, especially if your records sit in Xero, MYOB, or another cloud platform

A credential on its own doesn't guarantee clear advice. But it does tell you the person has chosen to operate within recognised professional frameworks.

If someone resists simple credential checks, stop there. A trustworthy practitioner won't treat verification as an insult.

Verify practical compatibility as well

In Perth and regional WA, fit often comes down to practical things people forget to test until too late.

Ask yourself:

- Do they understand your type of work or income structure?

- Can they explain issues without jargon?

- Will they work directly with your financial adviser or mortgage broker if needed?

- Are they responsive before you've even become a client?

The best accountants reduce friction. They don't create more of it.

A short verification checklist can help:

| Verification area | What to confirm |

|---|---|

| Registration | They appear on the TPB register if providing tax agent services |

| Qualifications | Any CPA or CA membership is current and relevant |

| Insurance | They hold professional indemnity cover |

| Experience | They routinely advise clients like you |

| Process | They can explain how work is reviewed, lodged, and communicated |

Essential Interview Questions for Your Shortlist

By the time you reach the interview stage, the goal isn't to test whether they know accounting theory. It's to find out whether they can handle your situation, communicate well, and protect sensitive information.

That last point matters more than many clients realise. Amid rising financial scams in Australia, a good accountant also needs strong digital safeguards, and both the ATO and TPB warn consumers to ask how firms protect MyGov-linked data and financial records, as discussed in this article on finding an accountant with proper safeguards.

Ask questions that reveal working style

A technical answer can sound impressive while telling you very little about what working with the person will feel like. Ask questions that force specifics.

Here's a practical interview table you can use.

| Question Category | Sample Question | What to Listen For |

|---|---|---|

| Relevant experience | What types of clients do you usually work with that are similar to me? | Familiarity with your stage of life, business type, or complexity level |

| Scope | What work would you handle directly, and what falls outside your scope? | Clear boundaries, not vague promises |

| Communication | How often do you communicate during the year, and by what method? | A defined process for email, phone, meetings, and urgent issues |

| Software | Which platforms do you work with most often? | Comfort with the systems you already use, such as Xero or MYOB |

| Team structure | Who will actually prepare and review my work? | Transparency about junior staff and review layers |

| Planning approach | Do you only handle compliance, or do you also flag strategic issues as they arise? | Awareness of planning opportunities without overpromising |

| Data security | How do you protect identity documents, bank details, and cloud accounting access? | Concrete procedures, secure portals, and cautious data handling |

| Collaboration | How do you work with financial advisers, lenders, or lawyers when a matter overlaps? | Willingness to coordinate rather than work in a silo |

What a strong answer sounds like

Good answers are usually plain, specific, and calm. They don't rely on jargon to create authority.

For example, if you ask about data handling, a strong accountant should explain how documents are shared, where they're stored, and how client access is controlled. If they shrug off the question or say “we take security seriously” without details, keep probing.

Good interview answers sound organised. Weak answers sound improvised.

Questions many people forget

Three questions often reveal more than the obvious ones:

- How do you explain financial issues to clients who aren't accountants?

- What do you need from me to keep the relationship efficient and accurate?

- When do clients usually realise they've outgrown basic compliance and need broader advice?

If you want extra ideas for shaping better interview prompts, Professional Careers Training's interview preparation guide is aimed at accounting interviews generally, but it's still useful for understanding how structured questions expose clarity, judgement, and process.

Understanding Fee Structures and Spotting Red Flags

Fees deserve more attention than they usually get. Not because the cheapest quote wins, but because fee structure tells you how the firm thinks about its work.

A vague quote often leads to vague service. A clear quote usually comes from a business with defined systems, boundaries, and deliverables.

Common pricing models

You'll usually see one of these approaches.

Hourly billing

This can work well when the scope is uncertain or the matter is complex. It's flexible, but it also creates cost uncertainty. If records are disorganised or the brief keeps changing, the final bill may feel disconnected from your original expectation.

Fixed-fee packages

These are easier to budget for and often suit tax returns, annual accounts, BAS support, or scheduled advisory meetings. The catch is scope. You need to know exactly what's included and what triggers extra fees.

Value-based or advisory pricing

This is common when the accountant provides ongoing strategic input rather than only compliance work. It can be sensible for business owners or households with layered financial decisions, but only if the deliverables are well defined.

If you're comparing broader professional costs across your financial life, it also helps to understand how financial advice fees work in Australia, because the same principle applies. Fees make more sense when tied to scope, accountability, and decision value.

Red flags worth taking seriously

Some warning signs should end the conversation quickly.

- No TPB registration where tax agent services are being offered. This is an immediate stop sign.

- Promises of guaranteed refunds or outcomes. Careful professionals don't sell certainty where facts and law still need review.

- No engagement letter. If there's nothing in writing about scope, responsibility, and fees, the risk shifts to you.

- Poor responsiveness during the sales process. If they're already hard to reach, service rarely improves after onboarding.

- Messy explanations of fees. If they can't explain how they bill, expect disputes later.

- Defensive behaviour when you ask basic questions. You want a professional relationship, not a gatekeeping exercise.

Compare proposals like a buyer, not a bystander

When you receive quotes, compare them across three things:

| Comparison point | What to check |

|---|---|

| Scope | What exactly is included, excluded, and optional |

| Access | How often you can contact them and who responds |

| Review process | Whether work is reviewed before lodgement or advice delivery |

That frame usually tells you more than the dollar figure alone.

Onboarding Your New Accountant for a Strong Partnership

Choosing well is only half the job. The handover period shapes whether the relationship becomes efficient or frustrating.

A good onboarding process should leave both sides clear on documents, deadlines, access, and responsibilities. If the first month feels chaotic, expect the rest of the relationship to carry the same tone.

What to prepare early

Have these items ready before the first working meeting:

- Identification documents required for engagement and verification

- Prior returns and financial statements so the new accountant can see history and continuity

- Entity documents for companies, trusts, or SMSFs if relevant

- Access list covering Xero, MYOB, bank feeds, payroll systems, and ATO-linked platforms where appropriate

- Questions and priorities written down, not held in your head

This saves time and reduces avoidable back-and-forth.

Set the rules of engagement

The strongest relationships start with practical clarity:

- who your main contact is

- how documents should be shared securely

- when you should contact them during the year

- what requires proactive review rather than waiting until tax time

- how they'll coordinate with your other advisers

That final point is where many households and business owners miss an opportunity. Your accountant shouldn't operate in isolation if your financial life also involves super, insurance, debt strategy, retirement timing, estate planning, or investment structures.

The accountant's work should support your wider strategy, not sit beside it disconnected.

For clients who want those moving parts aligned, Wealth Collective provides financial advice that can sit alongside your accountant's work, helping coordinate tax-aware planning around superannuation, investments, protection, debt reduction, and retirement decisions.

The best outcome isn't just finding a competent accountant. It's building a coordinated advice team that keeps your financial life moving in one direction.

If you want help deciding what kind of accountant fits your stage of life, or you want your accountant's work aligned with a broader wealth plan, speak with Wealth Collective. A short initial conversation can help clarify whether you need tax compliance, strategic coordination, or a more integrated financial plan before you make your next move.