Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Building wealth in Australia isn’t a secret reserved for the few. It’s about following a proven, practical blueprint. This guide lays out that exact roadmap, giving you a clear, achievable process to build real, lasting prosperity by focusing on what truly works.

Your Blueprint for Building Wealth in Australia

Australians are thinking more seriously about their money than ever before. With rising costs and economic uncertainty, a recent MLC research on Australian financial priorities found that 55% of us are now prioritising financial stability above all else. This figure climbs to 62% for those aged 31-45.

This growing desire for control is the perfect fuel for building wealth, especially when you know where to focus. For most Australian households, net worth is concentrated in two key areas: property and superannuation.

This guide isn’t about fuzzy theories. It’s a flight plan for your financial journey, designed to show you that building wealth is entirely possible when you follow the right steps. It’s the same process we use at Wealth Collective to help our clients achieve their financial goals.

The Three Pillars of Wealth Creation

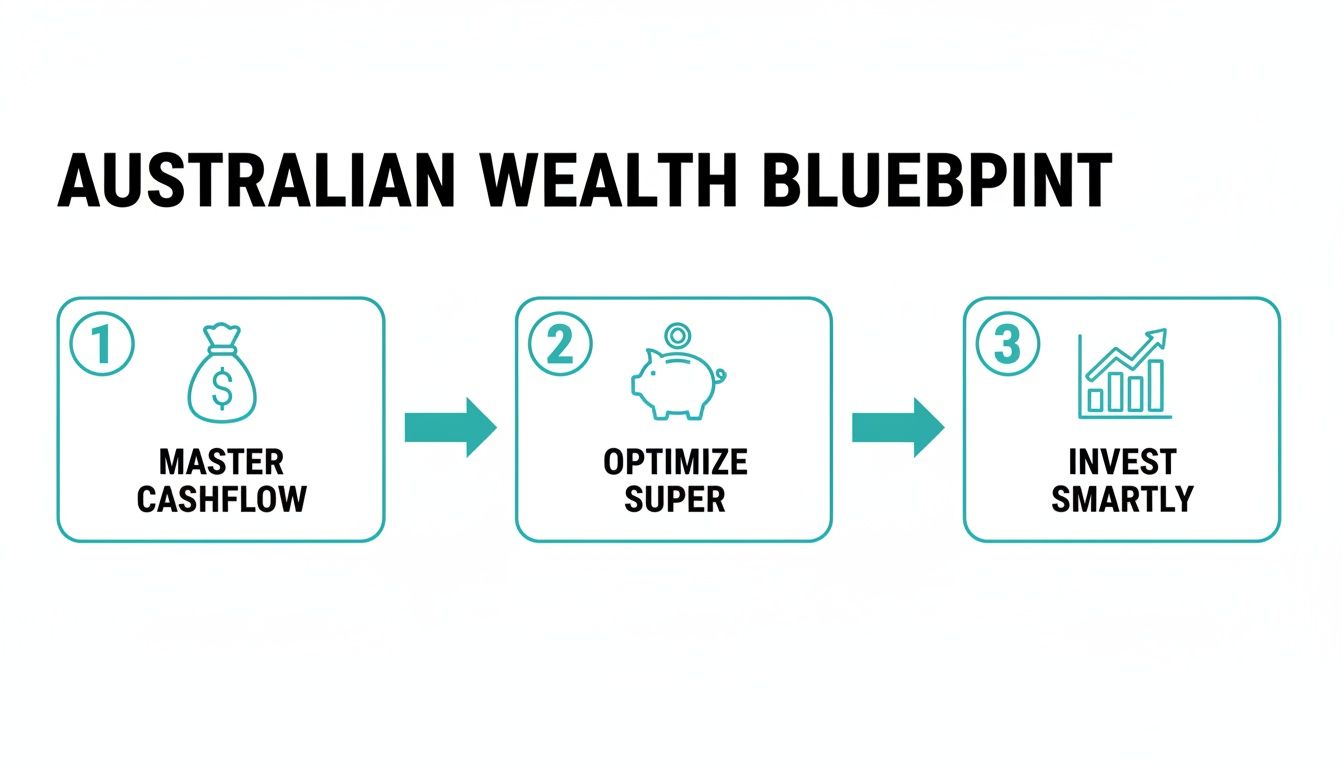

So, where do you start? The entire process boils down to three core pillars. We’ll dive deep into each one, but the strategy is all about taking deliberate, sequential action.

Think of it as a logical flow: first, get your money under control; second, make your biggest assets work harder; and finally, grow what’s left over.

This simple chart shows how these three pillars work together.

As you can see, mastering your cash flow is the foundation. It’s the essential first step that frees up the resources you need to properly optimise your super and start making smart investments.

The table below breaks down these fundamental components of the Wealth Collective strategy.

The Pillars of Australian Wealth Creation

| Pillar | Key Actions | Wealth Collective Service |

|---|---|---|

| Master Your Cash Flow | Build a realistic budget, create a savings system, and strategically pay down high-interest debt. | Cash Flow Coaching |

| Optimise Your Super | Review fees and performance, consolidate accounts, and choose the right investment option for your goals. | Superannuation Advice |

| Invest Smartly | Develop a personalised investment strategy, diversify across asset classes, and manage your portfolio tax-effectively. | Investment Advice |

Each pillar builds on the last, creating powerful momentum that turns your financial goals into reality. Every stage we cover is designed to give you more control, mirroring the structured approach we take with our clients to cut through complexity and provide a clear, actionable plan.

Wealth isn’t built by accident. It’s the result of a deliberate strategy, consistent execution, and the discipline to focus on what truly moves the needle—from your daily budget to your long-term investment portfolio.

A Roadmap for Your Financial Future

We’ll walk you through the key stages of building and protecting your financial future. Here’s a quick look at what we’ll cover:

- Building a Strong Financial Foundation: Get your cash flow sorted, smash high-interest debt, and build a solid safety net.

- Optimising Your Superannuation: Turn that sleepy super account into a high-performance engine for your retirement.

- Investing in Australian Markets: Learn how to make your money work for you in shares, property, and other growth assets.

- Protecting Your Progress: Make sure your wealth is properly safeguarded with the right insurance and estate planning.

Each section breaks these concepts down into no-nonsense, actionable advice. It’s the same proven framework that underpins our Guided Growth service, where we partner with clients to build a successful financial life, one step at a time. The journey starts right here.

Getting Your Financial Foundations Rock-Solid

Before you can build real wealth, you have to get the basics right. It’s like pouring the concrete slab for a house—skip it, and everything you build on top will crumble. In finance, that slab is a powerful cash flow system that puts you firmly in control of your money.

Too many people jump straight into investing, hoping for a big win. But we’ve seen it time and again: without a solid budget and a plan to crush bad debt, any gains can vanish in a heartbeat. Nailing this first builds discipline and, more importantly, frees up the cash you need to create real momentum.

This is exactly why it’s the non-negotiable starting point in our Guided Growth service. We insist on getting these fundamentals sorted because experience shows it’s the only way to build wealth that lasts.

A Budget That Doesn’t Feel Like a Cage

Let’s be honest, the word “budget” makes most of us groan. It sounds like spreadsheets and deprivation. Forget that. Think of it as a spending plan—a tool for telling your money where to go, so it starts working for you, not against you.

To start, simply track your income and expenses for one month. The goal isn’t to judge yourself; it’s to get a crystal-clear picture of where your money is actually going. You’ll probably be surprised.

Once you have that data, the 50/30/20 rule is a brilliant framework to build from:

- 50% on Needs: This covers non-negotiables: rent or mortgage, groceries, utilities, and transport.

- 30% on Wants: This is your lifestyle money for dining out, holidays, hobbies, and entertainment.

- 20% on Savings & Debt: This is the powerhouse. It’s the portion you’ll use to pay off loans, build your safety net, and eventually, invest.

This simple rule gives you an instant diagnostic. If ‘Needs’ are eating up 70% of your pay, you know exactly where the problem lies. You either need to trim those fixed costs or find a way to earn more.

Get Ruthless With High-Interest Debt

Nothing murders wealth creation faster than high-interest debt. Credit cards and personal loans, with interest rates often topping 20%, are designed to work against you. The interest compounds relentlessly, chewing up the very cash you should be investing.

Picture this scenario we see with young professionals in our cities:

A $10,000 credit card debt at a 21% interest rate. Making only minimum repayments could mean being stuck with it for over 25 years and handing over $20,000 in interest to the bank. That’s a house deposit, a new car, or a healthy share portfolio, gone.

To fight back, you have two main strategies:

- Debt Avalanche: Throw every spare dollar at the debt with the highest interest rate first. Mathematically, this saves you the most money.

- Debt Snowball: Focus on paying off the smallest debt first, regardless of the interest rate. The quick win gives you a huge psychological boost to keep going.

Which is better? The one you’ll stick with. The goal is the same: systematically destroy these financial anchors and free up your cash flow to build your future.

Weaving Your Financial Safety Net

Life happens. Cars break down, people get sick, and jobs can disappear. An emergency fund is your financial shock absorber, stopping bad luck from derailing your wealth plan or forcing you back into debt.

We advise our clients to aim for 3 to 6 months’ worth of essential living expenses stashed away. If your core monthly bills are $4,000, you’re shooting for a buffer of $12,000 to $24,000.

This might sound like a mountain, but you get there one step at a time. Set up an automatic transfer—even a small one—into a separate, high-interest savings account. Once you’ve paid off high-interest debts, you can redirect that cash to turbo-charge your emergency fund.

This groundwork—mastering your spending, clearing bad debt, and building a safety net—is where true financial freedom begins. It takes focus, but it’s the most important work you’ll ever do on your journey to building wealth.

Ready to get your foundation right? A complimentary 10-minute chat with our team can bring clarity to your very next steps.

Get Your Super Working as Hard as You Do

For most of us, superannuation happens in the background. It’s easy to see it as a locked box you can’t touch for decades. But treating your super passively is one of the biggest missed opportunities in building wealth in Australia.

It’s time to stop thinking of it as just a retirement fund and start treating it like the powerful investment engine it is.

The real secret sauce is time. Because of how compounding works in the low-tax world of super, even small tweaks you make today can have a massive impact on the nest egg you end up with.

The data is clear. According to the Finder Wealth Building Report 2026, those who start optimising their super early can end up with 67% more wealth by retirement than those who wait. It’s a powerful reminder that the best time to take action was yesterday. The next best time is right now. You can see the full breakdown by reading the full Finder Wealth Building Report.

Taking Control of Your Super

So, how do you become an active driver of your super’s growth? It starts with a few straightforward checks. These aren’t complicated financial gymnastics; they’re simple, effective tune-ups that ensure your money works for you.

This is exactly what we focus on in our Retirement Roadmap service. We help clients cut through the noise and get their super aligned with their financial goals.

Here are the key things we always look at first:

- Hunt Down and Combine Your Accounts: If you’ve had a few jobs, you likely have a few super accounts. Each one is being eroded by separate fees. Consolidating them into a single, low-fee account is the quickest win you can get.

- Check Your Fees and Performance: Are you in a fund that’s charging a fortune for mediocre returns? A fund charging just 1% more in fees can strip hundreds of thousands of dollars from your final balance. It’s a huge deal.

- Pick the Right Investment Mix: Don’t just settle for the default ‘balanced’ option. Your investment strategy should match your age and risk appetite. If you’re younger, you can generally be more aggressive for higher growth. Closer to retirement, you might want to dial down the risk.

Topping Up Your Super for Maximum Impact

Once your account is sorted, the next move is to accelerate its growth. Your employer’s mandatory 11% contribution is a solid foundation, but on its own, it’s rarely enough to fund the retirement lifestyle most of us dream of.

Making extra contributions is one of the smartest things you can do, thanks to generous tax rules.

- Concessional (Before-Tax) Contributions: This is where you ‘salary sacrifice’, asking your employer to pay a bit of your pre-tax wage directly into super. That money is only taxed at 15%, which for most people is far less than their usual income tax rate. It’s an instant tax win.

- Non-Concessional (After-Tax) Contributions: This is you transferring money from your own bank account—money you’ve already paid tax on. You don’t get another tax break upfront, but future investment earnings inside super are still taxed at the low rate of 15%.

Think about this: a simple salary sacrifice of just $100 a week could add over $250,000 to your final super balance over 30 years, assuming a 7% average annual return. That’s a life-changing amount from a small, consistent action.

If you’re lost in the jargon, our guide can help you understand what superannuation is in Australia in plain English.

Taking an active role with your super isn’t just a nice idea—it’s essential for anyone serious about building wealth. The choices you make today will shape your future.

A great first step is to book a complimentary 10-minute chat. We can quickly help you see how to turn your super into the wealth-building powerhouse it’s meant to be.

Putting Your Money to Work in the Australian Market

You’ve done the hard yards. You’ve built a solid financial foundation and turned your superannuation into a growth engine. Now, we put your surplus cash to work. This is the critical shift from simply saving to actively building wealth.

Investing can feel like a new world, but the principle is straightforward: make your money generate its own momentum. The aim is to build a portfolio that grows over the long haul, pulling your financial goals closer, year by year.

This isn’t about gambling on “hot tips” or trying to time the market—that’s a recipe for stress and disappointment. True wealth building comes from a disciplined, tax-aware investment strategy built around your life and ambitions. This is the core of our Guided Growth service, where we design personalised roadmaps for sustainable, long-term success.

Finding Your Mix: Shares, ETFs, and Managed Funds

For most people, the share market is the most accessible tool for building wealth outside of super and property. But a real strategy is more than buying a few familiar stocks. The secret ingredient is diversification—spreading your capital across different assets to smooth out the bumps.

-

Direct Shares: The classic approach of buying stakes in individual companies. It gives you total control but demands significant research and capital to build a genuinely diversified portfolio.

-

Exchange-Traded Funds (ETFs): Think of these as a basket of investments bundled into a single security. With one purchase, you can buy into the entire ASX 200, giving you instant diversification. They are a fantastic, low-cost way to get broad market exposure.

-

Managed Funds: Here, you pool your money with other investors, and a professional fund manager makes the decisions. You’re paying for expertise, which can be great, but it often comes with higher fees that eat into your returns.

Building a solid portfolio is like packing for a trip to Melbourne. You don’t just pack shorts; you need a jacket and an umbrella, too. A balanced mix of assets ensures your portfolio is prepared for different economic “weather.”

Getting your bearings can be a big step, which is why we created a straightforward resource to get you going. Have a look at our guide on how to start investing for more practical advice.

Australian Investment Options At a Glance

Choosing the right investment comes down to your goals, risk comfort, and how hands-on you want to be. Here’s a quick comparison of the most common options for Aussie investors.

| Investment Type | Best For | Typical Risk Level | Key Consideration |

|---|---|---|---|

| Direct Shares | Hands-on investors who enjoy research and portfolio management. | High | Requires significant time and knowledge to manage and diversify effectively. |

| ETFs | Investors seeking low-cost, instant diversification with a passive approach. | Medium to High | You get the market average—which includes both the ups and the downs. |

| Managed Funds | Investors who prefer professional management and are willing to pay for expertise. | Varies by Fund | Fees can significantly impact long-term returns; always check the fine print. |

| Investment Property | Long-term investors comfortable with using debt (leverage) and holding illiquid assets. | Medium | High entry costs, plus ongoing expenses like maintenance, rates, and land tax. |

Understanding these differences is the first step. A well-crafted plan doesn’t just pick one; it blends the right mix to suit your specific financial situation.

Property Investment in Today’s Market

For generations, property has been a cornerstone of Australian wealth creation, offering capital growth and rental income, often amplified by leverage.

But a smart property strategy involves far more than just buying the first house you see. It demands a deep understanding of location, property type, and market cycles. There are a few common approaches:

- The Classic Buy and Hold: The marathon, not the sprint. Buy a quality property in a good location and hold it for long-term growth while the tenant helps pay the mortgage.

- Renovate and Sell: A more active strategy. Buy a tired-looking property, add value through smart renovations, and sell for a profit.

- Development: The high-risk, high-reward end of the spectrum, involving anything from a simple subdivision to building townhouses.

Property can be an incredible asset, but it’s also illiquid and comes with hefty entry and exit costs. It’s a major commitment that must be a deliberate part of your overall wealth plan.

Advanced Moves for Business Owners and High-Income Earners

When your income grows or you run a business, sophisticated structures can open the door to greater control and tax advantages. The most common of these is a Self-Managed Super Fund (SMSF).

An SMSF is your own private super fund that you control directly. This structure gives you the freedom to invest in a wider array of assets, including direct property—you can even use your super to buy your own business premises.

While the flexibility is fantastic, an SMSF comes with serious legal and compliance responsibilities. They are not a set-and-forget option and absolutely require expert guidance to set up and manage correctly.

Ultimately, every investment decision should be tax-aware. From the asset you buy to the name on the title, each choice has a tax consequence. The goal is to legally minimise the tax you pay to maximise the net returns in your pocket. This is where professional advice really pays for itself.

Ready to build an investment strategy that truly fits your life? Book a complimentary 10-minute chat with us today to start the conversation.

Protecting Your Progress and Planning Your Legacy

As your net worth grows, a crucial question looms: how do you protect everything you’ve worked so hard for? Growing your wealth is one thing; securing it against the unexpected is what truly gives you peace of mind.

The strategy now shifts from pure growth to preservation and legacy. It’s about building a financial fortress around your assets and drawing a clear map for the future, ensuring your success supports you and your family for generations.

This is exactly why we created our Protection Plus service. We work with clients to put these robust safeguards in place so they can keep building with confidence.

Shielding Your Wealth from Life’s Curveballs

Many people think their property or share portfolio is their most valuable asset. It’s not. Your ability to earn an income is. An unexpected illness, serious injury, or premature death can instantly derail your family’s security and halt your wealth creation.

This is why personal insurance is essential. A well-designed insurance plan acts as a financial safety net, providing the funds needed to maintain your family’s lifestyle and clear debts without being forced to sell hard-won investments at the worst possible time.

The key types of cover to consider are:

- Life Insurance: Provides a lump sum payment to your family if you pass away, giving them the means to pay off the mortgage and secure their financial future.

- Total and Permanent Disability (TPD) Insurance: Pays a lump sum if an injury or illness leaves you permanently unable to work again.

- Trauma Insurance: Delivers a lump sum on the diagnosis of a specified critical illness like cancer or a heart attack, giving you financial breathing space.

- Income Protection: Replaces up to 70% of your pre-tax income if you’re temporarily unable to work due to sickness or injury.

These policies are fundamental parts of a defensive strategy designed to protect what you’ve built, no matter what.

Designing Your Retirement Roadmap

Retirement planning isn’t just stashing cash away for “one day.” It’s about intentionally designing the life you want when work becomes a choice. Creating a clear Retirement Roadmap is how you turn that dream into a solid, achievable plan.

The first step we take with clients is to define what retirement looks like for them. From there, we calculate their “retirement number”—the capital needed to fund that lifestyle. This number becomes the north star for every saving and investment decision.

Then, the focus turns to structuring your assets for the “decumulation” phase. This is where we arrange your super, properties, and share portfolios to generate a reliable, tax-efficient income stream.

A successful retirement plan isn’t defined by the size of your nest egg alone. It’s defined by how intelligently that nest egg is structured to provide a secure, tax-efficient income that lasts a lifetime.

Crafting a Lasting Legacy

Your legacy is about more than just passing on money. It’s about ensuring the wealth you’ve created continues to benefit the people and causes you care about. Thoughtful estate planning is the final, most critical piece of the puzzle.

A proper estate plan goes far beyond just a will. It ensures your assets are transferred smoothly, efficiently, and exactly as you intended. Without a clear plan, you risk leaving a legal and financial mess for your loved ones.

If you’re unsure where to begin, our guide explores what happens if you don’t have a will and highlights why it’s so important to get this right.

Protecting your progress and planning your legacy provides the ultimate financial security. It’s what ensures all your hard work translates into a lasting, positive impact.

So, Where Do You Go From Here?

You’ve just worked through a detailed plan for building real wealth in Australia. From getting your budget under control and making your super work harder, to investing with tax in mind – the path is now clear. But seeing the path and walking it are two different things.

Taking those first few steps can feel like the hardest part. That’s where we come in. With over 50 years of combined experience, our award-winning team at Wealth Collective knows how to cut through the noise and provide clear, straightforward financial guidance.

At Wealth Collective, our goal is to help you build your own wildly successful financial life. We achieve this by transforming complex financial topics into a clear and actionable plan, personalised to you.

Let’s Put Your Plan Into Motion

We know everyone’s situation is unique. You might be focused on paying down debt, or perhaps you’re ready to explore more sophisticated investment strategies. That’s why we’ve developed specific services to give you the exact support you need, right now.

- Guided Growth: A structured plan for young professionals and families to get on top of cash flow, optimise their super, and begin investing with confidence.

- Protection Plus: We’ll help you build a safety net for your family and assets with the right personal insurance, making sure your hard work is always protected.

- Retirement Roadmap: A complete strategy where we map out your retirement goals and structure your assets to create a tax-effective income stream for the future.

It all starts with a simple, no-pressure conversation. We offer a complimentary 10-minute chat where you can tell us what’s on your mind. We’ll listen to your goals and give you a clear picture of how we can help you get there.

Let’s work together to turn these ideas into your prosperous reality. Book your introductory call today and take that first, crucial step.

Your Wealth-Building Questions, Answered

As you start putting these strategies into action, questions will naturally come up. Here are some of the most common queries we hear from our clients, with our straightforward answers.

How Much Money Do I Actually Need to Start Investing in Australia?

Honestly, you can get started with less than you think. Forget the old idea that you need a huge lump sum. These days, with micro-investing apps and platforms offering fractional shares in Exchange-Traded Funds (ETFs), you can begin with just a few hundred dollars.

The real secret isn’t how much you start with, but how consistently you keep adding to it. A small, regular contribution is far more powerful over the long haul than waiting for the “perfect” moment to invest a big chunk of cash. That’s how real momentum is built.

The best time to start investing was yesterday. The next best time is today. The key is to start, no matter how small, and let compound growth begin its work.

Should I Pay Off My Mortgage Faster or Invest the Extra Cash?

This is a great question, and there’s no single right answer. It’s a tug-of-war between a guaranteed win and a potentially bigger one. The best choice depends on the numbers and your own comfort with risk.

-

Paying Off Your Mortgage: This is a guaranteed, tax-free return equal to your home loan’s interest rate. It’s a rock-solid, risk-free move that builds equity and provides incredible peace of mind.

-

Investing: This path offers the potential for much higher returns over the long term, but you have to be comfortable with market volatility. It’s a classic risk-reward trade-off.

For many, a balanced approach is the sweet spot. You might make extra mortgage repayments while also consistently putting money into your super or an ETF. We help clients model these scenarios as part of our Guided Growth process to see what makes the most mathematical and emotional sense.

What Is a Realistic Rate of Return to Expect From Investments?

It’s so important to set realistic expectations. Historically, a well-diversified portfolio of Australian and international shares has delivered an average return of around 7-10% per year over the long term.

That word “average” is key. It’s not a guarantee; some years will be up while others will be down. The trick is to not get caught up in short-term noise. Your expected return is tied to the assets you own, so focus on your long-term plan and let the market do its thing.

Everyone’s journey to financial security looks different. At Wealth Collective, our specialty is mapping out a clear, personalised plan that fits your life and ambitions.

If you’re ready to see what that looks like for you, book a complimentary 10-minute chat with our team today.