Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

June creeps up fast when you run a business. One week you’re focused on customers, staff, stock and cash flow. The next, you’re staring at a quote for a new machine, vehicle upgrade or office tech, wondering whether buying now is smart planning or just spending for the sake of tax.

That tension is real. A café owner in Perth might need a replacement espresso machine. A tradie may be looking at new tools and equipment. A consultant could be deciding whether to upgrade ageing laptops before year end. In each case, the purchase only makes sense if it improves the business first. The tax outcome should support the decision, not rescue a poor one.

That’s where the instant asset write off 2025 matters. Used properly, it can improve timing, lift after-tax cash flow and create room for bigger financial moves outside the business. Used poorly, it can lock money into assets you didn’t really need.

Your Guide to Smart Business Investment in 2025

A lot of small business owners are in the same position right now. Revenue is moving, expenses haven’t eased, and the list of things the business needs keeps growing. Equipment wears out. Software gets outdated. Vehicles become unreliable. At the same time, tax planning starts to matter more as the end of the financial year gets closer.

The practical question isn’t just, “Can I claim it?” It’s, “Should I buy it now, and if I do, what does that free up elsewhere in my finances?”

A strong tax deduction can make a good business purchase easier to justify. It can also help smooth a rough patch in working capital by reducing taxable income sooner rather than spreading deductions across future years. That timing difference matters when you’re trying to preserve flexibility.

For many owners, the smarter conversation starts with cash flow, not tax law. If you’re reviewing major purchases, it’s worth looking at the broader picture of small business cash flow management before making the call.

Why this matters in practice

The instant asset write-off isn’t just an accounting rule. It changes how fast you get the benefit of a legitimate business purchase.

That can affect decisions like:

- Replacing underperforming equipment when downtime is costing you time and revenue

- Upgrading technology so your team can work faster and more reliably

- Bringing forward planned purchases into the current financial year if the timing stacks up

- Protecting liquidity by reducing tax pressure earlier

Buy the asset because the business needs it. Claim the deduction because the rules allow it. Don’t reverse that order.

Handled well, this measure can support growth now and strengthen your personal position later. That’s the part many owners miss.

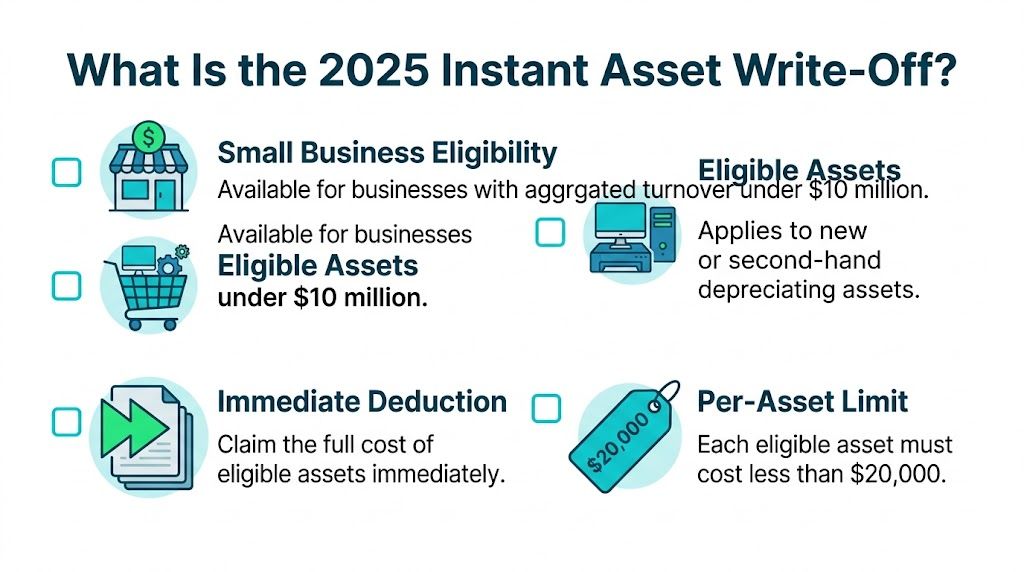

What Is the 2025 Instant Asset Write-Off?

The easiest way to understand the instant asset write-off is to compare it with ordinary depreciation.

Normally, when you buy a business asset, you don’t claim the full deduction straight away. You deduct it over time. The instant asset write-off changes that timing for eligible assets. Instead of waiting years to claim the cost, you may be able to deduct the business portion immediately.

For the 2024–25 income year, eligible Australian small businesses with aggregated turnover under $10 million can immediately deduct the full business cost of eligible depreciating assets costing less than $20,000, provided the assets are first used or installed ready for use between 1 July 2024 and 30 June 2025, as explained in this overview of the 2025 instant asset write-off rules.

Think of it as accelerated timing

A useful analogy is this. Standard depreciation is like getting your refund back in instalments. The instant asset write-off is like bringing more of that tax benefit into the current year.

That doesn’t mean the asset is free. It means the tax deduction arrives sooner.

The advantage is timing:

- You reduce taxable income in the current year

- You may improve near-term cash flow

- You avoid waiting for deductions to trickle through later years

- You gain more control over when purchases happen

What the rule is really designed to do

This measure encourages small businesses to invest in productive assets without having to wait years for the tax benefit. In practical terms, it helps businesses replace, upgrade or add assets that support day-to-day operations.

That’s why it often comes up around:

- equipment

- tools

- technology

- machinery

- some vehicles, subject to the rules that apply

The key idea is simple. If the asset qualifies, and the timing and cost are within the rules, the deduction is front-loaded.

The four moving parts

Most confusion disappears once you focus on four questions.

| Question | Why it matters |

|---|---|

| Is your business small enough under the turnover test? | The concession is aimed at eligible small businesses |

| Is the item a depreciating asset? | Not every business expense falls into this category |

| Does each asset cost less than the threshold? | The cap works on a per-asset basis |

| Was it first used or installed ready for use in time? | Ordering isn’t enough if the asset isn’t ready |

Practical rule: The write-off is about when the asset is ready for business use, not when you first started thinking about buying it.

The instant asset write off 2025 is valuable because it rewards decisive, well-timed investment. But it only works when the asset, the business and the dates all line up.

Confirming Your Eligibility Who Can Claim the IAWO

Eligibility usually comes down to three issues. Your business size. The type of asset. The date the asset becomes ready for use.

Miss any one of those, and the claim can fall apart.

Turnover test

The write-off is available to small businesses that fall within the required turnover threshold. In practice, that means you need to check whether your business is within the small business eligibility rules for the year you’re claiming.

The word aggregated matters. It means you shouldn’t look at one entity in isolation if there are connected businesses or related structures involved. Owners with a company, trust, partnership or side entity often trip up here because they assume each structure stands alone.

That assumption can create problems when:

- A family group operates through multiple entities

- A trading company and a separate service entity are linked

- A business owner controls more than one operation

- Revenue is split across structures for commercial reasons

If your setup is simple, the answer may be straightforward. If you’ve got connected entities, it’s worth checking before you commit to the purchase.

Asset type

Not every outgoing qualifies just because it helps the business.

The write-off applies to eligible depreciating assets. Broadly, these are assets that decline in value over time and are used in the business. Many common business items fit that description, but some costs don’t.

A practical way to think about it is this:

| Usually in scope | Usually needs closer review or is outside scope |

|---|---|

| Tools and equipment | Building works and structural improvements |

| Business machinery | Items that aren’t depreciating assets |

| Office technology | Costs treated under other tax rules |

| Business-use additions to qualifying assets | Assets that fail the timing or use tests |

If you’re unsure whether something is an asset improvement, a repair, or a different type of deduction altogether, get it checked before year end. Classification affects the tax outcome.

Ready for use matters more than the invoice date

This is one of the most common misunderstandings.

Placing an order doesn’t automatically secure the deduction. Paying a deposit doesn’t do it either. The critical point is whether the asset is first used or installed ready for use within the relevant period.

That practical distinction matters with:

- custom equipment that takes time to deliver

- vehicles delayed in stock

- software implementation that isn’t finished

- machinery sitting in a box, uninstalled

An asset can be paid for and still miss the write-off if it isn’t ready for business use by the deadline.

Business use also has to be real

If an asset has mixed use, only the business portion is claimable. That means you need a reasonable basis for apportionment and records that support it.

For example:

- a laptop used partly for personal purposes

- a vehicle with private travel

- equipment shared across business and non-business use

That doesn’t stop a claim. It just means the deduction must reflect actual business use rather than a rough guess.

Business structure doesn’t remove the need for care

Sole traders, partnerships, companies and trusts can all face the same core tests. The structure changes administration and tax context, but it doesn’t remove the need to check turnover, asset eligibility and timing.

Owners often focus on the headline rule and miss the detail. The headline gets attention. The detail determines whether the claim stands up.

The $20,000 Threshold Explained with Worked Examples

A business owner approves three purchases in May. A new coffee machine, a grinder and a POS terminal all support revenue straight away. The tax result depends less on the total spend than on how each asset is priced and identified.

The key rule is simple. The threshold applies per asset. It does not apply per invoice, per supplier or as a single annual cap across all purchases.

Example one with multiple eligible assets

Take that café example. If the coffee machine, grinder and POS terminal are separate assets and each costs less than $20,000, each item can potentially be claimed in full, assuming the other eligibility rules are met.

That point matters because many owners wrongly treat the threshold like a shopping budget. It is not. Several qualifying assets can still produce an immediate deduction if each one stands on its own and the invoice makes that clear.

A practical issue comes up here. If a supplier rolls everything into one vague line item, the tax position gets harder to defend. Clear itemisation often makes the difference between a straightforward claim and a messy year-end review.

Example two with a threshold edge case

A consultant buys a laptop for $19,999 and uses it wholly for business. On the face of it, that sits under the cap, so the full cost may be deductible in the year of purchase rather than spread over time.

The main planning value is cash flow. Bringing the deduction forward can leave more money available for debt reduction, a super contribution or working capital instead of waiting for depreciation claims to build gradually. That is the kind of decision we work through in tax planning advice for business owners, because the asset purchase should support the wider plan, not just this year's return.

Example three when the asset is over the cap

Now change the numbers. The business buys one item for $20,500.

That asset generally does not qualify for the immediate write-off under the threshold rule. It will usually be dealt with under the small business depreciation rules instead, which means the deduction is spread differently. The commercial decision may still be right, but the tax timing changes, and that affects how much cash stays in the business after tax.

I see this catch owners out when a quote creeps up late in the process. Freight, accessories, installation or a service package can push the asset over the line if they form part of the asset cost. A purchase that looked tax-effective at first can end up producing a much smaller first-year deduction than expected.

Common planning mistakes around the threshold

The errors are usually practical, not technical.

- Bundling separate assets poorly so the invoice does not show distinct items clearly

- Focusing on total spend instead of testing each asset separately

- Forgetting to reduce the claim for private use on mixed-use assets

- Approving a quote without checking the final asset cost once add-ons are included

- Buying an asset for the deduction alone even though it does little for profit, efficiency or business value

A simple decision filter

Use this check before signing off on the purchase:

| Question | Good sign | Warning sign |

|---|---|---|

| Does the asset improve the business? | It raises capacity, reliability or efficiency | The main reason is “it’s deductible” |

| Is each asset clearly under the threshold? | Separate items are priced clearly | Bundled pricing blurs what was bought |

| Will the tax outcome support a broader goal? | Tax saved can reduce debt or build retirement savings | The purchase strains cash flow for little strategic benefit |

| Can the business-use percentage be supported? | Logs, usage records or policy make the claim clear | Private use is substantial or poorly tracked |

Used properly, the threshold gives small business owners timing power. Used badly, it produces rushed spending and disappointing cash flow. The strongest results come when the purchase improves the business first, then the tax saving is directed into wealth building through debt reduction, super top-ups and the sort of structured decision-making we build into Guided Growth and Retirement Roadmap advice.

Strategic Tax Planning with the Asset Write-Off

A business owner approves a vehicle fit-out in May, claims the deduction, and then reaches August short on cash for BAS, loan repayments and super. I see this often. The tax result looks good on paper, but the actual outcome is weaker because no one decided in advance what the tax saving was meant to achieve.

The instant asset write-off works best inside a broader plan. If the asset already makes commercial sense, the deduction can improve after-tax cash flow and give you options. Those options matter more than the deduction itself.

Used well, the write-off can support priorities such as:

- reducing expensive business or personal debt

- making super contributions while taxable income is still high

- protecting working capital during a growth phase

- funding the next investment that lifts profit or efficiency

That is the difference between compliance and strategy. A deduction only lowers the cost. It does not fix a poor purchase, weak cash flow, or a lack of direction for the tax saved.

Put the tax saving to work

The better question is not, “Can I claim this?” It is, “What will this claim help me do next?”

For some owners, the best use of the tax benefit is debt reduction. If you are carrying high-interest equipment finance, credit cards, or a mortgage with investment plans on hold, directing the tax saved into repayments can improve cash flow faster than leaving the benefit to disappear into day-to-day spending.

For others, super is the smarter destination. Owners in strong profit years often want to build retirement capital while tax rates are still meaningful. In that situation, the deduction can help create room for concessional contributions, especially where retirement planning has been delayed while the business took priority.

This is the planning lens we use in Guided Growth and Retirement Roadmap work. The asset purchase is only one decision. The more important decision is where the released cash goes after the deduction lands.

A practical way to decide

Before committing to the purchase, set the tax outcome against a clear financial objective.

| If your priority is… | The write-off is useful when… | Poor use looks like… |

|---|---|---|

| Debt reduction | the tax saved is earmarked for repayments | the benefit is absorbed by general spending |

| Retirement savings | the cash saving supports planned super top-ups | super remains “something to do later” |

| Business growth | the asset improves capacity or margin | the purchase adds cost without a clear return |

| Cash stability | timing still leaves enough working capital | the deduction creates pressure after purchase |

This approach keeps the write-off connected to wealth building. That matters because small business owners often build wealth across several fronts at once. The business, the home loan, super, and family cash flow all compete for the same dollars.

Keep the bigger plan in view

The owners who get the most from the instant asset write off 2025 usually pre-allocate the benefit. They decide before purchase whether the tax saved will reduce debt, fund super, or support the next stage of growth.

If you want the asset decision to strengthen both the business and your personal balance sheet, broader taxation and tax planning advice should sit alongside the purchase decision. That is how a tax deduction becomes part of Guided Growth today and a stronger Retirement Roadmap later.

How to Claim the Write-Off and Keep Proper Records

The claim itself isn’t where most problems start. The problems usually start months earlier, when records are incomplete or the purchase wasn’t structured cleanly.

What needs to happen before claim time

You need more than a tax invoice. The ATO will expect the underlying facts to support the deduction.

Keep records that show:

- What was purchased and how the asset is described

- When it was bought

- When it was first used or installed ready for use

- How much of the use was business-related

- How payment was made and by which entity

If the asset has mixed use, record how you arrived at the business-use percentage. The more practical and consistent the method, the easier it is to defend.

A clean process works best

The simplest process is usually the strongest one:

Review the quote before purchase

Make sure the asset is clearly identified and the pricing is sensible.Check timing risk

Delivery delays and installation issues can affect the outcome.Keep the invoice and proof of payment together

Don’t leave documents scattered across inboxes and cards.Document the ready-for-use date

This matters more than many owners realise.Record business use promptly

Don’t try to reconstruct it at tax time from memory.

What the ATO tends to focus on

In practical terms, audit risk often rises when the story doesn’t line up. The invoice may say one thing, the asset arrives later, and nobody can show when it was operational.

Good records don’t create a claim. They protect a valid one.

If the asset is above the threshold, it generally won’t get immediate full deduction treatment under the under-threshold rule. Instead, it may go into the pool under the simplified depreciation system. That makes it even more important to classify the purchase correctly from the start.

A sensible tax planning review before year end can also prevent owners from overclaiming. If you’re looking at ways of legitimately lowering tax while staying on solid ground, this guide on how to reduce taxable income in Australia is a useful companion read.

Record-keeping habits that save headaches

| Habit | Why it helps |

|---|---|

| Store invoices centrally | Makes year-end review easier |

| Save installation evidence | Supports ready-for-use timing |

| Track private use early | Reduces guesswork |

| Match asset to business purpose | Shows commercial rationale |

Most write-off issues are preventable. Clean paperwork and clear timing solve a lot.

Frequently Asked Questions about the IAWO

A common year end scenario goes like this. A business owner buys equipment, assumes the tax deduction is straightforward, then finds the critical questions start after the purchase. Can it be second-hand? What if there is private use? What happens if the asset is sold later?

These are the points that affect planning.

Can I claim second-hand assets

Yes, provided the asset otherwise qualifies. The rule can apply to eligible depreciating assets whether they are new or second-hand, so long as the cost, business eligibility, and timing requirements are met.

For many owners, second-hand equipment can be the better commercial decision because it reduces upfront borrowing while still bringing forward a deduction. That can leave more cash available for debt reduction or a super contribution instead of tying every dollar up in brand-new plant.

What about GST

GST changes the claim amount. If your business is registered for GST and entitled to claim input tax credits, the asset cost for depreciation purposes is generally worked out excluding GST. If you are not registered, or cannot claim the full credit, the treatment can differ.

This is a common place where owners overstate the deduction. The invoice total is not always the tax value of the asset.

What happens if I sell an asset later

The tax effect does not stop at the initial write-off. If you later sell, trade in, or scrap the asset, that event can create an adjustment that flows through your tax position.

That matters for planning. An immediate deduction helps cash flow now, but the longer-term result still depends on how long you keep the asset and what you recover on sale.

Is the 2025 to 2026 extension actually in place

Yes. The extension of the $20,000 threshold for the 2025 to 2026 income year has been legislated, as noted earlier.

For practical decision-making, work from the law as enacted, not from headlines or pre-budget commentary.

Wasn’t there talk of a higher threshold

Yes, but proposed thresholds only matter if they become law. For tax planning, use the legislated $20,000 threshold unless and until Parliament changes it.

That sounds obvious, but plenty of poor buying decisions start with an optimistic assumption about a rule that never took effect.

Is this the same as temporary full expensing

No. They are different measures with different settings. Temporary full expensing was broader. The current instant asset write-off is narrower and depends much more on the threshold and eligibility rules.

Using old terminology can create expensive misunderstandings, especially if a purchase sits close to the limit.

Can I just buy something before 30 June and claim it

Purchase date alone is not enough. The asset generally needs to be first used, or installed ready for use, by the relevant deadline.

That distinction catches people every year. Paying a deposit in June does not fix a late delivery in July.

Does every asset under the threshold qualify

No. Cost is only one test. You also need to consider whether the item is an eligible depreciating asset, how much of it is used for business, and whether your business meets the small business rules.

Strategy is more important than speed. A rushed purchase can get a deduction. A well-planned purchase can get the deduction, improve operations, and leave room to put the tax saving toward stronger cash reserves, faster debt reduction, or personal wealth goals through Guided Growth and Retirement Roadmap planning.

If a purchase is borderline on timing, business use, or classification, get advice before you commit. The best IAWO decisions support both this year’s tax outcome and your longer-term wealth position.

Turn Tax Deductions into Long-Term Wealth

The instant asset write off 2025 is useful, but only when it supports a sound business decision. The asset should improve operations. The tax deduction should improve timing. The financial strategy should decide what happens next.

That sequence matters.

A well-timed deduction can reduce tax pressure, free up cash and create room for bigger priorities such as debt reduction, super contributions or stronger reserves. That’s where the write-off stops being a compliance topic and starts becoming part of a wealth-building plan.

Most missed opportunities don’t come from not knowing the rule exists. They come from treating it too narrowly. Owners focus on the tax return and ignore the broader financial move the deduction makes possible.

If you’re considering an asset purchase before year end, or planning ahead for the next income year, the best question isn’t whether you can claim it. It’s whether the purchase fits your business plan and your personal goals at the same time.

If you want clarity on whether an upcoming purchase fits your broader strategy, book a free initial call with Wealth Collective. We can help you assess the tax position, the cash flow impact and how the savings could support guided growth now or a stronger retirement roadmap later.