Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Over A$1 trillion is projected to change hands in Australia by the mid-2030s. For many families, that sounds like a national headline. In practice, it's personal. It affects the family home, super, business interests, inheritances between siblings, and the stress that can follow when no one is clear on the plan.

A lot of writing on intergenerational wealth transfer stays abstract. That's a problem in Western Australia, where families often need practical guidance on property, super, tax, insurance, and succession decisions that don't fit a one-size-fits-all template. As noted in research on wealth transfer and household financial risk in WA, existing commentary often under-explores how these transfers reshape household financial risk profiles, leaving pre-retirees and younger families without a clear framework for turning an inheritance into an organised plan.

The Great Australian Wealth Transfer Is Here

The phrase intergenerational wealth transfer can sound like industry jargon. It isn't. It refers to money and assets moving from one generation to the next, either during life or after death. In Australia, that transfer is now large enough that families can't afford to treat it as an afterthought.

For WA households, the issue isn't only the size of the transfer. It's the number of moving parts attached to it. A parent may want to leave the home to one child, equalise outcomes for others, support grandchildren, and avoid unnecessary tax on super. A business owner may want continuity for the operating child without creating resentment in the wider family. A recently retired couple may want to help children now, but still protect their own retirement security.

Why generic advice falls short

A lot of online content borrows heavily from overseas estate planning models. That often creates confusion for Australians, especially around superannuation, death benefit nominations, and the way family trusts fit into a broader estate plan.

WA families also tend to bring their own mix of issues to the table:

- Property-heavy wealth: The family balance sheet is often dominated by the home, investment property, or both.

- Small business complexity: Some families hold wealth through a company, trust, or farm structure rather than in personal names.

- Distance and blended families: Adult children may live interstate or overseas, and second marriages can complicate intent and fairness.

Practical rule: A good wealth transfer plan doesn't just say who gets what. It sets out how assets move, when they move, and what that means for tax, control, and family harmony.

That's why the right framework matters. You're not only trying to pass on wealth. You're trying to pass it on in a way that supports the people receiving it, reduces friction, and preserves options if life changes.

What Intergenerational Wealth Transfer Means for Your Family

Think of intergenerational wealth transfer like a relay race. One generation builds momentum. The next either carries that momentum forward or drops the baton because the handover was rushed, vague, or poorly structured.

In Australia, this matters now because the transfer is no longer theoretical. Intergenerational wealth transfer is projected to reach over A$1 trillion by the mid-2030s, and the average net worth of households headed by someone aged 65 or over is more than double the national average, setting the stage for substantial transfers as the large baby boomer-era cohort ages.

What actually counts as a transfer

Many people assume this only means an inheritance after death. It includes more than that.

A transfer can involve:

- The family home: Passed through an estate or sold and the proceeds distributed.

- Superannuation: Paid under super rules, which don't automatically follow your will.

- Gifts during life: Money for a home deposit, school fees, or business support.

- Investments and business assets: Shares, trust interests, or private company equity.

That's where families often get caught out. They think one will covers everything, when in reality some assets sit outside the estate and need separate attention.

Why families get confused

The most common confusion is assuming legal ownership, tax treatment, and control all mean the same thing. They don't.

A parent might intend for a child to receive an asset. But if the paperwork is outdated, the beneficiary structure is wrong, or the asset sits in super or a trust, the result may be very different from what the family expected. If you've never reviewed the basics, start with this guide on what happens if you don't have a will.

A transfer only works well when the documents, tax position, and family intent all line up.

A useful way to think about it is as a family garden. One generation plants and tends it. The next generation doesn't just inherit the fruit. They inherit the condition of the soil, the structure around it, and the habits needed to keep it growing.

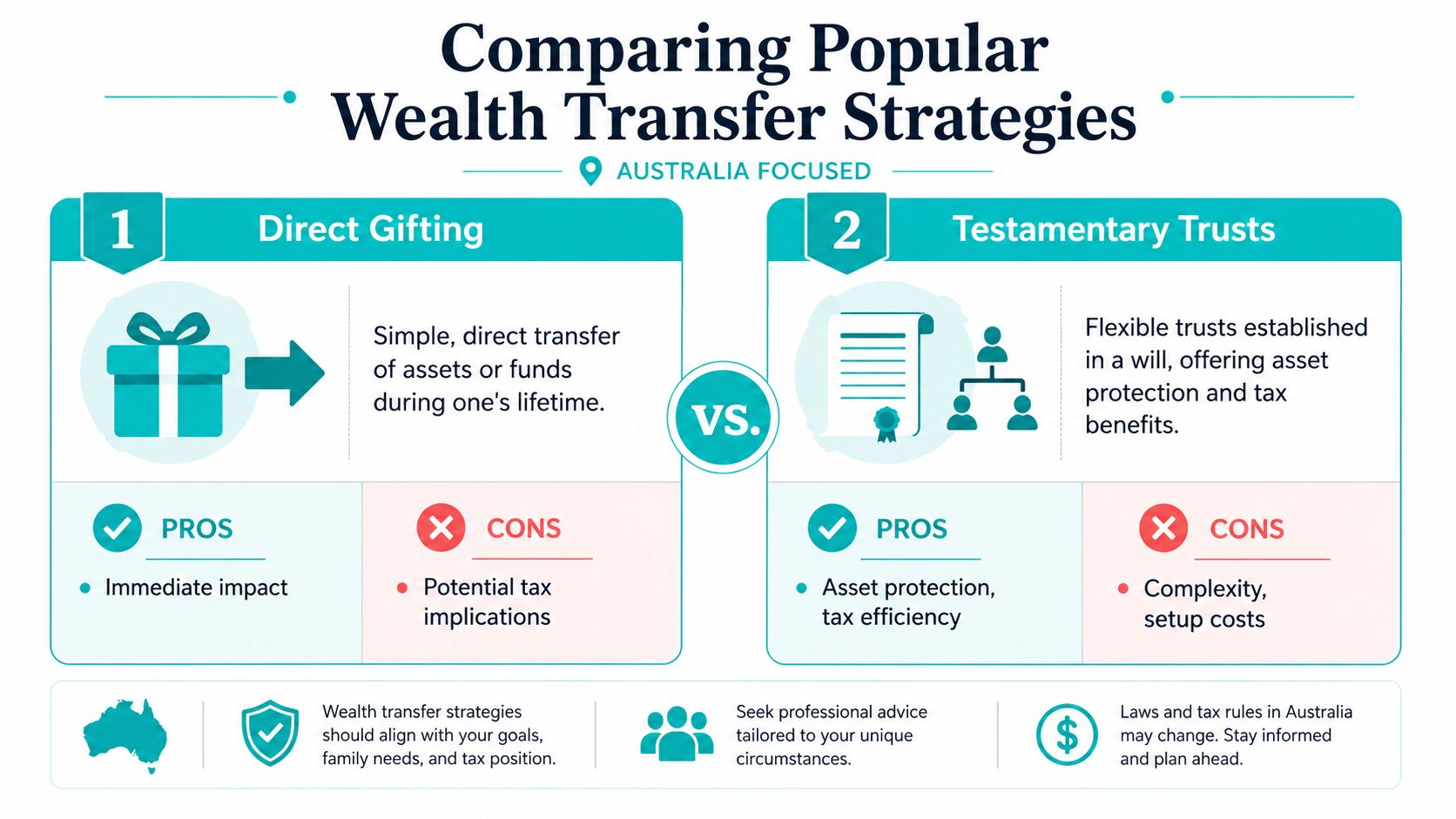

Comparing Popular Wealth Transfer Strategies

No single strategy suits every family. The right option depends on the asset, the beneficiary, the timing, and the level of control you want to keep.

Below is a simple comparison before we unpack the detail.

Australian Wealth Transfer Strategy Comparison

| Strategy | Best For | Tax Implications (Simplified) | Level of Control |

|---|---|---|---|

| Direct gifting during life | Parents wanting to help now with cash or selected assets | Can trigger tax or transfer consequences depending on the asset | Low once given |

| Will-based transfer | Straightforward estates and simple family arrangements | Depends on the asset and recipient | Moderate |

| Testamentary trust | Families wanting more asset protection and flexible control for beneficiaries | Can improve tax efficiency depending on circumstances | High |

| Super death benefit nomination | Passing super in a deliberate way | Depends heavily on whether the recipient is a dependant | Moderate to high |

| Business succession planning | Business owners wanting continuity and fairness across family members | Structuring matters and needs early planning | High |

| Life insurance proceeds | Creating liquidity for dependants or estate equalisation | Depends on ownership structure and recipient | Moderate |

Direct gifts versus structured transfers

A direct gift is simple. You transfer money or an asset during your lifetime and the recipient gets immediate use of it. That can be useful when parents want to help with a first home, education costs, or an early inheritance.

The trade-off is control. Once the gift is made, you usually can't decide how it will be used. There may also be tax or transfer consequences depending on the asset involved.

A structured transfer, such as through a testamentary trust, is slower and more deliberate. It can help where a beneficiary is young, vulnerable, in a high-risk profession, in a relationship that may not last, or not ready to manage a large inheritance outright. If you want a practical overview, this article on what is a testamentary trust in Australia is a useful starting point.

Super needs its own decision

Superannuation is where many otherwise well-organised estates go off track.

In Australia, taxed-element super balances can pass tax-free to dependants, but non-dependent adult children generally pay 15% plus the Medicare levy on the taxable component. For larger balances, that can mean tens of thousands of dollars in tax for a non-dependant beneficiary.

That leads to a very practical question. If two adult children are set to receive wealth, should they receive the super equally, or should some assets be reallocated so the after-tax outcome is fairer? The answer depends on the estate mix.

The beneficiary written on paper isn't always the beneficiary who receives the best after-tax result.

When business interests are involved

A family business adds another layer. The challenge isn't just succession. It's balancing continuity, control, and fairness. One child may work in the business. Another may not. Equal shares on paper can create operational deadlock or force a sale.

That's why business owners often need a joined-up succession plan rather than a basic estate plan. If you want broader context, these strategies for high-net-worth individuals are helpful as background, especially for families dealing with layered assets and protection concerns.

A useful test is this:

- If simplicity matters most: A direct transfer or straightforward will may work.

- If protection matters most: Testamentary trusts deserve a close look.

- If super is a major asset: Death benefit planning becomes central.

- If a business is involved: Succession planning should happen well before retirement.

Navigating the Australian Tax and Legal Maze

Families usually focus first on who should inherit. The harder question is what the recipient gets to keep after tax, transfer costs, and poor structuring.

The Melbourne Institute's HILDA Survey indicates that around 20 to 30% of households receive an inheritance, but the value clusters heavily among higher-income families. It also shows that for the top 10% of wealth holders, inheritances may explain more than 25 to 30% of their net worth, which is one reason tax-efficient planning matters so much.

Different assets create different problems

The family home, an investment property, listed shares, and super don't move under one neat rulebook.

A few examples show why:

- Family home: Often simpler from a tax perspective than investment assets, but ownership history and future use still matter.

- Investment property: Can carry capital gains tax issues and other transfer costs if handled poorly.

- Shares and managed investments: Timing and ownership structure can affect the eventual tax outcome.

- Superannuation: Paid under super law, not automatically under the will, which surprises many families.

If you haven't reviewed this before, it helps to understand what happens to super when you die, because super is often the asset that breaks the assumption that “my will covers everything”.

Timing matters as much as structure

Families often ask whether it's better to gift assets during life or pass them through the estate. The answer depends on the asset and the family's goals.

Giving now may help a child when they need it most. But it can also create tax consequences, reduce the giver's retirement buffer, and make fairness harder if later circumstances change. Waiting until death can preserve control, yet it may also miss opportunities to organise assets in a more efficient way.

A strong plan balances generosity with resilience. Parents still need enough flexibility for their own retirement, care needs, and changing family circumstances.

Legal documents must work together

The legal side isn't only about having documents. It's about having documents that are consistent.

That usually means checking:

- Your will: Does it reflect current wishes, relationships, and asset ownership?

- Super nominations: Are they valid, current, and aligned with the rest of the plan?

- Trust and company records: Do control provisions still work if someone dies or loses capacity?

- Powers of attorney: Can someone act if you can't?

Informal planning tends to fail in such situations. Families may have good intentions, but disconnected paperwork can produce an outcome no one wanted.

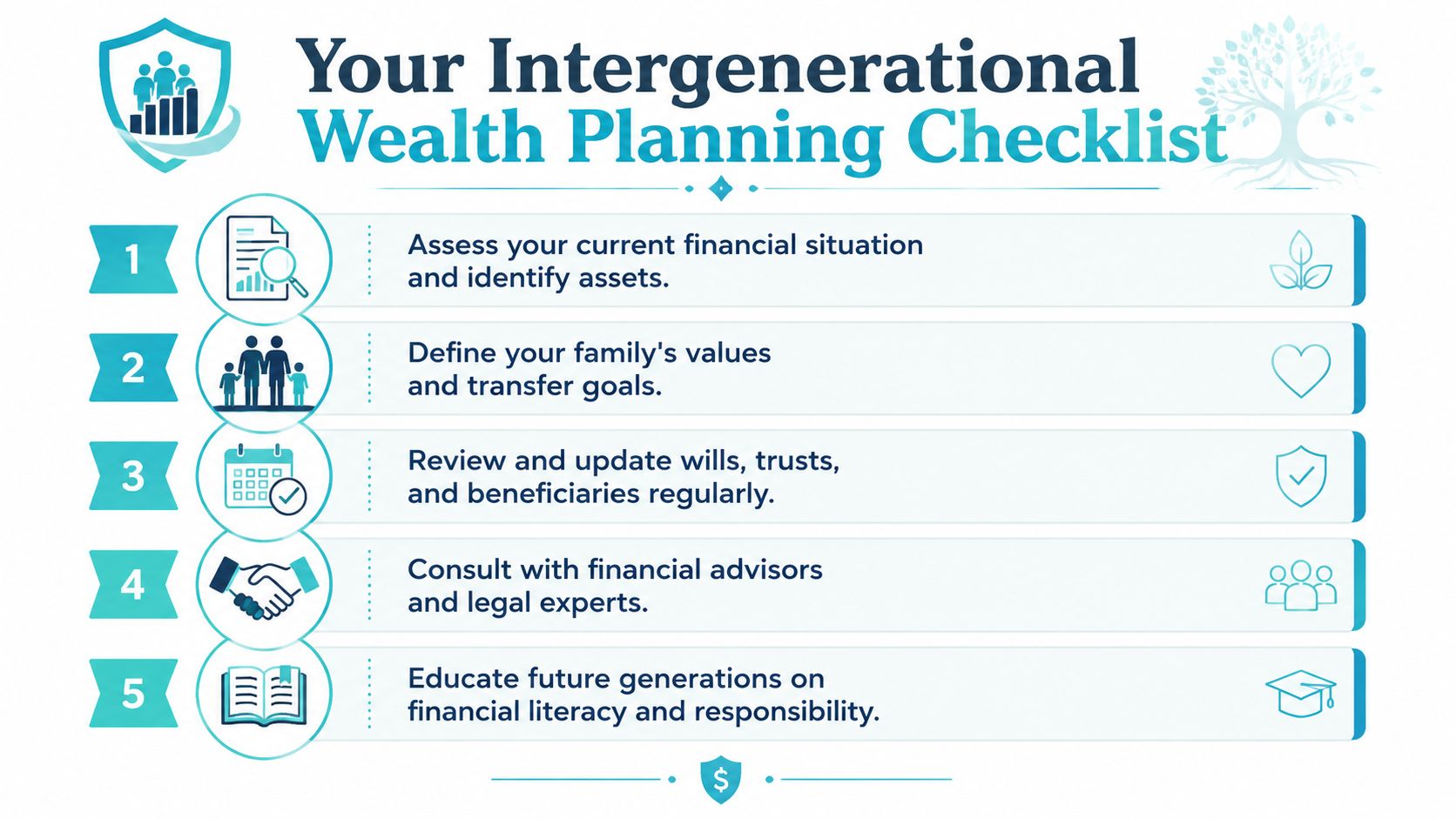

Your Intergenerational Wealth Planning Checklist

Many individuals delay estate and succession planning because it feels too big. The easiest way forward is to break it into a short list of decisions and actions.

The checklist below is practical enough to start this week. If you want a second framework to compare against, Brillant Law Firm's checklist is a useful reference point.

Start with clarity

Before changing structures or signing documents, get clear on what you own and what you want to achieve.

- List every asset: Include property, super, bank accounts, shares, trusts, companies, insurance, and debts.

- Separate legal ownership from intended beneficiaries: The person who owns an asset now may not be the person you want to benefit later.

- Write down your goals: Equal treatment isn't always equal outcomes. Some families want fairness, others want need-based support, and business families may prioritise continuity.

Then stress-test the plan

This is the part many people skip. They decide what seems fair, but don't ask how the plan holds up under real-world pressure.

Ask yourself:

- What if one child receives super and another receives property?

- What if a beneficiary divorces, goes bankrupt, or lacks financial discipline?

- What if a family member dies first?

- What if aged care or health costs change the plan late in life?

Key check: If your plan only works when everything goes perfectly, it isn't robust enough.

The core checklist

Review your will

If it's old, generic, or written before major family changes, it may no longer do the job.Check super nominations

Many people forget these entirely, or assume the nomination is permanent when it isn't.Map control of trusts and companies

Ownership and control are not the same thing. That distinction matters.Consider whether gifting now makes sense

Early support can be valuable, but only if it doesn't weaken your own position.Talk to family early

You don't need to disclose every figure. But explaining the reasoning behind key decisions can reduce conflict later.Teach the next generation how to manage wealth

A transfer works better when recipients understand investing, debt, tax basics, and long-term decision-making.

Common Wealth Transfer Pitfalls to Avoid

One of the biggest mistakes I see is people using generic estate planning material and assuming it applies neatly in Australia. It often doesn't.

In Australia, wealth-transfer planning commonly uses a blend of wills, binding death benefit nominations, and discretionary family trusts, which is quite different from the more trust-dominated models often described in US content. When families overlook these Australia-specific structures, the plan can become incomplete or misleading.

The mistakes that cause the most trouble

Some pitfalls are technical. Others are behavioural.

- Using a DIY will for a complex estate: If there's super, a business, a trust, or a blended family, a very simple will can leave major gaps.

- Forgetting to update nominations: Divorce, remarriage, children, and retirements all change the planning picture.

- Treating super like an ordinary estate asset: It isn't. That assumption causes real problems.

- Focusing only on tax: Saving tax matters, but not if the structure creates confusion, disputes, or loss of control.

- Avoiding family conversations: Silence may feel easier now, but it can increase suspicion later.

A better standard

Good planning isn't about chasing the cleverest structure. It's about making sure the structure matches the family.

Some families need simplicity. Others need stronger asset protection. Others need a way to deal fairly with a business child and non-business children. The mistake is assuming one document or one online template can solve every version of that problem.

Generic advice can be useful for orientation. It's rarely enough for implementation.

If your estate includes super, property, trusts, or business interests, local advice matters because the rules, documents, and sequencing all need to fit together.

Secure Your Family's Future with Wealth Collective

Intergenerational wealth transfer can create tremendous opportunity for a family. It can also create avoidable tax, confusion, and conflict when no one has joined up the legal, super, insurance, investment, and succession pieces.

That's why a clear process matters. For some families, the immediate need is risk management and document review. For others, it's investment structuring, super strategy, or retirement cash flow. Business owners often need an added layer of succession planning, and broader reading on essential estate planning for business owners can help frame the issues before formal advice begins.

Wealth Collective helps families work through this using three practical service pillars: Protection Plus, Guided Growth, and Retirement Roadmap. That means the conversation doesn't stop at “who gets what”. It extends to protecting the balance sheet, improving tax efficiency where appropriate, and making sure your money can support both your retirement and your legacy.

If you're in Perth, Dunsborough, or elsewhere in WA and want clarity without jargon, start with a simple conversation. A good first meeting should leave you with more confidence, not more confusion.

If you'd like a practical next step, book an initial call with Wealth Collective. It's a straightforward way to clarify what you own, identify gaps in your current plan, and map out how to build, protect, and transfer wealth with more confidence.