Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You open your super statement, skim past the balance, then notice a small line item: insurance premium. It's been coming out for years, and there's a good chance you've never checked what it covers.

That's normal. It's also risky.

Life insurance through super is convenient, automatic, and easy to ignore. That convenience is exactly why so many Australians keep it without ever asking the hard question: if something went wrong, would this cover be enough? For plenty of people, the answer is no. The trap is worst for pre-retirees and families who assume default cover stays steady when it often doesn't.

Why You Need to Understand Your Super Insurance

It's common for insurance inside super to be treated like background noise. The cover was added by default, the premiums look modest, and the paperwork is buried in a portal you rarely log into. That doesn't mean the policy is bad. It means you shouldn't assume it fits your life.

The widespread nature of life insurance through super is evident. In 2025, 52% of Australians surveyed held life insurance through their superannuation, with Western Australians showing the highest uptake at 57%, according to Budget Direct's life insurance survey statistics. In the same data, the average life insurance claim from super funds was $135,000 in 2023, compared to $509,000 for retail policies.

That gap should stop you in your tracks.

Default doesn't mean adequate

A default policy is designed to cover lots of members at once. It's built for broad affordability and simple administration. It is not built around your mortgage, your children, your income, or the fact that your financial obligations may be very different from the next member in the fund.

If you're in WA, this is even more relevant. More people here rely on super-based cover than anywhere else in the country, based on that surveyed data. That means more households are exposed to the same blind spot: believing they're protected because they have some cover.

Practical rule: If you haven't read the insurance section of your super account in the last year, you should assume you don't yet know what you're covered for.

What to check first

Before you do anything complicated, answer these three questions:

- What cover do you hold: Death, TPD, income protection, or only one of them.

- How much is insured: The dollar amount matters more than the fact that cover exists.

- When does it reduce or end: Many default policies become dangerous at this stage.

That last point is the one most generic guides miss. A lot of people only discover the reduction in cover when they're older, more exposed, and harder to insure elsewhere.

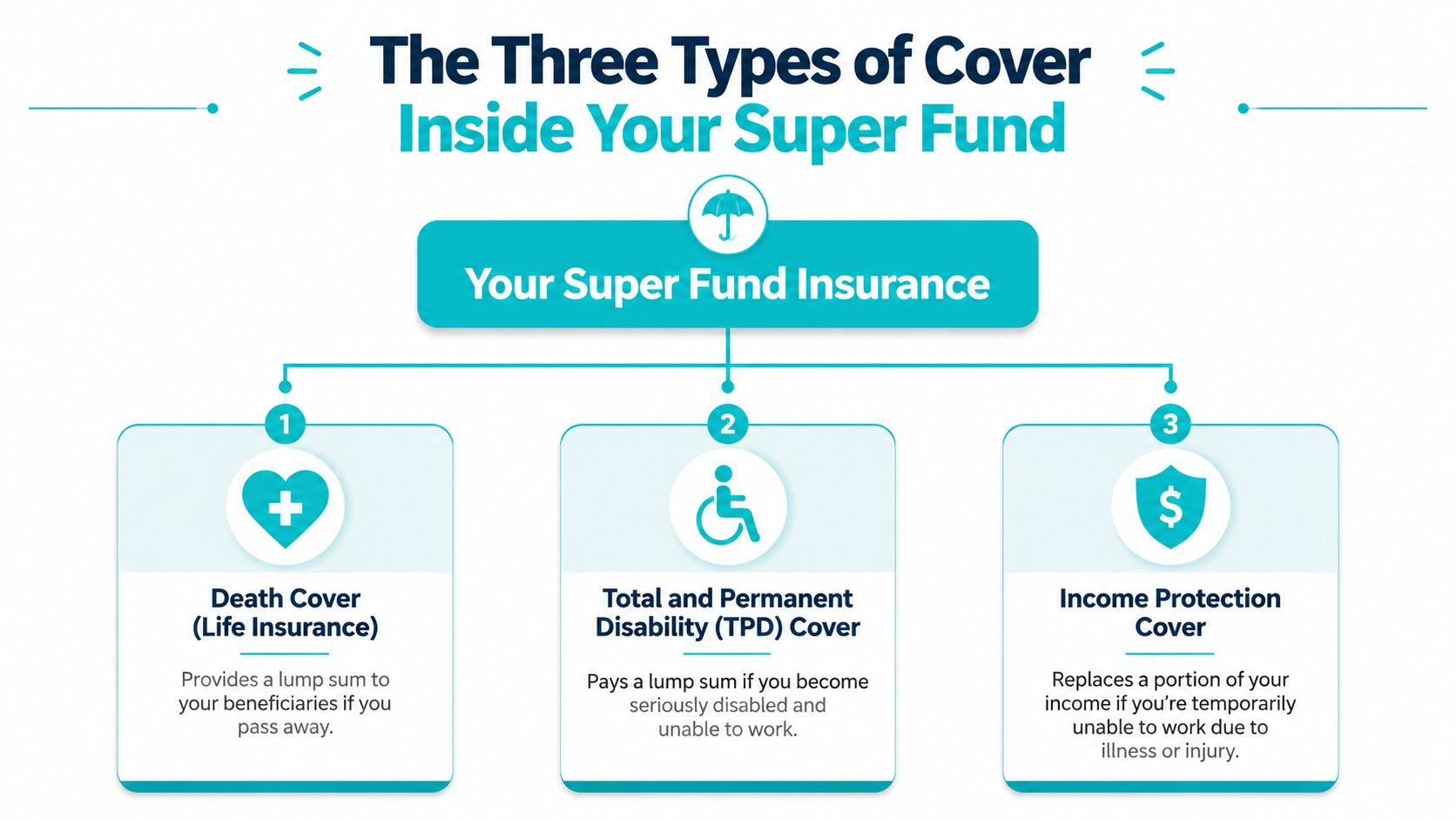

The Three Types of Cover Inside Your Super Fund

Insurance inside super usually falls into three buckets. If you don't know the difference, it's easy to overestimate what you've got.

Death cover

This is the policy many people mean when they say life insurance through super. If you die, it pays a lump sum to your beneficiaries, usually through the super fund first.

Think of it as a final financial handover. It can help your family cover debts, living costs, school fees, and the immediate disruption that follows a death. The key issue is amount. A default sum might sound reasonable until you compare it with the actual financial hole left behind.

TPD cover

Total and Permanent Disability cover pays a lump sum if you become seriously disabled and can't return to work under the policy definition.

This is the cover people underestimate most. Death cover protects your family if you're gone. TPD protects you if you're alive but unable to earn. That often means ongoing expenses, medical costs, home modifications, and a long period without normal income.

Income protection cover

Income protection is different. It usually pays a monthly benefit for a period if illness or injury stops you working temporarily.

It's closer to a replacement salary than a lump sum. That makes it useful, but the fine print matters. Waiting periods, benefit periods, and definitions vary widely. A policy inside super may be simpler than one held outside super, but simpler isn't always better.

Death cover is for the people you leave behind. TPD is for the life you still have to fund. Income protection is for the pay packet that stops when you can't work.

Who gets automatic cover and who doesn't

Automatic cover isn't universal. Automatic life and TPD insurance only begins at age 25, and if a member's balance is under $6,000, insurance does not start unless they actively request it or work in a hazardous job, as outlined by the Actuaries Institute's analysis of group insurance in superannuation.

That catches younger workers, new employees, casual staff, and people with interrupted work patterns.

If you want a plain-English breakdown of how these policies differ, our guide to life insurance types is a useful starting point.

The practical mistake people make

They assume “member” means “insured”.

It doesn't. You can have a super account and still have no default insurance in force, limited cover only, or cover that started years later than you think. Always confirm the status, not just the existence of the account.

The True Cost to Your Retirement Nest Egg

Paying premiums through super feels painless because the money doesn't leave your everyday bank account. That convenience is real. So is the trade-off.

According to Zurich's overview of life insurance in and outside super, life insurance premiums held within superannuation are typically paid from pre-tax contributions taxed at 15%, which can make funding cover tax-effective. But the same source notes the Productivity Commission estimated that for some members, premiums could reduce retirement balances by up to 28% ($125,000).

That's the core tension. Insurance inside super can be tax-smart today while still leaving you poorer at retirement.

Why the deduction feels smaller than it is

When premiums come from super, many people mentally file them as “cheap”. They aren't seeing the long-term opportunity cost. That money wasn't sitting idle. It was part of your retirement savings pool.

Every premium paid from super is money that doesn't stay invested for your future. Over long periods, that matters. The impact is more serious for people with lower balances, broken work history, or years of paying for cover they didn't really need.

The right question isn't just cost

A better question is this: am I paying for the right cover in the right place?

Sometimes the answer is yes. If cash flow is tight, using super can be a sensible way to keep important protection in force. In other cases, paying through super merely hides the cost and delays a proper review.

A useful habit is to look at your contributions, insurance deductions, and other recurring money decisions in one place. If you're trying to tighten your overall system, this personal finance tips for employer contributions resource can help you think more clearly about how regular contributions shape long-term outcomes.

A better way to judge the trade-off

Use this checklist:

- Keep cover in super when cash flow is the bottleneck: This can preserve protection you might otherwise cancel.

- Be sceptical if premiums have run untouched for years: Old settings often survive long after your life has changed.

- Review lower-balance accounts carefully: The retirement drag can hit harder when every dollar in super matters.

- Separate convenience from value: Easy deductions aren't the same as a sound insurance strategy.

Cheap premiums can be expensive if they quietly hollow out retirement savings or leave you underinsured when you need to claim.

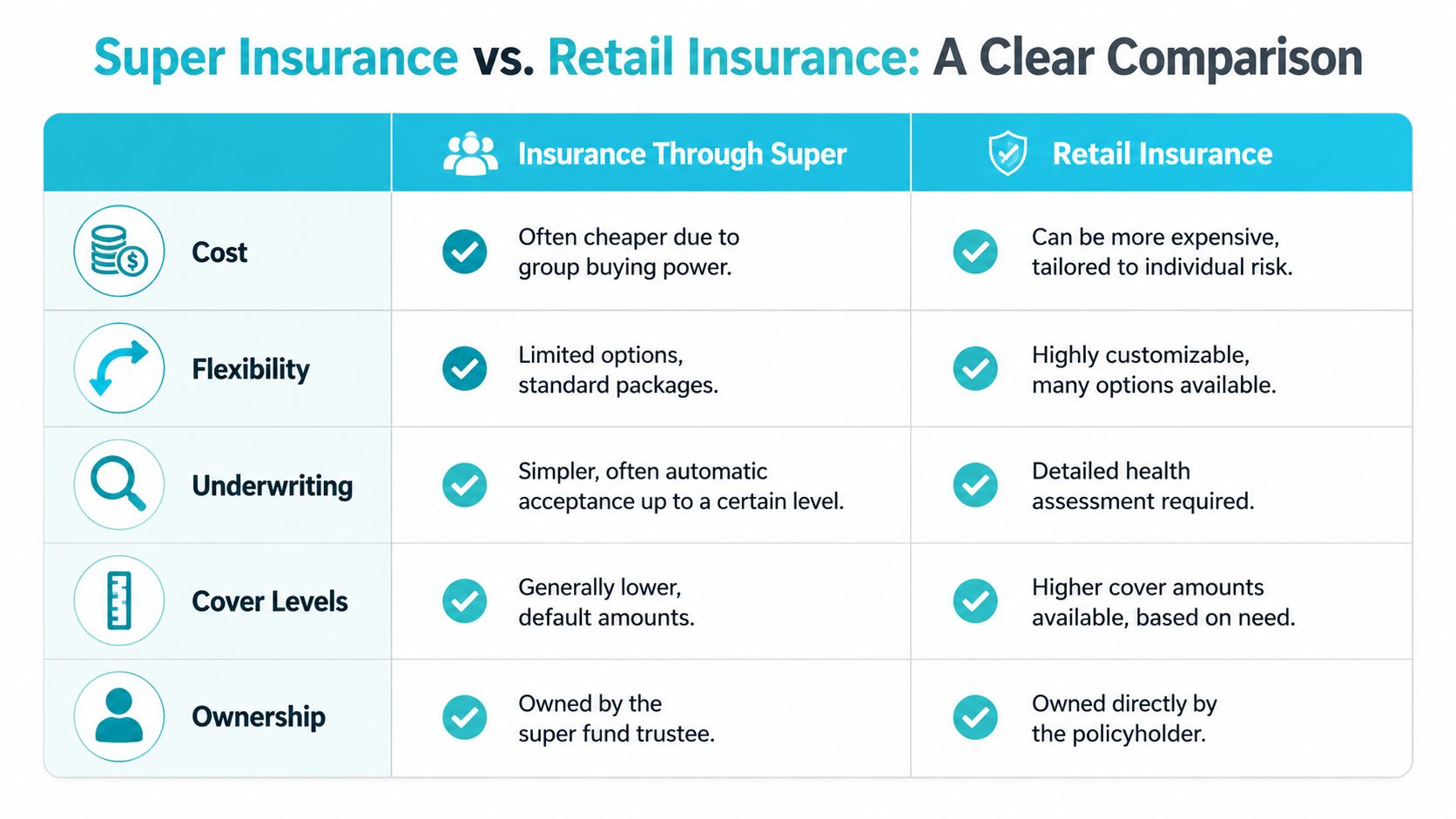

Super Insurance vs Retail Insurance A Clear Comparison

Most Australians don't need a lecture on theory here. They need a straight comparison.

Insurance through super is usually easier to get started with. Retail insurance bought through an adviser is usually more customized. The key question is whether convenience is worth the limitations.

Where super cover works well

Super-based cover can make sense if you want a basic safety net, straightforward administration, and premiums paid without squeezing monthly cash flow. Group arrangements can also make entry easier for some members.

That said, simplicity usually comes with less flexibility. You may get fewer design options, weaker tailoring, and definitions that don't line up with your occupation or actual needs.

Where retail cover usually wins

Retail insurance is built around the individual policyholder. That often means more choice over the amount insured, stronger policy design, and greater ability to match cover to debt, income, dependants, and profession.

The difference is most obvious when you look at claims. InsuranceWatch's comparison of superannuation insurance states that the average TPD claim payout from a retail policy purchased via an adviser is $643,000, whereas the average for a super fund policy is only $143,000. The same source notes that super fund TPD benefits may be subject to up to 22% tax if the member is under age 60.

That's not a small gap. It changes outcomes.

Insurance Through Super vs. Retail Insurance

| Feature | Insurance Through Super | Retail Insurance (via Adviser) |

|---|---|---|

| Cost | Often feels cheaper because premiums are deducted from super | Often higher upfront cost, but designed around the person insured |

| Customisation | Limited menu of options and default settings | Greater ability to tailor sums insured and structure |

| TPD definitions | Can be more restrictive and fund-driven | Often offers broader design options depending on policy |

| Ownership | Held through the super structure and trustee process | Owned directly by the policyholder |

| Claims outcome | Lower average TPD payout in the cited data | Higher average TPD payout in the cited data |

| Tax on payout | TPD benefits may face tax in some cases | Structure may differ depending on ownership and policy type |

| Expiry and changes | More likely to follow default fund rules | More scope to lock in suitable long-term design |

If you're comparing family protection options more broadly, this guide to find the best protection for your family is a helpful companion read.

You should also understand how tax treatment varies across policy structures. Our article on whether life insurance is tax deductible covers the practical issues Australians tend to miss.

A low premium is only a good deal if the policy still does its job when your family needs it.

The Hidden Risk for Pre-Retirees and Growing Families

The biggest problem with life insurance through super isn't just that the cover may be low. It's that many people assume it stays level when it often doesn't.

Stepped cover creates false confidence

Default TPD and life cover in super often use stepped benefit limits. That means the insured amount can reduce as you get older, especially as you approach retirement. Many members don't notice because the policy remains active. They see “insured” and assume the amount is stable.

That assumption can be disastrous.

Moneysmart's guide to insurance through super confirms that default cover typically ends entirely at age 70 for life and 65 for TPD. For pre-retirees, that creates a sharp protection gap at exactly the stage when replacing lost earning capacity can be hardest.

Why this hits at the worst time

Take a common WA household scenario. You're in your late fifties. You still have debt, maybe children who aren't fully independent, and a retirement date that's visible but not close enough to remove risk. You haven't reviewed your super insurance because you've had it for years and assume it's ticking along in the background.

Then you discover the TPD benefit has stepped down or is about to end.

That's not an admin detail. It's a structural weakness. You're older, underwriting may be tougher, and you have less time to recover from a poor insurance decision.

Growing families aren't safe either

This isn't only a pre-retiree issue. Families in high-expense years can also get caught because default cover rarely keeps pace with bigger mortgages, childcare costs, and a standard of living built around two incomes.

The problem is passivity. The fund doesn't know you upsized the home, had another child, or shifted into a more specialised occupation. Unless you act, the default settings stay in place.

- Check whether benefits step down by age: Don't rely on the summary screen alone. Read the schedule.

- Confirm end dates for each cover type: Death, TPD, and income protection can all work differently.

- Review after major life changes: A new mortgage, children, divorce, or business ownership should trigger a review.

The most dangerous insurance policy is the one you trust without checking.

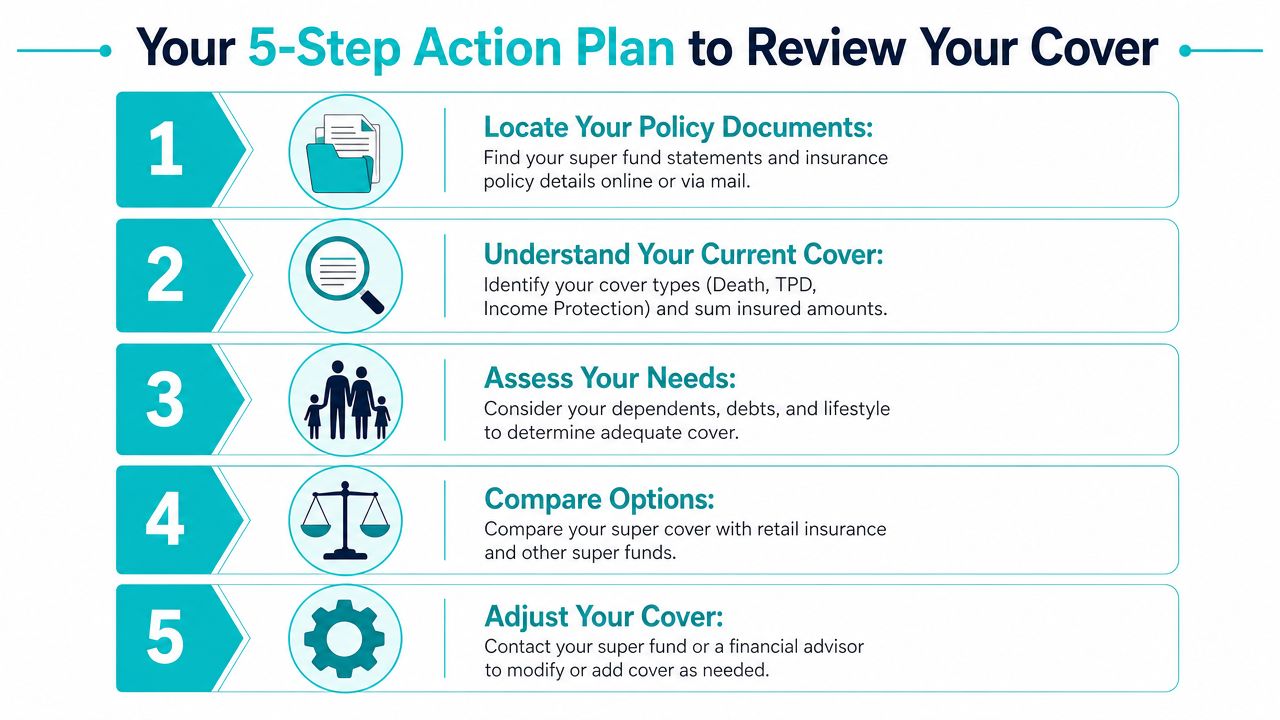

Your 5 Step Action Plan to Review Your Cover

You don't need to become an insurance technician. You do need a process.

Step 1 Find the documents

Log into your super portal and pull the insurance guide, latest statement, and any cover confirmation notices. Don't stop at the balance screen. You need the actual policy terms or member booklet.

If you can't find the cover amount, premium, expiry date, and definitions in a few minutes, call the fund and ask for them.

Step 2 Work out what you're protecting

Start with your obligations, not the product. List debts, ongoing household spending, dependants, and how long your family would need financial support if your income disappeared.

If you want to get your broader finances organised before doing this review, a practical guide to achieving financial clarity can help you centralise the information that affects insurance decisions.

Step 3 Hunt for red flags

Most reviews derive real value from the following. Look specifically for:

- Stepped cover: Benefits that reduce with age.

- Low sums insured: Amounts that won't clear debt or replace income meaningfully.

- Restrictive definitions: Especially around TPD and who qualifies for a claim.

- Expiry traps: Cover that ends before you expect.

Step 4 Compare your options properly

You're not only deciding between “keep” and “cancel”. You may be comparing default super cover, extra cover inside the fund, a different super arrangement, or cover held outside super.

If changing funds is part of the solution, our guide on how to switch super funds covers the practical steps and common mistakes.

Step 5 Get advice before making the final move

This is the point where DIY often breaks down. Replacing or adjusting insurance can trigger underwriting, changed definitions, or tax and ownership issues that aren't obvious from a summary page.

One option is to use an adviser-led review service that compares your current super-based policy with alternatives and checks whether the structure still suits your goals. Wealth Collective offers that kind of review as part of broader advice around personal insurance and super optimisation.

Key takeaway: Don't cancel old cover before new cover is approved and in force. That mistake is hard to unwind.

Build Your Financial Fortress with Wealth Collective

The right insurance setup depends on where you are in life.

If you're younger, the priority is making sure you have cover and locking in the right foundations early. If you're a high-income earner, default super insurance usually won't match your lifestyle risk or income exposure. If you're nearing retirement, stepped cover and expiry dates need immediate attention.

The blunt truth is this: life insurance through super is a starting point, not a complete strategy. It can be useful. It can be tax-effective. It can also be weak, outdated, or badly misaligned with what your family would need in a crisis.

Good advice should simplify that decision. It should tell you what you have, what it does well, where it falls short, and whether you should keep it, top it up, replace it, or restructure it. That's the kind of work that fits into a proper financial plan, not a guess based on a statement line item.

If you want clarity without the jargon, start with a short conversation and get your cover checked before the default settings make the decision for you.

If you want clear advice on your super insurance, retirement readiness, and overall protection strategy, book a free introductory chat with Wealth Collective. It's a simple way to understand what you've got, where the risks sit, and what to do next.