Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You're probably in one of two camps right now.

You're earning well, the mortgage is under control, super is building, and life feels like it's moving forward. Or you've just hit a stage where more people rely on you. A partner, kids, maybe staff, maybe ageing parents. Either way, the same question shows up fast once the novelty wears off. What happens if your income stops, or if you're no longer here?

Most Australians lump life insurance and income protection into the same mental bucket. That's a mistake. They solve different problems, pay in different ways, and fit different life stages. If you get the structure wrong, you can end up insured for the event you're least likely to face first, while leaving your day-to-day cash flow exposed.

Protecting Your Life vs Protecting Your Livelihood

A Perth couple I'd describe as typical of many clients are doing all the right things. They've bought a home, they're talking about a renovation, and one of them has just stepped into a higher-paying role. On paper, they're progressing. In reality, they're also more fragile than they were a few years ago.

That sounds harsh, but it's true.

When your lifestyle expands, your commitments expand with it. Repayments, childcare, school fees, subscriptions, holidays you've already budgeted for, and a retirement plan that assumes steady earnings. The biggest asset in that picture usually isn't the house or the super balance. It's your ability to keep earning.

That's where most confusion starts in the life insurance vs income protection conversation. People ask, “Which one is better?” That's the wrong question. The right question is, “What financial risk am I trying to solve first?”

If your family would struggle financially if you died, life insurance matters. If you'd struggle financially if illness or injury stopped you from working, income protection matters. For many households, both risks exist at the same time, but one is usually more urgent.

Your pay packet funds nearly every other financial goal you've got. Lose that, and the rest of the plan comes under pressure very quickly.

For readers comparing options in more depth, it's worth looking at your options for disability life insurance because disability-related cover often sits right beside this decision and shapes how much protection you need.

The point isn't to buy every policy available. The point is to match the right cover to the stage of life you're in now. A young professional with no dependants has a very different priority list from a family with a mortgage or a business owner whose income depends on showing up every day.

The Core Purpose of Each Cover

The cleanest way to understand life insurance vs income protection is this.

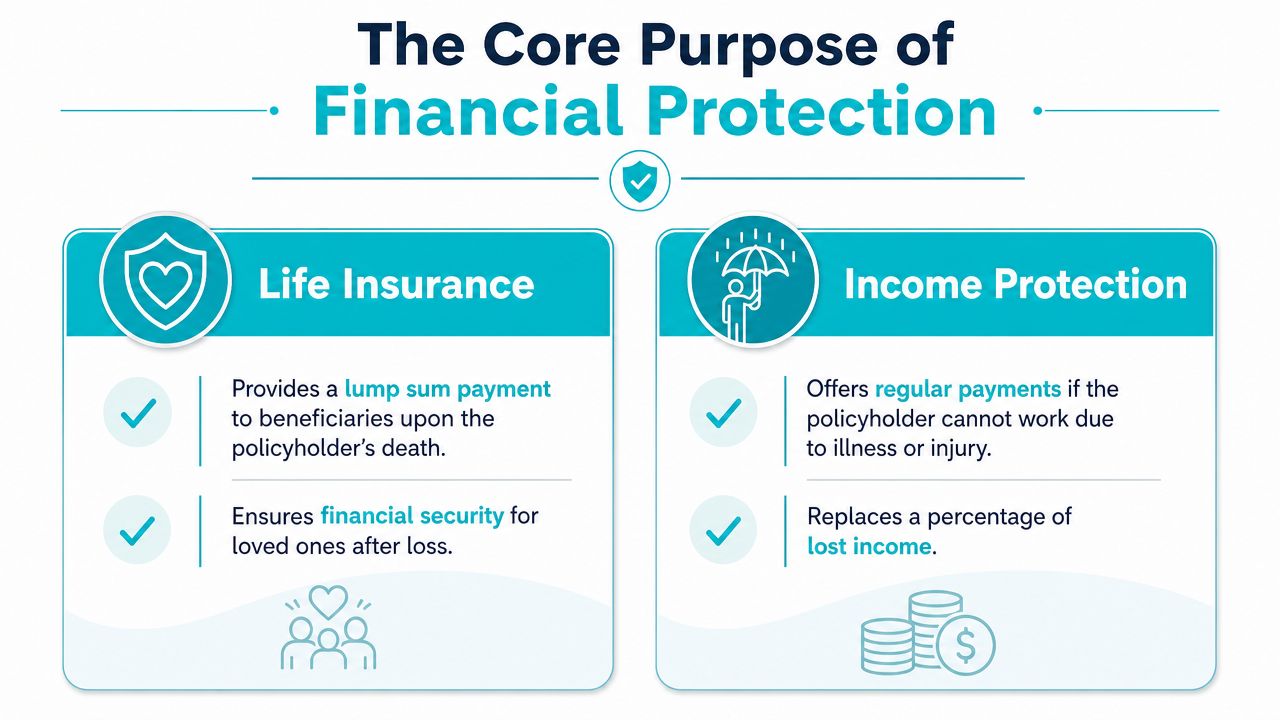

Life insurance is a financial parachute for your family. Income protection is the financial bridge that gets you over a career-interrupting injury or illness.

What life insurance is for

Life insurance is designed to create a lump sum if you die or are diagnosed with a terminal illness. That money gives the people left behind room to breathe. It can clear debt, protect the family home, support children, and stop your partner from having to make rushed decisions in the middle of grief.

It isn't meant to replace your monthly salary line by line. It's there to solve the bigger structural problem. How does the household keep going when one person's future earnings disappear altogether?

If you want a broader breakdown of policy structures, this guide to life insurance types is a useful place to compare how cover is typically set up in Australia.

What income protection is for

Income protection is different. It's built to support you while you're alive but temporarily or longer-term unable to work because of illness or injury. Instead of a one-off payout, it provides regular monthly payments to help cover the bills while you recover or adapt.

That matters because a far more common financial problem than death is interruption to earnings.

In Australia, the life insurance industry paid out $11.2 billion in claims in 2022, with Income Protection accounting for $3.7 billion of that total, making it the second-largest category after TPD, according to the Council of Australian Life Insurers claims data. That tells you something important. Income protection isn't a fringe add-on. It's a major part of how Australian households stay afloat when work stops.

The distinction people remember

Here's the simple version I give clients.

- Life insurance is about the people who depend on you if you're gone.

- Income protection is about keeping your financial life functioning if you're still here but can't earn.

- One protects a final event. The other protects an interruption.

- One is family-focused. The other is cash-flow focused.

There's also a useful contrast in international estate planning discussions. While the legal structures differ from Australia, California estate planning insights for ILITs show how seriously advisers treat life insurance when it's being used to protect intergenerational wealth rather than just cover a short-term expense.

If you remember nothing else, remember this. Life insurance protects the balance sheet your family would lose. Income protection protects the income stream your lifestyle depends on today.

Key Differences in Mechanics and Payouts

The biggest practical difference isn't philosophical. It's mechanical. These policies pay differently, trigger differently, and affect your cash flow in completely different ways.

Life Insurance vs. Income Protection At a Glance

| Feature | Life Insurance | Income Protection |

|---|---|---|

| Primary purpose | Protects dependants financially if you die or face terminal illness | Replaces part of your income if illness or injury stops you working |

| Payout style | Single lump sum | Monthly benefit |

| Who receives the money | Usually your beneficiary or estate | Usually you, the insured person |

| What it helps cover | Debt, living costs for family, future needs | Ongoing bills, mortgage, daily living costs |

| Best suited to | People with dependants, shared debt, legacy goals | People whose lifestyle relies on active earnings |

| Policy design focus | Total financial loss to the household | Temporary or longer work interruption |

For a more detailed local explanation of policy design and claim triggers, this overview of income protection insurance in Australia is a useful companion if you want to compare wording and common features.

How the payment process works

Life insurance is usually simpler at claim time. Claims are settled as a single lump sum payment, often processed within 14 to 30 days after medical verification, while income protection has a mandatory waiting period such as 30, 60, or 90 days before monthly payments start for a defined benefit period, as outlined in this Australian comparison of life insurance and income protection.

That difference matters more than is often understood.

If you die, your family usually needs immediate capital. They may want to clear the mortgage, create an emergency buffer, or reduce financial stress quickly. A lump sum suits that need.

If you're unable to work, the issue is ongoing income replacement. You don't need one large amount on day one nearly as often as you need a steady stream of money while expenses keep arriving every month.

Waiting periods and benefit periods

Income protection has moving parts you need to choose carefully.

- Waiting period means how long you self-fund before benefits start.

- Benefit period means how long the insurer can keep paying once your claim is accepted.

- Premium impact is direct. Longer waiting periods can reduce premiums, but they require a stronger cash buffer.

- Cash reserve strategy matters. If you only have a few weeks of savings, choosing a long waiting period can backfire.

Practical rule: Choose a waiting period your emergency fund can genuinely cover, not one that only looks cheaper on paper.

Do insurers actually pay claims

Scepticism is healthy, but blanket cynicism usually isn't. Valid claims do get paid. In Australia, retail life cover claims were paid at 97% and retail income protection claims at 95%, according to the 2024 life insurance claims and disputes statistics summary.

That doesn't mean every policy is equal. Definitions, exclusions, disclosure quality, occupation type, and the way the cover was set up all matter. But the data should give you confidence that these products are built to respond when they're structured properly and the claim fits the policy terms.

Cost and Tax Implications for Australians

Price matters, but tax treatment can matter just as much. I've seen people focus so hard on premium cost that they ignore where the policy sits and how benefits will be taxed later. That's short-sighted.

What usually drives the premium

With life insurance, premiums generally rise with age, health risk, smoking status, cover amount, and policy structure. Income protection premiums also depend on occupation, income, waiting period, and benefit period. Two people earning similar money can pay very different premiums if one works at a desk and the other works in a physically demanding role.

That's why the cheapest policy is rarely the best policy. Cheap cover can become expensive if the waiting period is wrong, the definition of disability is poor, or the monthly benefit doesn't line up with your actual expenses.

The tax question most people miss

The important Australian nuance is where the policy is held. Income protection premiums paid outside super are generally tax-deductible, while policies held inside super are paid with pre-tax contributions, but claim payouts may be taxed as income, which can affect long-term cash flow, as explained by Moneysmart's guide to income protection insurance.

That single detail changes the quality of the strategy.

If you hold income protection outside super, the premium deduction can help now. If you hold it inside super, you may preserve personal cash flow today, but the claim outcome can be less clean later because of how benefits may be taxed.

For a focused breakdown of that issue, this explanation of whether income protection is tax deductible is worth reading before you sign anything.

Why inside vs outside super isn't a minor detail

People often assume “inside super” automatically means smarter because it feels efficient. Sometimes it is. Often it isn't.

Consider the actual planning trade-offs:

- Outside super can support cleaner cash-flow planning. Premiums are generally deductible, and you're assessing the cover as part of your broader personal budget.

- Inside super can reduce immediate out-of-pocket pressure. That can help if cash flow is tight, but it also changes how claims may be treated.

- Retirement impact matters. If premiums come from super, that's money not remaining invested for later.

- Policy flexibility can differ. The best structure depends on your income, tax position, super balance, and whether the policy needs to integrate with other cover.

Don't treat tax deductibility as the goal. Treat it as one factor in building a protection strategy that still works when a claim actually happens.

My view on the smart order of decisions

I'd make the decisions in this order.

First, work out the risk you're trying to cover. Second, decide the right amount and structure. Third, choose where to hold the policy. Too many people reverse that sequence and start with tax. That usually leads to a compromised result.

Tax matters. Cash flow matters more. Claim outcome matters most.

Who Needs Which Cover and When

The right answer changes with your life stage. That's why generic insurance advice usually misses the mark. A person with no dependants, no mortgage, and a strong income trajectory doesn't need the same structure as a family of five or a business owner carrying guarantees.

The bigger point is this. Income protection is not a niche product for worst-case thinkers. It achieved a 95.0% industry average acceptance rate in 2024, according to Australian income protection claims statistics. That should reassure anyone who worries these policies are all promise and no delivery.

The young professional

If you're in your late twenties or thirties, earning well, and you don't yet have children, income protection is often the first cover I'd prioritise.

Why? Because your biggest asset isn't what you own today. It's what you're likely to earn over the next few decades. If illness or injury disrupts that path, your savings habit, home deposit plan, and super contributions all take a hit at once.

Life insurance may still matter if you've got debt with a partner or family members who'd be affected financially by your death. But if we're ranking urgency, income protection usually wins first for this group.

The growing family

Once you've got kids, a mortgage, and two incomes propping up one household, the answer changes. You usually need both.

Life insurance protects the family if one parent dies. Income protection protects the household if one parent survives but can't work for an extended period. That second scenario gets overlooked all the time, even though it can be financially brutal because expenses stay in place while earnings drop.

A useful practical resource for households under stress is this guide on financial planning after job loss. It's not an insurance article, but it does a good job of showing how quickly debt pressure builds when income disappears.

If your family budget only works because both salaries keep arriving, income protection isn't optional. It's core infrastructure.

The high-income earner

Executives and professionals with strong incomes often assume they're safe because they've built a buffer. Sometimes they have. Often the buffer is smaller than it looks once school fees, mortgage commitments, private health costs, and lifestyle spending are added up.

This group needs disciplined thinking. Income protection becomes important because the household is frequently built around a high salary that would be hard to replace quickly. Life insurance also matters if there's debt, children, or estate planning objectives.

The trap here is complacency. Strong income can hide weak protection.

The business owner or self-employed operator

If you run a business, your exposure is different again. You may not have the same employer leave entitlements or built-in safety nets. If you stop working, business revenue may also suffer. In many cases, that makes income protection the sharper immediate need.

Life insurance still matters if your family depends on your earnings or if there are debts tied to you personally. But for the self-employed, the first issue is often survival during downtime. No work can quickly mean no income.

The pre-retiree

If retirement is on the horizon, the conversation gets more selective. People then need to review, not just renew.

You may have reduced debt, adult children, and a stronger asset base. That can lower the need for large life insurance amounts. Income protection may also become less critical as work dependency drops, but it doesn't disappear automatically if you're still relying on employment income to finish the last stage of your plan.

Use this checklist:

- Still carrying debt: Review both covers.

- Still earning actively: Don't assume income protection is irrelevant.

- Dependants are independent: Life cover may be reduced, not necessarily removed.

- Super and investments are stronger: Reassess whether insurance should fill a smaller gap.

This visual summary captures those shifts well.

Your Decision Checklist and Next Steps with Wealth Collective

You don't need a perfect spreadsheet to make a smart decision. You need a clear filter.

Start with these questions.

Ask yourself these five things

- Who depends on me financially: If your death would leave a partner, children, or even ageing parents under pressure, life insurance moves up the list fast.

- How long could I cover expenses without income: If the answer is “not long,” income protection deserves immediate attention.

- Do I have debt that assumes my income continues: Mortgages, personal loans, and business guarantees all increase the need for cover.

- Am I holding cover in the right place: Inside super and outside super can produce very different outcomes.

- Have I reviewed my cover since my life changed: Marriage, children, a promotion, a business launch, or approaching retirement should all trigger a review.

The decision framework I'd use

If you have dependants or major shared debt, life insurance is usually essential.

If you rely on your salary or business income to keep everything running, income protection is usually the first line of defence. In Australia, income protection is contractually capped at replacing up to 70% of pre-tax income, with a monthly ceiling, which is why Medibank's overview of life insurance and income protection highlights the importance of structuring cover properly rather than assuming it will replace every dollar.

That cap is exactly why good advice matters. You can't afford to be casual when a policy only replaces part of your earnings. The waiting period, benefit period, ownership structure, and tax treatment all need to work together.

Good insurance advice isn't about selling more cover. It's about making sure the cover you pay for is the cover that actually solves the problem.

Even though many people understand the difference between life insurance and income protection, they often get stuck, unsure how much is enough, what should sit inside super, what should sit outside, or whether their existing policies are outdated.

That's the point where personalized advice saves time, money, and future regret.

If you want clarity on what cover you actually need, and how to structure it without guesswork, book a complimentary initial call with Wealth Collective. It's a simple way to pressure-test your current setup, understand whether life insurance, income protection, or both belong in your plan, and take the next step with confidence.