Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You open your tax return, spot a charge you weren't expecting, and realise Medicare wasn't the whole story. The standard levy is familiar. The Medicare Levy Surcharge catches people off guard, especially professionals, business owners, and dual-income households whose income has crept into a higher bracket.

That's why Medicare levy private health insurance isn't just a health decision. It's a cash flow decision, a tax decision, and for many households, a wealth protection decision. Buy the right cover and you may avoid an extra tax. Buy the wrong cover, or let it lapse, and you can still end up paying the surcharge anyway.

Is Private Health Insurance a Tax Strategy

For high-income earners, the honest answer is yes.

Private hospital cover sits in the same category as other practical tax planning choices. You're not buying it only for medical access. You're deciding whether to pay an insurer for compliant cover or pay the ATO a surcharge because you chose not to. That's a financial trade-off, not a philosophical one.

Many individuals approach this backwards. They ask, “Do I want private health insurance?” The sharper question is, “What's the cheapest compliant way to avoid an unnecessary tax while still fitting my broader financial plan?” That shift matters.

If your income is high enough, the Medicare Levy Surcharge becomes a line item you can plan around. If you ignore it, you're leaving your tax position to chance. If you treat it strategically, you can compare the likely surcharge against the cost and quality of cover, then decide with intent.

Three rules make this simpler:

- Know if you're exposed: many people underestimate their income for surcharge purposes.

- Check whether your policy qualifies: plenty of people assume any private cover will do. It won't.

- Tie the decision to your full tax picture: debt reduction, super contributions, family structure, and timing all matter.

Practical rule: If a decision affects your tax bill, annual cash flow, and risk protection at the same time, it belongs in financial strategy.

That's also why this topic fits naturally beside broader tax planning conversations such as reducing taxable income in Australia. Medicare levy private health insurance is one of those areas where a “small” decision can have an outsized impact because the wrong setup can cost you twice. Once in premiums, again in tax.

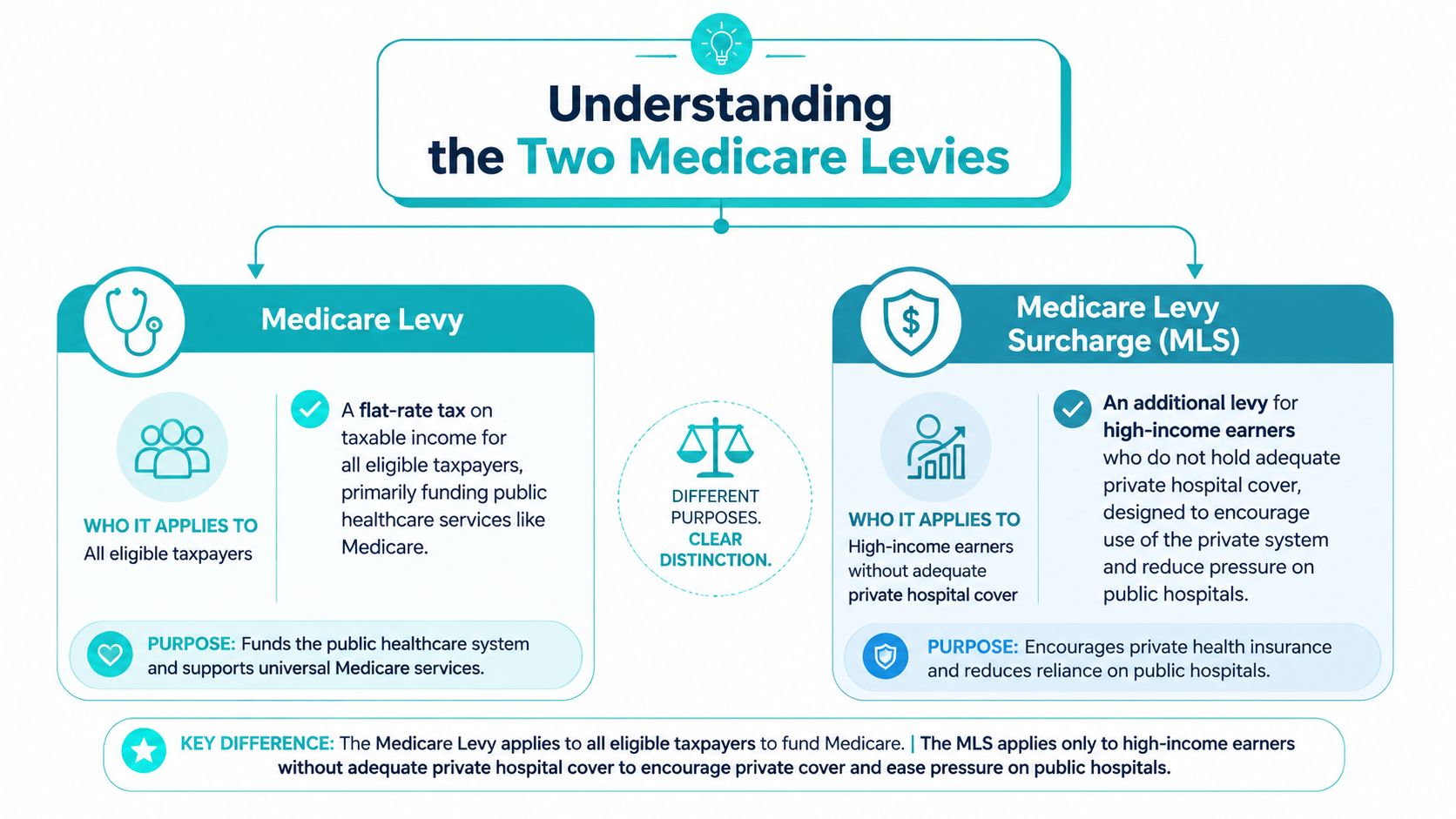

The Two Medicare Levies Explained

The confusion starts with the name. There are two different levies, and they don't do the same job.

The first is the Medicare Levy. Think of it as the general contribution most eligible taxpayers make toward the public health system.

The second is the Medicare Levy Surcharge, or MLS. That's the extra amount aimed at higher-income earners who don't hold appropriate private hospital cover. It exists to push more people into the private system and reduce pressure on public hospitals.

Medicare Levy versus MLS

A simple way to separate them:

- Medicare Levy: broad-based and tied to public healthcare funding.

- MLS: targeted and avoidable if you meet the rules for private hospital cover.

- Medicare Levy private health insurance link: this applies only to the surcharge side, not the standard levy.

That distinction matters because people often assume private health insurance wipes out “the Medicare levy.” It doesn't. It can help you avoid the surcharge if you're over the relevant income threshold and you hold qualifying cover.

Why the government uses the surcharge

The policy intent isn't subtle. The Medicare Levy Surcharge is designed to encourage higher-income earners to purchase private hospital insurance, and the same explanation notes that the top reason Australians take out private hospital cover is to avoid that extra tax. It also states that over 15.2 million Australians were covered by private health insurance as of June 2025, with avoiding the 1% to 1.5% surcharge presented as the primary motivation in that context, according to Australian Unity's explanation of the MLS.

The surcharge works like a nudge with teeth. If your income is high enough, doing nothing has a cost.

That's why the MLS shouldn't be treated as a minor tax technicality. It's a behavioural lever. The government uses it to make the “buy cover or pay extra tax” decision obvious for high-income earners.

What Is Qualifying Private Hospital Cover

Expensive mistakes can occur. Not all private health insurance counts for MLS purposes.

A lot of people have some form of cover and assume they're protected. They're not. The test is strict. It's effectively pass or fail.

Hospital cover is the key

To avoid the surcharge, you need approved hospital cover from a registered insurer. Extras cover on its own doesn't do the job. Ambulance-only benefits don't do the job either. If your policy doesn't cover hospital treatment in the right way, the ATO won't care that you were paying premiums.

That's why comparing policies only on price is risky. The cheapest option isn't automatically compliant. And a policy that looks “close enough” can still leave you exposed.

The excess limit is not optional

For the 2026 to 2027 financial year, qualifying private hospital cover must have a maximum excess of $750 for singles and $1,500 for couples or families, according to the Australian Government's privatehealth.gov.au guidance on the Medicare Levy Surcharge. Policies above those excess limits fail the approved cover test.

That means this isn't a matter of preference. It's a compliance rule.

Check your policy against these points:

- Hospital component present: extras-only cover won't exempt you.

- Excess within the limit: above $750 for singles or $1,500 for couples and families means it doesn't qualify.

- Registered insurer: the cover must be recognised.

- No gaps in cover: even a short lapse can create a problem.

Key takeaway: The wrong private health policy can be the worst of both worlds. You pay premiums and still owe the surcharge.

Why this catches people out

Insurers market policies as “basic”, “starter”, or “budget-friendly”, but those labels don't tell you whether the cover works for tax purposes. You need to check the hospital component and the excess, not just the monthly premium.

That's especially important if you're trying to keep costs down. A bargain policy that fails the excess test isn't a bargain. It's wasted money.

The practical approach is simple. Before renewal, before switching funds, and before tax time, confirm your policy passes the MLS test. If it doesn't, treat that as a financial problem first and a product problem second.

The 2026 Income Thresholds and Surcharge Rates

The surcharge doesn't apply because you feel well-paid. It applies because your income for MLS purposes lands above a defined threshold and you don't hold approved hospital cover.

That income figure can be broader than many people expect. It explicitly includes reportable fringe benefits and amounts on which family trust distribution tax is paid, according to Private Healthcare Australia's MLS guide.

2026 to 2027 Medicare Levy Surcharge thresholds and rates

| MLS Rate | Singles Income Threshold | Family Income Threshold |

|---|---|---|

| 0% | $0 to $105,000 | $0 to $210,000 |

| 1.00% | $105,001 to $123,000 | $210,001 to $246,000 |

| 1.25% | $123,001 to $164,000 | $246,001 to $328,000 |

| 1.50% | $164,001 and over | $328,001 and over |

These thresholds are where many tax estimates go wrong. People look only at salary. The surcharge test doesn't.

What to check before you assume you're safe

Use this checklist before you conclude you're under the line:

- Taxable income: start here, but don't stop here.

- Reportable fringe benefits: salary packaging and employer-provided benefits can matter.

- Trust-related amounts: if family trust structures are part of your affairs, the MLS calculation may reach further than expected.

- Family income: couples and families need to assess the household position, not just one person's income.

For families, the threshold also increases by $1,500 for each dependent child after the first, as noted in the same private health guidance discussed earlier.

If you're close to a threshold, “roughly right” isn't good enough. MLS is one of those taxes where small miscalculations create annoying surprises.

Why this belongs in tax planning

The surcharge is payable through your tax return, which means many people don't feel it until after the financial year has already ended. That delay is why it catches people. By the time you see it, the fix is too late.

That's also why broader tax awareness matters. Even though it deals with a UK rule, Stewart Accounting tax insights are a useful reminder that income thresholds often create hidden tax traps once earnings cross a line. The Australian version is the same in spirit. You need to plan before the threshold bites, not complain after.

If you want this assessed properly, it belongs inside a wider taxation and tax planning approach, not as a rushed decision in June.

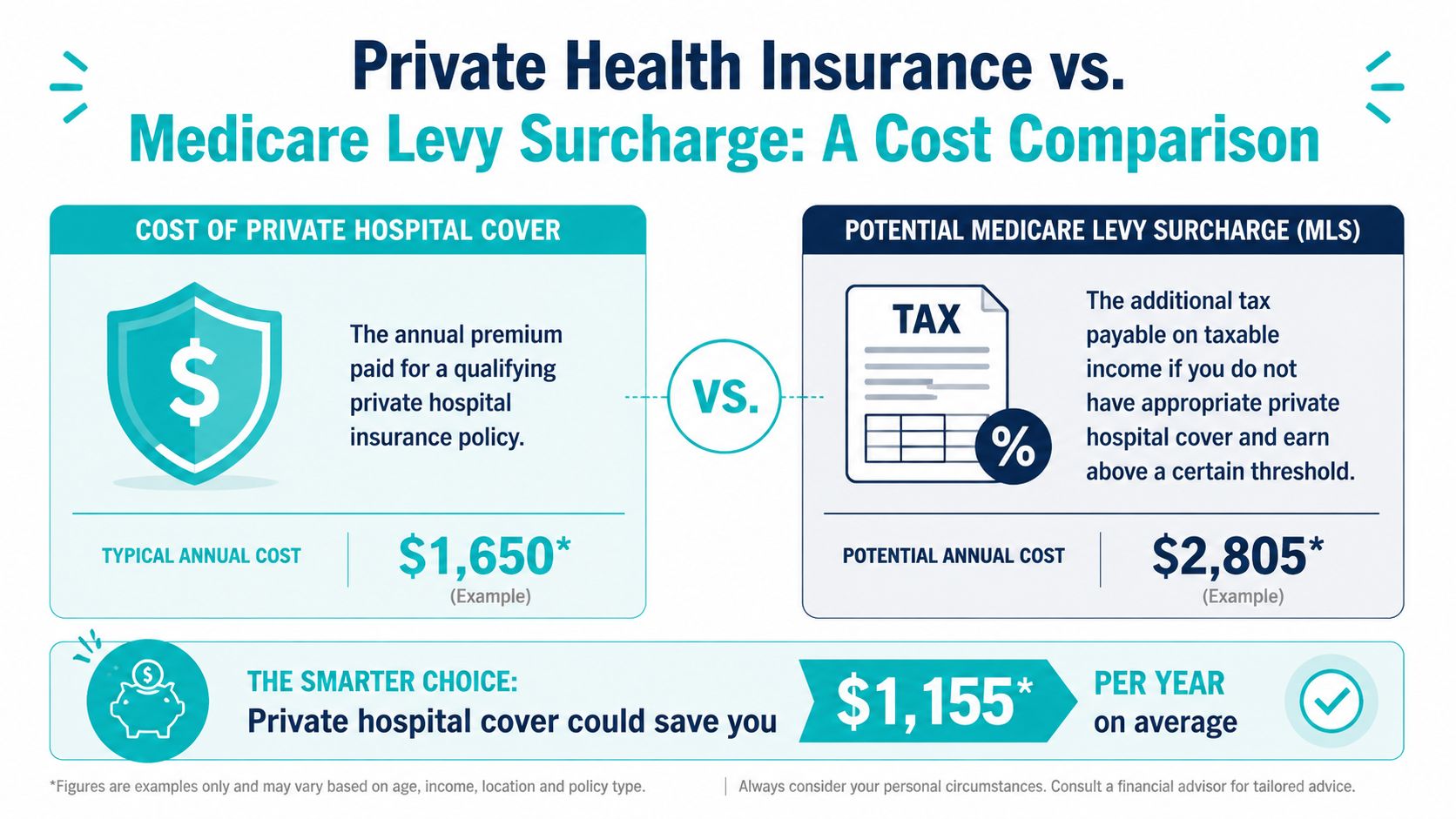

Doing the Maths Is Private Health Insurance Worth It

This is the only question that really matters. Is qualifying private hospital cover cheaper, or more useful, than paying the surcharge?

For many people, the answer is straightforward. If the surcharge would be material and the policy cost is reasonable, private cover works as a tax management tool. That isn't gaming the system. It's using the rules exactly as they were designed.

Start with the break-even question

The formula is simple in principle:

- Estimate your income for MLS purposes.

- Identify your likely MLS rate.

- Compare the likely surcharge with the annual cost of a qualifying hospital policy.

- Then ask a second question. If costs are close, which option gives you more practical value?

You don't need a complex spreadsheet to understand the logic. You do need accurate inputs.

Three common scenarios

A young professional in Perth crosses the singles threshold and has no hospital cover. The surcharge becomes a real tax cost, payable through the tax return. That person should compare the annual cost of compliant single hospital cover against the likely MLS bill and choose the better number, while also considering whether having hospital access fits their risk profile.

A dual-income family in Dunsborough often makes this decision at the household level. Family income determines the bracket, and children can affect the threshold settings. In practice, this means one partner can assume they're fine based on their own income while the family as a whole is exposed. The right comparison is family surcharge versus family cover, not one person's premium versus one person's salary.

A pre-retiree couple may have an even more layered calculation. They might want to avoid the surcharge, keep flexibility around healthcare access, and coordinate the decision with super and drawdown strategy. For them, the pure tax comparison is only the first screen.

Don't buy junk just because it's cheaper

There's a reason policymakers have paid attention to cheap policies used mainly to avoid the surcharge. Historical analysis cited unpublished ABS data from the 2004/05 National Health Survey showing that low-cost policies bought to bypass the MLS created tax losses of between $110 million and $250 million in that financial year, according to The Australia Institute paper on MLS revenue loss.

That history tells you something useful. People have long treated Medicare levy private health insurance as a financial arbitrage decision. The mistake is stopping there.

Cheap cover that qualifies may solve the tax issue. It may still be poor value if the policy gives you very little when you actually need treatment.

A practical decision filter

Use this sequence:

- First test: does the policy qualify for MLS exemption?

- Second test: is the premium likely lower than, or close to, the surcharge you'd otherwise pay?

- Third test: if you had a hospital event, would this policy still feel like a sensible purchase?

If the answer is yes to all three, the decision is usually easy. If the policy qualifies but is terrible value, it may still be worth upgrading rather than buying the absolute cheapest option.

That's the maths. Not just tax saved. Total value received.

Strategic Decisions for Your Stage of Life

The right answer changes with your stage of life. The rule book stays the same. Your priorities don't.

Young professionals

If you're early in your career and your income has started climbing, don't treat this as a once-a-year admin task. It's one of the first signs that your finances need a proper structure. Hospital cover, cash flow, debt reduction, and salary packaging all start interacting.

A lot of younger earners buy the cheapest cover that passes the surcharge test and move on. That can be sensible, but only if the policy is the right fit and the rest of your tax settings are clean. If they aren't, a short-term saving can become a long-term mess.

Families

For families, this choice becomes a household planning issue. Income thresholds apply at the family level, and the threshold rises by $1,500 per dependent child after the first, as noted in the GMHBA discussion of MLS family scenarios and related cover questions in their Medicare Levy Surcharge guide.

That's why family cover decisions shouldn't be made in isolation.

- Cash flow matters: premiums need to fit the monthly budget.

- Structure matters: the policy has to match the family's likely healthcare use.

- Tax matters: one bad assumption about income or cover can turn into an avoidable surcharge.

Pre-retirees and retirees

Nuance matters most. The same GMHBA guidance highlights a common issue for dual-income retirees. Basic Hospital Cover may avoid the 1.00% to 1.50% MLS, but if the excess is too high it may not satisfy the approved cover requirements relevant to some broader planning considerations, which can create a “double tax” problem in the way many retirees describe it.

The closer you are to retirement, the less useful isolated product decisions become. You need coordination between tax, super, insurance, and drawdown strategy.

If retirement planning is on your radar, this is also where trade-offs around contributions and cash flow need proper modelling. Decisions such as whether salary sacrifice is worth it can change your broader planning position, even if they don't replace the need to check MLS exposure directly.

The mistake at this stage is assuming “any cover” solves the issue. It doesn't. The policy has to be compliant, and it has to fit the rest of your financial life.

Take Control of Your Tax Your Next Step

By now, the pattern should be clear. Medicare levy private health insurance isn't a side issue. It's one of those practical decisions where tax, insurance, and wealth strategy intersect.

If your income puts you in the firing line, you have three choices. Ignore it and risk an avoidable tax bill. Buy cover blindly and hope it qualifies. Or make the decision properly, with your income, family setup, retirement timing, and broader strategy all considered together.

The wrong setup costs money in obvious and non-obvious ways. You can overpay in premiums. You can still get hit with the surcharge. You can choose a policy that technically qualifies but adds very little value. None of those outcomes are hard to avoid once someone reviews the full picture.

Your next move should be simple. Get clarity before tax time forces the issue. A short conversation can tell you whether private hospital cover is the right tax strategy for you, whether your current policy qualifies, and how this decision fits with your broader plan for debt reduction, super, investing, and retirement.

Book a complimentary introductory call with Wealth Collective if you want a clear answer on whether your private health insurance is helping your tax position or costing you more than it should.