Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Most property investors start with the same assumption. You buy well, hold on, wear the shortfall, and hope future growth makes the pain worthwhile.

That approach can work. But it isn’t the only way to invest, and in a higher-rate environment, it often isn’t the most comfortable way to build wealth.

A lot of motivated WA investors want something more practical. They want a property that helps carry itself. They want income now, not just a story about what the property might be worth years from today. They want fewer surprises when rates move, and more control over how quickly they can reduce debt or reinvest.

That’s where positive geared properties come in.

For the right investor, a positive geared property can turn an investment from a monthly drain into an income-producing asset. It can create breathing room in your household budget, support retirement planning, and make it easier to hold property through uncertain markets. It also suits circumstances many Western Australian investors are facing, especially those looking beyond the usual capital-city mindset and paying closer attention to Perth, regional hubs, and lifestyle markets such as Dunsborough.

Rethinking Property Investment for Today

For years, many Australians were taught to see property as a long game built on sacrifice. Buy in a growth area. Tip in your own cash every month. Claim the tax deduction. Wait.

That still appeals to some investors, but plenty of smart buyers now want a property that contributes to their financial life sooner. They’re less interested in carrying an ongoing loss and more interested in steady cash flow, lower stress, and better flexibility.

That shift matters most when money feels tighter. If your investment needs constant support from your salary, it competes with other goals. It can slow debt reduction, limit your ability to save, and reduce your confidence to buy again later. A property that pays its way changes that dynamic.

Why cash flow matters more than many investors realise

Cash flow gives you options. It can help you:

- Reduce pressure on your salary: You’re not topping up the property from your own pocket each month.

- Build resilience: If rates, repairs, or life circumstances change, you have more room to move.

- Reinvest strategically: Surplus income can support loan reduction, buffers, or future investing.

- Stay invested longer: Holding a property is easier when it isn’t draining your household finances.

A good property strategy shouldn’t just look smart on paper. It should be manageable in real life.

This is one reason positive gearing has become more relevant. In a market where finance costs matter, investors are paying closer attention to assets that can stand on their own.

For WA investors, that often means looking more carefully at local demand, rental conditions, and yields, rather than following broad national headlines. Perth and regional Western Australia don’t always behave like Sydney or Melbourne. That can create opportunities if you know what to look for.

What Exactly Is a Positive Geared Property

A positive geared property is one where the rent you collect is higher than the total cost of owning the property. If the money coming in is greater than the money going out, the property produces a surplus.

That’s the simplest definition. In practice, it is useful to consider it a small business asset. If you owned a vending machine, you’d want it to bring in more than it costs to stock, service, and maintain. A rental property works the same way.

The basic formula

The calculation is straightforward:

Rental income minus ownership costs = cash flow

If the result is above zero, the property is positively geared.

What counts as income and costs

The income side is quickly understood. It’s usually just the rent.

The cost side is where confusion starts. Investors often underestimate how many expenses sit behind a property, especially if they only focus on the mortgage.

Common ownership costs include:

- Mortgage repayments: These are often the largest ongoing expense.

- Council rates: A regular cost that must be factored in from the start.

- Insurance: Building and landlord cover can affect your cash flow materially.

- Property management fees: If an agent manages the property, this needs to be included.

- Maintenance and repairs: Even well-kept properties need ongoing attention.

- Other property costs: Depending on the asset, there may be additional recurring expenses.

A property is only positive if the rent exceeds the full ownership picture, not just one line item.

A real yield example

A commonly used benchmark example shows how yield drives the result. A $300,000 property renting for $410 per week, or $21,320 annually, has a gross rental yield of 7.10%, calculated as annual rent divided by purchase price, multiplied by 100. That sits above the general 6 to 7% threshold often needed for positive cash flow in the current market, as outlined in B.Invested’s explanation of positively geared property.

That example matters because it gives you a practical filter. Many investors hear the term “positive gearing” and assume it’s rare or mysterious. It isn’t. But it does usually require a property with stronger yield characteristics than the average metro growth asset.

Practical rule: If the yield is too low, the property has to rely more heavily on your salary to survive.

Gross yield is a starting point, not the finish line

Gross yield helps you screen properties quickly, but it doesn’t tell you everything. A property can look strong at first glance and still disappoint once you account for full costs.

That’s why experienced investors treat gross yield as the first pass, then test the actual cash flow position with a more complete budget. The point isn’t to chase the highest yield possible. It’s to find a property where income, finance, and risk are in balance.

For many WA investors, that often means looking at suburbs and towns where affordability supports better rent-to-price ratios than you’d typically find in premium inner-city markets.

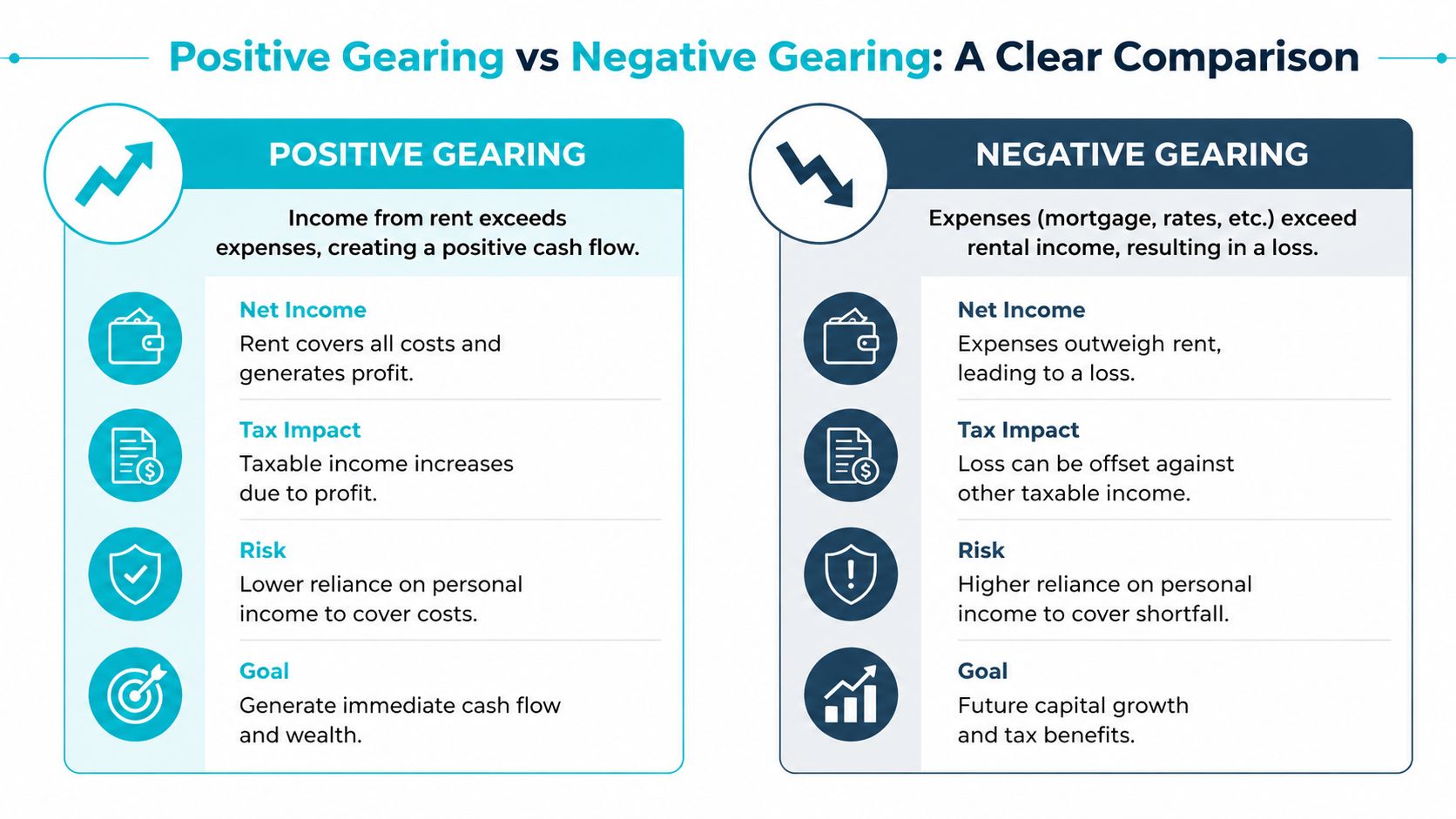

Positive Gearing vs Negative Gearing A Clear Comparison

Most Australian investors have heard more about negative gearing than positive gearing. The tax conversation tends to dominate. But tax is only one part of the decision.

The bigger question is how the property behaves in your life. Does it require support, or does it provide support?

The core difference

With positive gearing, rent exceeds costs and the property generates surplus income.

With negative gearing, costs exceed rent and you cover the gap from other income sources, often with the expectation that tax deductions and capital growth will justify the shortfall.

In the post-2022 rate-hike environment, positive gearing gained more attention as a risk-management strategy because a self-funding portfolio can reduce pressure in softer markets. Guidance discussed in InvestorKit’s positive cash flow property guide also notes that a 7%+ gross yield is often used as a safety buffer so pre-tax cash flow can cover costs.

Positive Gearing vs. Negative Gearing at a Glance

| Attribute | Positive Gearing | Negative Gearing |

|---|---|---|

| Cash flow | Rent is higher than ownership costs | Ownership costs are higher than rent |

| Tax treatment | Net rental profit is generally assessable income | Net rental loss may help offset other taxable income |

| Reliance on salary | Lower | Higher |

| Portfolio pressure | Often easier to hold through rate or vacancy stress | More exposed if personal income tightens |

| Primary goal | Immediate income and sustainability | Capital growth and tax-effect outcomes |

| Ideal investor mindset | Wants income, buffers, and control | Comfortable funding losses for longer-term upside |

Cash flow and borrowing capacity

Cash flow shapes what you can comfortably hold. If a property runs at a loss, lenders and borrowers both know that someone has to fund that gap. Usually, that’s your salary or business income.

That doesn’t automatically make negative gearing bad. It just makes it more demanding. If rates rise, vacancies drag out, or household expenses increase, the shortfall can become more noticeable very quickly.

Positive gearing changes that equation. A property producing surplus income can help preserve flexibility and, in some cases, support future borrowing rather than restrict it.

Tax is not the strategy

Negative gearing often gets framed as a tax win. The problem is that a deduction doesn’t erase the loss. You’re still spending more than you earn on the property.

Positive gearing has the opposite issue. Because the property makes money, some of that income may be taxable. Many investors see that as a drawback, but it’s usually the better problem to have. Profit with tax is still profit.

If you want a broader primer on the mechanics, this guide on negative gearing for investors is a useful background read. For a localised explanation of how the concept works in Australia, see this overview of negative gearing in Australia.

Risk and investor goals

The right approach depends on what you’re trying to achieve.

Choose positive gearing if you care most about:

- Immediate cash flow

- Holding costs that feel manageable

- Building buffers and reducing debt

- Lower dependence on future price growth

Choose negative gearing if you’re comfortable with:

- Funding a shortfall from income

- Waiting longer for the investment to improve

- Higher exposure to interest-rate and servicing risk

- A strategy more dependent on future capital growth

Some investors don’t need the biggest tax deduction. They need the property to stop asking them for money.

That distinction matters. Many investors don’t fail because they chose the wrong suburb. They fail because they chose a structure they couldn’t comfortably hold.

Is Positive Gearing the Right Strategy for You

A positive geared property isn’t automatically the best choice for every investor. The right answer depends on your stage of life, your tolerance for risk, and what job you need the property to do.

For some people, the appeal is stability. For others, it’s speed. For others again, it’s the relief of owning an investment that doesn’t create a monthly drain.

Pre-retirees who want income, not just equity

If retirement is getting closer, cash flow usually starts to matter more than theory.

A property with a surplus can help create a non-super income stream while you’re still working, and later support lifestyle costs once work slows down. That can be especially valuable for people who don’t want to rely on selling assets at the wrong time.

Many pre-retirees also prefer the emotional comfort of an investment that contributes to the household rather than competes with it. They’ve often moved past the stage where aggressive speculation feels exciting. They want durable, understandable income.

Young professionals and dual-income households

This group often has strong earning power but limited spare time. They may be capable of funding a negatively geared property, but that doesn’t mean they want to.

A positive geared strategy can suit professionals who want their investments to build wealth without continuously eating into lifestyle, travel plans, school fees, or mortgage reduction goals on their home. It can also create a cleaner runway for a second purchase because the first property places less strain on overall cash flow.

Some long-term investors use a blended mindset. They may start with a property that isn’t strongly positive, then watch it improve over time. According to NAB’s discussion of gearing, rental growth in Australia has averaged 4 to 7% annually, and that growth can turn an initially negatively geared property into a positively geared one over 5 to 10 years as rents rise and the loan principal stays stable or declines, as noted in NAB’s guide to property gearing.

Small business owners who want diversification

Business owners understand cash flow better than most. They know revenue can be uneven, and they usually value income streams that aren’t tied to their own labour.

A positive geared investment property can play a useful role here. It can diversify household wealth away from the business and provide income that doesn’t depend on the next client, contract, or trading cycle.

That doesn’t mean every business owner should chase high-yield property. It means they should be especially thoughtful about whether an investment adds stability or adds another cash demand.

A few signs it may suit you

Positive gearing often fits well if you relate to several of these points:

- You want a property that can largely support itself

- You value income and flexibility over a pure growth bet

- You’re conscious of rate risk and borrowing capacity

- You want to reduce the need to top up losses from salary

- You prefer slower, steadier compounding to a more aggressive approach

The best property strategy is the one you can hold with confidence through ordinary life, not just ideal conditions.

The reverse is also true. If your main priority is maximum long-term growth and you’re comfortable funding shortfalls for years, another strategy may suit you better. Positive gearing is not a badge of sophistication. It’s a tool. The essential question is whether it matches your financial life.

How to Find and Analyse Properties in Western Australia

Western Australia deserves its own lens. National property commentary often smooths over local differences, yet WA investors know that Perth, Bunbury, Mandurah, Geraldton, and Dunsborough can behave very differently from east-coast markets and from each other.

That matters because positive geared properties are usually found through local economics, not broad slogans.

Start with WA conditions, not national assumptions

WA has rental dynamics that can support stronger cash flow, but only if you buy selectively. A key data point is that Perth’s metro vacancy rate reached 0.4% in Q1 2025, with annual rental growth of 12.7%. At the same time, some WA outer suburbs still produced only 4.2% gross yield, while high-employment regional hubs such as Bunbury and areas linked to the mining boom could deliver yields above 6%, according to this WA-focused discussion of positively geared property.

The lesson is simple. Tight vacancy alone doesn’t guarantee a positive geared result. You still need the purchase price, rent level, and running costs to stack up.

Where WA investors often look

Positive cash flow opportunities in WA often sit in places with a practical mix of affordability, tenant demand, and economic activity.

Common search areas include:

- Bunbury and nearby regional hubs: These can offer stronger yield profiles when employment demand is healthy.

- Mandurah and selected outer-metro markets: They may suit investors who want a balance between accessibility and rental return.

- Perth employment corridors: Not every suburb works, but job access matters.

- Lifestyle-driven regional areas including around Dunsborough: These markets need closer analysis because appeal alone doesn’t guarantee the right cash flow outcome.

If you’re working through the buying process from scratch, this guide on how to buy an investment property is a useful companion.

The three numbers to check first

You don’t need a complicated spreadsheet to assess a property at the shortlist stage. You do need discipline.

Gross yield

This is the first filter.

Gross yield = annual rent ÷ purchase price × 100

Use it to compare opportunities quickly. If the gross yield is too low, the chance of positive cash flow usually falls away unless the property has unusually low costs or low debt attached to it.

Net yield

Net yield goes further by accounting for recurring property expenses. It gives a more realistic picture of the income left after ongoing costs.

Rather than relying on a selling agent’s summary, build your own estimate. Include rates, insurance, management, and a maintenance allowance. If the property is part of a complex, account for ongoing strata-type costs as well.

Cash-on-cash return

This tells you how hard your own capital is working.

Some investors focus only on yield and forget the structure of the purchase. Deposit size, loan terms, and acquisition costs all affect the return on the cash you put in. A property can look attractive on yield and still underperform for your personal situation if the funding structure is poor.

A practical due diligence checklist

Run through these questions before you get emotionally attached to any deal:

- Tenant demand: Is there a clear reason people want to live there, such as employment access, services, lifestyle, or transport?

- Vacancy risk: Tight vacancy helps, but look at local conditions, not just the broader region.

- Employment base: Areas tied to diverse or durable jobs tend to hold up better.

- Property type: Ask whether the dwelling suits the local tenant pool.

- Rent realism: Use current market rent, not an optimistic estimate.

- Maintenance exposure: Older properties can still work, but you need to budget properly.

- Exit appeal: A property should be rentable now and saleable later.

Buy for cash flow with the same care you’d use if the property had to support itself from day one. Because that’s exactly what you want it to do.

Common mistakes WA investors make

One is chasing yield without checking quality. A very high advertised rent can distract you from weak tenant demand, poor resale appeal, or heavy maintenance.

Another is assuming any low-vacancy market will produce positive gearing. It won’t. If the entry price is too high relative to rent, the numbers still won’t work.

A third is buying based on familiarity. Plenty of investors stick too close to where they live, even when better cash flow opportunities sit elsewhere in the state. Good investing starts with evidence, not postcode loyalty.

Navigating Tax and Finance Successfully

Positive cash flow is only useful if you understand how tax and lending interact with it. Many investors often oversimplify these aspects.

A property can produce surplus income and still deliver a better after-tax result than expected once you account for allowable deductions. On the finance side, the structure of the debt often matters as much as the property itself.

How tax works on a positively geared property

If your property earns more than it costs to hold, that net rental income is generally part of your assessable income. That means tax isn’t something to ignore just because the property feels profitable month to month.

But taxable income and cash flow aren’t always identical. Some deductions affect your tax position even though they don’t involve a fresh cash payment in that year.

Examples of deductible property-related items can include:

- Interest and finance-related costs

- Property management fees

- Council rates and insurance

- Repairs and other eligible expenses

- Depreciation, where applicable

If you want a practical overview of the types of deductions investors commonly review, this article on how to claim real estate investment deductions is a handy checklist-style resource.

Why depreciation matters

Depreciation is one of the most misunderstood parts of property investing. Many investors think only in terms of rent received and bills paid. Tax law doesn’t stop there.

A property may produce positive cash flow before tax, but depreciation can reduce the amount of profit that is ultimately taxed. That can improve the after-tax outcome without changing the rent collected.

This doesn’t mean every property will have the same depreciation profile. The age of the building, fixtures, and quality of records all matter. That’s why investors usually need coordinated advice from both a property-focused accountant and a lending adviser who understands the broader strategy.

For a broader look at how tax settings can affect rental property outcomes, see this overview of tax benefits of rental property.

Finance structure can make or break the strategy

The same property can feel very different under two different loan structures.

Lenders assess serviceability, deposits, buffers, and your overall financial position. A positively geared property can help your file look stronger than a heavily loss-making one, but that doesn’t remove the need for careful debt structuring. Loan type, repayment choice, and the amount of equity or cash you contribute all influence the final outcome.

A few finance principles matter:

- Deposit strength matters: More equity or cash contribution can improve the cash flow position.

- Buffer planning matters: Positive today doesn’t guarantee positive after a rate change or repair bill.

- Portfolio sequencing matters: Your first investment should support, not sabotage, future borrowing.

The right tax result is rarely an accident. The right finance result isn’t either.

Build Your Cash Flow Strategy with Wealth Collective

Positive geared properties appeal to investors for a simple reason. They can offer income, control, and a more resilient way to build wealth.

For some people, that means creating a portfolio that doesn’t rely on constant salary top-ups. For others, it means shaping retirement income earlier, reducing debt faster, or building enough surplus cash flow to invest again with confidence. The strategy is practical, but it still needs careful planning around property selection, lending, tax, super, and risk management.

When you’re ready to turn theory into a personalised plan, Wealth Collective can help map the strategy to your stage of life. That may mean a Guided Growth approach if you’re building wealth and want your investments to work harder without derailing cash flow. It may mean a Retirement Roadmap if you’re focused on income, debt reduction, and a smoother transition into retirement.

A short initial conversation can clarify whether positive gearing fits your goals, your borrowing position, and the WA market opportunities you should be watching.

Frequently Asked Questions

Can I buy a positive geared property through super

Possibly, but the structure matters. Super-based property investing has different rules, lending settings, and liquidity considerations from investing in your own name. The main issue isn’t whether positive cash flow is attractive. It’s whether the purchase fits the fund’s strategy, cash needs, and compliance obligations.

What happens if interest rates rise after I buy

A positive geared property can become less positive, neutral, or even negative if finance costs rise enough. That’s why investors should leave room in the numbers rather than buying on a razor-thin surplus. A sensible buffer matters more than a perfect spreadsheet.

Should I use surplus cash to pay down debt or buy again

That depends on your broader strategy. Some investors prioritise reducing debt for security and cleaner future cash flow. Others reinvest sooner to grow the portfolio. The right answer usually comes back to your age, income stability, risk tolerance, and borrowing capacity.

Are positive geared properties always in regional areas

Not always, but they’re often easier to find where prices are more affordable relative to rent. That’s one reason regional WA and selected outer-metro locations attract attention. The better question is whether the area has durable tenant demand and the right purchase-price-to-rent balance.

Is positive gearing better than negative gearing

Not universally. It’s better for some goals and less suitable for others. If you want income, lower portfolio pressure, and a more self-funding asset, positive gearing often makes sense. If your goal is stronger capital growth and you can comfortably carry shortfalls, another approach may suit you.

If you want help turning these ideas into a practical plan, speak with Wealth Collective. A complimentary introductory call can help you assess whether positive geared properties suit your goals, your borrowing capacity, and your next step in Perth, Dunsborough, or elsewhere in Australia.