Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You log into your super account, see that insurance premiums are being deducted, and assume the job is done. That’s a common position. It also leaves a lot of people with a false sense of security.

A rest income protection policy can be valuable. For many members, it gives them a built-in starting point without needing to sit through medical underwriting or apply for a separate policy from scratch. But default cover inside super is a foundation, not a finished protection plan.

The part that catches people out is simple. They know they “have insurance”, but they don’t know how much it would pay, when it would start, how long it would last, or what could stop a claim. Those details matter far more than the label on the account.

Your Superannuation Safety Net Is It Strong Enough

A lot of Australians treat insurance inside super like the spare tyre in the boot. They’re glad it’s there, but they don’t inspect it until they’re stranded on the side of the road.

That’s usually how the conversation starts. Someone has a mortgage, kids, rent, or just regular bills that won’t stop if they get sick or injured. They’ve seen “income protection” on their super statement, so they assume they’ve covered the risk. Then they realise they’ve never checked the rules.

Why default cover feels safer than it often is

Default insurance can be useful because it removes friction. If cover starts automatically, more people have at least some protection. That matters, especially for workers who might never buy insurance privately unless something prompts them to act.

But “some protection” and “enough protection” are not the same thing.

If your income pays for the household, the car, school costs, groceries and loan repayments, then the pertinent question isn’t whether you have cover. It’s whether the cover matches your life. A policy can exist and still leave a serious gap between what comes in and what still has to go out each month.

The protection gap most people miss

The gap usually shows up in one of these ways:

- The benefit is lower than expected: a member assumes the policy will replace their whole wage, but it won’t.

- The timing is misunderstood: the member expects payments straight away, but there’s a waiting period.

- The rules change with work status: someone changes jobs, stops work, or becomes inactive and doesn’t realise that can affect eligibility.

- The family relies on more income than the policy was designed to replace: default cover may help, but not enough to preserve the household’s standard of living.

Insurance inside super should be treated like a first draft. Useful, but not ready to sign off without review.

That’s particularly relevant if your finances have become more complex. A younger worker with low expenses may view default cover very differently from a dual-income family or a pre-retiree trying to protect the final years before retirement.

The practical value of a rest income protection policy isn’t just in having it. The value comes from knowing exactly where it helps, where it falls short, and what needs to be checked before life puts it to the test.

Unpacking Your Rest Income Protection Policy

A Rest income protection policy works like a temporary replacement for part of your wage when illness or injury stops you from working. The purpose is simple. Keep enough money coming in to help you cover regular bills while you recover.

That sounds straightforward until you look at the fine print that shapes what gets paid.

What the policy is designed to pay

Rest explains that its income protection can provide up to 77% of pre-disability income, plus an extra 12% super contribution component. The same claims information also shows that default cover can change by age, and gives an example of a young retail worker who received more than $23,000 after back pain stopped them working, according to Rest’s income protection claims information.

The first part of that benefit is aimed at day-to-day cash flow. Rent or mortgage payments, groceries, utilities, transport, and other living costs do not pause because your body does.

The second part is easy to miss. If you are off work for months, your income usually drops and your super contributions can stop as well. That 12% component is meant to reduce the long-term hit to your retirement balance. It helps, but it does not automatically mean your retirement savings stay fully on track.

Why that can still leave a gap

A common misunderstanding is that a percentage-based benefit will neatly match a household budget. It often does not.

If your take-home pay has been covering debt repayments, school fees, childcare, rising rent, or a mortgage assessed on two incomes, a partial replacement can feel a lot smaller than expected. The numbers may look acceptable on paper and still be tight in real life.

This is the point many members discover the default-cover trap. The policy can be useful and still fall short of what your household needs each month. That risk gets sharper if your employment changes, your expenses rise, or you are relying on cover you have never checked against your current income.

Age-based cover is not the same as needs-based cover

Default cover is built around broad member profiles, not your personal budget.

A younger member may have lower cover because the fund assumes income and commitments are lower early in working life. Later on, the insured amount may rise. But life rarely follows a neat formula. A 27-year-old with rent, a car loan, and a new baby can be under more pressure than a 40-year-old with low debt and strong savings.

That is why I tell clients to treat default cover like the spare tyre in a car. It may get you off the side of the road. It is not the same as checking whether all four tyres are right for the trip you are taking.

If you want broader context on how cover inside super works, our guide to superannuation income protection explains where these policies fit and where the limits usually show up.

The practical question to ask

The useful question is not whether Rest cover exists in your account. The useful question is whether the benefit would carry your household through a real interruption to income without forcing major financial damage.

That includes a less obvious risk. If you lost your job rather than your health, income protection would usually not respond. That unemployment trap catches people who assume any interruption to pay will trigger cover. It will not.

For broader context on how disability protection fits within a wider risk plan, that resource is a helpful reference.

A policy inside super can be a solid starting point. It still needs to be tested against your actual income, debts, work pattern, and family responsibilities before you rely on it.

How to Qualify and Make a Claim with Rest

You stop work because of illness or injury. The payslip stops. Bills do not. That is the moment default cover stops being a line in your super account and turns into a real test of whether the policy will support you.

Rest’s income protection settings can include a waiting period before payments start, and cover may continue when you change jobs if your new employer keeps paying into the same Rest account, as noted in Finder’s overview of Rest income protection. Those details matter because a claim is never just about being unwell. It is also about timing, work status, account status, and whether you can financially hold on long enough for the policy to respond.

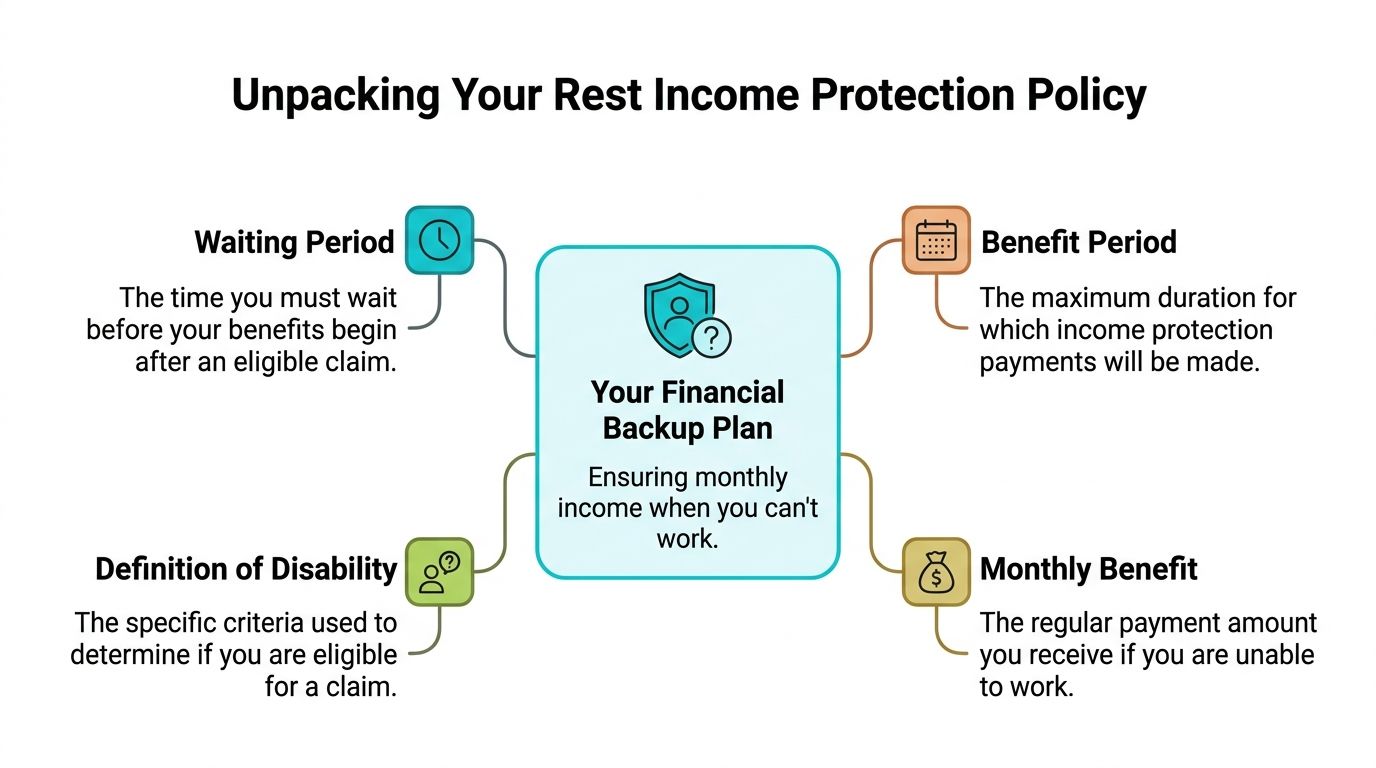

Start with the waiting period

The waiting period is the gap between the day you become unable to work and the day benefits may begin on an approved claim.

Waiting period

The period you must serve after illness or injury stops you from working, before the insurer starts paying an approved claim.

A lot of members confuse this with sick leave. It works more like an excess on car insurance. You carry the first part yourself, then the insurer may step in if the claim is accepted.

That has real consequences. If your waiting period is 60 or 90 days, you need another way to cover rent or mortgage repayments, groceries, utilities, and debt commitments during that time. If you want a clearer picture of the gaps, our guide to what income protection does not cover explains the limits people often miss.

Benefit amount matters. Benefit duration matters too.

Many members focus on the monthly payment and stop there. That is only half the picture.

Benefit period

The maximum period the insurer may continue paying monthly benefits while you remain eligible under the policy.

A policy with a modest monthly benefit for a longer period can produce a better outcome than a higher payment that stops sooner. Recovery does not always run on a neat schedule. Some health events interrupt income for months, not weeks. If the policy runs out before your earning capacity returns, the financial pressure lands back on you.

What usually decides whether a claim is accepted

At claim time, the insurer is not asking whether you have premiums coming out of super. It is asking whether you meet the policy terms on the date that matters.

The main checkpoints are usually these:

You were covered when the illness or injury stopped you from working.

If cover had reduced, ceased, or changed before that point, the claim can be affected.You meet the policy’s disability definition.

Medical evidence needs to support that your condition prevents you from working under the policy rules, not just that you are unwell.Your work and account details line up with the policy conditions.

Employment pattern, contribution history, and account activity can all become relevant.You provide the documents the insurer asks for.

Medical certificates, employer statements, and proof of earnings often form the backbone of the claim.You remain eligible while benefits are being assessed and paid.

Some claims require ongoing updates, not just one application form at the start.

Many individuals often overlook a key point. They assume the only question is medical. In practice, claims are often part medical, part administrative, and part contractual.

A practical way to approach the claim

If I were guiding a new client through a Rest claim, I would keep the process plain and methodical.

- Notify early. If illness or injury may keep you off work beyond your waiting period, start the claim discussion early rather than after savings have already been drained.

- Collect records upfront. Have medical reports, payslips, tax records if relevant, and employer details ready. Missing documents often slow claims down.

- Check your exact policy settings. Confirm the waiting period, benefit period, and any changes you previously made inside the fund.

- Track the process. Keep copies of forms, note call dates, and follow up if the file goes quiet.

That last point matters more than people expect. Claim delays often start with incomplete paperwork, unclear medical wording, or assumptions that the insurer will chase every missing detail for you.

Job changes can create confusion

A change of employer does not always mean a change of policy. If contributions keep going into Rest, cover may continue without a fresh application. That convenience helps, but it should not give you false comfort.

A policy can remain in place while your real risk position changes underneath it. Casual hours, unpaid leave, a break between jobs, or reduced income can all alter how suitable the cover is and how a future claim may be assessed. The policy may still exist. Your protection gap may still be growing.

A policy that follows you from one job to the next can be useful. It still needs to be checked against your current work pattern, cash reserves, and household commitments.

That is the adviser’s view on default cover in super. The question is never only, “Do I still have insurance?” The better question is, “If I had to claim next month, would this policy work the way I assume it will?”

Common Traps in Your Rest Super Insurance

The biggest mistake people make with super insurance is assuming that because premiums are deducted, cover must be working exactly as expected.

That assumption can be expensive.

A major concern raised about Rest was the risk of members holding “illusory” policies during unemployment or account inactivity of 13+ months, with a 2018 class action and criticism from APRA over premiums being deducted from unemployed members who were unable to claim. The same reporting noted 37 income protection claims were denied on those grounds in the five years prior to 2018, according to Super Review’s report on the Rest class action.

The unemployment trap

This is the hidden risk that deserves far more attention.

A member may think, “My premium is still coming out, so I’m insured.” But if the policy has work-status conditions, being unemployed or inactive can create a mismatch between what the member thinks they own and what they are eligible to claim.

That’s why this trap is so serious. It’s not the obvious problem of having no policy. It’s the harder problem of having a policy that may not respond when needed.

Why this catches casual and changing workers

Rest has strong relevance for workers in sectors where employment patterns can shift. Casual work, part-time work, job changes, unpaid breaks, and periods without contributions can all create confusion.

If your employment has become less stable, these are the questions worth asking:

- Am I still actively eligible under the policy terms?

- Has my account become inactive in a way that affects insurance?

- If I had to claim now, what evidence of work status would the insurer require?

- Am I paying for cover that no longer matches how I’m employed?

A lot of members never ask those questions because they assume insurance in super is passive. It isn’t. It needs checking.

Offsets can reduce what you receive

Another trap is misunderstanding how much the insurer will pay once other income sources are considered.

With Rest, offsets apply so total income from all sources doesn’t exceed the policy limit described in the policy material. In everyday terms, if you receive sick leave, workers’ compensation, or similar payments, the income protection payment may be reduced.

That can surprise people who mentally add every support payment together and assume they’ll all stack neatly.

Practical rule

Don’t estimate a claim by looking only at the headline monthly benefit. Check what other payments may reduce it.

Default cover can still be the wrong fit

There’s also a design issue with any default group policy. It has to suit a broad membership base. That means it won’t be built around your exact debt level, tax position, partner’s income, or business obligations.

Common mismatches include:

- A mortgage that needs more monthly cash flow than the policy would provide

- A household where one income supports multiple dependants

- A self-employed person whose business costs continue even if personal income stops

- A pre-retiree who needs to protect super in the final years before retirement

If you want a clearer sense of the exclusions and limitations that often catch people out, this article on what income protection does not cover is worth reading closely.

The main lesson is simple. A rest income protection policy can be useful, but it should never be treated as “set and forget”. The risk isn’t only underinsurance. It’s paying for a safety net with holes you don’t know are there.

Comparing Your Options Inside and Outside Super

A client in their mid-30s comes in with a familiar assumption. Their income protection sits inside super, premiums are being deducted unnoticed, and they take that to mean the problem is handled.

Sometimes it is partly handled. Often it is only partly funded.

That distinction matters. Cover inside super and cover outside super are not rival camps. They are two different ways to insure the same income, and each solves a different problem. Inside super often helps with affordability. Outside super often gives you more control over definitions, benefit design, and how closely the policy matches your real life.

A practical way to assess it is to picture your protection like home security. Default cover inside super can work like the standard lock that came with the front door. It may be enough for some households. But if you have a larger property, more valuables, or a weak side gate, you may need stronger protection in the places the basic setup does not cover well.

A side by side view

| Feature | Inside Super (e.g., Rest) | Standalone Policy |

|---|---|---|

| How premiums are funded | Usually paid from your super balance | Usually paid from your personal cash flow |

| Ease of starting cover | Often simpler because cover may be automatic or easier to access | Usually more tailored, but often involves more active application steps |

| Cost position for basic cover | Group design can make entry-level cover cheaper to hold | May cost more, especially where features are broader |

| Customisation | Usually more standardised | Usually offers more scope to tailor features |

| Definitions and policy design | Built for a broad group of members | Often more individually structured |

| Impact on super balance | Premiums can reduce retirement savings over time | Does not directly reduce your super balance |

| Portability and control | Can be linked to your super arrangements and contribution pattern | Often gives more direct personal control over the policy |

| Best fit | Good starting point for many workers wanting a basic safety net | Often better for people needing precision, stronger tailoring, or greater certainty around structure |

Where cover inside super can work well

Super-based cover usually appeals for one simple reason. It is easier to keep in place when day-to-day cash flow is tight.

That can be useful for younger workers, people rebuilding savings, or anyone who wants some protection in place before committing to a separate premium from their bank account. Group insurance can also be simpler to start, which reduces the risk of doing nothing for years while meaning to "get around to it."

Industry-wide reporting from APRA on life insurance claims and disputes also shows why group cover should not be dismissed as low quality by default. It plays a large role in the Australian protection market and regularly pays substantial numbers of claims, even though product design is necessarily standardised across a broad membership base. The lesson is not that group cover is better in every case. The lesson is that it can be a legitimate foundation.

Where outside-super cover often becomes the better tool

A standalone policy usually starts to make more sense once your finances stop looking average.

That includes people with rising incomes, large fixed expenses, family commitments, or business cash flow that depends heavily on their ability to work. In those situations, the critical risk is not only whether a claim would be paid. It is whether the policy structure would be adequate when pressure hits.

This is also where the unemployment trap deserves attention. If your cover is tied to a super arrangement and your work situation changes, the practical risk is not just a missed contribution. You may lose track of whether cover continues, reduces, or ends under the rules of that fund. A separate policy can reduce that dependency because ownership and payment sit more directly with you.

The question I would ask a new client

Do you want the cheapest way to hold some cover, or do you want the clearest way to protect your actual financial life?

For many people, the answer is neither extreme. The better setup is often a layered one. Keep the inside-super cover if it is cost-effective, then add outside cover only where there is a genuine gap. That might be a longer benefit period, a stronger definition, or enough monthly cover to protect the mortgage and household costs properly.

A related issue is making sure you are comparing different types of protection correctly. Income protection replaces part of your income if illness or injury stops you working. Trauma cover serves a different purpose. This explainer on Critical Illness vs Income Protection is useful if you want to see where each type of policy fits.

If you want a clearer framework for weighing price, definitions, waiting periods, and ownership structure, this guide on how to compare income protection policies properly will help.

A policy that looks affordable on paper can still leave a serious gap in real life. The right comparison is not inside super versus outside super. It is whether your current setup would still hold up if your income stopped next month.

Tailoring Your Cover for Your Life Stage

A one-size-fits-all policy only works if your life is one-size-fits-all. Very few people stay in that position for long.

The right way to assess a rest income protection policy is to ask how well it fits your current stage of life, not how convenient it was when it first appeared in your super account.

Young professionals

If you’re early in your career, default cover can be a sensible starting point. You may not want to commit a large amount of personal cash flow to insurance, and some protection is usually better than ignoring the risk altogether.

But early career workers often underestimate how quickly their income becomes their biggest asset. If your salary is rising, your rent is climbing, and your lifestyle depends on continued work, the main question is whether your cover is keeping pace.

A useful check is to ask yourself whether the current policy would merely help you survive, or whether it would allow you to recover without derailing your financial progress.

Dual-income families

These households often think they are safer because there are two earners. Sometimes that’s true. Sometimes it hides a concentration risk.

If one income disappears, the household may still face the same mortgage, childcare, school costs and general living expenses. In many families, one income also carries the larger share of fixed commitments.

That means default cover may not be enough even when both partners work. The issue isn’t only replacing income. It’s protecting the household system that depends on it.

Questions worth asking include:

- Would one partner’s income cover the essential bills alone?

- Would a waiting period force the family to use savings quickly?

- Does the current cover reflect today’s expenses, not the lifestyle from several years ago?

Small business owners

Business owners need a different lens. You don’t just lose personal income when you can’t work. The business may also lose momentum, revenue, or client relationships.

A standard group policy may help with personal income, but it often won’t line up neatly with the realities of running a business. You may still have rent, wages, software subscriptions, vehicle costs, and tax obligations tied to the business structure.

That doesn’t automatically make super-based cover unsuitable. It just means the margin for error is smaller, and generic settings are more likely to leave blind spots.

Pre-retirees

For pre-retirees, the stakes are different again. The final years before retirement can be important because there’s less time to rebuild savings after a health event.

At this stage, the policy needs to be assessed not just for immediate income support, but for how it interacts with retirement planning. A period out of work can affect cash flow, contribution patterns, and the timing of retirement itself.

The closer you are to retirement, the less room you usually have for an insurance mistake.

For this group, the right answer often comes from coordination. Super, cash reserves, debts, retirement timing and existing insurance all need to be looked at together. That’s why broad default settings are rarely enough on their own.

How to Build Your Financial Safety Net

A rest income protection policy can do an important job. It can provide a meaningful starting point, especially for members who might otherwise have no protection at all. But after that starting point, the important work begins.

You need to know what the policy would pay, when it would start, what could reduce the benefit, and whether your current work situation still supports a valid claim. You also need to decide whether the cover suits your stage of life or whether it suits the average member profile the fund had in mind.

A practical review checklist

Before relying on any default cover, it helps to check five things:

- Your actual monthly needs: list the bills that would continue if your income stopped.

- Your waiting period resilience: work out how you’d cover the gap before payments begin.

- Your employment status: confirm that your work pattern and account activity still align with policy eligibility.

- Your offsets and limitations: understand what other payments could reduce the claim.

- Your broader protection mix: decide whether default cover should stand alone or sit beside more customized insurance.

The bigger lesson

Individuals often don’t need more product information. They need clearer judgement.

The challenge isn’t reading another policy summary. It’s connecting the policy to your mortgage, your family, your business, your super balance, and your retirement timeline. That’s where insurance stops being an administrative line item and starts becoming part of a real financial plan.

If reviewing your cover has made you realise there may be gaps, that’s a good result. It’s far better to identify those gaps in a calm review than during a claim.

If you want help turning default cover into a proper protection strategy, Wealth Collective can help. Their advisers work with Australians who want clear guidance on super, personal insurance and long-term financial planning, using a simple process that starts with a free 10-minute introductory call.