Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A lot of people reach retirement planning in Australia at the same point. The mortgage is smaller than it used to be, super has finally become a meaningful number, and the question stops being “Am I saving enough?” and becomes “How do I turn all of this into a life that works?”

That's where retirement planning often gets messy. Super, the Age Pension, tax, debt, investments, estate planning. They all affect each other. A decision that looks sensible in isolation can create a poor outcome once the full picture is considered.

The better approach is to treat retirement as an integrated plan, not a checklist. If you're in Perth, regional WA, or anywhere else in Australia, that usually means getting clear on the lifestyle first, then testing how each retirement pillar supports it.

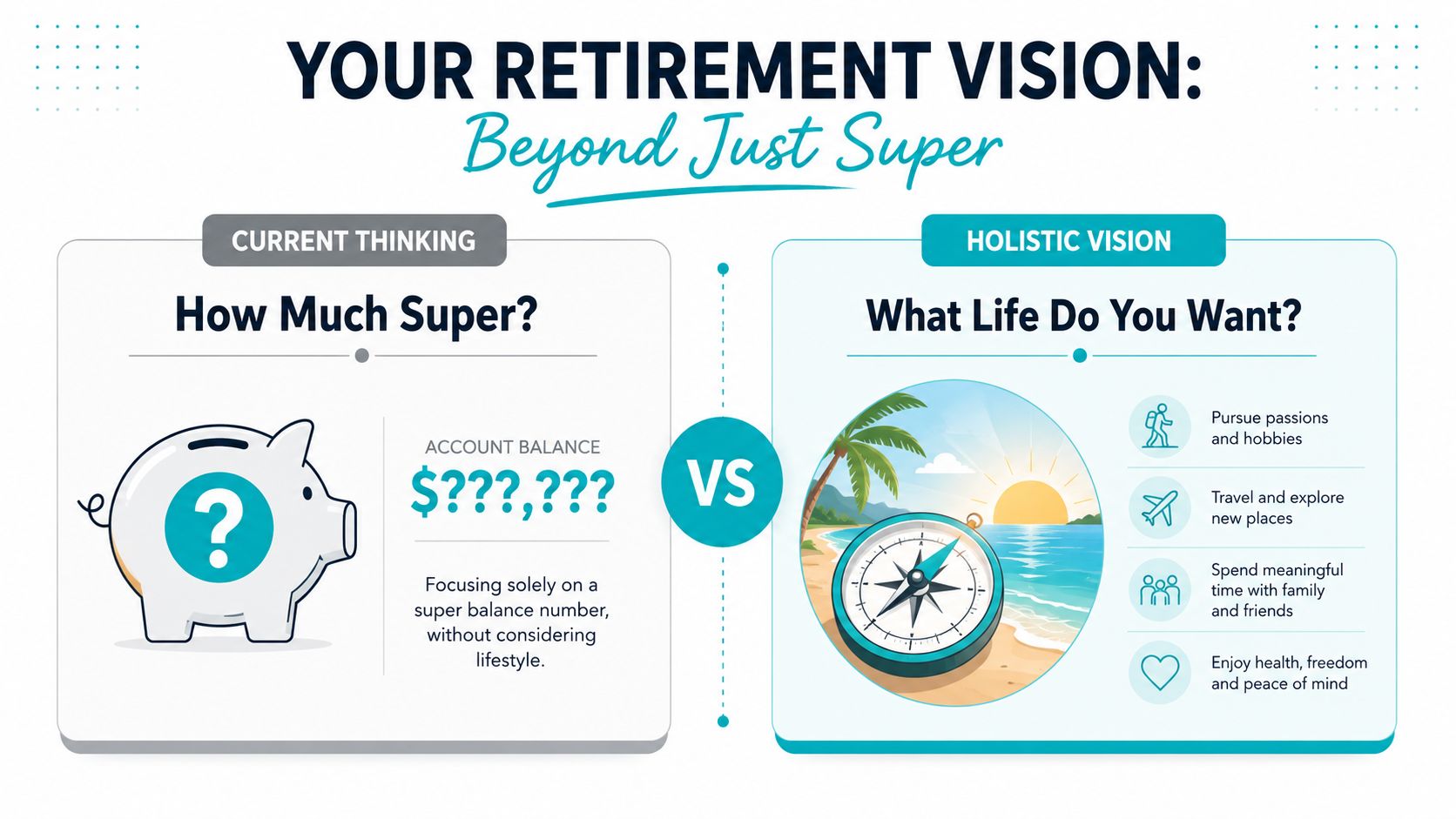

Defining Your Retirement Vision and Cashflow Needs

Many individuals start with the wrong question. They ask, “How much super do I need?” before they've worked out what they want retirement to look like.

That matters because retirement spending isn't one number. It depends on the life you want to fund. Travel, helping adult children, replacing cars, hobbies, private health costs, home maintenance, and whether you own your home all change the answer.

Start with lifestyle, not balance

The ASFA Retirement Standard gives a useful reality check. For the December quarter 2025, ASFA estimates that a single person aged 65 to 84 needs $54,840 a year for a comfortable lifestyle and $35,503 for a modest lifestyle, while a couple needs $77,375 a year for a comfortable lifestyle and $51,299 for a modest one. ASFA also notes these figures assume the Age Pension is received within Australia's mixed retirement income system, as set out in the ASFA Retirement Standard.

Those figures are not your budget. They're a benchmark. They help you decide whether your expectations sit closer to modest, comfortable, or something more personalized.

Practical rule: If you can't describe the week you want to live in retirement, you're not ready to choose the income you'll need.

Questions that sharpen the picture

I find it helps to map retirement as a series of real decisions, not vague goals. Ask yourself:

- Housing first: Will you stay in the family home, renovate it, downsize, or relocate?

- Travel expectations: Are you planning occasional local trips, regular interstate travel, or larger overseas holidays?

- Work by choice: Do you want to stop completely, reduce to part-time work, or keep consulting for a few years?

- Family support: Will you help children, grandchildren, or ageing parents financially?

- Health and care: Do you expect rising medical costs, home support, or changes to insurance needs?

- Lifestyle rhythm: What will fill your time. Golf, volunteering, caravanning, community work, hobbies, or something else?

If downsizing is part of the plan, practical preparation matters as much as financial modelling. A resource like DIYAuctions' guide for seniors can help you think through the practical side of moving before you make financial assumptions around it.

Turn the vision into a cashflow target

Once the lifestyle is clearer, sort spending into three buckets:

| Spending bucket | What belongs here | Why it matters |

|---|---|---|

| Core costs | groceries, utilities, rates, insurance, transport | These must be funded every year |

| Lifestyle costs | travel, dining, hobbies, gifts | These shape whether retirement feels constrained or enjoyable |

| Irregular costs | car replacement, repairs, health events, helping family | These often derail otherwise sensible plans |

That process gives you something far more useful than a super target. It gives you an annual income target that reflects your actual life.

In retirement planning in Australia, that's the foundation. Without it, every product discussion is premature.

Maximising Your Superannuation Engine

Once you know the lifestyle you're aiming to fund, super becomes a tool rather than a mystery. It's still the main retirement asset for many Australians, but the biggest mistake is assuming compulsory contributions will automatically deliver the outcome you want.

The gap between a modest and comfortable retirement makes that clear. For a comfortable retirement at age 67, ASFA estimates a single person needs around $630,000 in super, compared with $110,000 for a modest retirement. For a couple, the estimate is $730,000 for a comfortable retirement and $120,000 for a modest retirement, based on the assumptions discussed in this Australian retirement model summary.

Why the compulsory system doesn't answer the whole question

Australia's super guarantee has risen above the older 9% level that many people still have in mind, and that's helpful. But it doesn't solve every retirement problem equally.

If you're close to retirement, the runway is shorter. If you rent, your retirement costs are often tougher to absorb. If your balance is modest, the challenge is less about the super account itself and more about how it will work alongside the Age Pension, housing, and drawdown strategy.

That's why broad statements like “just contribute more to super” are only partly useful.

The contribution decisions that matter

For most pre-retirees, there are a handful of levers worth reviewing carefully:

- Employer and voluntary contributions: Know what's already going in and whether that pace matches the retirement target you've set.

- Salary sacrifice: This can be an effective way to build super from pre-tax income when it fits your cashflow.

- After-tax contributions: These may suit people with available savings, inheritances, or proceeds from asset sales.

- Investment mix inside super: A portfolio that made sense at 40 may not suit someone planning to draw on it soon.

- Multiple funds and fees: Consolidation can simplify administration where it's appropriate and where insurance or legacy features won't be lost.

For readers wanting a plain-English refresher on how the system works, this overview of superannuation in Australia is a useful starting point.

More super is helpful. Better structured super is what usually makes the difference.

What works and what doesn't

What tends to work is a deliberate contribution plan tied to a known retirement date, expected spending, and likely pension position.

What often doesn't work is one of these common patterns:

- Set and forget: People keep the same contributions and investment settings for years without checking whether they still match the goal.

- Balance obsession: They focus on hitting a round number without planning how the money will be converted to income.

- Late lump decisions: They wait until the final year before retirement to ask whether extra contributions would have helped.

- Ignoring the rest of the balance sheet: They build super while carrying debt or leaving tax planning too late.

The practical question isn't whether super matters. It does. The practical question is whether your super strategy fits your retirement system as a whole.

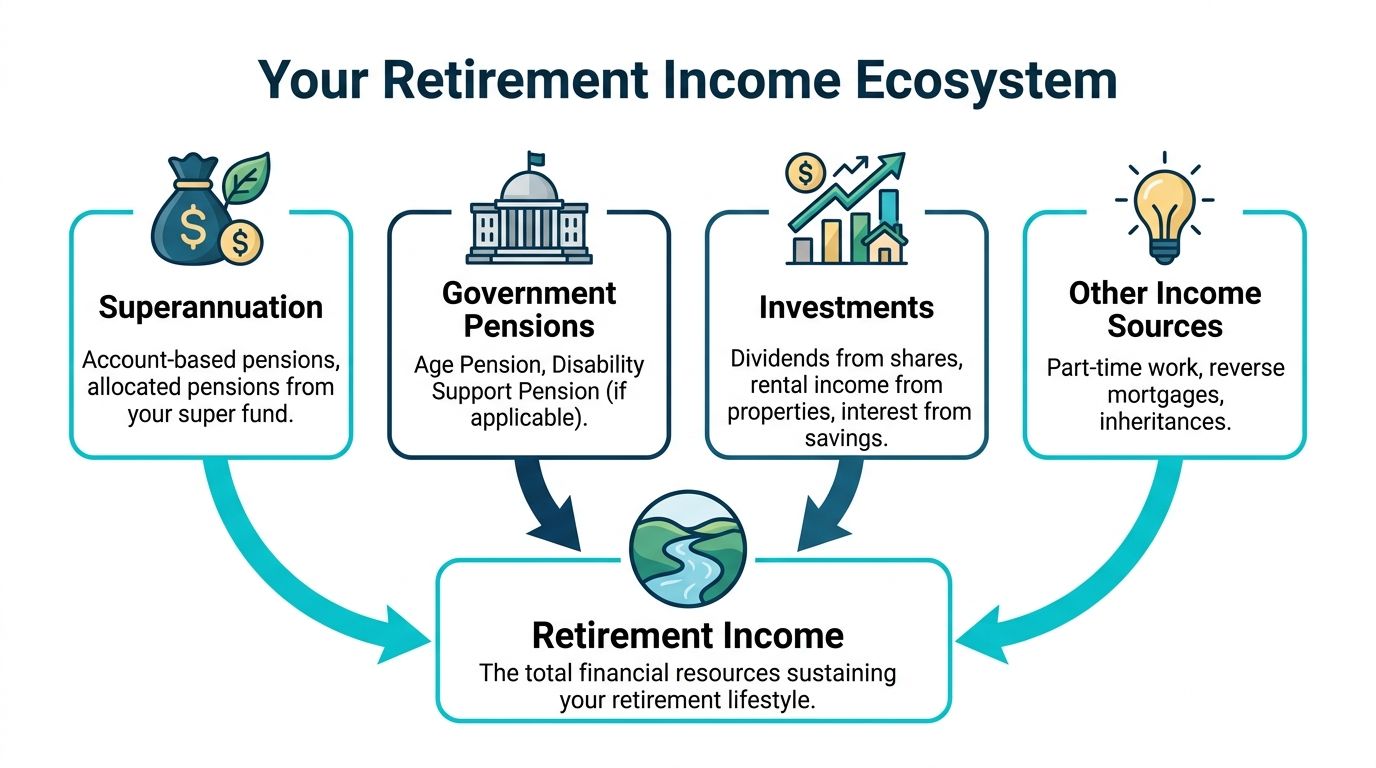

Modelling Your Future Income Streams

Accumulating money is only half the job. Retirement succeeds or fails on income design.

That's the point where many people become uncertain. They know they'll have super, perhaps some personal investments, maybe part-time work, and possibly the Age Pension. What they don't know is how those pieces should be sequenced.

Income in retirement is a system

A practical workflow used in Australian retirement planning is to map income sources first, estimate spending second, and optimise the drawdown strategy last. Australians can generally access super from preservation age, which is 60 for everyone currently in the workforce, depending on birth date, and a starting benchmark is to estimate retirement spending at about two-thirds of current living costs before comparing account-based pension, annuity, lump-sum, and Age Pension outcomes, as outlined in AMP's retirement planning guide.

That sequencing matters. It stops people from choosing products before they understand the cashflow problem those products need to solve.

The main income sources and their trade-offs

A retiree's income might come from several places at once:

| Income source | Where it helps | Where caution is needed |

|---|---|---|

| Account-based pension | Flexible access and familiar structure | Draw too hard too early and long-term sustainability suffers |

| Annuity | Can provide a steadier income base | Less flexible than keeping all funds fully accessible |

| Lump sum | Useful for debt clearance, major expenses or restructuring assets | Easy to overuse without a wider cashflow plan |

| Age Pension | Important support within the broader system | Means testing and asset positioning need care |

| Non-super investments | Can add flexibility and tax planning options | Different ownership structures can change outcomes |

| Part-time work | Can reduce pressure on super in early retirement | Needs to be coordinated with broader income planning |

If tax is part of the equation, Allied Tax Advisors' retirement tax strategies are a helpful general resource for thinking through sequencing and withdrawal order.

Where advice adds real value

This is usually where DIY planning starts to fray. Not because the ideas are hard to understand, but because the interactions are easy to misjudge.

An account-based pension may look simple until you compare it against Age Pension outcomes. An annuity may look restrictive until you model what reliable lifetime income could do for confidence and spending discipline. A lump sum may feel attractive until it creates tax, pension, or estate complications elsewhere.

That's why a proper retirement income plan should test different combinations, not just pick the most familiar option. If you want a clearer view of how these structures work, this guide to retirement income streams explains the main pathways in practical terms.

The best drawdown strategy isn't the one with the most flexibility on paper. It's the one that keeps income reliable without boxing you in later.

Clearing Debts and Reducing Tax Pre-Retirement

Retirement income works better when it isn't being pulled apart by old liabilities. That's why the years before retirement should focus on cleaning up the balance sheet as much as building assets.

For many households, the first issue is the mortgage. Carrying debt into retirement isn't automatically wrong, but it does reduce flexibility. A loan repayment that feels manageable while you're working can become a source of pressure once income becomes fixed or semi-fixed.

Clearing the decks before work stops

Start with a straightforward test. If your employment income stopped next year, which debts would still feel comfortable?

That question often changes the discussion. The debt might be technically affordable, but still emotionally draining. Retirement tends to feel more secure when core living costs are low and predictable.

Useful pre-retirement actions include:

- Prioritise non-deductible debt: Home loan debt often deserves attention before optional investing outside structured retirement goals.

- Avoid new lifestyle debt: Cars, renovations, and large discretionary purchases close to retirement can crowd out flexibility.

- Use windfalls intentionally: Bonuses, inheritances, or asset sale proceeds shouldn't drift into general spending without a plan.

- Stress test repayments: Check how the budget looks on retirement income, not just on current salary.

Tax planning needs timing, not guesswork

Tax planning before retirement is less about chasing tricks and more about coordinating the timing of decisions.

For example, selling an investment property, realising gains on shares, making super contributions, or restructuring ownership can all affect your position. The same move can be sensible in one year and poor in another, depending on your taxable income, pension timing, and retirement start date.

That's why broad tax tips often disappoint. Tax doesn't sit in a separate box. It intersects with super access, asset sales, Centrelink outcomes, and estate planning.

A sound approach is to review major assets and ask:

- What do I intend to keep in retirement?

- What do I intend to sell?

- When should each decision happen?

- What does that do to tax and future income?

The aim is simple. Preserve more of your capital for retirement living, rather than letting old debts and avoidable tax erode it.

Protecting Your Wealth and Estate

A retirement plan that ignores risk isn't complete. It may look organised on paper, but it's still vulnerable.

As retirement approaches, the focus often shifts heavily to super and investments. That's understandable. But accumulated wealth can be damaged quickly by illness, incapacity, poor documentation, or family disputes after death. Protection planning matters because it keeps the rest of the strategy intact.

Insurance still matters near retirement

Insurance needs usually change in the pre-retirement years. Earlier in life, the priority is often replacing income for a young family. Closer to retirement, the role may shift toward protecting assets, supporting a spouse, or creating breathing room if health changes derail the transition out of work.

Review these areas carefully:

- Life cover: Does it still reflect your debts, dependants, and legacy intentions?

- TPD cover: Would a permanent health event before retirement disrupt the plan materially?

- Trauma or critical illness cover: Could a serious diagnosis force early access to savings or alter retirement timing?

- Cover inside super: Is the policy still appropriate, and do you understand the trade-offs of holding it there?

What doesn't work is leaving old insurance untouched because “it's already in place”. Policies can become mismatched to your actual needs.

Estate planning is part of financial planning

Estate planning is not just about who gets what. It's also about who can act if you can't.

A proper retirement plan should include current legal documents and clear beneficiary arrangements. In practice, that usually means reviewing your will, enduring powers, and super death benefit nominations together, not separately. Super is especially important because it doesn't always flow under your will in the way people assume.

A well-funded retirement can still create family stress if the legal instructions are unclear or out of date.

The goal here isn't complexity. It's certainty. If something unexpected happens, the people around you should know what you wanted, who is authorised to act, and how the financial structure is meant to work.

Your Implementation and Review Schedule

Retirement plans rarely fail because someone had no intention of getting organised. They usually fail because decisions were delayed, fragmented, or never revisited.

That's risky in Australia because retirement doesn't always happen on your preferred schedule. The ABS reported that, in 2024 to 2025, Australians aged 45 and over intended to retire at 65.6 years on average, but retired at 63.8 years on average. The same ABS release also reported 156,000 people aged 45 and over retired, and that there were 4.5 million retirees aged 45 and over in Australia, with the government pension remaining the most common main source of income for retirees, according to the ABS retirement and retirement intentions release.

That gap between plan and reality is one of the most important facts in retirement planning in Australia. It means your strategy needs to cope with an earlier finish than expected.

A practical review rhythm

A retirement plan should be reviewed when life changes, not only when markets move. Good trigger points include:

- Work changes: reduced hours, redundancy, business sale, or a planned retirement date becoming clearer

- Family changes: death of a spouse, helping children financially, or caring for parents

- Asset changes: selling property, receiving an inheritance, or moving house

- Health changes: anything that may bring retirement forward or alter spending

- Legislative changes: super, pension, or tax settings that may change strategy

A simple implementation schedule often looks like this:

| Time frame | Focus |

|---|---|

| 5 to 10 years out | clarify lifestyle target, review super settings, assess debt reduction path |

| 2 to 5 years out | model retirement income options, test pension interaction, plan asset sales |

| 12 months out | finalise structure, confirm cash reserves, update estate documents |

| Ongoing in retirement | review drawdown, tax position, spending pattern, and family goals |

Where many people get stuck

Most households can identify their broad goals. The sticking point is execution.

They're unsure whether to contribute more to super or pay down the mortgage. They don't know whether an account-based pension alone is enough. They haven't tested how the Age Pension fits in. They suspect tax can be improved, but they're wary of making a wrong move.

That's where a structured advice process becomes useful. Wealth Collective's Retirement Roadmap is designed to help clients define retirement goals, map future cashflow, review super and investment settings, and coordinate retirement income decisions with debt, tax, and estate planning. It's one planning framework for the whole retirement picture, rather than separate decisions made in isolation.

What an effective plan looks like

A workable retirement plan is usually clear on five points:

- The lifestyle target is defined. You know what you're trying to fund.

- Super is being used deliberately. Contributions, investment settings, and structure match the goal.

- Income streams have been modelled. You know how super, pension, and other assets interact.

- Debt and tax have been addressed. Old liabilities aren't draining retirement income.

- Protection and estate planning are current. The plan can withstand disruption.

If any of those five are still vague, the next step isn't more reading. It's getting the numbers and decisions tested properly against your circumstances.

If you want help turning these moving parts into a personal plan, book an initial conversation with Wealth Collective. A short call can clarify where you stand now, which decisions matter most, and whether a personalized retirement roadmap would help you move forward with more confidence.