Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Many Australians reach retirement with a strange balance sheet. They may own a valuable home, yet still feel cautious about day-to-day cashflow. The house is solid. The budget feels less so. That tension is often what brings people to search for reverse mortgage calculator australia.

A common situation looks like this. A couple in Perth wants to stay in the family home, help cover rising living costs, maybe update the bathroom, maybe visit family more often. They're not looking for a flashy financial product. They're looking for breathing room without having to sell.

A reverse mortgage can sometimes help with that. But it's not a simple “how much can I get?” question. It's really a long-term trade-off between cashflow today and home equity later. That's why a calculator matters. Used properly, it helps you test consequences before you make commitments.

Planning Your Retirement Cashflow in Australia

For many retirees, the goal isn't complicated. Stay at home. Keep control. Have enough income to live comfortably.

The challenge is that retirement cashflow rarely arrives in a neat, predictable pattern. Some years are steady. Other years bring bigger expenses, such as home repairs, health costs, family support, or the desire to enjoy retirement while you can. That's where home equity enters the conversation.

When the house is rich but the budget is tight

Consider a retiree in Perth or Dunsborough who owns their home outright but feels reluctant to draw down savings too quickly. They may already be reviewing super, pension eligibility, and other retirement income streams. Even after that, there can still be a gap between what life costs and what the household can comfortably spend.

A reverse mortgage is one possible tool in that gap. It lets eligible homeowners access part of their home equity without selling the property straight away. For some people, that can create flexibility. For others, it can create future pressure if the numbers aren't tested carefully.

Practical rule: Treat a reverse mortgage calculator like a stress test, not a green light.

That distinction matters. Many people open a calculator hoping for reassurance. What they need is perspective. The most useful result isn't the maximum amount available. It's a clearer understanding of what borrowing today might mean for future choices.

Why the calculator is the first sensible step

A reverse mortgage affects more than one moving part at once. It changes debt, future equity, and often your comfort level about staying in the home long term. A good calculator helps you see those moving parts together.

The most useful mindset is this:

- Cashflow first: what problem are you trying to solve?

- Equity second: how much home value do you want to preserve?

- Time horizon third: how long might you stay in the property?

- Family context: do estate plans or future care needs matter strongly here?

Used that way, the calculator becomes a planning tool. It moves the conversation away from “How much can I borrow?” and towards “What happens if I do?”

What Is a Reverse Mortgage in Australia

A reverse mortgage is a loan against your home that lets you draw on part of its value while you keep living there. For many retirees, that can feel like turning a large but quiet asset into money that can support day-to-day life.

The appeal is easy to understand. A home may hold a lot of wealth on paper, yet paper wealth does not pay for repairs, dental work, helping family, or making retirement a little more comfortable. A reverse mortgage can provide access to some of that value without selling the property straight away.

The key point is that it is still a loan.

How it differs from a standard home loan

A standard mortgage usually starts with a large debt that shrinks as you make repayments. A reverse mortgage often does the opposite. You usually receive funds now, make no regular repayments from income, and the balance grows over time as interest and fees are added. The loan is commonly repaid later, such as when the home is sold, when the borrower moves into aged care, or from the estate.

That repayment structure can relieve pressure on retirement cashflow. It can also make the long-term cost harder to feel in real time, because the borrower is not seeing a monthly repayment leave the bank account.

That is where confusion starts.

Why the debt can grow faster than people expect

A reverse mortgage works like a snowball rolling downhill. Interest is added to the loan balance, then future interest is charged on that larger balance. Over many years, the debt can increase much faster than borrowers first expect.

This is compounding debt.

A useful way to picture it is an unpaid tab that stays open for a long time. Nothing seems urgent month to month, but the total keeps rising in the background. A calculator helps bring that hidden growth into view, which is why advisers use it as a risk check rather than a reassurance tool.

At the same time, your remaining equity can shrink. If debt is growing and the home value does not rise as hoped, the share of the property left for future choices becomes smaller. That matters if you may want to downsize later, fund aged care, or leave more to family.

A reverse mortgage can improve cashflow today while reducing flexibility later.

How the money is usually accessed

Reverse mortgage funds are often available as a lump sum, regular payments, a line of credit, or a mix of these options. The structure matters because it affects how quickly interest starts building and how much equity may remain over time.

Lenders also place limits on how much can be borrowed, usually based on age, property value, and loan policy. As noted earlier, lenders commonly allow access to only a portion of the home's value, not the full amount. Westpac explains that reverse mortgages can be set up in different drawdown formats, with interest compounding until the loan is repaid.

From an adviser's perspective, that is the key lesson. A reverse mortgage is not just a way to get a number from a calculator. It is a strategic decision about using home equity now while protecting future options. The calculator helps you test that trade-off, but personalised advice matters because the calculator cannot judge your time horizon, care needs, estate goals, or comfort with seeing equity fall. That is exactly why many retirees need a broader plan, such as Wealth Collective's Retirement Roadmap, before treating any loan estimate as workable.

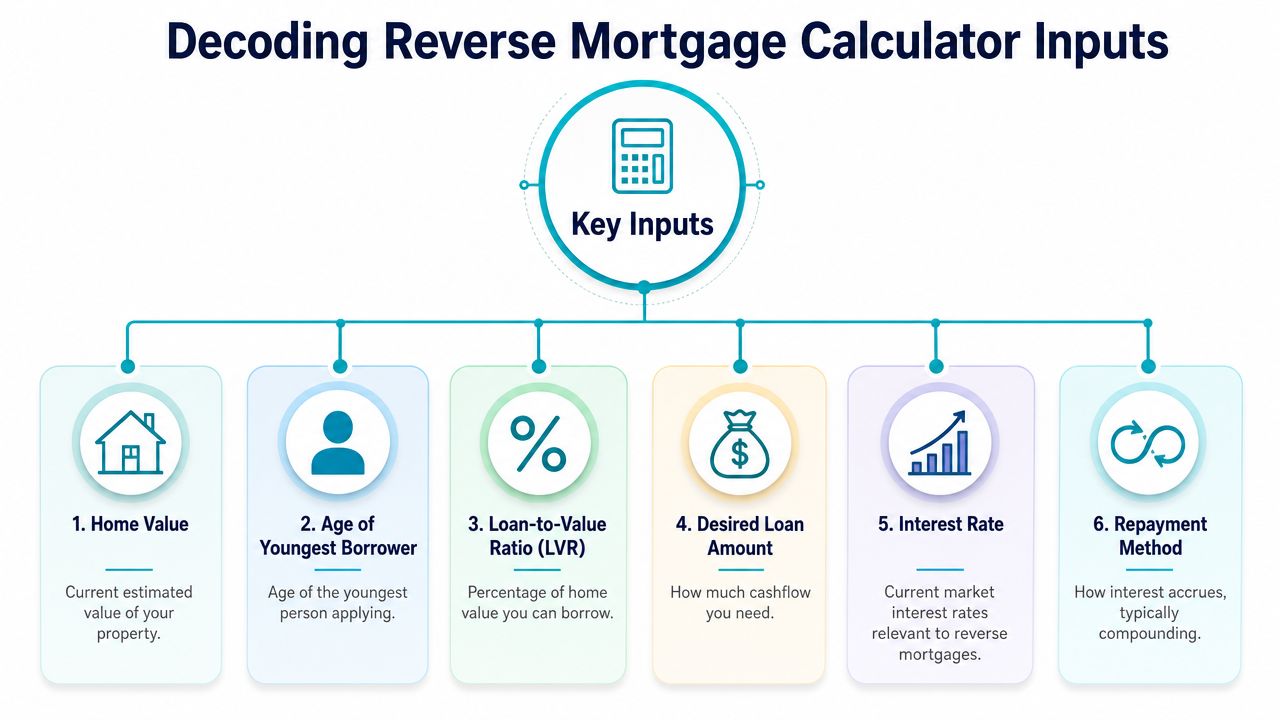

Decoding the Reverse Mortgage Calculator Inputs

A reverse mortgage calculator only helps if you treat each input like a planning assumption, not a blank box to fill in quickly.

That distinction matters more than many retirees expect. A calculator can produce a neat estimate while still giving false comfort if the starting assumptions are too hopeful. A slightly higher home growth rate, a slightly lower interest rate, or a skipped fee can make the result look safer than it really is. From an adviser's perspective, this is why the calculator works best as a risk-testing tool. It helps you ask, “What happens if life is less tidy than my first estimate?”

The inputs that matter most

The fields are simple. The judgement behind them is not.

| Input | Why it matters |

|---|---|

| Age of youngest borrower | This affects how much may be available to borrow, because the loan may need to last for many years. |

| Property value | The home secures the loan, so its current value shapes the borrowing range. |

| Loan amount sought | This shows whether the amount you want fits within likely lending limits. |

| Interest rate | This affects how fast the loan balance can grow through compounding. |

| Fees | Setup costs and ongoing charges can add to the balance over time. |

| Property growth assumption | This shapes how much equity may remain later, even if the debt itself is unchanged. |

A useful way to read these inputs is to split them into two groups. One group controls how fast the debt grows. The other group affects how much home value may still be left after that debt is repaid. If you only focus on the projected loan balance, you can miss the bigger planning question, which is how much flexibility remains for downsizing, aged care, or estate goals.

Age is carrying more weight than many people realise

Age is not there for identification. It is one of the main drivers of the estimate.

For couples, calculators usually use the age of the youngest borrower because that person is likely to remain in the property longer. That often reduces the amount available compared with using the older partner's age alone. It can feel like a technical detail, but it changes the shape of the whole strategy.

This is a common point of confusion. A retiree might look at home value first and assume that is the main number that matters. In practice, age and time horizon work like the length of a repayment-free runway. The longer the expected runway, the more carefully the borrowing limit is set.

Interest and growth are working against each other

Interest compounds on the loan balance. Property growth, if it occurs, may support the equity side of the picture.

A simple comparison helps here. The debt side works like a snowball rolling downhill. Each year's interest can add to the balance, and next year's interest may then be charged on that larger amount. The home value side can also rise over time, but it will not always rise at the pace you hope for. If debt grows faster than property value, your remaining equity shrinks.

That is why a calculator should never be used as a machine for producing one reassuring number. It is better used as a pressure-testing tool.

The assumption that deserves the most scepticism

The property growth field often causes the biggest planning mistake.

People are naturally anchored to the value of their home and the story they tell themselves about what it “should” be worth later. That can lead to optimism that makes the long-term projection look more comfortable than it is. A reverse mortgage calculator cannot warn you when you are being too generous to your future property value. It processes what you enter.

Fees can be treated the same way. Small ongoing charges may not look important at the start, but over a long retirement they can push the balance higher than expected.

Use scenarios, not a single estimate

A better approach is to run a few versions of the same plan and compare them.

- Base case. Reasonable assumptions for rates, fees, and home growth.

- Conservative case. Lower property growth or a longer loan period.

- Pressure case. Higher costs, weaker growth, or both.

That process gives you a more honest picture of risk. It also helps surface the questions a calculator cannot answer on its own. How much equity do you want to protect? How sensitive is your plan to a poor property market? Would a smaller drawdown still meet your cashflow needs?

Those are advice questions, not calculator questions. That is exactly where a broader strategy process, such as Wealth Collective's Retirement Roadmap, becomes valuable. The calculator can show possible outcomes. A personalized plan helps decide whether those outcomes still fit the life you want later.

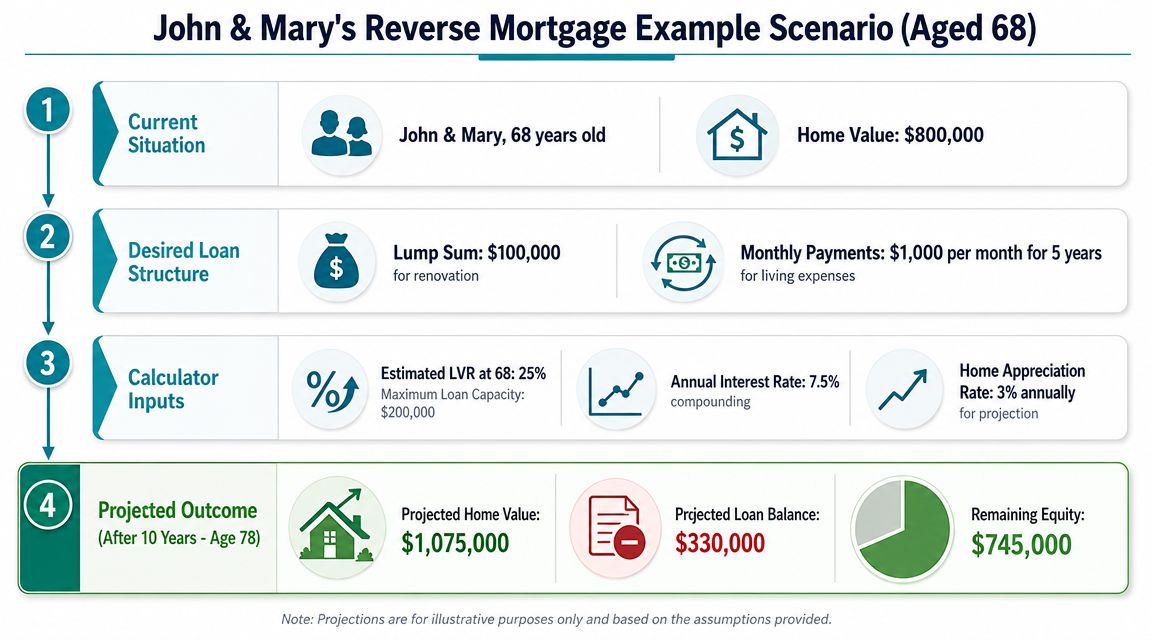

A Step-by-Step Calculator Example Scenario

John and Mary are both 68, own their home in Western Australia, and want extra retirement cashflow without selling. They are considering a reverse mortgage to pay for home upgrades and create a little more breathing room in their budget. A calculator helps them test that idea before they commit to it.

What the example is really showing

Start with the same fields a calculator asks for. Their ages. The home value. How much they want to borrow. Whether they plan to take a lump sum, regular payments, or a mix of both. Then come the assumptions doing the heavy lifting in the background, such as interest, fees, and future property growth.

The worked example in the infographic is useful because it turns an abstract idea into a visible pattern.

A reverse mortgage is less like a standard loan with regular repayments and more like a tap connected to the value in your home. The tap can solve a short-term cashflow problem, but the water meter keeps running. Interest is added to the loan balance, then future interest is charged on that larger balance. Over time, that can reduce the share of the home you still own outright.

For John and Mary, the main lesson is not the final number after ten years. It is the interaction between three moving parts:

- The amount drawn

- The length of time the loan remains in place

- The gap between debt growth and home value growth

That third point is where many retirees need to slow down. If the loan balance grows like a rolling snowball and the property value rises more modestly, the remaining equity can shrink faster than expected.

How to read the output like an adviser

As noted earlier, the Moneysmart calculator is the common starting point for this kind of projection. The value of the result is not just the borrowing amount shown on screen. The value is in what the projection reveals about future trade-offs.

A client working through this with an adviser would usually focus on three questions:

- What happens to the loan balance over time? A figure that looks manageable today can become much larger after years of compounding.

- How much home equity may remain later? That matters if John and Mary may need aged care options, a future move, or a financial buffer.

- How sensitive is the result to small changes? A modest shift in rates, time in the home, or property growth can change the picture a lot.

This is why calculators are better used as risk-testing tools than decision machines. A single output can look reassuring because it feels precise. Precision is not the same as safety.

Running the scenario twice changes the conversation

Here is a practical way to use the example. John and Mary first enter the amount they would like to access for renovations and lifestyle spending. Then they run a second version with conditions that are less forgiving. They might stay in the home longer. Their spending may rise. The property may not grow as hoped.

That second run often tells the more useful story.

It shifts the conversation from "How much can we borrow?" to "How much can we borrow and still protect future choices?" That is the question an adviser tries to answer, because retirement lending decisions affect more than this year's cashflow. They affect later flexibility, family options, and peace of mind.

A calculator can produce a projection. Personal advice helps decide whether that projection still fits the retirement life you want. That is the kind of work Wealth Collective's Retirement Roadmap is built to support.

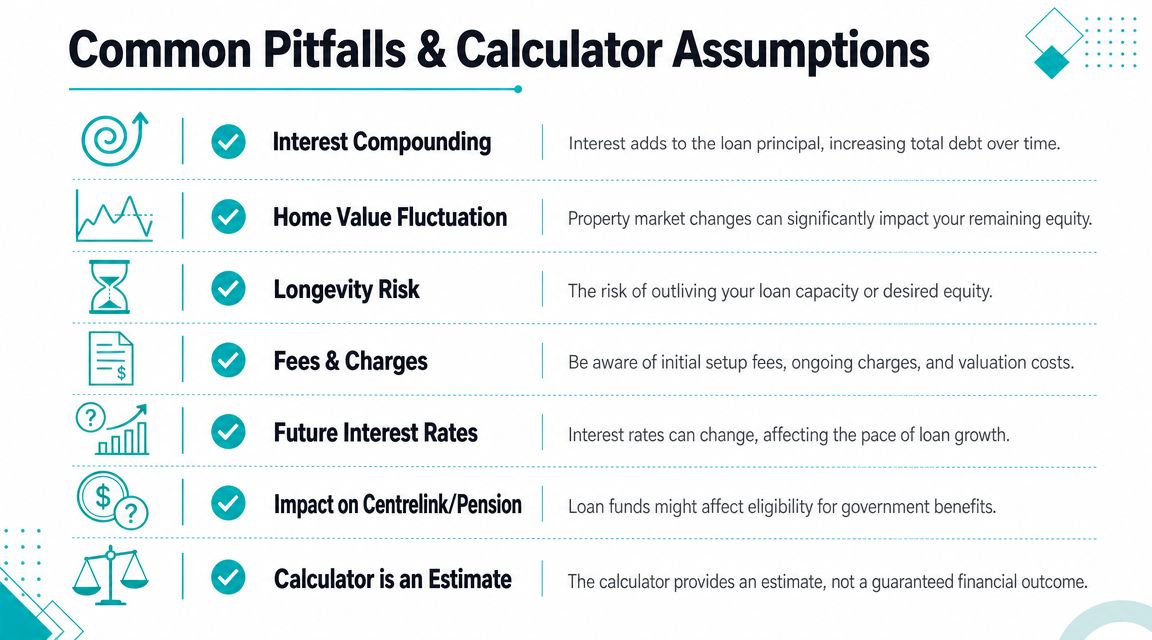

Common Pitfalls and Calculator Assumptions

Most reverse mortgage mistakes don't begin with bad intentions. They begin with assumptions that feel harmless. A user chooses a friendly property growth estimate, overlooks fees, or focuses on today's cash benefit instead of tomorrow's reduced flexibility.

That's why a reverse mortgage calculator should be used as a challenge tool. Its job isn't to confirm the best-case story in your head. Its job is to test whether the plan still holds together when conditions are less generous.

The assumptions that deserve the most scrutiny

A few risks come up again and again:

- Compounding interest: the balance doesn't just rise. Future interest is charged on prior interest as well.

- Property growth optimism: a strong estimate can make remaining equity look safer than it may be.

- Longer-than-expected time in the home: a plan that seems fine over a shorter period can look very different over a longer retirement.

- Fees and charges: even modest ongoing costs can shift the long-run picture.

- Changing rates: if borrowing costs rise, the debt path can steepen.

These are not edge cases. They are normal planning realities.

Stress-testing the downside

One of the most useful features in the Australian planning context is downside testing. Guidance on reverse mortgage calculators notes that ASIC's calculator includes scenario testing for 0% property growth and +2% interest-rate shocks, which helps advisers stress-test downside cases, especially where local property-price paths can vary materially, as described in this reverse mortgage calculator discussion from Seniors First.

That means you don't have to guess how to pressure test the result. You can deliberately ask tougher questions.

For example:

- What if the home doesn't grow in value for a long period?

- What if rates are higher than today's assumption?

- What if you need the loan to remain in place longer than planned?

A strategy that survives these tests is usually more trustworthy than one that only looks good in a smooth scenario.

Reality check: the calculator shows a model. Your retirement will not follow a model exactly.

What the no negative equity protection does and doesn't do

Many borrowers take comfort from the No Negative Equity Guarantee. That protection matters, because it means the amount owing on the loan won't exceed the value of the home when it is sold.

But people sometimes give it too much weight. It protects against ending up with a debt bigger than the sale value. It doesn't protect the amount of equity you hoped to keep. It doesn't guarantee a preferred inheritance outcome. It doesn't remove the impact of compounding.

That's why stress-testing matters more than reassurance language. A key planning question isn't just whether the debt can be repaid. It's whether the strategy still supports the life you want later on.

Navigating Regulations and Centrelink Rules

A reverse mortgage sits inside a regulated framework, and those protections matter. They help borrowers stay grounded in what the loan can and can't do.

Two ideas are especially important. First, borrowers generally retain the right to live in the home, provided loan conditions are met. Second, the no negative equity protection limits the debt outcome at the point of sale. Those protections reduce some legal and product risk, but they don't remove planning risk.

Consumer protection is not the same as strategic suitability

Retirees often get caught. They hear that the product has safeguards and conclude that it must therefore be suitable if they qualify. That's too big a leap.

A regulated loan can still be poorly matched to your goals. If the drawdown is too large, if the funds are used inefficiently, or if the plan weakens future flexibility, the issue isn't regulation. It's strategy.

That's also why Centrelink needs attention early, not as an afterthought.

Why the Age Pension question matters

How reverse-mortgage proceeds affect your pension position depends on how the money is received, held, and used. In practice, that means the impact can vary from one household to another.

If you're checking broader Australian Age Pension eligibility, it helps to understand the assets and income framework before you commit to any equity-release strategy. A reverse mortgage may interact differently with your position depending on whether funds remain in the bank, are spent on exempt purposes, or change your assessable assets.

For a more focused starting point, a dedicated Age Pension eligibility calculator can help frame the right questions before you seek personal advice.

Questions worth asking before you proceed

Rather than chasing one universal rule, ask these practical questions:

- Will the money sit in cash for a period? That can matter for means testing.

- Will it be spent quickly on home costs or debt reduction? The treatment may differ from funds that remain as assessable financial assets.

- Could the strategy change pension entitlements over time? What looks neutral at the start may not stay neutral.

The key point is simple. Reverse mortgage proceeds are not just loan proceeds. In retirement planning, they can also shape your broader benefit position. That's why a calculator result should always be read alongside pension, estate, and longevity considerations.

From Calculator to Confidence Your Next Step

A calculator can clarify the mechanics. It can show how debt may grow, how equity may change, and how different assumptions lead to different futures. That's useful. It's just not the same as a retirement plan.

Good retirement decisions sit at the intersection of numbers and judgement. You're not only weighing loan size. You're weighing lifestyle, future care options, family priorities, housing intentions, and your tolerance for uncertainty. A calculator can't balance those trade-offs for you.

What confidence actually looks like

Real confidence usually comes from being able to answer a short set of hard questions:

- Do I know why I'm using home equity, and for what purpose?

- Have I tested a conservative scenario, not just a comfortable one?

- Will this still leave me with options later in retirement?

- Have I looked at pension and estate impacts, not just borrowing capacity?

If any of those answers feel vague, that's normal. It doesn't mean the idea is wrong. It means the decision deserves proper modelling and personal advice.

Turning a calculator result into a plan

That's the point where structured retirement advice becomes valuable. The calculator gives you a starting map. Advice helps you decide whether the route suits your destination.

If you want to move from rough estimates to a clearer retirement strategy, professional financial advice for retirement planning can help connect the calculator result to the bigger picture, including cashflow design, pension interactions, and long-term equity preservation.

A reverse mortgage may be appropriate. It may also turn out that another income or capital strategy fits better. The important thing is that the decision is made with your full retirement picture in view, not just one projected number on a screen.

If you'd like help turning your calculator result into a practical retirement strategy, Wealth Collective offers a clear next step. Their Retirement Roadmap process is designed for Australians who want to understand cashflow, home equity, pension considerations, and long-term trade-offs before making a major retirement decision. You can book a complimentary 10-minute introductory call to talk through your situation and decide whether more detailed advice would be worthwhile.