Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Rent is often the biggest line item in the household budget. If you work in health, charity, or another concessionally taxed sector, you may have looked at your pay slip and wondered whether there's a smarter way to fund that cost without cutting back elsewhere.

That's where salary packaging rent comes in. It isn't a loophole, and it isn't available to everyone. For the right employee with the right employer setup, it can be a practical tax strategy that changes how part of your income is treated before tax is calculated.

The confusion starts because many Australians hear the phrase and assume it applies broadly. In reality, eligibility is narrow, the rules matter, and the value depends on your employer, your cap, and the way your package is administered. If you're in WA and trying to build momentum financially, that distinction matters. Rent savings can support bigger goals such as debt reduction, super contributions, or a cleaner monthly cash flow. If you're also thinking about the broader picture, Velzee's wealth guide is a useful read on building strong financial habits early.

Is Salary Packaging a Hidden Gem in Your Pay Slip

A Perth nurse opens her payslip, checks her rent due date, and sees the same pattern every fortnight. Income comes in, tax comes out, rent gets paid, and there's less left than expected. She's not looking for a gimmick. She's looking for a smarter structure.

That's the appeal of salary packaging rent. For some employees, rent can be paid as part of an approved salary packaging arrangement, which means an eligible expense is funded from pre-tax income rather than only from after-tax cash salary. The result can be a lower taxable income and stronger take-home pay if the arrangement is set up correctly.

Why people get stuck on this topic

The concept of paying rent is generally clear; it's the associated tax language that causes bewilderment. Terms like salary sacrifice, fringe benefits, concessional caps, and eligible living expenses can make a straightforward concept feel harder than it is.

The practical question is simpler than the jargon suggests. Can your employer let you direct part of your pay toward rent in a tax-effective way?

Practical rule: If your employer can't offer salary packaging under the relevant rules, the strategy usually stops there.

That's why this topic connects closely with broader planning decisions. If you're weighing rent packaging against other tax moves, salary sacrifice to super explained by Wealth Collective helps clarify how different pre-tax strategies work and where each one fits.

What a good decision looks like

A good decision here isn't “package everything you can”. It's knowing:

- Whether you're eligible under your employer's category

- Whether your rent qualifies under the arrangement offered

- Whether the benefit is worth it after any fees and flow-on effects

- Whether it fits your wider plan for debt, super, investing, and retirement

That last point matters more than is commonly understood. A tax strategy should support your life, not just make a payslip look clever.

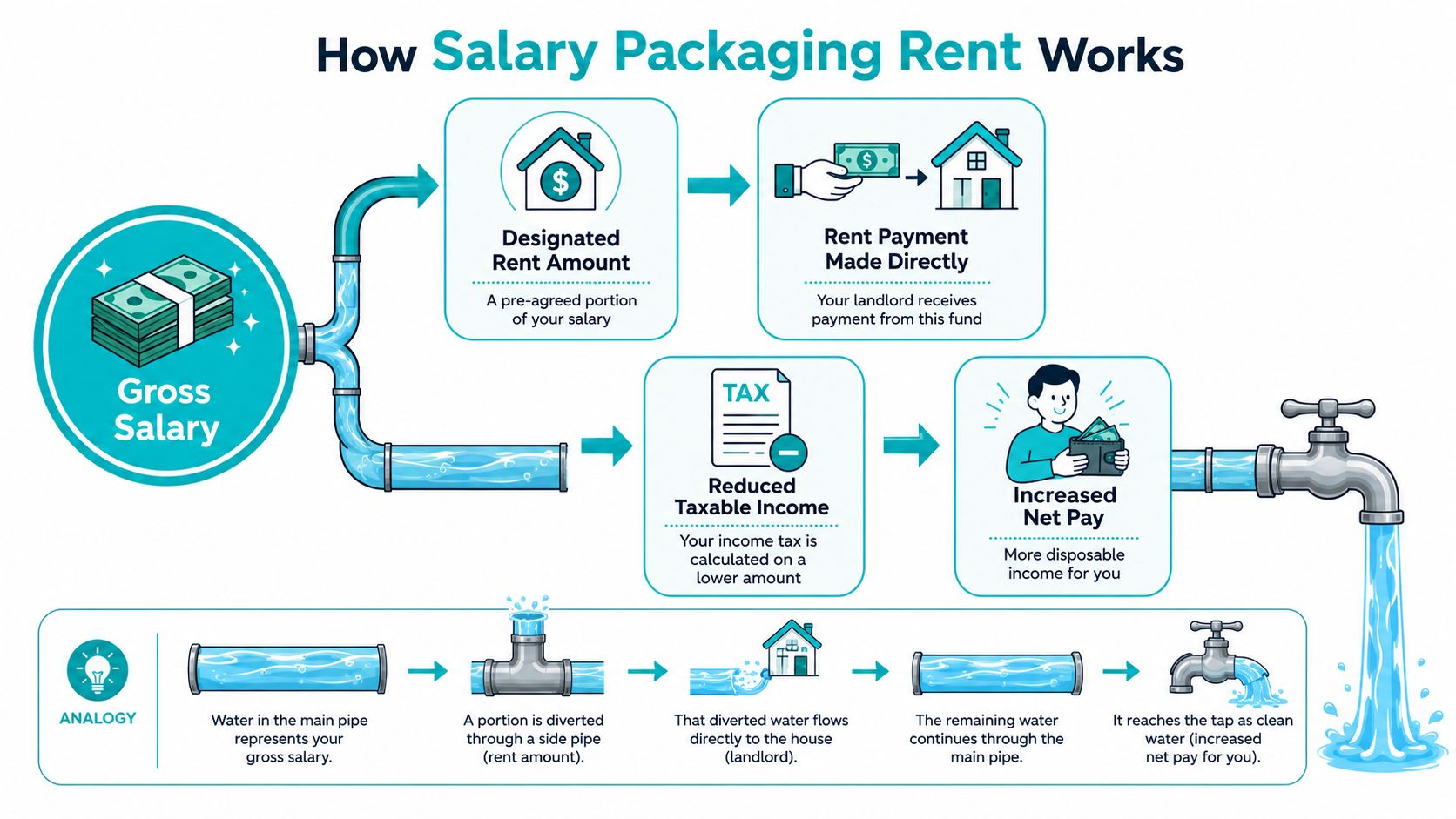

How Salary Packaging Rent Actually Works

The easiest way to understand salary packaging rent is to think of your pay as going into two buckets. One bucket is your ordinary cash salary. The other is a pre-tax bucket your employer uses for approved benefits.

If rent is an eligible benefit in your arrangement, you agree to give up part of your future salary, and your employer directs that amount toward the approved rent expense. Tax is then calculated on the reduced cash salary rather than the full amount.

The basic mechanism

Here's the simple version:

- You make an agreement with your employer before the relevant work is performed.

- A portion of your salary is redirected toward an approved benefit.

- Your rent expense is paid or reimbursed under the packaging arrangement.

- Your taxable income is lower than it would have been if you had taken the same amount entirely as cash salary.

According to Moneysmart's salary packaging guidance, the arrangement must be agreed before work is performed, and expenses paid through ordinary payroll deductions aren't treated as salary sacrifice. That same guidance explains the core tax effect: part of your remuneration shifts from post-tax cash salary to a pre-tax fringe benefit, which can reduce taxable income and PAYG withholding.

A few terms worth translating

Some of the jargon sounds more intimidating than it is:

- Salary sacrifice means you agree to receive less future cash salary in return for a benefit.

- Pre-tax income means the amount is dealt with before income tax is applied to your cash salary.

- Fringe benefit is the tax category used for certain non-cash or employer-provided benefits.

- FBT stands for Fringe Benefits Tax. Whether and how it affects the outcome depends on employer type and the benefit structure.

If you want a plain-English primer on the tax side of fringe benefits, Ashfield accountant FBT guidance can help you understand the language you'll see in provider documents.

Salary packaging rent only works when the paperwork, timing, and employer arrangement line up. You can't usually recreate the outcome after you've already earned the salary.

What this is not

It isn't an informal deal where you tell payroll to take rent out of your net wages. It also isn't a universal employee perk.

A proper arrangement sits within employer policy and tax rules. That's why two people with the same rent can get very different results depending on where they work and how their package is set up.

Who Qualifies for This Powerful Benefit

This is the point many readers need first. Salary packaging rent is not a standard benefit across the whole Australian workforce. It's mainly relevant where the employer has access to concessional treatment under the fringe benefits rules.

The strongest fit is usually employees in sectors such as not-for-profits, hospitals, and ambulance services. In those settings, the structure can be meaningful because the employer category allows a more favourable packaging framework.

The groups most likely to be eligible

For many eligible workers, rent can be treated as a living expenses benefit when the property is their principal residence and the lease is in their name or held jointly. Maxxia's rent salary packaging guide notes that many not-for-profit workers have a cap of $15,900 for general living expenses, while public hospital and ambulance employees are typically capped at $9,010.

That single distinction explains a lot. If you work for an ordinary private-sector employer, salary packaging may exist in some form, but rent packaging usually won't be the broad tax-saving opportunity people expect.

What to check before assuming you qualify

A useful way to test your position is to work through these questions:

- Employer type: Are you employed by a not-for-profit, public hospital, ambulance service, or another employer with relevant concessions?

- Benefit design: Does your employer's packaging provider allow rent as an eligible living expense?

- Lease setup: Is the home your principal residence, and is the lease in your name or jointly held where required?

- Employment terms: Does your contract, award, or industrial arrangement allow the sacrifice?

Key question: Don't ask only “Can I package rent?” Ask “Can my employer legally and administratively offer rent packaging in my role?”

Who usually won't get much value from it

Some workers hear about salary packaging rent from a friend in health or charity and assume they can do the same thing. Often they can't.

That doesn't mean there are no tax-planning options. It means this specific strategy is concentrated in employer categories where the concession structure supports it. For everyone else, the conversation usually shifts to different forms of salary sacrifice, super planning, debt management, or investment strategy.

A Worked Example of Salary Packaging Rent

The clearest way to judge salary packaging rent is to stop thinking in slogans and start thinking in mechanics.

Take Chloe, a social worker in Perth employed by an eligible not-for-profit. Her rent is a genuine monthly expense, her lease is set up correctly, and her employer offers salary packaging for living expenses. She wants to know one thing: what changes if she uses the arrangement?

Chloe without packaging

Without salary packaging, Chloe receives her full salary as ordinary taxable income. She pays tax through PAYG withholding, then pays rent from what's left in her bank account.

That's the standard pattern most employees know. Tax is calculated first. Living costs are paid second.

Chloe with rent packaging

Now assume Chloe directs eligible rent expenses into her salary packaging arrangement, up to the living-expense cap commonly used in many not-for-profit settings. William Buck's guide to salary packaging notes that many hospitals have a tax-free cap of $9,010 per year and many not-for-profit organisations have a cap of $15,900 per year, with rent or mortgage repayments included in some arrangements.

That doesn't mean Chloe gets free rent. It means part of her remuneration is being applied differently for tax purposes.

Here is the before-and-after logic.

| Metric | Without Salary Packaging | With Salary Packaging |

|---|---|---|

| Salary received from employer | Full salary paid as ordinary taxable cash salary | Part of salary redirected into approved rent packaging arrangement |

| Rent funding | Paid from after-tax income | Eligible rent paid or reimbursed through pre-tax packaging arrangement |

| Taxable income | Higher | Lower |

| PAYG withholding | Higher | Lower |

| Cash flow effect | Less room after rent is paid | More room if the arrangement delivers a net tax benefit |

Why the table doesn't show invented tax numbers

A lot of online examples go wrong here. They plug in assumed tax rates, guessed provider fees, or made-up “you save” figures and present them as fact. That's risky because the outcome depends on details such as:

- Your employer category

- The cap available to you

- Whether FBT concessions apply

- Any administration fees

- Your broader financial position

That's why the more useful question isn't “How much can I package in theory?” It's “How much of my eligible rent changes my result in practice?” If you want to compare this with other ways to structure your pay and tax position, this guide to reducing taxable income in Australia gives useful context around where salary packaging sits among other options.

A worked example should help you ask better questions, not push you into copying someone else's setup.

What Chloe should ask payroll or the provider

Before signing anything, Chloe should ask for a written breakdown covering:

- Eligible rent rules for her lease and residence

- Cap treatment for her employer category

- Any provider or administration fees

- How reimbursements or payments are processed

- What happens if she changes employers or moves house

That conversation often matters more than the headline promise of “more take-home pay”.

The Pros Cons and Important Alternatives

Salary packaging rent can be useful. It can also be oversold.

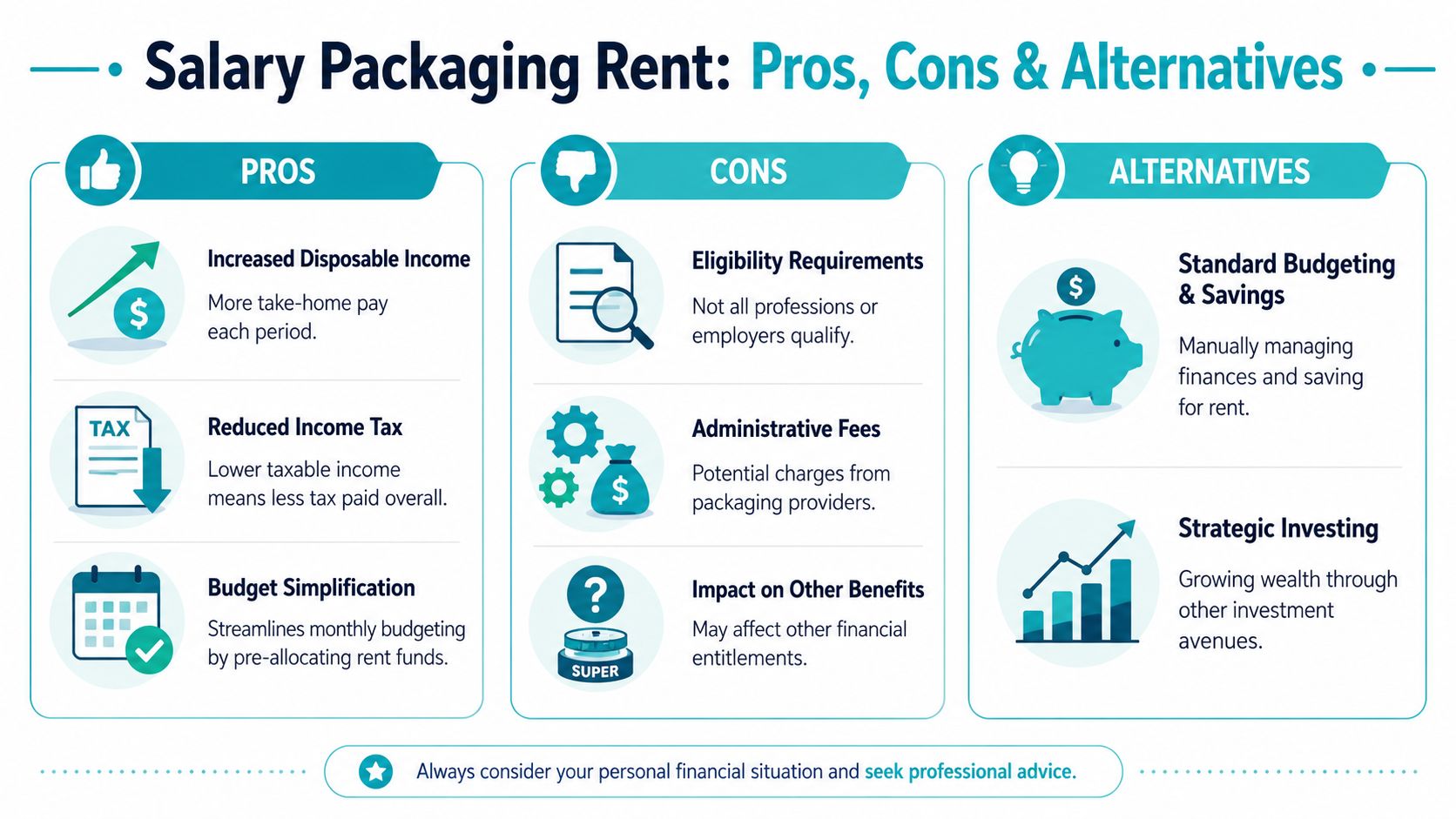

The upside is straightforward. If you're eligible and the arrangement is efficient, paying rent through pre-tax packaging can improve disposable income and reduce tax paid through normal salary treatment. It can also make budgeting cleaner because a major expense is handled through a structured payroll process.

Where the real-world ceiling shows up

The value isn't unlimited. MYOB's not-for-profit salary packaging overview makes the key point well: the practical value depends on your sector and cap structure, such as the $15,900 living-expense cap in many not-for-profit settings. In other words, the practical question is how much the arrangement changes your taxable income after FBT considerations and fees, not just whether rent is technically packageable.

That's where many people overestimate the benefit. Once you hit your effective ceiling, extra rent doesn't automatically create extra tax value.

Pros and drawbacks side by side

A balanced view looks like this:

- Cash-flow upside: An eligible arrangement can leave more room in your regular budget.

- Tax treatment: Part of your remuneration may be treated more favourably than ordinary salary.

- Administrative simplicity: Some people like having rent handled within a formal payroll-linked process.

Then the less obvious side:

- Narrow eligibility: Many employees won't have access.

- Fees and administration: Packaging providers may charge fees, which reduce the net benefit.

- Flow-on effects: It may affect items tied to your broader income position, such as lending assessments or other entitlements.

If you're already comparing this against sacrificing to super or other package structures, this overview of the disadvantages of salary sacrifice is worth reading before you commit.

The smartest comparison isn't “packaging versus doing nothing”. It's “packaging versus the next best use of that same cash flow”.

Alternatives worth considering

For some households, another strategy may be a better fit:

- Extra super contributions can suit long-term retirement planning.

- Standard budgeting and debt reduction may create more flexibility if your rent or work situation changes often.

- Broader advice planning can help if rent packaging is only one piece of a larger tax and wealth puzzle.

Your Next Steps with Wealth Collective

What's needed regarding salary packaging rent isn't more hype, but clarity.

If you're eligible, this strategy can be worthwhile. If you're not eligible, or if the administration costs and side effects outweigh the upside, it can become a distraction. The challenge isn't understanding the headline. It's testing whether it works in your actual situation.

What a practical review should cover

A proper review usually looks at:

- Your employer category and available caps

- Your lease and living-expense eligibility

- Any provider fees or payroll constraints

- How the arrangement interacts with your broader goals

- Whether another strategy would do the job better

For clients who want help turning tax concepts into an actual plan, Wealth Collective offers advice across super, tax-aware structuring, debt reduction, and retirement planning through its Guided Growth service pillar. That can be useful when salary packaging rent is only one moving part in a wider financial plan.

A sensible first move

You don't need to arrive with every answer. You do need the right questions.

Bring your pay slip, your package summary if you have one, and details of your lease. Then ask whether the arrangement improves your position once the fine print is considered. A short introductory conversation is often enough to tell whether this is a strategy worth pursuing further.

Frequently Asked Questions About Salary Packaging

Some of the most important questions show up after you understand the basics. These are usually the practical issues that affect whether salary packaging rent will work for you.

Is remote area rent the same as ordinary salary packaging rent

No. It's a separate category with different rules.

SalPac's remote area benefit overview explains that remote area rent benefits are distinct from general salary packaging. To qualify, you must live and work in an ATO-designated remote area, your employer must agree, and the benefit may cover up to 50% of rent rather than sitting inside a general living-expense arrangement.

That matters because some people search for salary packaging rent expecting a broad option, when their eligibility may depend entirely on remote-area rules.

Can I package rent if I share a lease

It may be possible, but the lease and occupancy details need to line up with the provider's requirements. The key issue is usually whether the property is your principal residence and whether your name appears on the lease in the required way.

Ask for the provider's document checklist before assuming shared housing will qualify.

What happens if I change jobs

A packaging arrangement is usually tied to the employer offering it. If you move to a new role, the new employer may not offer the same benefit, the same cap, or the same provider process.

That's why job changes can interrupt the strategy. Before switching roles, check whether the benefit continues, ends, or needs to be re-established from scratch.

Are administration fees a deal-breaker

Not always. But they do matter.

Some arrangements still stack up well after fees. Others don't. The important step is to ask for the net effect rather than the headline feature. If the provider can't explain the practical after-fee result clearly, that's a warning sign.

Can I just ask payroll to deduct rent from my salary

Not in the way many people assume. Ordinary payroll deductions aren't automatically salary sacrifice. The arrangement has to meet the formal requirements and be set up correctly in advance.

What should I gather before speaking to an adviser

Bring these items if you can:

- Your latest payslip

- Your salary packaging summary

- Your lease agreement

- Any provider forms or fee schedules

- A list of your financial goals, especially if tax savings are meant to support debt, super, or retirement planning

If you want help working out whether salary packaging rent improves your position, Wealth Collective can help you review the numbers, the rules, and the alternatives so you can make a confident decision.