Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You open your payslip, glance at your super balance, and feel that familiar tension. You're earning well enough. You're contributing something. But you still can't tell whether your super is on track for the retirement you want.

That uncertainty is exactly why a salary sacrifice super calculator matters.

Used properly, it gives you a clean first look at one of the simplest ways to build retirement wealth more efficiently. But a calculator is only useful if you understand what it's showing you, what it ignores, and where the traps sit. This often leads to errors: either the tool is never used, or it is trusted too much.

Is Your Super Working Hard Enough for Your Retirement

For a lot of Australians, retirement planning feels vague until it suddenly doesn't. One day you're focused on mortgage repayments, school fees, or getting ahead in your career. Then you realise the years are moving quickly and your super balance will need to carry a lot more weight later on.

That's where salary sacrificing earns serious attention. It gives you a way to direct part of your income into super before income tax is taken out, which can make your money work harder inside a lower-tax environment. For people who want to grow wealth with more intention, that's not a minor tweak. It's a meaningful lever.

Still, the strategy confuses plenty of people. They're not sure how much they can contribute, whether it affects take-home pay too heavily, or whether they're stepping into a tax problem by accident.

Why this matters now

You don't need to be close to retirement to care about this. Young professionals use salary sacrifice to build momentum earlier. Dual-income households use it to improve tax efficiency. Pre-retirees use it to sharpen their final working years and get more deliberate about what their income is doing.

A good Salary Sacrifice Super Calculator helps answer the first practical question: “If I redirect some salary into super, what happens to my pay and my tax position?”

That's the right starting point. It turns a fuzzy idea into something concrete.

Salary sacrifice isn't just about saving tax. It's about deciding that part of your income should serve your future self instead of disappearing into day-to-day spending.

The real value of the calculator

A calculator gives you visibility. It can show the likely impact on your cash flow and highlight whether the strategy seems manageable. That alone helps people move from indecision to action.

But calculators don't create strategy. They don't know your broader goals, your other assets, your timing, or whether this move fits with the rest of your financial life. Treat the tool as the first checkpoint, not the final answer.

What Exactly Is Salary Sacrificing to Super

Salary sacrifice is a formal arrangement with your employer. You agree that part of your pre-tax salary will go straight into your super fund instead of landing in your bank account as regular pay.

The easiest way to think about it is a river.

Your gross salary is the full river flow. Before all of it reaches the sea, you open a gate and divert part of that water into a reservoir. That reservoir is your super fund. Because the diversion happens before income tax is worked out on that part of your pay, your taxable income is reduced.

What happens mechanically

The process is simple:

- You nominate an amount with your employer.

- Payroll sends that amount into your super fund from your pre-tax salary.

- The remaining salary continues through payroll and is taxed in the usual way.

- Your take-home pay is lower than it would have been otherwise, but more money is being channelled into super.

The Australian Taxation Office treats salary sacrifice amounts as employer super contributions, which means they're in addition to the government's mandatory Super Guarantee and they aren't counted as assessable income for PAYG withholding tax purposes, as outlined in the ATO's guidance on salary sacrificing super.

What it isn't

Here, people often mix things up.

Salary sacrifice is not the same as adding after-tax money to super from your bank account. The Australian Retirement Trust makes that distinction clearly in its explanation of salary sacrifice contributions. One happens before tax is deducted from your pay. The other happens after you've already received and paid tax on the income.

That difference matters because the tax treatment is different, the planning considerations are different, and the impact on your cash flow is different.

Simple test: If the money never hits your bank account and goes from payroll into super, it's salary sacrifice.

Why people choose it

Individuals use salary sacrifice for one of three reasons:

- Tax efficiency: They want more of their income directed into a lower-tax structure.

- Forced discipline: They know they'll invest more consistently if it's automated through payroll.

- Retirement focus: They want to close the gap between their current super balance and their target lifestyle later on.

It's straightforward in concept. The complications start when contribution caps, payroll timing, and long-term strategy enter the picture.

Tax Benefits and Contribution Rules You Must Know

A calculator can show a tax saving. It cannot tell you whether the strategy is set correctly.

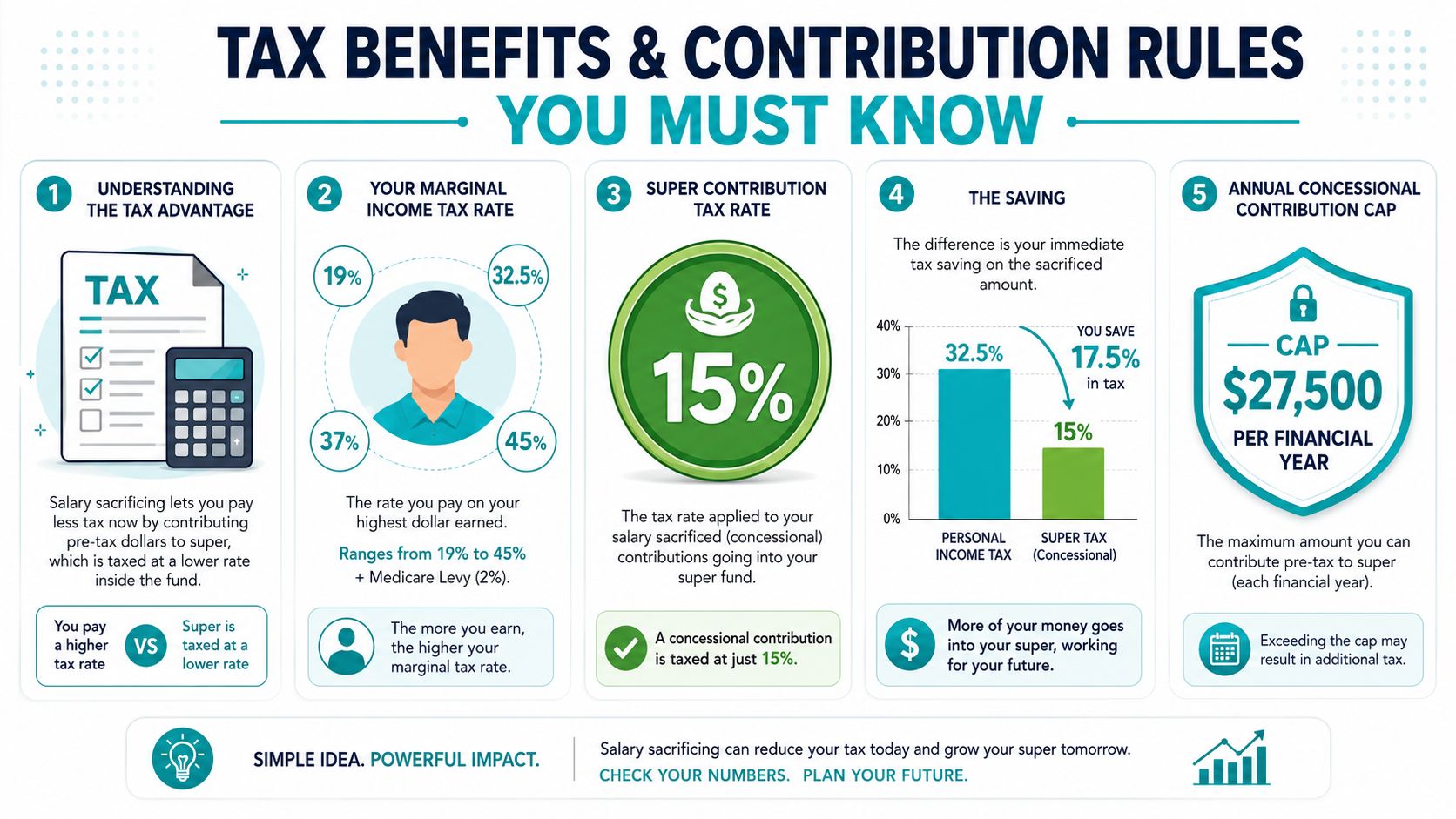

The tax benefit is real. Salary sacrifice contributions are concessional contributions, which are generally taxed at 15% inside your super fund, as the ATO explains. If your marginal tax rate is higher than that, directing part of your pre-tax salary into super can leave more of that money invested for retirement instead of lost to personal income tax.

Where the tax advantage comes from

The comparison is straightforward. Income paid to you as salary is taxed at your marginal rate. Income redirected into super through salary sacrifice is generally taxed at the concessional super rate instead.

That gap is the whole reason this strategy works.

It also explains why salary sacrifice tends to suit professionals on higher incomes, people with stable cash flow, and employees who want a disciplined way to build retirement savings without relying on willpower each month. Done properly, the same earnings can buy you more retirement capital.

The cap matters more than the tax rate

This is the rule that catches people.

For the 2025–26 financial year, the concessional contributions cap is $30,000, according to the ATO concessional contributions cap rules. That cap covers all concessional contributions for the year, including your employer's Super Guarantee contributions and any salary sacrifice amounts.

Many employees look at the cap and assume they can salary sacrifice the full amount. They can't. Your employer is already using part of that space through compulsory super contributions. The result is simple. Your available room is smaller than it looks on paper.

What you should check before setting an amount

Set your salary sacrifice amount after you check these three points:

- Your remaining cap space: Start with the annual concessional cap, then subtract expected employer contributions for the year.

- Your pay cycle and payroll timing: Late June contributions can be received in July, which can shift which financial year counts them.

- Your actual household cash flow: A tax benefit is not enough reason to squeeze your budget.

If you run a business or have uneven income, clean records matter. Many clients reviewing contribution strategies also compare Australian accounting software so payroll, super payments, and cash flow are easier to track accurately.

Practical rule: Check your employer contributions first, then choose your salary sacrifice amount.

The planning opportunity many calculators miss

A basic calculator usually tests one year in isolation. Real advice goes further.

Unused concessional cap amounts from earlier years may create extra contribution opportunities if you qualify. That rule can materially change how much you contribute and when. If you want to understand that strategy properly, start with our guide to carry-forward concessional contribution rules and timing.

This is why the calculator is only the first step. It gives you a starting number. An adviser helps you decide whether that number fits your tax position, your contribution limits, and your long-term retirement plan.

How a Salary Sacrifice Super Calculator Works

Before even opening it, the calculator is often overcomplicated. It's often mistaken for some advanced tax engine. Usually, it isn't. A salary sacrifice super calculator is just a model that compares two scenarios: your pay without salary sacrifice, and your pay with it.

That's it.

The main inputs

Most calculators ask for a small set of details. Common inputs include:

- Gross annual salary: Your income before tax.

- Pay frequency: Weekly, fortnightly or monthly pay.

- Salary sacrifice amount: The amount you want to redirect into super.

- Existing employer contributions: Some calculators allow for this, some don't.

- Financial year settings: Better tools reflect the current contribution cap and related rules.

The quality of the result depends entirely on the quality of the inputs. If your salary changes during the year, if you receive bonuses, or if your employer contribution pattern isn't consistent, a basic calculator can give you a false sense of precision.

What the calculator is doing behind the scenes

The process is usually straightforward:

- It models your pay as normal employment income.

- It subtracts the proposed salary sacrifice amount from taxable salary.

- It estimates your revised take-home pay.

- It shows the amount directed into super.

- It compares the tax outcome between both scenarios.

The good calculators are useful because they turn theory into a weekly, fortnightly or monthly number you can feel. That's what makes the decision practical. You stop asking, “Should I salary sacrifice?” and start asking, “Can I comfortably live on this adjusted pay?”

A calculator is most helpful when it changes a vague intention into a decision you can actually implement through payroll.

What the outputs really mean

When you see the results, focus on three outputs:

- Reduced take-home pay: This tells you the lifestyle cost of the strategy right now.

- Extra super contribution: This tells you how much more is going into retirement savings.

- Estimated tax saving: This shows the immediate structural benefit of redirecting part of your income.

Don't treat the output as a promise. Treat it as a planning estimate.

Where calculators usually fall short

Most calculators are static. Your life isn't.

They often assume stable salary, smooth payroll processing, and simple contribution patterns. They usually don't account for job changes, income fluctuations, missed payroll runs, or more advanced super strategies. They're excellent for testing a first move. They're weak at building a full retirement contribution plan.

That's why the smartest way to use a salary sacrifice super calculator is as a decision aid, not as your entire strategy.

Seeing the Impact Real World Salary Sacrifice Examples

You run the calculator, trim your take-home pay by a manageable amount, and see your super contributions rise. That is useful. It is not the decision. The decision is choosing an amount that fits your cash flow, stays inside the cap, and supports your broader plan.

Two people can look at the same calculator and need completely different advice.

Chloe is in her mid-career. She wants to build retirement savings without squeezing her budget so hard that she quits the strategy after a few pay cycles. David is closer to retirement. He has less time for trial and error, so every contribution decision needs to be tighter and more deliberate.

A practical rule applies to both. Your employer's Super Guarantee contributions already use part of your concessional cap, so your salary sacrifice amount should be calculated after those employer contributions are accounted for. A useful community explanation of that calculation appears in this AusFinance discussion on calculating salary sacrifice amounts.

Chloe wants a strategy she will actually stick with

Chloe does not need an aggressive number. She needs a sustainable one.

For her, the calculator is a filter. It helps her test whether a smaller, consistent contribution leaves enough room for mortgage repayments, holidays, school fees, or other priorities that matter right now. A plan she can maintain for years will beat a bigger contribution she cancels after one expensive quarter.

Her decision should answer three questions:

- What reduction in take-home pay feels comfortable every pay cycle?

- How much cap space is left after employer contributions?

- Does this contribution still leave room for other goals?

If Chloe wants the tax benefit without creating pressure at home, start modestly and review it after a few months. That is the right move more often than people think.

David needs precision, not enthusiasm

David is in a different position. He is not testing a habit. He is making the most of limited working years.

That means the calculator is only a starting point. He needs to check payroll timing, year-to-date employer contributions, and whether a higher contribution this year still makes sense alongside his retirement date, drawdown plans, and other assets. For someone near retirement, careless administration can do real damage. If you want a clear view of the risks and disadvantages of salary sacrifice, read that before locking anything in.

Short version: David should not set a number once and hope payroll gets it right.

What a $10,000 salary sacrifice actually changes

A simple example shows why salary sacrifice gets attention.

If $10,000 is taken as regular income, it is taxed at your marginal rate. If that same $10,000 is directed into super as a concessional contribution, it is generally taxed at the concessional contribution rate within super, assuming you remain within the relevant rules and caps. That difference can create a meaningful tax benefit, but the exact result depends on your income and contribution position.

| Metric | Without Salary Sacrifice | With Salary Sacrifice |

|---|---|---|

| Treatment of the extra $10,000 | Paid as regular income | Directed into super before tax |

| Tax outcome on that amount | Taxed at your marginal tax rate | Taxed as a concessional contribution in super |

| Take-home pay | Higher now | Lower now |

| Super balance impact | No extra contribution from this amount | Extra contribution added to super, less contribution tax |

| Planning value | More cash flow today | More retirement savings and potential tax efficiency |

This is the main point of the example. Salary sacrifice changes the trade-off between present cash flow and future wealth. It does not tell you the right number for your situation.

What these examples should tell you

Chloe and David should not use the same contribution strategy, even if they earn similar incomes.

Chloe needs a contribution level she can repeat without stress. David needs tight control over timing and totals. The calculator helps both of them get an initial answer, but it cannot judge sustainability, spot administration risk, or fit the strategy into a full retirement plan.

Use the calculator to test a first move. Then get advice before you treat that number as a strategy.

Common Pitfalls and How to Avoid Them

You set up salary sacrifice, watch your take-home pay change, and assume the rest is handled. That is where people get caught.

The calculator gives you a useful starting number. It does not protect you from cap breaches, payroll errors, reporting issues, or a contribution level that stops making sense six months later. If you want this strategy to work, treat it like an active plan, not an automatic setting.

Exceeding the concessional cap

The concessional cap is the first thing to control. Salary sacrifice contributions count toward it. Employer Super Guarantee contributions count too. If you ignore the combined total, you can tip over the limit and create an avoidable tax problem.

Use a simple checking process:

- Start with employer contributions: Work out how much of the cap is already being used before you add anything extra.

- Check year-to-date figures: Use payslips and your super fund records, not memory.

- Review after any job or pay change: A new employer, bonus, or pay rise can shift the result quickly.

- Stop relying on rough estimates: Close enough is not good enough with contribution caps.

This is one of the clearest reasons a calculator is only step one. It can model an amount. It cannot monitor your real contributions through the year.

Assuming your employer handles everything perfectly

Payroll can process instructions. You still need to check the outcome.

Salary sacrifice can go wrong through a delayed start date, the wrong deduction amount, or contributions landing later than expected. A small admin error can leave you short of your target or push you closer to the cap than you realised.

Do three things every time you set up or change an arrangement:

- Get the salary sacrifice agreement in writing.

- Check your next payslip to confirm the deduction started correctly.

- Confirm the contribution reached your super fund.

Stay on top of it. Nobody will care about the accuracy of your retirement strategy more than you do.

Forgetting the reporting side

Salary sacrifice does not disappear just because it happens before tax. It still affects your reportable income position, and that can matter when you apply for a loan, assess family benefits, or review household cash flow.

Broader planning matters. A calculator will not tell you how salary sacrifice interacts with lending capacity or other financial decisions. If you want to pressure-test the trade-offs, read our guide to the disadvantages of salary sacrifice.

If cash flow is already tight, fix that first. Many people can save from subscription leaks and free up room before they commit to a higher super contribution.

Treating salary sacrifice as a forever setting

A salary sacrifice amount should be reviewed, not forgotten.

Your income changes. Living costs change. Career plans change. What felt comfortable at the start of the financial year can become too aggressive after a mortgage increase, a new child, or a move to part-time work. The opposite is also true. Some people set the amount too low and leave tax savings on the table for years.

Review your arrangement regularly and adjust it with intent. The right number is the one you can sustain, keep within the rules, and fit into your wider wealth plan. That is the difference between using a calculator and using a strategy.

Beyond the Calculator Building Your Retirement Roadmap

A salary sacrifice super calculator is a strong starting point. It can show whether the strategy has potential for you and whether the cash flow impact is realistic.

But it can't build your retirement plan.

It won't tell you how salary sacrifice fits with debt reduction, investment strategy, insurance, estate planning, retirement timing, or your partner's super position. It also won't reliably account for more advanced contribution opportunities. That limitation matters.

Where calculators stop

Existing salary sacrifice calculators consistently fail to address the nuanced impact of the bring-forward rule for concessional contributions, and they often treat the $30,000 cap as a rigid annual limit without accounting for strategic flexibility, as noted by SalarySacrificeCalc.com.au.

That's a serious gap for pre-retirees and higher-income earners. If you're making meaningful contribution decisions in the years before retirement, you need more than a generic output screen. You need judgement.

What a proper strategy looks like

A useful retirement plan pulls several moving parts into one clear framework:

- Retirement Roadmap: How your super strategy supports the income and lifestyle you want later.

- Guided Growth: How super, investments, debt reduction, and cash flow work together now.

- Ongoing adjustment: How the strategy changes when your salary, work plans, or retirement timing change.

That broader view matters because salary sacrifice should support your life, not distort it.

A lot of people who are trying to optimise their finances also find value in tightening everyday spending leaks. If you're reviewing cash flow before increasing super contributions, this guide on how to save from subscription leaks can help you free up room without feeling squeezed.

A calculator gives you a number. Advice gives you a direction.

The best next step is simple. Use the calculator to test the idea. Then speak with someone who can pressure-test the assumptions, confirm the contribution strategy, and connect it to the rest of your financial future.

If you want help turning salary sacrifice into a smarter retirement strategy, book a free, no-obligation 10-minute introductory call with Wealth Collective. Their advisers can help you cut through super complexity, understand your options clearly, and build a plan that supports your version of a wildly successful financial life.