Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You might be in one of these camps right now.

One of you is working full-time while the other is part-time, on parental leave, easing into retirement, or taking a break from paid work. You're trying to do the sensible things with money, keep the household running, build super, reduce tax where you can, and avoid strategies that feel fiddly or overhyped.

This is one of the cleaner wins available to couples. The spouse contribution tax offset won't transform your entire financial life on its own, but it's a smart move when it fits. Beyond that, it can help you build retirement savings more fairly across the household, not just in the name of the higher earner.

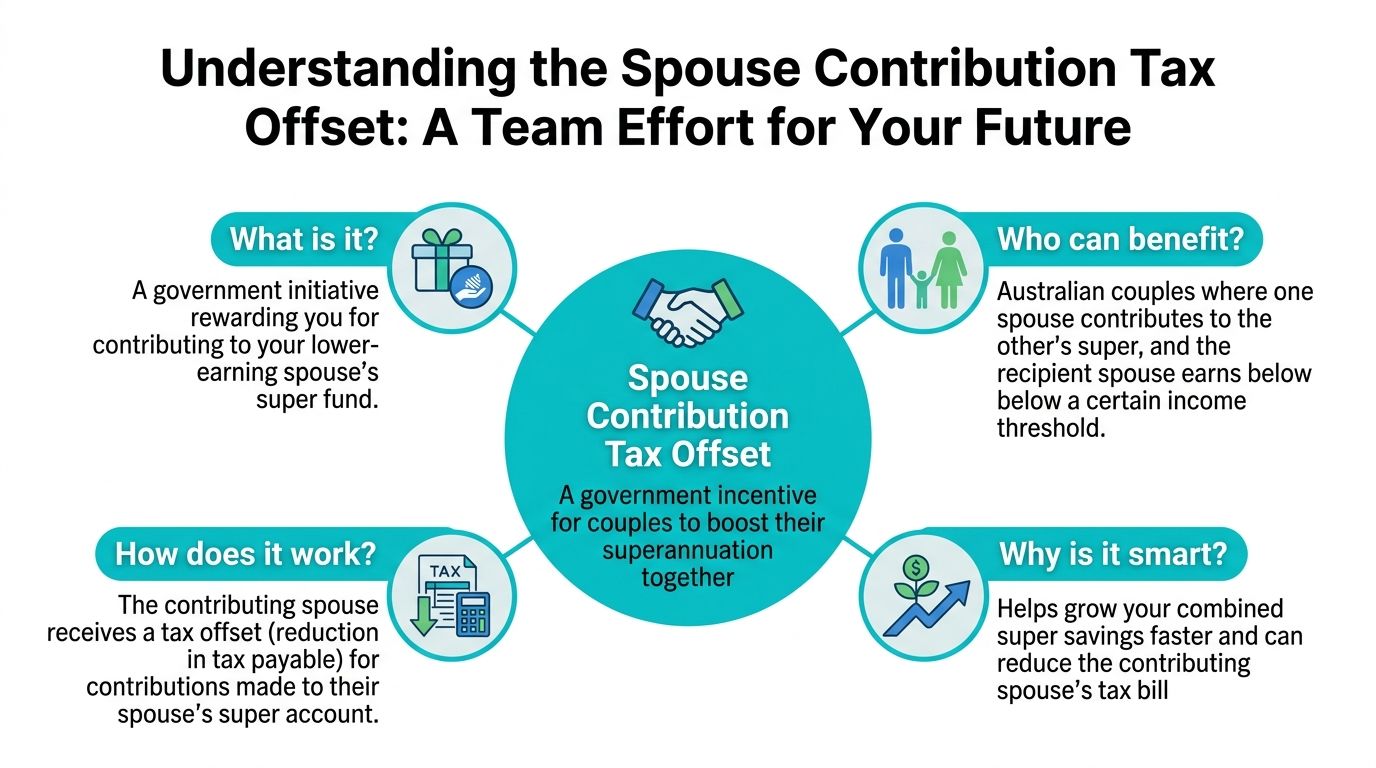

What Is the Spouse Contribution Tax Offset

One partner is earning most of the income. The other is working less, on leave, or winding back. A spouse contribution tax offset lets you turn that uneven income period into a useful family strategy by adding to your partner's super and cutting your own tax at the same time.

The rule itself is simple. If you put after-tax money into your spouse's super and they meet the ATO rules, you may be able to claim a tax offset of up to $540. The maximum offset is worked out as 18% of the first $3,000 you contribute for an eligible spouse whose income is $37,000 or less, as explained in the ATO guidance on spouse super contributions.

The three numbers that matter

- $3,000 contribution amount: Only the first $3,000 of an eligible spouse contribution counts toward the offset.

- 18% offset rate: That is the rate used to calculate the tax benefit.

- $540 maximum offset: That is the annual cap for this strategy.

Keep the math in perspective. Put in less than $3,000 and the offset is smaller. Put in more than $3,000 and this specific tax benefit does not increase.

That does not make extra contributions a bad idea. It just means you should make them for the right reason, usually to build the lower-balance spouse's retirement savings, not because you expect a bigger offset.

Why smart couples use it

The actual value is bigger than the tax saving.

In many households, one super balance pulls ahead for years because one partner earns more, stays in full-time work longer, or keeps receiving stronger employer contributions while the other takes on more unpaid family work. A spouse contribution is one of the cleanest ways to rebalance that over time.

That matters for more than fairness. It can improve how you build retirement assets as a household, especially for single-income families, pre-retirees trying to lift one weaker balance, and couples where one partner has had career breaks. Used properly, this is a family wealth-building move with a tax benefit attached.

My view is simple. If one spouse's super has fallen behind and you have spare cash flow, this strategy deserves serious attention.

If you want a plain-English refresher on how these after-tax super top-ups work, this guide on after-tax super contributions is a good starting point.

Are You and Your Spouse Eligible

A lot of couples miss this offset for a simple reason. They assume any payment into a partner's super will qualify. It won't.

Eligibility is what separates a smart family wealth move from an admin mistake. If you are using this strategy to strengthen one spouse's retirement position, especially in a single-income household, after a career break, or in the years before retirement, get the setup right before the money goes in.

Rules for the spouse receiving the contribution

Start with the receiving spouse. They need to clear every test below.

- Total super balance test: Their total super balance must be under $1.9 million as of 30 June 2024 for the 2024 to 2025 financial year, based on the LCI Partners explanation of the spouse contributions tax offset.

- Age test: They must be under 75 when the contribution is made. A fund can still accept the contribution up to 28 days after the end of the month in which they turn 75, as noted earlier.

- Contribution cap awareness: For the 2026 to 2027 financial year, the cap for after-tax contributions is $130,000. If your spouse has already used up that cap, this strategy can fail.

- TFN on file: Their tax file number must be recorded with their super fund. If it is missing, you can create problems for the contribution and the offset claim.

Rules for the spouse making the contribution

The contributing spouse has rules too, and people often make errors concerning them.

- Use after-tax money: The contribution must come from money you have already paid tax on.

- Do not claim a deduction: If you intend to claim the contribution as tax-deductible, it is not the same strategy and the spouse offset does not apply.

- The annual offset cap still applies: Even if your circumstances are unusual, the offset itself does not go beyond the annual maximum already covered earlier.

This is one piece of a broader tax planning strategy to reduce taxable income in Australia, but it only works well when it also improves the lower-balance spouse's long-term super position.

A practical yes or no filter

You are usually in good shape to consider this strategy if the answer is yes to most of these:

- One spouse has lower income for the year

- That same spouse has less super than they should

- You have spare cash flow from the household budget

- You want to build family retirement wealth, not just chase a tax outcome

- You are making an after-tax spouse contribution, not mixing it up with a deductible personal contribution

My advice is simple. If one partner's super has fallen behind, check eligibility first and then act. Done properly, this is a clean way to shift more retirement savings into the right hands while picking up a tax benefit along the way.

If anything about the balance test, age timing, or contribution type looks unclear, get advice before you transfer the money. That small check can save you from an avoidable mistake.

How the Offset Calculation and Income Thresholds Work

A couple can do everything right in principle and still miss value here by getting the numbers wrong.

The spouse contribution tax offset is simple once you strip it back. It is a non-refundable 18% tax offset on the lesser of $3,000 or the amount you contribute to your spouse's super. If you want the full result, the receiving spouse's income must stay within the lower income threshold. Aware Super's spouse contribution guide sets out the same framework.

Start with the maximum outcome

If your spouse's income is $37,000 or less, you can claim the full offset on up to $3,000 of eligible spouse contributions.

That means:

- Contribute $3,000. Claim a $540 offset.

- Contribute $1,500. Claim a $270 offset.

The rule is mechanical. You get 18 cents back for every eligible dollar, up to the cap. For families with one lower-income partner, that makes this a practical way to build the right spouse's super while trimming tax at the same time.

Then check the taper

The offset starts shrinking once your spouse's income goes above $37,000.

The reduction is direct. For every $1 of income over $37,000, the amount of contribution eligible for the offset falls by $1. Once your spouse's income reaches $40,000, the offset is gone.

That narrow range matters. A spouse on variable hours, bonus income, or irregular self-employed earnings can slip from a full offset to a partial one faster than expected.

Spouse Contribution Tax Offset Calculation 2026

| Spouse's Income | Maximum Eligible Contribution | Potential Tax Offset (18%) |

|---|---|---|

| $37,000 or less | $3,000 | $540 |

| Between $37,000 and $40,000 | Reduced by $1 for every $1 over $37,000 | Reduced proportionally |

| $40,000 | $0 | $0 |

What this means in practice

This is not a big-dollar tax strategy. It is a precise family wealth move.

For a single-income household, the numbers are usually straightforward. If one partner earns little or nothing, funding that spouse's super can improve long-term balance between both accounts and give the contributing spouse a tax offset. For pre-retirees, it can also help direct extra retirement savings toward the partner who is behind, instead of letting the wealth gap between spouses widen.

If your spouse's income is close to the cutoff, calculate first and contribute second. Guessing here is how couples overestimate the benefit.

Used properly, this fits neatly into a broader tax planning approach for lowering your assessable income in Australia, but the primary win is bigger than the tax return. You are building retirement assets across the family, not just chasing a one-year offset.

Your Step-by-Step Guide to Claiming the Offset

A lot of couples get this wrong in a very ordinary way. The money goes into super, but it is coded incorrectly, lands too late, or the tax return claim does not match what happened.

Claiming the offset is simple if you treat it like a family strategy, not a rushed June admin task.

The practical workflow

Confirm the plan before any money moves

Check that your spouse qualifies, then decide how much to contribute based on the offset you can claim. If your household cash flow runs through shared savings, this is a good time to review your joint bank account options so the contribution comes from a clear, trackable source.Ask the super fund how they want it processed

Do not guess. Contact the receiving spouse's fund and ask exactly how to make a spouse contribution, and what they need it called on their system. Some funds use a specific form number or contribution code. Ask for it by name so your payment does not end up recorded as a general personal contribution.Make the contribution early enough to be received in time

Year end timing matters. If you wait until the last few days of June, you are relying on bank processing times and the fund's internal allocation team. I tell clients to get this done well before year end. That gives you time to fix any admin issue while the window is still open.Keep proof that matches the claim

Save the confirmation, receipt, bank record, and any form you submitted. If the fund issued correspondence showing the contribution type, keep that too. Clean records make tax time easier and protect you if the contribution needs to be verified later.

Where the claim goes

You claim the offset in your tax return under “Superannuation contributions on behalf of your spouse”.

Keep the wording in your records consistent with the wording in the return. If your paperwork says one thing and your return says another, you create a problem that is easy to avoid.

It also helps to remember what this offset does. It reduces the tax you owe. It is not a separate cash payment.

Smart habits that prevent mistakes

- Check your spouse's final income position before contributing. This matters most for casual workers, contractors, and anyone with uneven earnings.

- Make sure the fund treats it as a spouse contribution. Good intentions do not fix bad coding.

- Do not leave it until the final week of June. This is the most common avoidable error.

- Match the claim to the contribution that landed. Claim what happened, not what you planned to do.

One more point. If you are using this strategy as part of a broader family wealth plan, do not treat it as a one-off tax trick. Review it each year alongside contribution caps, cash flow, and the gap between each spouse's super balance. That is where a small offset starts doing a bigger job for the household.

Strategic Scenarios for Australian Couples

Rules are useful. Strategy is better.

The spouse contribution tax offset becomes more powerful when you stop seeing it as a once-a-year tax trick and start treating it as part of how your household builds wealth together.

Pre-retirees balancing uneven super

A lot of pre-retiree couples arrive at the same point with very different super balances. One spouse may have spent more years in full-time work. The other may have taken career breaks, worked part-time, or prioritised family responsibilities.

In that situation, a spouse contribution can do two useful jobs at once. It directs money to the spouse who needs the super boost more, and it rewards the contributing spouse with a tax offset if the rules line up. That's a better use of surplus cash than leaving the lower-balance spouse permanently behind.

This isn't just about fairness. It's about optionality later. More balanced retirement assets can make planning simpler and reduce pressure on one spouse's account.

Young families protecting momentum

Parental leave is one of the most common times for retirement savings to slow down. Household income changes, cash flow tightens, and super contributions often drop for the parent who steps back from work.

That's exactly when a spouse contribution can make sense. It keeps some retirement savings momentum going during a season when one income often carries more of the load. If you're running the household jointly, this is one practical way to reflect that shared effort.

And if you're tidying up household banking while you're at it, comparing joint bank account options can help couples decide how to manage shared cash flow for recurring goals like super top-ups, emergency savings, and bills.

High-income earner with a part-time spouse

This is one of the clearest fits.

One spouse earns strongly. The other works part-time, consults casually, or earns below the full-threshold level for the offset. The household has capacity to save, and the lower-earning spouse's super is lagging.

In that case, a spouse contribution is disciplined and efficient. You're moving money to where the long-term retirement need is greater, while picking up a tax offset along the way. It won't replace larger planning strategies, but it's the sort of move financially organised couples stack year after year.

Good family wealth planning doesn't only ask who earned the money. It asks where the money should go next.

Common Mistakes and How to Avoid Them

Couples usually miss this offset for boring reasons, not strategic ones. The money goes in, but the paperwork, timing, or household planning around it falls short.

The pattern I see most often is simple. A couple hears “tax offset,” focuses on the refund, and forgets that this is still part of a broader family wealth decision. If you want this strategy to work, treat it like a planned move inside the household balance sheet, not a last-minute tax season errand.

Mistake one: treating side income and extras as if they do not count

This catches part-time workers, consultants, and spouses with salary packaging more than anyone else. The problem is not confusion about salary. The problem is forgetting about the rest of the income picture.

A spouse might look under the threshold based on wages alone, then tip over once fringe benefits, employer super amounts, or side-hustle income are included. That can reduce the offset or wipe it out altogether.

- Fix it this way: Review the receiving spouse's full income position before the contribution goes in.

- Why it matters: A strategy that looks smart in April can fail in July if you only checked the payslip.

Mistake two: making the contribution without coordinating the rest of the household plan

This offset is small. The planning mistake gets expensive when couples chase it while ignoring bigger issues such as contribution caps, account balances, cash flow pressure, or a spouse whose super already needs a different strategy.

That is why organised families review this alongside their other super moves for the year. If you want a broader framework, our guide on how to maximise superannuation helps you place spouse contributions in the right order with other opportunities.

Good advice starts with the household goal, then picks the tax strategy that supports it.

Mistake three: assuming the fund will sort out the admin

Super funds follow process. They do not guess what you meant.

If the contribution is sent through without the right form or instructions, you can create a mismatch between what happened and what you plan to claim. Then tax time becomes a clean-up job. That is avoidable.

- Fix it this way: Check the fund's spouse contribution procedure before transferring the money.

- Why it matters: Clear records make the claim straightforward and reduce the risk of disputes later.

Mistake four: leaving the decision until late June

Late June is where good tax ideas get missed. Banking delays, fund processing times, unsigned forms, and plain old family busyness get in the way.

Pre-retirees and single-income families are especially prone to this because they are often juggling multiple year-end decisions at once. Set the amount earlier, move the money earlier, and keep proof of the contribution.

Mistake five: chasing the offset while ignoring the bigger tax picture

A household can do this correctly and still make poor overall decisions. If cash flow is tight, debt is expensive, or another strategy deserves priority, forcing a spouse contribution just to get an offset is not smart planning.

Sometimes the better move is to sort the larger tax and cash flow questions first. If property debt is part of that discussion, the Beshay Realty home loan tax guide is a useful plain-English reference for understanding what does and does not help on the home loan side.

The best couples use this offset as one small, disciplined move inside a bigger plan. That is how a modest tax rule starts doing real work for long-term family wealth.

Integrating This Strategy Into Your Wealth Plan

The spouse contribution tax offset is useful. It's also small in the context of an entire financial life.

That's not a criticism. It's a reminder to use it properly.

A tax offset is not a financial plan

A good household strategy coordinates cash flow, debt, super, investing, insurance, and retirement timing. The spouse contribution tax offset can support that plan, especially when one partner's retirement savings need attention, but it shouldn't sit in a vacuum.

For example, some couples should prioritise debt reduction before adding extra super. Others are better served by combining super contributions with broader investment planning. Homeowners may also need to understand where tax deductions do and don't apply in the property space, and this home loan tax guide offers a useful plain-English summary for that part of the picture.

Where this fits for different households

This strategy often works best when it supports one of these broader goals:

- Balancing retirement assets: One spouse's super is materially behind and needs attention.

- Maintaining momentum through life changes: Career breaks, part-time work, or parental leave have interrupted one partner's retirement savings.

- Making surplus cash work harder: You've already stabilised the essentials and want another legitimate, targeted move.

- Tidying up the household strategy: You want your tax decisions and super decisions to pull in the same direction.

The bigger question to ask

Don't ask only, “Can we get the offset?”

Ask, “Is this the best next use of our money given everything else we're trying to achieve?”

That's the right question for couples who want to build wealth deliberately. Sometimes the answer is yes. Sometimes the answer is yes, but only after you restructure cash flow or coordinate it with other super strategies. If you're exploring the broader super side of that equation, this guide on how to maximise superannuation is a solid next read.

A well-run advice process does exactly that. It puts the spouse contribution tax offset in context, tests whether it fits, and combines it with the rest of the decisions that shape your future.

If you want clarity on whether the spouse contribution tax offset fits your situation, Wealth Collective can help you cut through the noise and build a coordinated plan. Their advisers work with young families, professionals, pre-retirees and retirees to turn tax, super and retirement decisions into practical action. Book a complimentary 10-minute chat and see how a personalized plan can help you create your own wildly successful financial life.