Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You’ve probably reached the point where holding assets in your own name no longer feels smart.

Maybe you run a profitable business in Perth. Maybe you and your partner have built a strong income, bought property, built an investment portfolio, and now you’re thinking about tax, risk, and what happens if one of you gets sued, dies unexpectedly, or wants a cleaner way to pass wealth to the next generation. That’s usually when trusts move from “something rich people use” to “something we should seriously look at”.

Starting a trust in Australia isn’t difficult in theory. In practice, it’s easy to get wrong. The legal document has to be right. The control roles have to be right. The bank account and tax registrations have to match the deed. And in Western Australia, the property and lending issues can change the economics of the whole structure.

Why Trusts Are a Cornerstone of Australian Wealth Strategy

A trust isn’t a niche structure. It’s one of the main ways Australians hold wealth, run family investments, and manage business risk.

According to ATO trust data summarised by Arielle, in the 2021-22 income year there were 1.49 million trusts and super funds in Australia, compared with 1.18 million companies registered. The same source notes that discretionary trusts, or family trusts, make up over 80% of all trusts established. That tells you two things. Trusts are mainstream, and those who establish them often prioritise flexibility.

Why affluent families use them

The appeal is simple. A trust can help separate legal control from beneficial enjoyment. That matters when you’re trying to protect assets, manage who receives income, or create a more controlled way to transfer wealth across generations.

For business owners, that separation can be valuable. For high-income families, the distribution flexibility can be useful. For retirees and pre-retirees, a trust can be part of a broader estate planning and investment structure.

Practical rule: If your wealth is growing faster than your structure is evolving, you’re taking avoidable risk.

A lot of people first ask whether a trust is “worth it”. That’s the wrong question. The better question is whether your current ownership structure still suits the size and complexity of your life.

Why family trusts dominate

Discretionary trusts dominate because they give the trustee discretion over how income and capital are distributed among eligible beneficiaries. That flexibility is powerful when family incomes vary year to year, when adult children come into the picture, or when one spouse owns a riskier business than the other.

If you want a clean legal primer before making decisions, What Is a Trust and How Does It Work is a useful legal overview.

The mistake I see most often is treating a trust like a tax trick. It isn’t. A good trust is part of a wider strategy that deals with ownership, control, succession, and risk. Tax efficiency matters, but it should never be the only reason you set one up.

Choosing Your Trust Structure The Critical First Decision

If you choose the wrong trust structure, everything that follows gets harder. Lending becomes clunky. Distributions become limited. Joint ownership gets messy. Succession becomes a fight.

That’s why the first decision isn’t “should I get a trust?” It’s “which trust fits what I’m trying to do?”

Know the key players first

Before comparing structures, get clear on the roles.

- Settlor: The independent person who starts the trust by providing the initial settlement amount. They shouldn’t be a beneficiary.

- Trustee: The legal owner of the trust assets and the party responsible for operating the trust according to the deed.

- Beneficiaries: The people or entities who may receive income or capital from the trust.

- Appointor: The person with ultimate control over who can appoint or remove the trustee. This role is often more important than people realise.

If the trustee runs the trust day to day, the appointor controls the controller. That’s a serious power. Get it wrong and you can create family conflict or hand long-term control to the wrong person.

The trust types that matter most

Most clients considering starting a trust in Australia are weighing one of four structures.

| Trust Type | Primary Use Case | Income Distribution | Best For |

|---|---|---|---|

| Discretionary trust | Family wealth holding and tax planning | Trustee decides each year within the deed rules | Families, business owners, flexible investment structures |

| Unit trust | Shared ownership where interests need to be fixed | Based on units held | Business partners, joint ventures, unrelated investors |

| Hybrid trust | Combines features of discretionary and fixed interests | More complex and deed-dependent | Specific strategic cases where tailored legal advice is essential |

| Testamentary trust | Trust created through a will after death | Controlled under the will terms | Estate planning and intergenerational asset control |

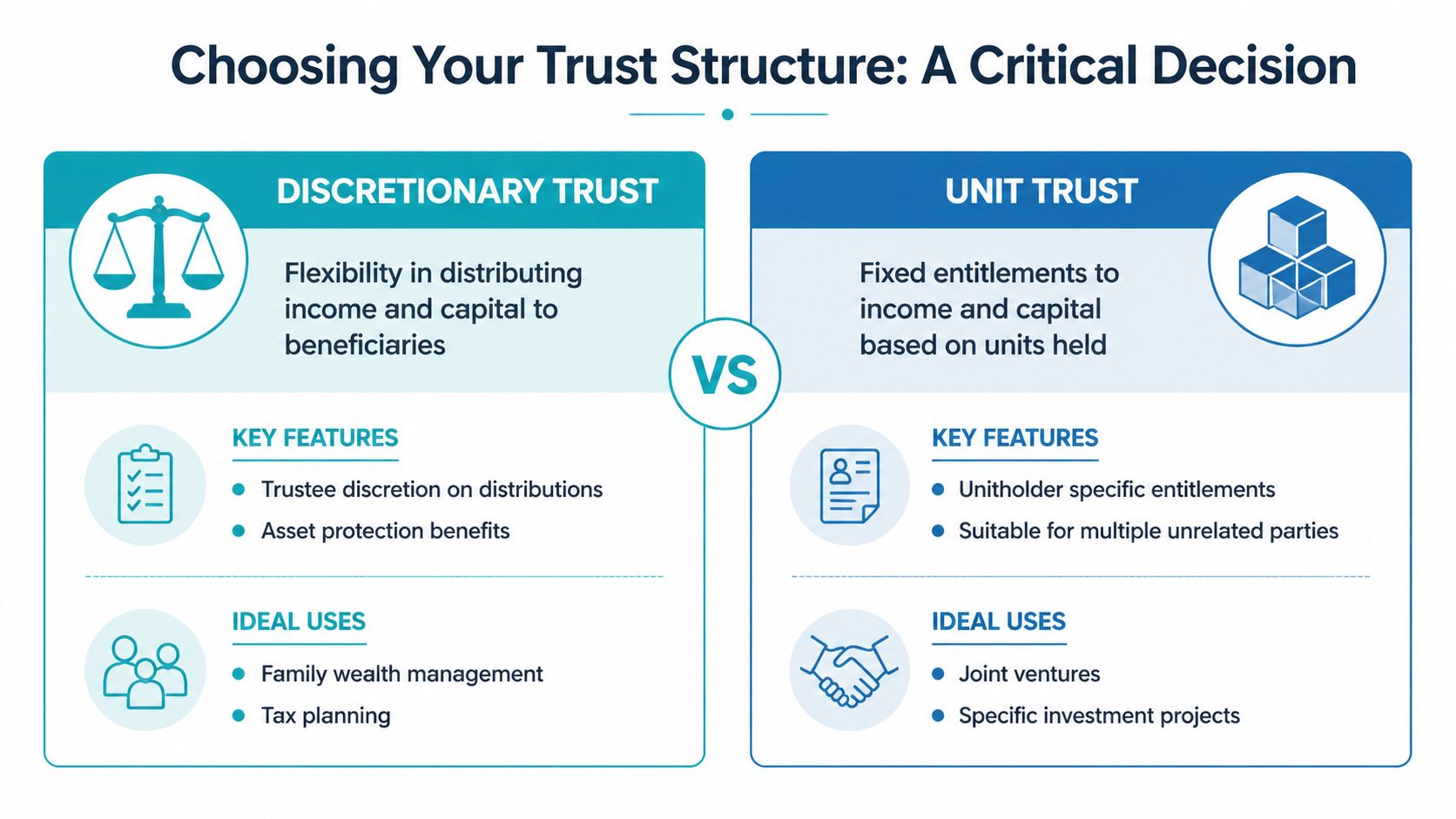

When a discretionary trust is the right call

A discretionary trust is usually the default for families with uneven incomes, private investments, or a desire for long-term control. It works well when you want flexibility rather than fixed ownership percentages.

It’s often the best fit if you want to hold shares, managed funds, or a family investment property and make annual distribution decisions based on the family’s circumstances. If you want a more detailed walkthrough of that structure, this guide on how a family trust works is worth reading.

The biggest advantage of a family trust isn’t complexity. It’s optionality.

When a unit trust makes more sense

A unit trust is cleaner when multiple parties contribute capital and expect clear entitlements. If you’re buying an investment with a sibling, business partner, or another family group, a unit trust often works better than a discretionary trust because everyone knows what they own.

That clarity matters. Discretionary trusts are flexible, but they can create tension when unrelated parties want certainty. Unit trusts trade flexibility for precision.

The structures people misuse

Hybrid trusts get attention because they sound like the best of both worlds. Sometimes they are. More often, they’re used by people who don’t fully understand the trade-offs.

A testamentary trust is different again. You don’t set it up during life as a standard family investment vehicle. It arises under a will and is part of estate planning, not routine asset acquisition.

If you’re unsure, use this shortcut:

- Want flexibility within a family group: discretionary trust.

- Need fixed ownership across parties: unit trust.

- Need something specialised: get specialised legal and tax advice before you move.

- Planning post-death control: look at testamentary trust planning through your estate documents.

The wrong structure can still “work”. It just creates friction for years. The right one makes everything cleaner from day one.

The Core Setup Process From Deed to Bank Account

This is the part people underestimate. They think the trust exists once someone says, “Let’s call it the Smith Family Trust.” It doesn’t.

A trust starts with paperwork, but valid paperwork. Then it needs proper execution, registration, and administration. If any of those steps are sloppy, the trust can become expensive dead weight.

According to Gartly Advisory’s guide to setting up a family trust, the full setup process typically takes 2-4 weeks with professionals, and professional setup usually costs between A$1,500-$5,000. The same source states that up to 30% of template-based deeds are invalidated due to non-compliance with state-specific duties, and 15% of trusts fail initial TFN approval because of poor documentation. That’s why I’m blunt on this point. Don’t DIY this with a bargain template.

Step one starts before the deed

The first move is deciding exactly what the trust is for.

Are you holding investment assets? Running a business? Planning for family wealth transfer? Bringing in another investor? The answer shapes the deed, the trustee choice, the beneficiary class, and the tax registrations.

If you don’t define the job of the trust before it’s created, you’ll often end up with a structure that’s technically valid but strategically wrong.

Draft the deed properly

The trust deed is the controlling legal document. It sets out the trustee powers, beneficiary definitions, appointor role, distribution rules, and how the trust can be managed over time.

Cheap templates often fall short. A generic deed might not fit your state requirements, your asset mix, or your succession needs. It might also omit powers you’ll wish you had later.

Use a lawyer who drafts deeds for Australian trusts regularly. Your accountant can help with tax implications, but the deed itself should be professionally prepared.

A trust deed isn’t admin. It’s the operating system for the entire structure.

Settle and execute the trust correctly

Once the deed is ready, the trust is settled. That usually means an independent settlor provides a nominal settlement amount to the trustee and the relevant parties sign the deed.

The nominal amount often used is A$10, as outlined in the verified guidance above. That figure isn’t economically important. The legal process is.

After execution, the trustee should record the first meeting and resolutions. That meeting typically confirms that the trustee accepts the appointment, notes the trust has been established, and authorises the next administrative steps.

Choose the trustee and appointor with care

You can use an individual trustee or a corporate trustee. Both can work. But if you’re building meaningful wealth, I usually prefer a corporate trustee because it creates cleaner separation and better continuity when control changes.

The appointor deserves just as much attention. Many people obsess over beneficiaries and barely think about the appointor. That’s backward. The appointor can control who controls the trust.

A sensible setup usually includes clear thought around:

- Succession control: Who steps in if you die or lose capacity.

- Practical management: Who can sign, approve transactions, and deal with banks and advisers.

- Family dynamics: Whether future disputes are likely and how control can be protected.

Register for tax and open the bank account

Once the trust is established, the trustee applies for a TFN. If the trust will carry on an enterprise, the trustee may also apply for an ABN. Some trusts also need GST registration depending on what they’re doing, but that depends on the actual activity.

Then open a dedicated bank account in the trustee’s name as trustee for the trust. The account title matters. The banking trail matters too.

The settlement sum should go through that account first. After that, all trust income and expenses should run through it. Don’t mix trust money with personal funds. That kind of laziness creates record-keeping problems and weakens the integrity of the structure.

The practical sequence that works

A clean setup usually follows this order:

- Clarify the purpose and select the trust type.

- Choose the control parties, especially trustee and appointor.

- Have the deed drafted for your actual circumstances.

- Execute and settle the trust correctly.

- Minute the first trustee resolutions.

- Apply for TFN and ABN if required.

- Open the bank account in the correct trustee capacity.

- Transfer or acquire assets properly in the trust structure.

People get into trouble when they scramble the sequence. They buy an asset first, then try to “put it in a trust later”. They sign a deed they haven’t read. They open the wrong bank account. They use personal expenses through the trust account and call it efficient. It isn’t. It’s messy.

Starting a trust in Australia works best when you treat the setup like infrastructure, not paperwork.

Navigating Costs Compliance and WA-Specific Hurdles

A trust can be a strong structure. It is not a cheap one, and it is not a hands-off one.

The setup cost is only the opening fee. The critical question is whether the trust will deliver enough strategic value to justify the ongoing administration, legal discipline, and lender friction that can come with it.

The costs people plan for and the costs they miss

The focus is often on deed preparation and registrations. Fair enough. Those are visible.

What they often miss is the annual discipline. The trustee has to keep records, maintain a separate banking trail, lodge returns, document decisions, and make proper distribution resolutions on time. If those basics slip, the structure loses much of its value.

A trust works well when the owner respects process. It becomes painful when the owner wants the benefits without the governance.

Western Australia has its own quirks

Generic trust articles usually lean on eastern states examples. That’s not good enough if you live in WA and hold property here.

According to Canstar’s trust setup overview, Western Australia requires nominal stamp duty on trust deeds, typically A$20-A$200. The same source notes that banks in WA can impose 20-30% stricter LVR limits on trust-held residential properties. If you’re borrowing to invest, that matters.

Those lending settings can affect:

- Deposit requirements: You may need more equity upfront.

- Cash flow planning: Reduced borrowing can change your acquisition timeline.

- Portfolio design: A trust-held property strategy may not perform the way a spreadsheet assumes.

Property transfers need special care

Many WA investors encounter a common pitfall. They assume they can buy in one name and “move it into the trust” later with minimal fuss. That can trigger duty and other complications depending on the transaction.

If property is involved, get advice before signing a contract. Don’t rely on broad internet guidance written for a national audience. WA property and revenue issues need local attention, especially where landholder duty or lender policy could alter the economics.

Local insight: In WA, the right trust strategy on paper can still be the wrong funding strategy if the bank treats the trust borrower more conservatively.

Compliance isn’t optional admin

A trust has to be actively managed. At a minimum, the trustee should treat these as essential habits:

- Separate banking: Every dollar in and out should flow through the trust account.

- Clean records: Keep documents, resolutions, and supporting paperwork organised.

- Timely distribution decisions: Trustee resolutions need to be prepared before the end of the financial year if distributions are being made.

- Regular reviews: Revisit the deed and control structure when family, business, or asset ownership changes.

The people who complain most about trust compliance are usually the people who tried to treat the trust like a filing cabinet. A trust is closer to a small legal machine. It needs maintenance.

If your asset base is modest and your affairs are simple, a trust may be more burden than benefit. If your wealth is growing, your income is uneven, or asset protection matters, the discipline is usually worth it.

Common Pitfalls and Advanced Strategies to Avoid Them

Most trust mistakes don’t happen at setup. They happen after setup, when people assume the structure will keep working without attention.

That assumption causes trouble. Trusts reward discipline and punish shortcuts.

A key issue flagged in Clean Slate’s family trust guidance is that trust losses cannot be distributed, which means beneficiaries can’t use those losses for negative gearing offsets in their own names. The same source says recent ATO 2025 guidance escalated Section 100A reimbursement audits and flagged 22% of discretionary trusts for scrutiny. That should get your attention.

Trapped losses are real

If a trust holds a negatively geared asset, the loss stays in the trust. It doesn’t flow out to beneficiaries to reduce their personal taxable income.

That makes trusts a poor fit for some negatively geared strategies. People who assume they’ll get the same personal tax outcome they’d get from owning an asset directly often discover the problem after the purchase, not before it.

This doesn’t mean trusts are bad for property or growth assets. It means you need to choose the structure based on the actual investment profile, not on a generic “trusts are tax effective” slogan.

Section 100A is not background noise

Section 100A matters when trust distributions are allocated one way on paper but enjoyed by someone else in substance. The classic danger zone is where a beneficiary is made presently entitled, but the money or benefit ends up elsewhere.

The ATO’s focus here means trustees need to ensure their distribution decisions are commercially and legally defensible. Minutes, cash movements, beneficiary accounts, and actual benefit flow all matter.

If your distribution strategy looks clever but the benefit doesn’t reach the beneficiary you nominated, expect scrutiny.

That’s why year-end trust planning should be coordinated, documented, and reviewed by professionals who understand current compliance risk. If tax planning is part of your objective, this broader guide on reducing taxable income gives useful context, but trust distributions need their own careful treatment.

Other mistakes that quietly damage trusts

Some traps don’t make headlines, but they still create expensive problems.

- Bad appointor planning: The trust can become unstable if control on death or incapacity hasn’t been thought through.

- Template deed complacency: A deed that was “fine at setup” can become limiting when your assets, family, or strategy changes.

- Mixed-purpose structures: Using one trust for every asset and every activity can create avoidable complexity and risk concentration.

The better approach

The strongest trust strategies are boring in the right way. They are well documented, conservatively operated, and reviewed when something important changes.

Good trustees ask practical questions:

- Does this asset belong in the trust at all?

- Does the deed still support what we’re doing?

- Do the distributions reflect real entitlement and real benefit?

- Has control been properly planned if something happens to the current decision-maker?

That’s the difference between owning a trust and using one well.

Conclusion Is a Trust Your Next Step to a Wildly Successful Financial Life

For the right client, a trust is one of the best ownership structures available in Australia. It can improve control, support asset protection, create distribution flexibility, and help organise wealth transfer far more effectively than ad hoc personal ownership.

But not every trust is a good trust. And not every person needs one.

According to InvestSMART’s summary of ATO data, over 1.02 million trusts were registered in Australia in the 2022-23 financial year. The same source notes that a minimum asset base of around $300,000 is often recommended for a trust to be financially viable, once you account for setup costs and ongoing compliance. That’s a useful filter. If your asset base and complexity aren’t there yet, a trust may be premature. If they are, delaying the structure can be the expensive move.

A simple trust readiness checklist

Use this before you start.

- You have a clear purpose: Asset protection, family investment, business structuring, or estate planning.

- Your asset base justifies the work: The structure needs enough scale to warrant the cost and admin.

- You know who should control it: Trustee and appointor choices have been considered carefully.

- You’re willing to maintain it properly: Separate accounts, annual resolutions, tax returns, and record-keeping are part of the deal.

- You’ve checked WA realities: Especially if property, duty, or lending will affect the plan.

- You’re getting legal and tax advice together: A trust is where law, tax, finance, and family dynamics all meet.

My recommendation

If you’re a high-income earner, business owner, or established family with meaningful assets, don’t keep asking whether trusts are “good”. Ask whether your current structure is still good enough.

That’s the sharper question.

Starting a trust in Australia should be deliberate. If you treat it like a strategic decision instead of a form-filling exercise, it can become one of the most useful foundations in your financial life. If you rush it, copy a template, or set it and forget it, the same structure can become a compliance burden with limited upside.

A well-built trust doesn’t just hold assets. It creates order. It defines control. It gives you more deliberate choices about risk, tax, and succession. That’s what strategic planning should do.

If you’re considering a trust and want clarity before you commit, Wealth Collective can help you think through whether the structure fits your assets, goals, and family circumstances. A short introductory call is a practical first step. You’ll get clear direction on whether a trust belongs in your plan, what to watch for in WA, and what to do next without guesswork.