Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

A lot of Australians start thinking about term insurance at the same moment life gets more serious.

You buy a home in Perth. The mortgage repayment lands. Maybe there's a child on the way, or one partner has stepped back from full-time work. You're doing well on paper, but one quiet question starts following you around: if one of us died, could the other keep this whole thing going?

That's where term insurance australia stops being a search term and becomes a planning decision.

Term insurance isn't about fear. It's about replacing the financial role you play in your household if you're no longer here. For some people, that means clearing a mortgage. For others, it means preserving school options for children, giving a surviving partner time to breathe, or making sure a business isn't forced into a rushed sale.

Individuals don't need a complicated lecture. They need someone to translate insurance into plain English and help them decide what's enough, what's missing, and what's worth paying for. That's the spirit behind a practical protection plan. Keep the essentials covered, avoid expensive misunderstandings, and make sure the policy fits your actual life.

Securing Your Family's Financial Future

A couple in their thirties buys their first place south of the river. Settlement goes through, the photos are taken, and everyone feels relieved. Then real life returns. There's a large home loan, council rates, childcare to think about, and one income already spoken for before payday arrives.

That's often the point where protection becomes less abstract.

If one partner died, the loss wouldn't only be emotional. The household could also lose years of future income, super contributions, and the person who helped carry the debt. The surviving partner might need to cover mortgage repayments, everyday bills, legal costs, and time away from work, all at once.

The risk most families leave unmeasured

Many households assume they've dealt with this because there's some cover in super. Sometimes there is. Sometimes it's enough for a single person with modest commitments. Often it isn't enough for a family with a mortgage and dependants.

The issue isn't whether you have insurance. It's whether the amount and structure match the life you've built.

A mortgage is a long-term promise. Protection is the funding plan for that promise if life changes abruptly.

A calmer way to think about it

A useful starting point is this: if your income stopped permanently tomorrow because you passed away, what financial gaps would your family face within the first month, the first year, and the next decade?

That question usually brings clarity fast.

For a young family in WA, the answer may include the home loan, living expenses, future education costs, debts, and room for the surviving partner to make decisions without immediate financial pressure. That's why term insurance belongs alongside cash flow planning, debt strategy, and super decisions. It's part of responsible financial architecture, not an isolated product purchase.

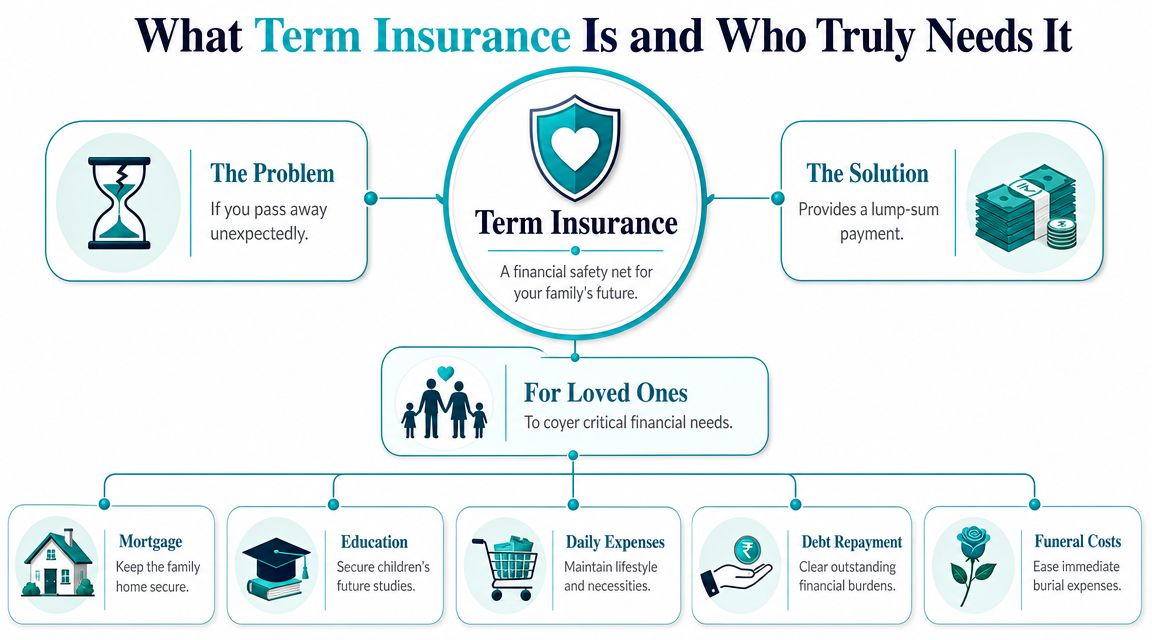

What Term Insurance Is and Who Truly Needs It

Term insurance is a policy designed to pay a lump sum to your beneficiaries if you die during the insured period. In many policies, terminal illness cover is also included as an accelerated benefit. Think of it as a financial backstop for the income, stability, and obligations you bring to your household.

It helps your family absorb a loss that would otherwise hit at the worst possible time.

Think of it like income replacement by lump sum

If you insure your car, you're protecting against the cost of a crash. If you insure your life with term cover, you're protecting against the financial impact of your death on the people who depend on you.

That's why term insurance usually isn't about you. It's about the people and liabilities you'd leave behind.

The need is broader than many people realise. The Council of Australian Life Insurers reported that 15.0 million people in Australia were covered by life insurance in 2022, insurers paid $2.9 billion for death cover that year, and 1.0 million Australians were underinsured to meet basic needs according to CALI's life insurance claims and coverage data. The message is simple: cover is common, but adequate cover is not.

Who usually needs it most

Some people can postpone the decision. Others really shouldn't.

- Mortgage holders need cover because a home loan doesn't disappear when one income does.

- Parents with dependent children often use term insurance to protect schooling, housing stability, and day-to-day living costs.

- Business owners may need it to protect family cash flow, support debt repayment, or create options if the business relies heavily on them.

- People with personal debt should consider who would carry that burden if they died.

- Couples with unequal incomes often have a hidden vulnerability. The higher earner is obvious, but the lower earner may still provide childcare, household management, or part-time income that would be expensive to replace.

When you might not need much

If you have no dependants, minimal debt, strong assets, and no one relies on your income, your need may be smaller. Even then, some cover can still make sense if family members would face funeral costs or if debts would fall back on a partner.

Practical rule: the bigger your responsibilities to other people, the more important term insurance becomes.

Decoding Key Policy Features and Exclusions

A policy isn't just a sum insured. The fine print shapes whether the cover still works for you years from now.

That matters because two policies can look similar in a quote comparison and behave very differently over time.

Premium style changes the long-term cost

One of the first choices is usually between stepped premiums and level premiums.

- Stepped premiums generally start lower, then rise as you age.

- Level premiums are designed to be more stable earlier on, though they can still change in some circumstances set out in the policy.

Stepped premiums can suit people who want lower upfront cost or expect to review cover regularly. Level premiums can make sense for people planning to hold cover for many years. Neither is universally better. The right choice depends on cash flow, time horizon, and how likely you are to keep the policy long term.

Policy duration and indexation matter more than people expect

The long-term value of a policy is heavily influenced by design. Some Australian insurers offer term life cover to age 99, while others stop much earlier. Some policies also include automatic indexation that can increase the benefit by 5% annually or CPI, whichever is higher, as described in Allianz's overview of life insurance features.

That sounds technical, but the practical point is straightforward. If you set a cover amount today and never review it, inflation can slowly reduce its real purchasing power. Indexation helps protect against that erosion.

For a broader plain-English explanation of the moving parts, what life insurance covers is worth reviewing before you compare policies.

Exclusions are where many buyers get caught

People often compare only price. The better question is, “Under what conditions will this policy pay, and when might it not?”

Common areas to review in the Product Disclosure Statement include:

- Exclusions for specific circumstances or activities

- Premium adjustment rules so you know what may change over time

- Claims process details including what evidence may be required

- Terminal illness provisions and how they interact with the death benefit

- Expiry conditions tied to age, term length, or policy anniversaries

The best-value policy isn't always the cheapest one. It's the one that still solves the problem when your family needs it.

How Australian Term Insurance Costs Are Calculated

Insurance pricing feels mysterious until you know what the insurer is assessing.

In Australia, term insurance premiums are highly personalised. Insurers look at your risk profile, not just the cover amount you request. That's why your quote can differ sharply from a friend's, even if you're the same age and asking for similar cover.

The main factors that shape your premium

According to Compare the Market's explanation of term life insurance pricing and PDS requirements, key underwriting variables include age, health status, smoker status, occupation, and the sum insured. Some insurers also use questionnaires or medical exams depending on the risk tier.

In practice, that means:

- Age usually matters because risk rises over time.

- Health history affects how the insurer views the likelihood of a future claim.

- Smoking can materially affect pricing because it changes risk.

- Occupation and lifestyle matter if your work or activities are considered higher risk.

- Sum insured matters because larger benefits create larger potential claims.

Why quotes vary so much

Two people can both ask for the same amount of cover and receive different offers because insurers are pricing the probability and size of a claim, not selling a standard retail item.

A desk-based accountant who doesn't smoke and has a clean medical history will often present differently to an applicant with a hazardous occupation, complex health history, or nicotine use. That doesn't mean one person can't get cover. It means the underwriting outcome may differ.

A simple household budget also helps you decide what premium is sustainable before you apply. If you need a practical refresher on cash flow, Senki's guide to creating your personal budget is a useful starting point.

What to look for before you apply

Australian insurers must provide a Product Disclosure Statement before purchase, so use it. Don't treat it as paperwork to skim after you've chosen a premium.

Check these points carefully:

- Premium basis so you know how costs may change.

- Disclosure requirements so your medical and lifestyle information is complete and accurate.

- Definitions and exclusions because wording can affect claim outcomes.

- Ownership structure especially if you're deciding between personal ownership and super ownership.

If a premium only works when everything goes perfectly, it may not fit your life.

Term Life vs TPD and Income Protection

Many people often find themselves tangled. They ask for “term insurance” when they're really trying to solve a different risk.

Term life insurance covers death and often terminal illness. TPD covers a permanent disability that stops you working again. Income protection is designed to replace part of your income if illness or injury keeps you off work for a period of time.

The confusion matters. The Financial Services Council estimates around 1.0 million Australians are underinsured for death/TPD, as outlined in the FSC underinsurance research report. Part of that shortfall comes from people buying one type of cover and assuming it solves every problem.

The simple way to separate them

Think about the question each policy answers.

- Term life asks, “What happens financially to the people I leave behind if I die?”

- TPD asks, “What if I survive, but can never return to work?”

- Income protection asks, “What if I'm alive, recovering, and my salary stops for a while?”

Those are different risks. That's why the covers are complementary, not interchangeable.

Term Life vs. TPD vs. Income Protection

| Cover Type | What It Covers | How It Pays Out | Primary Purpose |

|---|---|---|---|

| Term Life | Death, and often terminal illness under the policy terms | Usually a lump sum | Protect dependants, clear debts, support long-term family stability |

| TPD | Permanent disability meeting the policy definition | Usually a lump sum | Fund rehabilitation, debt reduction, ongoing living needs, and structural life changes |

| Income Protection | Illness or injury that prevents you from working, subject to policy terms | Usually regular monthly payments for an approved period | Help replace lost income while you recover |

A practical example

Take a family with a mortgage and two young children.

If one parent dies, term life cover can give the surviving family a lump sum to reduce debt and maintain stability. If that same parent survives a severe illness but can't work again, term life won't solve that problem on its own. TPD may. If the parent is off work for months and likely to return later, income protection is often the cover designed for that period instead.

For a deeper look at disability cover in particular, total and permanent disability insurance helps clarify where TPD sits in the broader protection mix.

One policy protects your family from your death. Another protects you from the financial consequences of surviving the event.

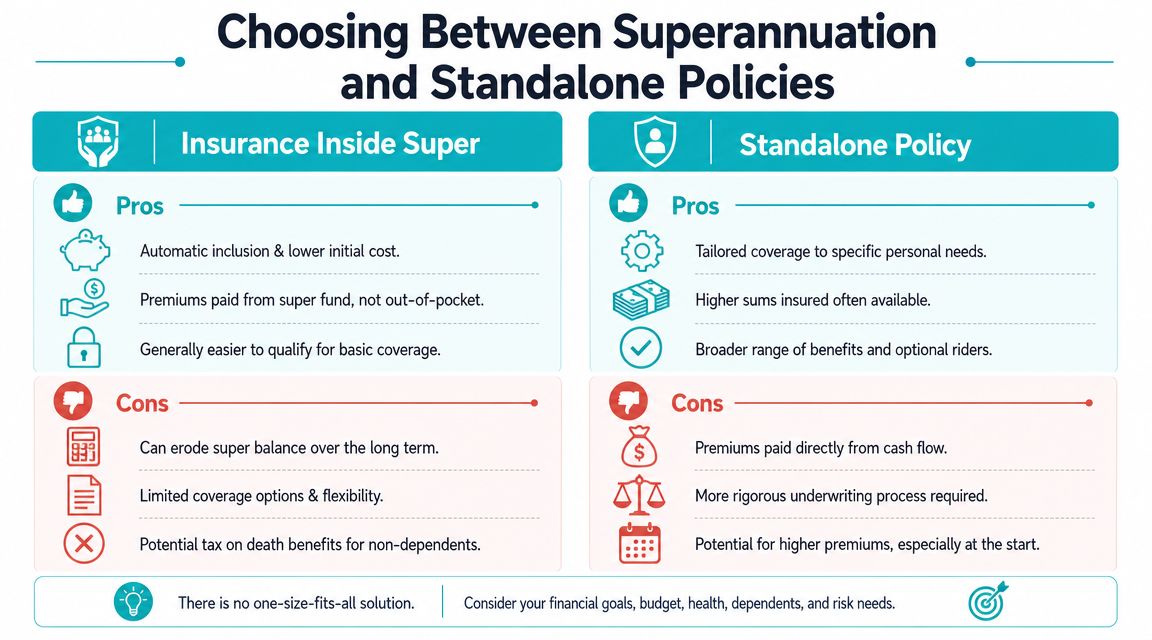

Choosing Between Superannuation and Standalone Policies

This is one of the most important trade-offs in term insurance australia.

Insurance inside super is often easy, familiar, and cheaper. A standalone policy often gives you more control, stronger tailoring, and a clearer fit for complex needs. The problem is that many Australians stop the comparison after the word “cheaper”.

Why cover inside super is attractive

Premiums for life insurance through super can be as low as half the price of buying it directly, according to Rainmaker's insurance industry reporting. That cost difference is real, and for some people it makes cover accessible when cash flow is tight.

There's also convenience. Premiums can be paid from your super balance instead of your bank account, and default cover may require less active decision-making at the start.

You can also explore the broader interaction between insurance and retirement savings through superannuation income protection, especially if you're reviewing multiple policy types together.

Where cheap can become expensive

Lower cost doesn't automatically mean better protection.

NobleOak notes that underinsurance is higher among people with super-held cover, and estimates default policies often provide only about two-thirds of the death cover most families need, as outlined in its discussion of whether you may be underinsured. That creates a dangerous illusion. You feel covered, but the amount may not be enough to clear a mortgage, support children, and protect a surviving partner's lifestyle.

A standalone policy is often stronger when you need:

- More customized cover for a specific debt, family structure, or business obligation

- Higher sums insured than default arrangements provide

- Feature choice such as policy design, ownership, and optional extras

- Certainty across life changes if you change jobs or want cover independent of your super fund settings

A useful decision filter

Insurance inside super can be a sensible base layer. For many households, though, it shouldn't be the whole strategy.

If you're single, renting, and building savings, default cover might be enough for now. If you have dependants, a large mortgage, or a more complex financial life, the better question is whether your super policy leaves a gap. In a higher-cost environment, that gap can be painful.

Your Path to Protection A Simple Checklist

Good insurance decisions rarely come from grabbing the first quote. They come from matching the policy to the job it needs to do.

The clearest path is to work through the decision in order, not all at once.

The Wealth Collective path to protection

Assess what would need funding

Add up the obligations your family would face if you died. Think mortgage, personal debts, living costs, future education needs, and any buffer that gives your partner time to regroup.Check what you already have

Review your super fund insurance, any existing retail policies, and whether the ownership structure still suits your circumstances. Many people discover they have cover, but not enough, or not in the right place.Compare the structure, not just the premium

Look at stepped versus level premiums, expiry ages, indexation, terminal illness terms, and exclusions. Cheap cover that stops early or doesn't fit your needs can be poor value.Complete disclosures carefully

Be precise with medical history, smoking status, occupation, and lifestyle details. Problems often start when people rush the application or assume a detail doesn't matter.Review after major life changes

Buying property, having children, changing jobs, taking on business debt, or nearing retirement can all change what “enough cover” looks like.

Common mistakes to avoid

- Relying on default super cover without checking adequacy

- Choosing by price alone

- Underestimating future living costs

- Ignoring inflation and policy duration

- Forgetting to update beneficiaries or ownership arrangements

One practical option for people who want help comparing cover, super settings, and broader personal insurance decisions is Wealth Collective, which provides advice across protection, superannuation, debt reduction, and long-term planning.

Good cover should do one thing very well. It should give your family options at a time when they'll need them most.

If you want help working out whether your current cover is enough, or whether insurance inside super is leaving a gap, you can book a free introductory call with Wealth Collective. It's a simple starting point to review your situation, talk through your options, and decide what protection makes sense for your family.