Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

On a lot of weeknights in Perth, the conversation happens after dinner. The kids are finally down. The mortgage repayment is due soon. One partner asks a simple question that’s hard to answer calmly: if one of us wasn’t here next year, what would happen to the house, the school fees, and everything we’ve been building?

That’s where term life insurance usually enters the picture.

It isn’t about fear. It’s about making sure a bad event doesn’t become a financial disaster for the people you love. For many Australians, especially young professionals, dual-income households, business owners, and people edging toward retirement, term life insurance is the cleanest way to protect a very specific period of life. The years when debt is higher, children are dependent, and your income carries a lot of the load.

An Introduction to Protecting What Matters Most

A Perth family settles into a new routine a few months after moving in. The mortgage is manageable. Childcare is booked. One partner works in the city, the other might be on a FIFO roster, and every pay cycle already has a job to do. Then a harder question turns up at the kitchen bench. If one income disappeared, how long would the plan still hold?

For a lot of households, the answer is uncomfortable. The loan might still need to be paid. Rent or school fees would not pause. Groceries, car repayments, and everyday bills would keep coming. Grief is hard enough on its own. Financial pressure can force rushed decisions at the worst possible time.

Term life insurance is one way to create breathing room. It is designed to pay a lump sum if the insured person dies during the chosen cover period. In plain English, it gives a family time, options, and money to deal with the practical fallout of losing someone who helped hold the household together.

That matters in Western Australia for reasons that are easy to miss if you only read generic guides. Perth families often carry large mortgages. FIFO households can depend heavily on one higher income. Many people also hold some life cover inside super, but the default amount is often a starting point, not a finished plan. It may be useful, yet still fall well short of what a partner, children, or a surviving co-borrower would need.

A simple way to look at it is this. Your financial plan has weak points. The years with a big home loan, young children, or one income doing most of the heavy lifting are usually the riskiest. Term life insurance is built for that stretch of life.

The goal is not to pile on cover for the sake of it. The goal is to match cover to a real problem. Keep the house. Clear debt. Fund a few years of living costs. Give a surviving partner room to make careful decisions instead of urgent ones.

That practical fit matters more than labels, especially once superannuation enters the picture. Many Australians have some cover through their super fund and assume the job is done. Sometimes it is a decent base. Sometimes it is too small, ends when you change jobs or funds, or is set up in a way that does not match your family’s needs.

Good cover should make sense on paper and in real life.

What is Term Life Insurance and How Does It Work

The easiest way to understand term life insurance is this. It’s like renting financial security for your family.

You pay for cover for a set period, called the term. If you die during that period, the policy pays a lump sum to the beneficiary or beneficiaries named on the policy. If you outlive the term, the cover ends unless you renew or change it under the policy rules.

The three moving parts

Every term life policy is built around a few core decisions.

- The term. This is the length of time you want cover to stay in place. People often align it with a mortgage, their children’s dependency years, or the final stretch of working life.

- The cover amount. This is the lump sum that would be paid on a valid claim.

- The premium. This is what you pay to keep the policy active.

A simple example helps. Say you’ve got a mortgage, two young children, and one partner would struggle to cover everything alone. You might choose a term that runs through the years when the loan is largest and the children still rely on your income. If something happens during that period, the payout gives your family options.

What term life insurance is designed to do

Term life insurance is usually best for temporary but high-stakes financial responsibilities.

That includes things like:

- Home loan protection so your family doesn’t have to sell under pressure

- Income replacement for a partner who needs time to regroup

- Children’s costs while they’re still at school or uni

- Business debt or guarantees where one person’s death would create immediate strain

This is why term cover suits many working households. Your risk isn’t permanent. It’s heaviest during the years when debt and family obligations are highest.

Practical rule: Match the policy to the problem. If the main risk disappears over time, a term policy often makes more sense than paying for lifelong cover you may not need.

How it differs from whole of life

People often hear “life insurance” and assume every policy works the same way. It doesn’t.

Term life insurance covers a defined period. Whole of life or other permanent cover aims to last for life and may include additional features. That can make those products useful in some situations, but also more expensive and more complex.

The appeal of term life is its clarity. You’re buying protection for a window of time when your family would be most financially vulnerable.

A consumer comparison can be helpful if you’re weighing choosing life insurance options. The key is not to start with the product name. Start with the financial problem you need solved.

What happens if you outlive the term

This part trips people up. If the policy reaches the end of its term and you’re still alive, there’s usually no death benefit paid. That doesn’t mean the policy failed. It means it did its job during the years you needed it most.

Good term planning asks a better question. By the time the cover ends, have you reduced debt, built assets, grown super, and reached a point where your family would be more financially secure without that insurance? If the answer is yes, the policy has served its purpose well.

Decoding Your Policy Key Features and Common Exclusions

Once you move past the basic idea, the next challenge is the policy document. Many smart people switch off at this stage because insurers use language that sounds heavier than it needs to.

A term life policy is still just a contract. It sets out what’s covered, when the insurer pays, what evidence is needed, and where the exclusions sit. If you know what to look for, the document becomes far less intimidating.

Features that can add real value

Some policy features are easy to overlook when you’re focused on premium alone.

Terminal illness benefit usually means the policy can pay early if you’re diagnosed with a qualifying terminal illness under the policy definition.

That matters because the financial pressure often starts before death. Medical costs, reduced work capacity, and family support needs can all show up quickly.

Another feature worth asking about is:

Guaranteed future insurability generally means you may be able to increase cover after certain life events without going through full new medical underwriting.

Typical trigger events can include marriage, having a child, or taking on a larger mortgage. The exact rules depend on the insurer, so it’s worth checking whether there are deadlines, caps, or event conditions.

Other policy features can include conversion options, ownership flexibility, and benefit payment terms. Not every feature will matter to every household, but some can be very useful if your life is changing quickly.

The exclusions people should actually read

Most exclusions are not there to trick you. They’re there to define the insurer’s boundary of risk. But you do need to know about them.

Common exclusions or claim limits can include:

- Early suicide clauses. Many policies apply a waiting period for suicide after commencement.

- Non-disclosure issues. If a person leaves out important health, occupation, or lifestyle information, the insurer may investigate heavily at claim time.

- Specific hazardous activities. Some high-risk pursuits may be excluded or require special acceptance.

- Policy lapse. If premiums stop and the policy lapses, cover can end.

The practical lesson is simple. A cheap premium isn’t helpful if the ownership, definitions, or disclosure process are wrong from the start.

Why wording matters more than most people expect

Two policies can look similar from a marketing summary and still behave differently when a family needs to claim. Definitions matter. So do ownership details, especially where super is involved. One setup may suit a family with children. Another may suit a business owner with debt tied to the company.

A good review usually starts with questions like these:

| Policy area | What to check |

|---|---|

| Ownership | Who owns the policy, and who receives the benefit |

| Beneficiaries | Whether the intended people can receive funds as planned |

| Definitions | How death, terminal illness, and key events are defined |

| Flexibility | Whether cover can change as your life changes |

| Premium structure | Whether cost stability matters more than lower upfront price |

The fine print shouldn’t scare you off

It should slow you down just enough to ask better questions.

If you’re comparing policies, don’t just ask “what does it cost?” Ask what events allow increases, what evidence is required at claim time, whether the ownership structure suits your family, and what exclusions could matter in your actual life. A FIFO worker, a surgeon, and a café owner in Perth may all need term life insurance, but their policy details won’t necessarily look the same.

That’s where advice often earns its keep. Not by making the contract mysterious, but by translating it into plain English before you sign.

Term Life vs The Alternatives Finding the Right Fit

A Perth family with a new mortgage often asks a simple question: “What cover solves our problem?” That is the right place to start.

Term life insurance is built for one specific risk. If you die during the policy period, it pays a lump sum to help clear debts, replace income, or give your family breathing room. But death is only one way a household can come under pressure. A long illness, a disabling injury, or months away from work can do just as much damage to the budget, especially in WA households relying on one main income or a FIFO roster.

Personal insurance at a glance

| Insurance Type | What it Covers | Typical Payout |

|---|---|---|

| Term Life Insurance | Death during the policy term, and sometimes terminal illness under the policy terms | Lump sum |

| Whole Life Insurance | Lifelong cover with added product features depending on the policy | Lump sum |

| Income Protection | Loss of income if illness or injury stops you working temporarily | Monthly benefit |

| Total and Permanent Disability insurance | Permanent disability that meets the policy definition | Lump sum |

When term life is the right fit

Term life usually suits people with a clear financial deadline.

You might have 25 years left on a home loan in Perth. You might be raising children who will depend on your income for another 10 or 15 years. You might have personal guarantees tied to a small business. In those cases, the job of the policy is straightforward. Create a pool of money if you die too soon.

That is why term cover often fits:

- Parents with young children who want school costs, rent or mortgage payments, and daily living expenses covered

- Couples with a mortgage who want the surviving partner to keep the home without immediate financial panic

- Borrowers with a defined debt period such as a home loan, investment loan, or business debt

- People comparing cost carefully who want cover focused on protection rather than lifelong product features

In Australia, that practical focus matters even more because many people hold life cover through super. Term-style death cover inside super can be cost-effective and convenient, but it also comes with rules around ownership, beneficiaries, and how benefits are paid. For a FIFO worker in the Pilbara or a family in Baldivis trying to stay ahead of mortgage repayments, those details can change whether cover works the way they expect.

Where the other covers may fit better

Term life does not replace your income if you are still alive but unable to work.

Income protection is the policy built for that problem. It usually pays a monthly benefit when illness or injury stops you earning, subject to waiting periods and policy terms. For a tradie in Mandurah or a nurse in Perth who depends on regular wages, that can matter more in day-to-day life than a death benefit alone.

TPD insurance deals with a different situation again. It is designed for severe, permanent impairment that meets the policy definition. The payment is generally a lump sum that can help reduce debt, fund care, cover home modifications, or support a longer-term plan if returning to work is unlikely.

Some households also look at trauma cover for specified medical events such as certain cancers, heart attacks, or strokes. That type of cover can make sense where the financial shock is less about permanent disability and more about treatment costs, time off work, and recovery.

Choosing the mix that matches real life

A good way to compare these options is to ask what would hurt your household first.

If the biggest risk is a surviving partner being left with a large mortgage, term life may be the foundation. If the bigger risk is several months off work after an injury, income protection may deserve equal attention. If you are arranging cover through super, the conversation gets even more practical because not every type of cover works the same way inside super, and not every family situation suits a super-owned policy.

If you want a plain-English comparison before choosing, this guide to life insurance types explains the main categories clearly. For another perspective on choosing life insurance options, it helps to compare how term and longer-duration cover are typically used.

The right fit is the policy, or combination of policies, that matches the financial pressure your family would face.

Who Needs Term Life Insurance and How Much is Enough

A Perth family with a new mortgage can look secure on paper. Two incomes. Kids in school. Bills under control. If one person dies, that picture can change fast, especially if the surviving partner needs time off work or cannot keep up the home loan alone.

That is the group term life insurance is usually built for. People with dependants, shared debts, or both.

Four WA situations where term cover often makes sense

A couple in Subiaco with a fresh mortgage often wants a simple result. If one partner dies, the other can stay in the home and avoid rushed financial decisions. Cover may need to clear most or all of the loan, then add a buffer for living costs and childcare.

A FIFO worker living near Dunsborough may have a different pressure point. Household cash flow can depend heavily on one income, and the way insurers assess mining, offshore, or remote-site work can be more complex than a basic online quote suggests. In Australia, that conversation also overlaps with super, because many people in these roles already hold some default cover inside their fund without knowing whether it is enough.

A Perth small business owner can be exposed in two directions at once. There may be a home mortgage, business lending, and personal guarantees signed with the bank. If that person dies, the family may be dealing with grief, loan pressure, and business disruption at the same time.

A pre-retiree may need less cover than a 35-year-old with young children, but that does not always mean no cover. If there is still a mortgage, a financially dependent spouse, or a desire to leave assets intact rather than forcing their sale, term life can still play a useful role.

How to judge whether you need it

A practical test is to ask one question. If you died this year, who would have a money problem within the next 30 days?

For some households, the answer is obvious. The mortgage still has twenty years left. School fees are ongoing. One parent works part-time because someone has to do school pick-up. For others, the issue sits inside super. They have some death cover through their fund, but it may be far below what the family would need once debts and future costs are added up.

That is why generic rules of thumb often miss the mark. A FIFO family in WA, a self-employed tradie in Baldivis, and a public servant in Joondalup can all be the same age and need very different cover amounts.

Fixed cover or decreasing cover

If your main goal is protecting a large debt that shrinks over time, decreasing term cover can be worth considering. It works a bit like your mortgage balance. As the loan reduces, the insured amount reduces as well.

That structure can suit borrowers in Perth who mainly want the house protected and are less concerned about leaving a large extra lump sum. It can also suit business owners using cover to match a reducing business loan. The trade-off is simple. A falling benefit may cost less, but it gives less flexibility later if your family needs money for more than debt repayment.

A simple way to estimate the amount

You do not need a perfect number on day one. You need a sensible first draft.

Start with four buckets:

-

Debts to clear

Include the mortgage, personal loans, credit cards, and any business debt that would become the family’s problem. -

Income gap at home

Estimate how much your partner or dependants would need each year, and for how long. Many Perth families want enough to create breathing room for several years, not just a few months. -

Future costs

Schooling, childcare, specialist care, or support for ageing parents can all matter. These are the expenses people forget because they are not due tomorrow, but they still arrive. -

What you already have

Savings, investments, and super death benefits can reduce the amount of external cover required. The key word is can. Super cover should be checked, not assumed.

If you want a more detailed method, this guide on how much life insurance you need gives a useful framework.

Where underinsurance usually starts

The most common mistake is counting only the debt and ignoring the family’s recovery time. Paying off a mortgage helps, but it does not replace lost income, school costs, or the option for a surviving partner to reduce work while the household adjusts.

Another common problem is overestimating cover inside super. Many Australians have default death cover through superannuation, which is a helpful starting point, but default amounts are often designed for broad member groups, not for your actual mortgage in Perth or your family setup. Ownership through super can also affect how benefits are paid and who receives them, so the policy amount is only part of the picture.

The right amount is the amount that lets your family keep control. Keep the home if that matters. Keep time on their side. Keep choices open during a very hard period.

Cost, Super and the Application Process

Price is usually the first question. Fair enough. If you are juggling a Perth mortgage, school fees, or variable income from FIFO work, you need to know whether cover will fit the household budget now and still make sense in ten years.

A useful way to look at premiums is this: you are not just paying for a dollar amount of cover. You are paying for a mix of risk, timing, and policy design. Two people can ask for the same cover amount and receive very different prices because the insurer is assessing a different overall picture.

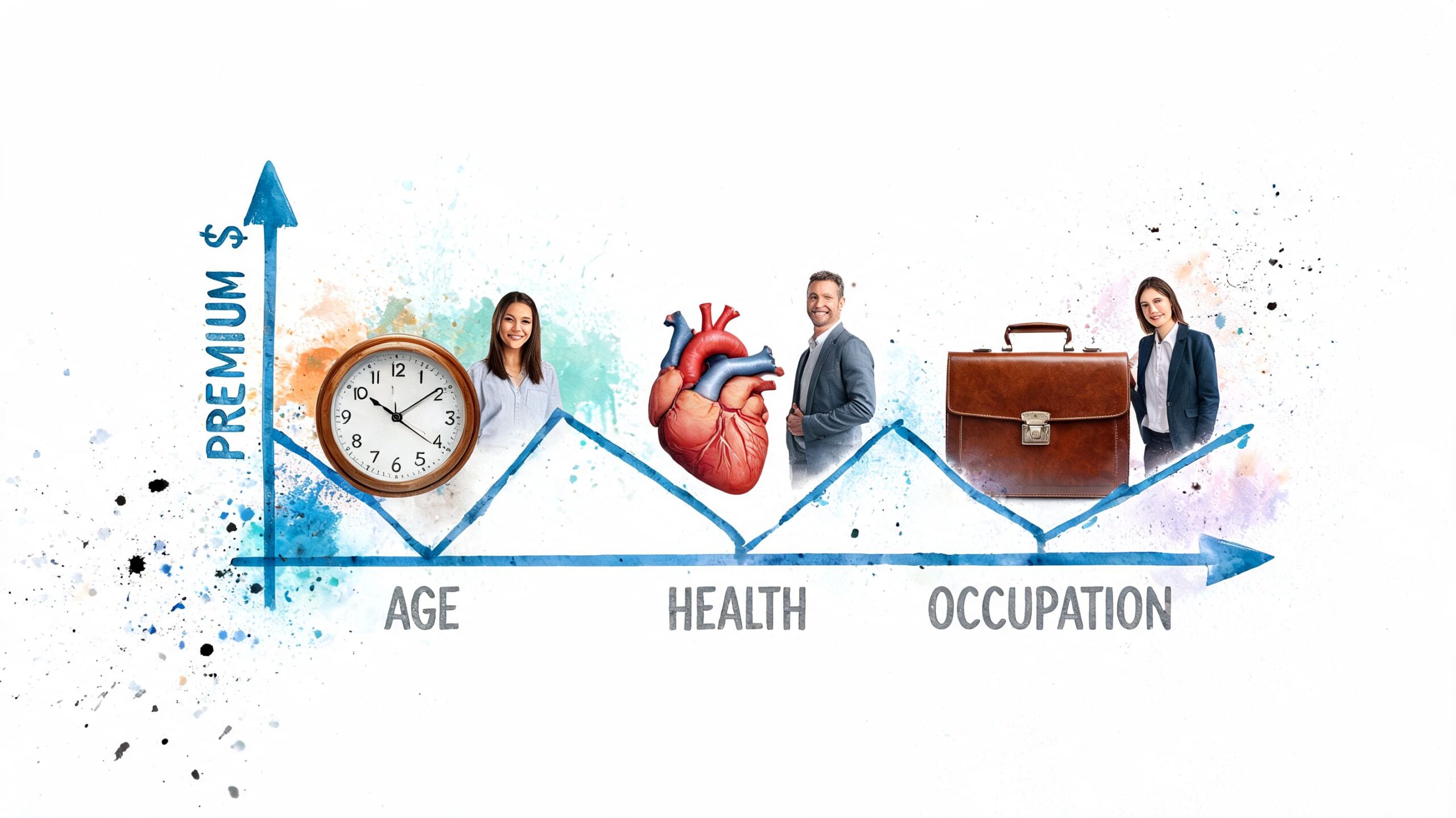

What affects your premium

Insurers usually focus on a handful of factors.

- Age. Applying earlier often means lower starting premiums.

- Health. Current conditions, past treatment, medications, and family history can affect pricing or the terms offered.

- Occupation. Physical work, remote work, underground work, and frequent travel can all matter.

- Lifestyle. Smoking, risky hobbies, and some overseas travel plans may increase cost or lead to exclusions.

- Cover design. The amount insured, how long you want the cover, whether premiums are stepped or level, and whether the policy sits inside or outside super all affect what you pay.

For many West Australians, occupation is where online quotes stop being helpful. A metro office worker, a Pilbara FIFO operator, and a self-employed sparky may all need cover for the same family goal, but the underwriting path can look quite different.

Stepped premiums versus level premiums

This is one of the biggest practical decisions, and it is often missed.

Stepped premiums usually start lower because they are based on your age each year. That can suit someone who wants short-term cover or needs to keep early costs down. The catch is that premiums often rise as you get older. A policy that felt cheap at 32 can feel heavy at 47, which is often the stage when children are still at home and the mortgage is still large.

Level premiums work more like fixing part of the cost earlier. They are usually higher at the start, but they aim to reduce the rate of increase over time. They can make sense if you expect to keep the cover for many years.

It helps to picture it like choosing between a cheaper rent today that rises often, or a higher rent with more stability. Neither option is automatically right. The better fit depends on your timeframe, cash flow, and whether you are covering a short sharp risk, such as the peak mortgage years, or a longer family dependency period.

Holding cover inside or outside super

The Australian system adds another layer.

Term life insurance can often be arranged through superannuation, and for many people that is the first place they encounter it. The premium may be deducted from your super balance rather than your everyday bank account, which can help cash flow. For someone feeling pressure from Perth housing costs, that can sound appealing.

But the money still comes from somewhere. Paying premiums from super can reduce what stays invested for retirement. Benefit payment rules can also be less straightforward, especially in blended families, separation situations, or where there is no current binding nomination.

There is also a difference between having cover in super and having the right cover in super. Default insurance through a fund is often a starting point, not a finished plan. It may be too small, the premium type may not suit how long you need cover, and the definitions may not line up with your wider estate planning.

If you want a plain-English refresher on policy structure before comparing ownership options, this guide on how life insurance works in Australia is a helpful starting point.

Ownership also connects to who receives the money and how it is controlled after death. That is one reason some families end up discussing beneficiary nominations, wills, and even broader estate tools at the same time.

What the application process usually involves

Many people expect a long, awkward process. It is usually more straightforward than they fear, although complex occupations or medical histories can add a few extra steps.

A typical application includes:

-

Initial fact find

You give details about your health, work, income, debts, existing cover, and what the policy needs to do. -

Insurer assessment

The insurer reviews the application and may ask follow-up questions. -

Medical evidence if required

Depending on the amount of cover and your history, this may involve a GP report, blood test, or nurse screening. -

Offer terms

The insurer may offer standard rates, apply a loading, add an exclusion, or ask for more information. -

Policy commencement

Once the terms are accepted and the policy is put in force, cover begins.

Good advice can make this process clearer, especially if you are deciding between cover inside super, cover outside super, or a mix of both. Wealth Collective’s Protection Plus service is designed to review cover needs, ownership, and premium structure together so clients can compare practical options instead of sorting through insurer differences on their own.

Take Your Next Step Toward Financial Security

A lot of people treat life insurance as a set-and-forget item. They tick the box inside super, keep paying whatever appears on the statement, and assume the job is done.

But is it?

If you’ve changed jobs, taken on a bigger mortgage, started a business, had children, separated, remarried, or moved closer to retirement, the old setup may no longer fit. A policy that once made sense can become too small, too expensive, or owned in the wrong place.

That’s especially true with term life insurance because it works best when it is tied to a clear purpose and a clear timeframe. If the purpose has changed, the policy probably deserves a review as well.

The next step doesn’t need to be a big one. It just needs to be deliberate. Review what cover you already have. Work out what it is meant to protect. Check whether the premium path still suits your plan. Then speak with someone who can translate the details into an action list that makes sense for your life in WA.

Frequently Asked Questions About Term Life Insurance

Should couples get one joint policy or two separate policies

Most couples are better off at least considering two separate policies rather than assuming one joint arrangement is cleaner.

Separate cover can offer more flexibility if your incomes, health history, debt responsibilities, or future plans are different. It also makes it easier to change one person’s policy without disturbing the other’s. Joint arrangements can look simpler at first glance, but simplicity on application day doesn’t always mean simplicity later.

What happens when a term life policy ends

When the term finishes, the cover usually ends if no claim has happened during that period.

Depending on the policy, you may have options to renew, apply for new cover, or convert to another type of product. The important point is not to leave that decision until the final weeks. Review the policy early enough to compare your options properly and consider whether you still need cover at all.

Can I change my cover if my circumstances change

Often, yes, but how easy that is depends on the policy wording.

If your debt increases, your family grows, or your business obligations change, you may be able to increase cover. Some policies include future-insurability features for certain life events. In other cases, you may need to go through fresh underwriting. That’s why it helps to treat term life insurance as something to review after major life changes rather than something you buy once and forget.

Can I keep term life insurance if I move overseas

Maybe, but you need to check the insurer’s rules.

Some policies can stay in force if you move, while others may apply conditions based on where you live or travel. Claims handling, taxation, and policy servicing can all become more complicated once you’re no longer based in Australia. If an overseas move is even a possibility, raise it before you apply and again before you relocate.

Is default insurance in super enough for most people

Sometimes it’s a useful starting point, but it’s not automatically enough.

Default cover is designed for scale, not for your exact mortgage, family structure, or business risk. It may be appropriate as part of the solution, but many people need to review the amount, ownership, and premium type to make sure it matches what they’re trying to protect.

Do healthy people need to think about renewability and conversion

Yes, because good health today doesn’t guarantee easy access to future cover.

If your health changes later, a policy feature that allows some form of renewal or conversion can become very valuable. Even if you never use it, knowing whether the option exists helps you plan ahead instead of scrambling when circumstances shift.

If you want help turning this into a clear plan, book a free introductory chat with Wealth Collective. A short conversation can help you work out what your current cover is doing, where the gaps may be, and what kind of term life insurance structure may suit your situation.