Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

It's often assumed that a will dictates where assets go upon death. That’s often true for bank accounts, property and personal belongings. It’s not automatically true for super.

That gap catches families at the worst possible time. A person may have spent years building wealth, updating their will, and talking clearly about what they wanted, only for their super fund trustee to make the final decision because the right nomination was never put in place.

If you’ve ever asked what is a binding death benefit nomination, the short answer is this: it’s the document that gives your super fund legally enforceable instructions about who should receive your super death benefit.

The Multi-Million Dollar Question What Happens to Your Super

A common scenario goes like this. Someone dies, the family finds a current will, and everyone assumes the estate process is straightforward. Then they learn the deceased’s super doesn’t automatically fall under the will.

That surprises people because super is often one of the largest assets they own. In Australia, superannuation assets totalled about $3.9 trillion as at 30 June 2023 according to the Expand death benefit nomination fact sheet. For many families, the super balance can be as important as the family home, and sometimes more important from a cash flow and tax perspective.

A simple way to think about it

A binding death benefit nomination, or BDBN, is a written direction to your super fund trustee. If it’s valid, the trustee is legally required to distribute your death benefit to the eligible people or to your legal personal representative in the proportions you’ve nominated.

The easiest analogy is this. Think of your BDBN as a sealed instruction letter handed directly to your super fund. If the letter is valid and properly delivered, the trustee must follow it.

Without that letter, the trustee usually has discretion. They may consider your wishes, your family circumstances and the fund rules, but they’re still making the call.

Why people get caught out

People often confuse three separate things:

- Their will

- Their super account

- Their super death benefit nomination

Those aren’t the same document, and they don’t always work together automatically.

A will can control assets in your estate. Super is held by the trustee of your fund. Unless your super is directed into your estate through a valid nomination to your legal personal representative, it may sit outside your will entirely.

Practical rule: If your super is important to your family’s financial security, treat it as a separate estate planning task, not an afterthought.

The practical consequence

If your instructions are missing, invalid or out of date, the people you intended to benefit may not receive your super in the way you expected. That can create delay, tension and tax consequences at the same time.

If you want a broader explanation of the estate planning side, this guide on what happens to super when you die is a useful companion.

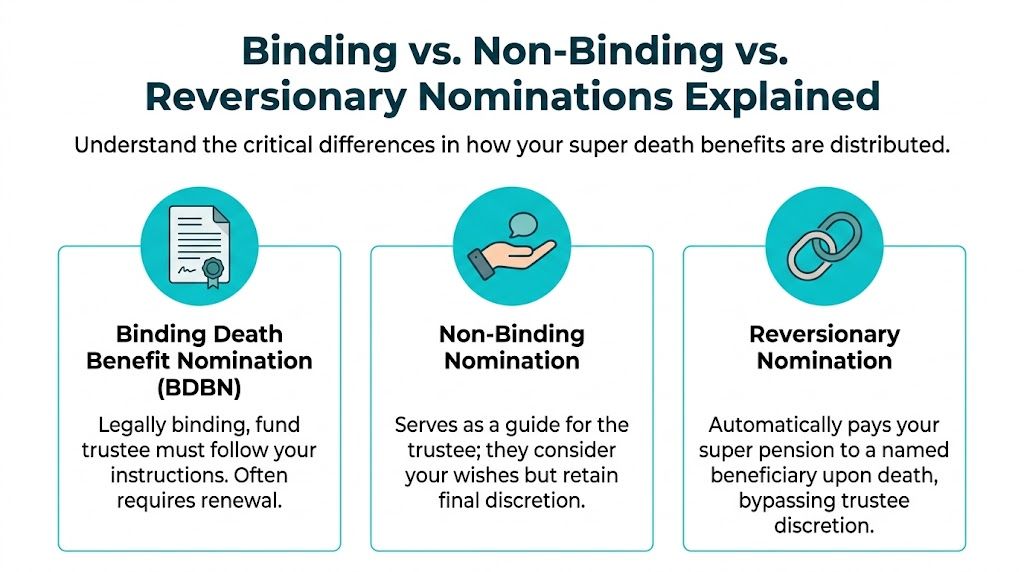

Binding vs Non-Binding vs Reversionary Nominations Explained

Not every nomination gives you the same level of control, a fact that can trip up many smart people. They’ve filled in a form at some point, but they’re not sure whether it was binding, non-binding, or linked to a pension.

The differences matter because the trustee’s role changes depending on the nomination type.

According to Treasury discussion paper material cited in the brief, only 28% of public offer super fund members had lodged any death benefit nomination by 2023, and BDBNs made up only about 15 to 20% of those. The same material notes $33.5 billion in annual death benefits paid in FY2022/23. You can see why this matters in practice when so much is being paid and many members haven’t lodged clear instructions through the Treasury discussion paper link.

The core differences

| Option | What it does | Trustee discretion | Best suited to |

|---|---|---|---|

| Binding nomination | Directs the trustee to pay as instructed, if valid | Very limited | People who want certainty |

| Non-binding nomination | Tells the trustee your preference | Trustee keeps the final say | Simpler family situations where flexibility is acceptable |

| Reversionary nomination | Continues a pension to a nominated dependant automatically | Reduced in the pension context | People already drawing a super pension |

Binding nomination

A BDBN is the strongest instruction of the three.

If it’s valid, the trustee must follow it. That makes it especially useful for people who want control over who receives their super and in what proportions.

It’s often the right tool for:

- Blended families, where assumptions can lead to conflict

- Pre-retirees, where super may sit outside the estate plan unless directed properly

- Business owners, where liquidity for family members matters

- People with clear beneficiary intentions, especially if they don’t want the trustee weighing competing claims

Non-binding nomination

A non-binding nomination is closer to a recommendation. You’re telling the trustee who you’d like to receive the benefit, but you’re not removing the trustee’s decision-making power.

That doesn’t mean it’s useless. In some cases, flexibility can help. But it does mean the final outcome may not match your expectations.

A lot of members think they’ve “done their nomination” when in fact they’ve only lodged a non-binding preference.

A nomination form is only as powerful as the legal effect attached to it.

Reversionary nomination

A reversionary nomination usually applies to a pension account, not an accumulation account. If you’re already receiving an income stream from super, a reversionary nomination can allow that pension to continue automatically to a nominated dependant after death.

This is different from a BDBN. It isn’t just naming a beneficiary for a lump sum. It’s directing what happens to the pension itself.

The practical test to use

If you’re unsure what you have, ask three questions:

- Is my nomination binding or only a preference?

- Does it apply to my accumulation account, my pension account, or both?

- Does it expire?

Those three questions uncover most of the misunderstandings advisers see in this area.

The Legal Framework Getting Your BDBN Right

A BDBN only works if it’s valid. That sounds obvious, but it’s where many problems begin.

The legal rules are strict because a BDBN is meant to remove trustee discretion. If a nomination doesn’t meet the fund’s requirements and the broader legal framework, it can fail.

Who you can nominate

Under the SIS framework described in the verified material, a valid BDBN can direct your super death benefit to:

- Eligible dependants

- Your legal personal representative, meaning your executor or estate administrator

A common mistake people make is assuming they can nominate anyone they like in the same way they can leave assets under a will. Super doesn’t work that way.

Eligibility matters. So does the exact way the nomination is completed.

The checklist that matters

For many public offer and retail or industry funds, a BDBN must be completed with precision. Common requirements include:

- Using the fund’s form rather than a homemade version

- Nominating eligible recipients only

- Allocating the benefit in proportions that total exactly 100%

- Signing the form correctly

- Having it witnessed properly

- Making sure the trustee receives it before death

The witnessing step catches people out more often than it should. The verified material states that improper witnessing is one of the common reasons nominations fail, and industry audits estimate 20 to 30% of BDBNs are invalidated in these circumstances, as noted in Toyne Accountants’ explanation of binding death benefit nominations.

Lapsing and non-lapsing

For most retail and industry funds, BDBNs are lapsing. That means they expire after three years unless renewed, according to the same Toyne material.

That expiry date holds greater significance than commonly understood. A form that was valid when you signed it may later stop having any binding effect at all.

By contrast, non-lapsing nominations can remain in force until revoked or changed, but they’re not available in every structure and often depend on the rules of the fund or trust deed.

If your fund uses a lapsing nomination, diarising the renewal date is part of the job. Signing the form once isn’t enough.

Where legal and estate planning overlap

A valid BDBN doesn’t replace your will. It needs to work with it.

If your estate planning documents don’t line up, your family can end up dealing with a mismatch between your will, your super nomination and the practical realities of your household. That’s one reason people reviewing their estate plan should also understand what happens if you don’t have a will, because super disputes often sit alongside broader estate confusion.

Costly Mistakes Common Pitfalls and Tax Traps of BDBNs

The expensive mistakes aren’t usually dramatic at the start. They look small. An old form. A missing witness. A nomination made before a divorce. A child who’s now an adult and financially independent. Then someone dies, and the consequences become very real.

That’s why a BDBN should never be treated as set-and-forget paperwork.

The tax trap many families miss

One of the biggest problem areas is the difference between a dependant for super death benefit purposes and a person you wish to benefit.

The verified data states that nominating non-dependants, such as adult children who are not financially dependent, can trigger 15 to 30% tax on the taxable component of the super death benefit. It also states that 25% of super death benefit disputes involve tax issues, particularly in blended families, and that an invalid BDBN can lead to an unintended 32% tax hit according to the material linked from Monaco Solicitors’ discussion of binding and non-binding nominations.

That surprises people because they assume “my child” automatically means “tax-free”. In super, it often doesn’t.

Common mistakes that create problems

- Old family circumstances: Marriage, separation, divorce, new children and stepchildren can all change what “fair” and “intended” look like.

- Wrong beneficiary choice: A person may be emotionally important to you but not qualify under super law.

- Invalid execution: A form can fail because of witness issues, incorrect completion, or using the wrong document.

- No coordination with the will: A nomination to the estate can be useful, but only if the will then directs the estate in the way you want.

- No review after retirement changes: Starting a pension, consolidating funds or moving to an SMSF can all change what documentation is needed.

Blended families need special care

Blended families often bring the hardest questions.

A person may want to provide for a current spouse while also protecting children from an earlier relationship. If the nomination is vague, outdated or legally ineffective, the trustee may need to weigh competing claims. Even when everyone acts in good faith, people can have completely different views about what the deceased “would have wanted”.

The emotional problem and the tax problem often arrive together. That’s why blended family super planning needs precision, not assumptions.

Tax and estate planning need to work together

For some families, directing the benefit to the legal personal representative can support broader estate planning. For others, a direct nomination to an eligible dependant may be more suitable. The right answer depends on family structure, tax position and the wording of the will.

If super forms part of a broader estate strategy, this overview of CGT and deceased estates helps explain why death benefit planning shouldn’t happen in isolation from tax planning.

Binding Nominations in Action Real-World Examples

The rules make more sense when you see how they play out in real life.

Example one

Leanne is in her early sixties, recently remarried, and has two adult children from her first marriage. She wants her spouse to have immediate financial security, but she also wants her children to benefit from wealth she built long before the second marriage.

Her will reflects that intention. The problem is that her super won’t necessarily follow the will unless she gives the fund valid directions.

Leanne reviews her super arrangements and makes a fresh binding nomination aligned with her current family situation and the rest of her estate plan. She checks that the nominated recipients are appropriate, that the percentages are correct, and that the form is executed exactly as the fund requires.

When she dies, there’s no need for the trustee to guess. Her super is distributed according to the nomination. Her family doesn’t have to debate what she meant, and they’re not left trying to interpret old paperwork from another stage of life.

Example two

Aaron owns a small business. He’s organised in most areas and has a will, insurance and a good accountant. Years earlier, he completed a binding nomination through his public offer fund.

Then life got busy. The business expanded. His focus shifted. The nomination lapsed and no one noticed.

After Aaron’s death, his family assumes the old nomination still applies. It doesn’t. The trustee now has discretion. Family members point to conversations Aaron had over the years. The will says one thing. The super fund process asks different questions. Tension builds because the written instruction everyone relied on is no longer binding.

The issue isn’t that Aaron ignored planning. It’s that he thought one completed form solved the problem permanently.

The lesson in both stories

The first example isn’t about luck. It’s about alignment.

The second isn’t about recklessness. It’s about false confidence.

Both people cared about their families. Only one had current, effective documentation that matched the legal rules of the fund at the time it mattered.

Your Step-by-Step Guide to Securing Your Super Legacy

If you want to get this sorted, keep the process practical. Don’t start with theory. Start with the exact fund and the exact form.

Step one get the right form

Contact each super fund you hold and ask for its binding death benefit nomination form.

Don’t assume one form covers every account. If you have multiple funds, each fund may have its own process.

Step two confirm who can be nominated

Before filling anything in, check who the fund allows you to nominate under the law and the fund rules.

If you’re considering nominating your legal personal representative, make sure your will is current. If you’re nominating individuals, make sure they’re eligible and that the intended distribution is clear.

Step three complete the allocations carefully

Your allocation needs to be exact.

If the form requires percentages, they must total 100%. Small errors can create big problems later, especially where more than one beneficiary is involved.

Step four get the witnessing right

This isn’t the place to cut corners.

The verified material notes the importance of proper witnessing by two non-beneficiary adults over 18 signing simultaneously in the relevant context. If your fund has additional procedural requirements, follow them exactly.

Keep a quiet half hour aside for this. Most nomination errors happen when people rush an important document between other tasks.

Step five lodge it and confirm receipt

Once the form is signed, witnessed and complete, send it to the fund using the method they require.

Then confirm the trustee has received and accepted it. Keep copies with your estate planning documents and let your executor know where they are.

Step six review it regularly

Review your nomination when life changes. Also review it if your fund changes, if you start a pension, or if your family structure changes.

A simple annual review habit can save your family from the mess caused by an outdated form.

A quick review list

- Check the fund name: Has your super been rolled over or consolidated?

- Check the nomination type: Is it binding, and is it still current?

- Check the people named: Would you still choose them today?

- Check the estate plan: Does the nomination still fit your will?

- Check your records: Can your executor find the documents easily?

Take Control of Your Wealth Plan with Confidence

A BDBN is powerful because it can turn your intentions into enforceable instructions. It’s also unforgiving, because small mistakes can undo the result you wanted.

That’s especially true when your situation is more complex than a simple spouse-only arrangement.

When DIY becomes risky

You should be particularly careful if any of these apply:

- You have a blended family

- You own an SMSF

- You’re a business owner with succession concerns

- You’re approaching retirement and drawing a pension

- You want your super planning to work with testamentary trust planning

- You’re concerned about tax for adult children or other non-dependants

SMSFs deserve special mention. The verified material states that deed mismatches and related issues contributed to an 18% rise in SMSF disputes over invalid nominations in WA between 2024 and 2025, and that 60% of SMSF owners may lack a valid BDBN, according to the material cited from Rudd Mantell’s explanation of binding death benefit nominations.

That doesn’t mean every SMSF nomination is unsafe. It does mean the deed, the nomination wording and the administrative process all need to line up.

What good advice actually does

Good advice in this area isn’t just “fill in this form”.

It means someone helps you:

- identify whether your current nomination is binding

- check whether your chosen beneficiaries are appropriate

- assess whether nomination to the estate or direct nomination is better suited

- coordinate your super instructions with your will

- review tax risks before your family inherits a problem

- make sure lapsing nominations don’t expire

- review SMSF deed rules where relevant

Why this matters in WA

For many WA families, especially pre-retirees, executives and business owners, super is too significant to leave to assumptions. Family structures can be complex. Asset pools can be split across entities. Verbal intentions rarely carry legal weight when documents are missing or flawed.

The people left behind don’t need more ambiguity. They need clear instructions and a plan that holds up under pressure.

If you’ve been asking what is a binding death benefit nomination, the answer is simple. It’s a legal direction for your super. The harder question is whether yours is valid, current and properly integrated into your wider wealth plan.

If you want clarity on whether your current super nomination will do what you intend, Wealth Collective can help you review it in the context of your broader strategy. Whether you’re preparing for retirement, managing a blended family, running an SMSF or trying to protect your family from unnecessary tax and dispute, a short conversation can identify the gaps quickly. Book a free 10-minute introductory call and get clear on the next step.