Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Income protection insurance replaces part of your income if illness or injury stops you working. In Australia, that usually means a monthly benefit based on your recent earnings, with examples of 75% or 90% of pre-tax income and the calculation commonly based on the 12 months before you became unable to work.

If you're a busy professional or business owner, that matters more than many appreciate. Your car can be insured. Your home can be insured. Your ability to earn an income is often the engine that pays for everything else, from the mortgage to school fees to the steady progress you're making with super and investments. When that engine stalls, the financial pressure can start quickly.

Individuals often first look into this after a trigger moment. A colleague goes off work unexpectedly. A new mortgage settles. A baby arrives. A business starts depending more heavily on one owner's output. At that point, the question stops being abstract. It becomes practical. If you couldn't work for a while, what would keep the cash flow going?

What Is Income Protection Insurance Exactly

Income protection insurance is a policy that pays a monthly benefit if illness or injury leaves you unable to work for a period of time.

For an Australian professional, that is less about abstract insurance theory and more about a practical question. If your income paused next month, what would keep the mortgage, rent, school fees, business overheads, and everyday spending running without forcing a major reset?

What problem it solves

Income protection exists to protect cash flow while your health is affecting your ability to earn. It is designed to reduce the financial strain of being temporarily out of action, not to create a lump sum windfall.

That distinction matters because many people assume insurance only responds to the worst-case event. In practice, income protection is often about keeping ordinary life on track during a difficult stretch. The aim is stability. Bills still get paid. Plans do not need to be abandoned at the first interruption to your income.

A simple way to frame it is this. Your income funds the rest of your financial life. If that income stops, even a well-organised household can feel pressure quickly.

What it usually pays

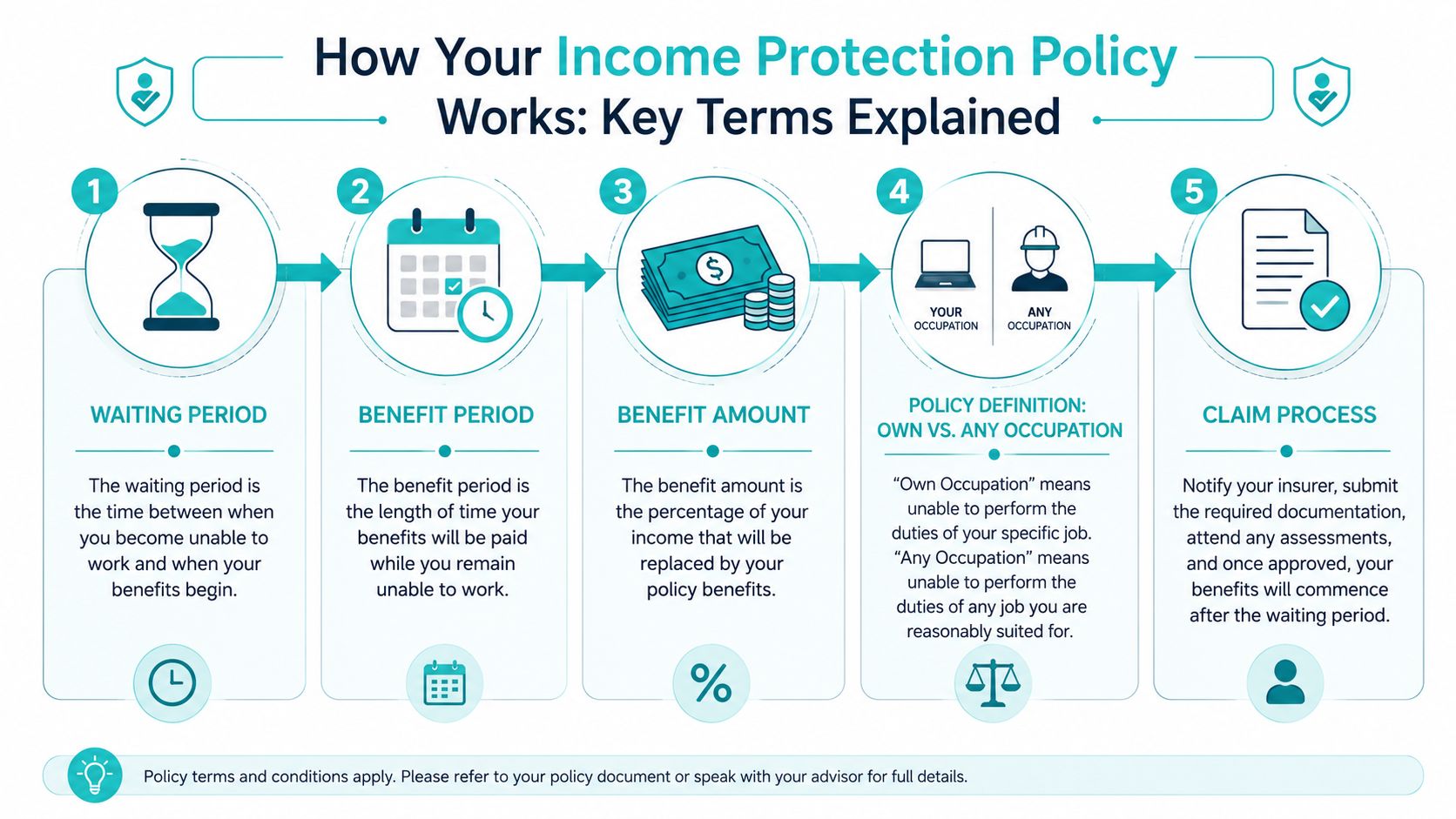

The benefit is usually a percentage of your pre-disability earnings, paid monthly, subject to the policy terms and how your income is assessed.

That sounds straightforward until you look at how different Australians get paid.

If you are a salaried employee on a stable PAYG income, the calculation is often easier to follow. If you are self-employed, paid partly through dividends, receive bonuses or commissions, or run a business with uneven profits through the year, the main decision is not just whether to get cover. It is how the policy defines income, and whether that definition matches the way money reaches you.

That is often the point where confusion starts. Two people can each earn a strong income and still need very different policy structures.

Why the details matter early

A doctor, consultant, tradie, and company director may all ask the same opening question, but the useful follow-up questions are different. Is your income steady or seasonal? Would you hold the cover personally or through super? How long could you cover expenses from savings before you needed the policy to start paying? If you want a plain-English primer on one of those moving parts, understanding coverage waiting periods is a helpful place to start.

At Wealth Collective, we often find that people do not need a more complicated definition. They need a clearer link between the product and the choices in front of them.

So the cleanest answer to "what is income protection insurance?" is this. It is insurance designed to replace part of your income for a period if sickness or injury stops you working, with the right setup depending heavily on how you earn, how much flexibility you have, and whether the cover sits inside super or outside it.

How Policies Work Key Terms Explained

Once you understand the basic idea, the next step is knowing what determines the policy you buy. This knowledge influences whether good cover fits neatly into your life or leaves awkward gaps.

Waiting period

The waiting period is the time you must be off work before benefits start. Think of it as the excess on a car policy, except measured in time rather than dollars.

A shorter waiting period can mean the policy starts helping sooner. A longer waiting period usually means you'll need more savings, leave entitlements, or cash reserves to bridge the gap yourself.

If this part feels fuzzy, this guide on understanding coverage waiting periods gives a useful plain-language explanation of how waiting periods work across insurance products.

Benefit period

The benefit period is how long the insurer can keep paying once a claim is accepted and the policy conditions continue to be met.

This is one of the biggest real-world choices in a policy. Some people mainly want help through a medium-term disruption. Others want cover structured for a much longer interruption to earning capacity. The right answer usually depends on your debts, family commitments, cash reserves, and whether one income supports multiple people.

How your income is measured

Many professionals and business owners require more than a generic explainer. A major underserved angle in Australia is how income protection works for contractors, small-business owners, commission-based staff, and people with variable income, because real-world coverage depends on policy structure and how benefit amounts are calculated from pre-disability income rather than a simple fixed salary, as noted in this background explanation of income protection insurance.

For non-standard earners, the practical questions are usually things like:

- What counts as income: Is it salary, drawings, commissions, or business profit?

- How is it proven: Will the insurer rely on tax returns, payslips, financial statements, or a combination?

- What if income has recently changed: If a business has grown quickly, does the policy reflect current reality or a historical average?

The policy wording matters most when your income doesn't arrive in a neat, predictable fortnightly amount.

Indemnity, agreed value, and partial benefits

You may also hear terms like indemnity and agreed value. In plain language, these relate to how the insurer determines what you can be paid at claim time. The detail can be technical, but the practical takeaway is simple. You want to know whether the benefit is locked in ahead of time or reassessed against income evidence when you claim.

Then there's partial disability or partial benefits. This can matter a lot if you can return to work in a reduced capacity rather than all at once. A policy with sensible partial disability terms can support a gradual comeback instead of forcing an all-or-nothing outcome.

Occupation definition

One more term deserves attention. The policy's definition of being unable to work.

Some policies assess whether you can perform your own occupation. Others use broader wording. For a surgeon, pilot, tradesperson, or specialist professional, that distinction can be significant because your earning power may depend on doing a very specific role, not just any role.

Income Protection vs TPD and Life Insurance

People often bundle these covers together as “personal insurance”, but they do different jobs. One isn't a substitute for the others.

| Feature | Income Protection | TPD Insurance | Life Insurance (Death Cover) |

|---|---|---|---|

| Main trigger | Illness or injury prevents you from working under the policy terms | Permanent disability under the policy definition | Death |

| How it pays | Monthly benefit | Lump sum | Lump sum |

| Primary purpose | Help cover ongoing living costs while income is interrupted | Help fund major long-term financial adjustments | Help support dependants and estate needs after death |

| Best suited to | Cash flow protection during a period away from work | Bigger structural needs such as debt reduction or care planning | Family protection and legacy planning |

| How to think about it | Replaces part of your earnings for a period | Helps if work capacity is lost on a lasting basis | Protects others financially if you die |

Income protection is about income continuity. TPD is about the financial impact of a more permanent loss of working capacity. Life insurance is about protecting the people and plans that depend on you if you're no longer here.

That's why many people hold these covers together rather than choosing one “winner”. Each one addresses a different risk.

If you want a deeper look at the second category, this guide to total and permanent disability insurance explains how TPD works and where it fits.

A simple way to frame it is this. Income protection helps pay the bills while life keeps moving. TPD and life cover deal with bigger permanent financial consequences.

The Financials Tax Super and Costs

A practical question sits underneath the tax and cost discussion. If your income stopped for a few months, would you rather pay premiums from your day-to-day cash flow now, or from your super balance over time?

Inside super or outside super

In Australia, income protection can sit inside super or outside super through a policy held directly with an insurer. Both can work. The better fit depends on what you are trying to protect and how you want the cost to be funded.

Holding cover inside super can feel easier because premiums may be deducted from your super balance rather than your bank account. The trade-off is straightforward. Money going to premiums is money not staying invested for retirement.

Cover held outside super keeps that cost separate from retirement savings and may offer more room to tailor the policy. That can matter if your income is uneven, you receive bonuses or distributions, or you want more control over features and ownership.

Default cover through super deserves a closer look too. It is convenient, but convenience is only the starting point. If you changed jobs, became self-employed, took on a large mortgage, or now support a family, the cover you were switched into years ago may no longer match your situation.

Why structure matters

Policy structure affects more than where the premium is paid. It can shape how suitable the cover is for your work pattern, tax position, and long-term plans.

A salaried employee with predictable PAYG income often has a simpler decision. A business owner or contractor usually does not. If your income comes from a mix of salary, trust distributions, retained profits, or fluctuating revenue, the definition of income and the way it is assessed become much more important.

That is why the right question is rarely, “Do I have cover?” A better question is, “If I could not work, would this policy calculate my benefit the way I expect?” Personalized advice can also help compare direct cover, super-based cover, and any existing default policy side by side. For a practical look at one part of that decision, see this guide to the income protection insurance tax deduction.

What affects the cost

There is no standard price tag because insurers are pricing both you and the policy design.

Common factors include:

- Your occupation: Physical work, hazardous duties, and specialised roles are often assessed differently from office-based roles.

- Your age and health: Current health, medical history, and lifestyle factors can affect premiums and underwriting terms.

- Waiting period and benefit period: A longer waiting period can reduce cost. A longer benefit period usually increases it.

- How your income is earned: Straight salary is usually simpler to verify than business income, commission, or irregular drawings.

- Policy features and definitions: Added options, stronger definitions, and policy flexibility can change the premium.

Cheap cover can create an expensive problem if the policy does not fit your actual income or working arrangement.

For Australian professionals, the financial decision is rarely just about finding the lowest premium. It is about balancing current cash flow, the effect on super, tax treatment, and whether the policy is built for the way you earn. That is often the point where a short conversation with an adviser saves a lot of guesswork.

Understanding Exclusions and the Claims Process

Insurance becomes much less intimidating when you know two things up front. What the policy may not cover, and what happens if you need to claim.

Common exclusions

Every policy has exclusions, limits, and definitions. That isn't a sign the product is flawed. It's how the contract is built.

Common exclusions can relate to areas such as:

- Pre-existing conditions: Some conditions may be excluded or specially treated depending on your medical history and underwriting outcome.

- Self-inflicted harm: Policies commonly place limits around these circumstances.

- Specific activities: Certain hazardous pursuits or work situations may not be covered in the standard way.

- Non-disclosure issues: If important health, occupation, or income information wasn't disclosed properly, that can affect a later claim.

The fine print matters here. So does the quality of the application.

If you want a practical overview of these boundaries, this article on what income protection does not cover is a helpful companion piece.

What claiming usually looks like

When readers ask me what the claims process feels like, the honest answer is this. It's administrative, medical, and often emotional, because it usually happens when you're already dealing with a hard situation.

The process usually follows a sequence like this:

- You notify the insurer that you may need to claim.

- Medical evidence is gathered from your treating doctors or specialists.

- Income evidence is provided so the insurer can assess the benefit under the policy terms.

- The insurer assesses the claim against the wording, definitions, and supporting documents.

- Payments begin if the claim is accepted and the waiting period conditions are met.

Why support matters

A claim isn't just a form. It's a process that asks you to connect health evidence, work capacity, and financial records in a clear way.

That's one reason many people prefer not to set these policies up on guesswork alone. A well-structured policy can be easier to understand at claim time, and good advice at application stage can reduce avoidable problems later.

Making the Right Choice for Your Situation

The right policy depends less on the label and more on your circumstances. Income pattern, debt level, family responsibilities, and job risk all pull the design in different directions.

Three common scenarios

A self-employed tradie usually has two risks at once. Personal income stops, and business momentum may also slow. That person often needs close attention on waiting period, occupation wording, and how income will be evidenced if a claim arises.

A dual-income couple with a large mortgage may be less worried about replacing every dollar and more focused on keeping the household stable if one person is off work. The question becomes how much cover is enough to keep the essentials moving without overpaying for features they're unlikely to use.

An executive on a high base salary plus bonus might need to examine how variable remuneration is treated. The headline income can look strong, but the policy only works properly if the benefit calculation reflects how that person is paid.

The decision points that matter

When you compare options, start with the choices that most affect outcomes:

- How long could you self-fund: This helps shape the waiting period.

- How predictable is your income: This affects how closely you need to review definitions and income evidence requirements.

- How specialised is your role: Occupation wording matters more when your job isn't easily interchangeable.

- Where is your current cover held: Existing super cover may be useful, but it still needs to be tested for fit.

A useful outside perspective on disputes is this piece from Melanson Law Group on claim denials. It isn't Australian advice, but it does highlight a timeless point. Claim problems often trace back to definitions, documentation, and policy fit.

Good insurance decisions usually happen before you buy. Bad surprises usually happen when nobody checked the details.

Personal insurance is one of those areas where “good enough” can be misleading. The cover that suits an employee on a fixed salary may not suit a practice owner, contractor, or family with uneven cash flow. That's why a short conversation with an adviser is often the fastest way to narrow the field and avoid expensive assumptions.

Your Income Protection Questions Answered

Can I get income protection if I'm self-employed

Yes, self-employed people can often get cover, but the important issue is how the policy measures your income and what documents will be needed to support a claim. If your earnings vary, that needs careful attention at application stage.

What happens if I change jobs

Your policy may still continue, but a job change can affect whether the cover remains appropriate. A move from office work into a more physical role, or from salary into self-employment, can change the risk profile and the way the policy should be structured.

Does income protection cover mental health conditions

Some policies may cover mental health conditions, subject to the wording, underwriting decisions, and the strength of medical evidence. This is one of those areas where broad assumptions can cause trouble, so it's worth checking the specific terms carefully.

Is cover through my super fund enough

Sometimes it is. Sometimes it isn't. Default cover can be a useful starting point, but it may not reflect your current income, role, or personal obligations. The main question isn't whether you have cover. It's whether the cover is suitable.

Do I need income protection if I have savings

Savings and income protection do different jobs. Savings help with flexibility and short-term resilience. Insurance is there for the risk that the interruption lasts longer, costs more, or arrives at the worst possible time.

What's the smartest next step

Get clear on your current cover, your monthly commitments, and how your income is earned. Then have someone stress-test the setup against your real-life risks, especially if you're self-employed, paid partly by commission, or relying on super-based default cover.

If you want help working out what income protection should look like for your situation, book a conversation with Wealth Collective. A short initial chat can help you understand whether your current cover is appropriate, where the gaps may be, and what questions to ask before making a decision.