Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Only 1 in 3 Australians have formally planned for long-term care needs and costs according to the Australian Institute of Health and Welfare. That should worry every family in Western Australia.

Aged care planning is still often treated as something you deal with after a health event. That's backwards. Aged care is not just a care decision. It's a cash-flow decision, an asset decision, a legal decision, and often a family conflict decision if nobody plans early.

I've seen the same mistake over and over. Families wait until Mum falls, Dad's memory slips, or a hospital discharge forces a rushed choice. At that point, options narrow, paperwork piles up, and perfectly good assets get handled badly. The pressure isn't only emotional. It's financial.

Good aged care planning gives you control. It helps you protect retirement income, make cleaner decisions about the home, reduce avoidable stress for adult children, and document who will act if capacity changes. Done properly, it turns a crisis into a process.

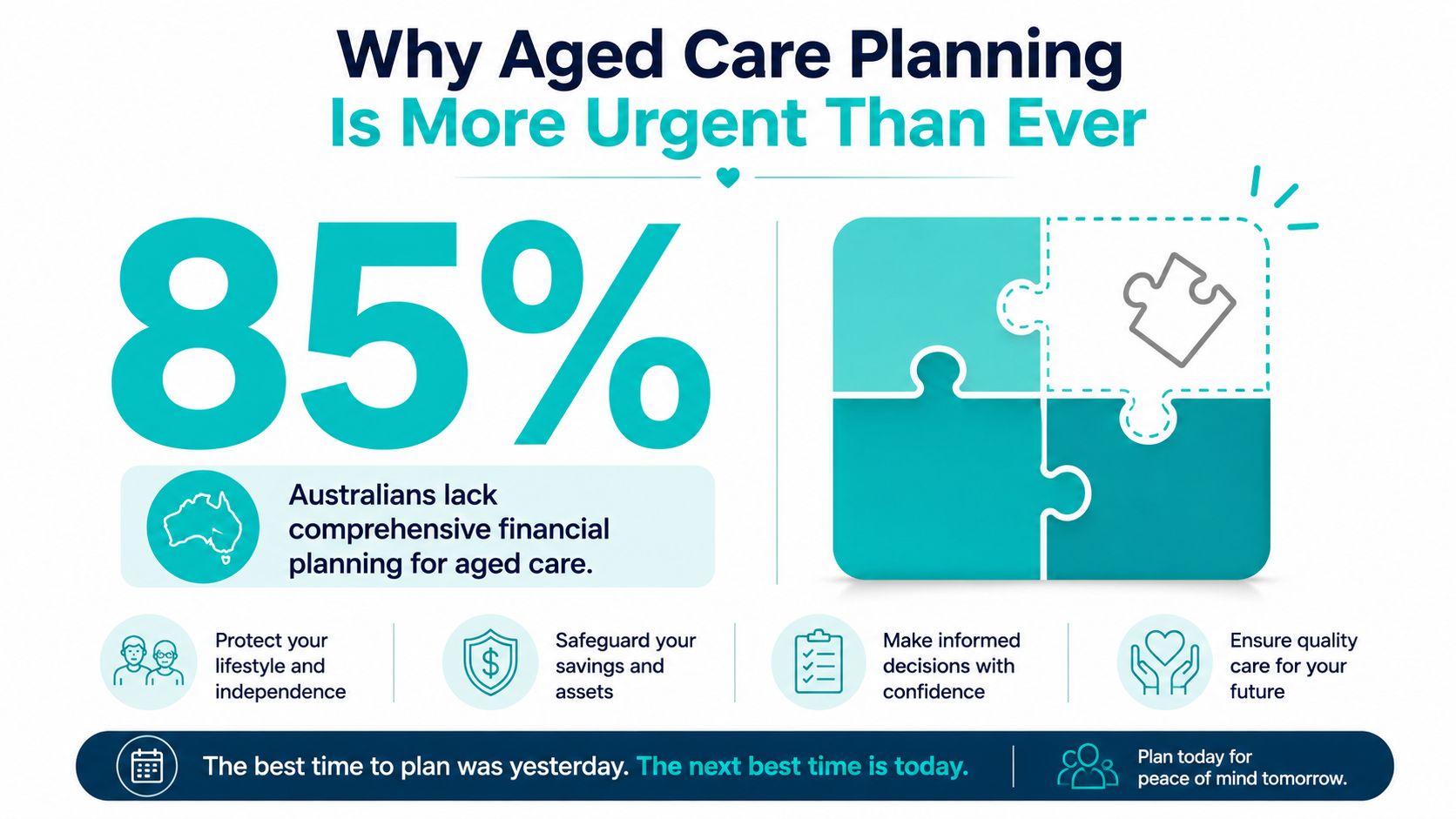

Why Aged Care Planning Is More Urgent Than Ever

Only 1 in 3 Australians have formally planned for long-term care needs and costs. For the other two-thirds, aged care often arrives as a financial shock, not a managed transition.

That is the problem. Families still treat aged care as a future health issue, when it is often one of the biggest late-life financial decisions they will make. Delay usually means less choice, more pressure, and expensive mistakes with the home, cash flow, and family decision-making.

The primary risk isn't just about care

People often focus on beds, providers, and paperwork. Fair enough. But the harder questions are financial, and they arrive fast:

- Income: Can ongoing care fees be covered without cutting the surviving spouse's lifestyle?

- Cash access: Is there enough liquidity if a lump sum or urgent accommodation payment is required?

- Property: Does keeping the home still make sense, or is it draining options?

- Authority: Who can act legally and financially if capacity changes?

These are wealth decisions. Leave them unresolved and the family ends up making high-stakes calls in a hospital room, after a fall, or during a discharge deadline. That is when people sell the wrong asset, draw money from the wrong structure, or lock themselves into a poor arrangement because they ran out of time.

Practical rule: If a care event would force a rushed property or investment decision, your plan is not finished.

WA families also face a practical problem. Distance matters. Regional and remote households can have fewer providers, longer waiting times, and more pressure to accept the first workable option. That makes financial preparation more important, because flexibility buys time and better choices.

If care at home is the likely first step, understand how the aged care support at home program fits into the broader funding and planning picture. Do that early, before urgency takes over.

At Wealth Collective, we treat aged care planning as part of a serious advice framework alongside retirement income, super, tax, and estate planning. That is the right approach. Good planning protects wellbeing, but it also protects family wealth from avoidable erosion. Start before the decision is urgent. That is how you keep control.

Understanding Care Needs and Australian Options

The first useful step in aged care planning isn't comparing brochures. It's getting clear on what help is needed now, and what's likely to be needed later.

A practical care plan starts with a formal needs assessment that maps current and expected limits in daily living, then turns that into a written plan covering tasks, responsible people, and timing, as outlined in this elder care planning guide. That sounds simple, but most families skip it and go straight to reacting.

Start with the assessment, not the assumption

Families often say, “Mum only needs a bit of help.” Then a few months later they're juggling medications, falls risk, transport, meal prep, and decision-making. A proper assessment forces clarity.

Focus on practical questions such as:

- Daily living: Can the person manage bathing, dressing, meals, mobility, and medication safely?

- Home safety: Is the current home still workable, or is it becoming part of the problem?

- Carer strain: Is a spouse or adult child shouldering too much?

- Future progression: Is the current issue likely to stay stable, or become more demanding?

Write it down. Verbal understandings fall apart quickly when multiple relatives are involved.

The main care pathways

Most families are deciding between support at home and residential aged care, with some movement between the two over time.

Support at home

This suits people who want to remain in familiar surroundings and can still do so safely with help. Support may include personal care, domestic help, nursing input, mobility support, or respite for a family carer.

If you want a plain-English overview of one of the emerging home-based pathways, this guide to the aged care support at home program is a useful starting point.

Home care often feels emotionally easier. It can also be financially deceptive if nobody tracks ongoing out-of-pocket costs, home modifications, transport, and informal carer burnout.

Residential aged care

Residential care becomes relevant when home is no longer safe, practical, or sustainable. That may happen because of frailty, cognitive decline, complex medical needs, or because the family support system has reached its limit.

This option gives structure and regular support, but it also introduces larger funding decisions and more formal means-testing. That's where many families first realise aged care planning is really financial planning.

A clear care recommendation is better than a vague promise that “we'll manage somehow”.

Turn care needs into a shared plan

A workable aged care plan should answer three things:

- What support is needed

- Who is responsible for each part

- When the arrangement gets reviewed

That last point matters. Care needs don't stay still. A plan that worked after one hospital discharge may be wrong six months later.

Decoding Aged Care Costs and Payment Structures

Aged care planning gets expensive fast. Families run into trouble when they do not know what must be paid, when it falls due, and which assets will carry the load.

Treat this as a funding strategy, not an admin exercise. The fee structure shapes cash flow, pension outcomes, investment decisions, and what your family keeps over time. Get it wrong and you can force an unnecessary asset sale, strain the spouse still living at home, or lock in a payment method that looked simple but was never affordable.

The cost categories families need to understand

Aged care fees usually sit across several layers, and each one affects your plan differently.

Everyday care charges

These are the ongoing costs tied to daily living and care delivery. Many families fixate on accommodation and overlook the recurring fees. That is a mistake, because recurring fees are what test monthly affordability.

If the income plan cannot comfortably support those charges, the strategy is already weak.

Means-tested contributions

Government support depends on your financial position, so income and assets directly affect what you pay. Strategy becomes critical at this point. The same pool of wealth can lead to very different results depending on who owns the assets, how they produce income, how liquid they are, and whether changes are made before or after entry into care.

If you want an early sense of how retirement entitlements may interact with these decisions, use this Age Pension eligibility calculator before getting personal advice.

Families who are also comparing broader asset-protection approaches often read about protecting assets from nursing home costs, but Australian aged care rules are different. Use overseas content as a prompt for questions, not as a plan.

Accommodation costs

This is usually the most confusing part of residential care. The main decision is whether to pay accommodation as a Refundable Accommodation Deposit (RAD), a Daily Accommodation Payment (DAP), or a mix of both.

RAD versus DAP at a glance

A RAD is usually paid as a lump sum. A DAP is an ongoing payment charged instead of that lump sum. The right choice depends on available cash, expected investment returns, Centrelink treatment, estate goals, and whether keeping the home still stacks up financially.

| Feature | Refundable Accommodation Deposit (RAD) | Daily Accommodation Payment (DAP) |

|---|---|---|

| How it's paid | Lump sum accommodation payment | Ongoing periodic accommodation payment |

| Cash flow impact | Reduces available capital upfront | Preserves capital but increases ongoing expenses |

| Estate considerations | Balance is typically treated as refundable to the estate, subject to the relevant rules and deductions | No lump sum balance to be refunded in the same way |

| Best suited to | Families with strong liquidity or a clear asset strategy | Families who need to retain capital or avoid selling assets immediately |

| Main risk | Ties up a large amount of money | Can place sustained pressure on retirement cash flow |

| Common mistake | Paying a large lump sum without modelling future income needs | Choosing ongoing payments without testing how long they remain affordable |

Don't make the RAD decision in isolation

I'll be blunt. Families should not choose RAD or DAP based on pressure from a facility deadline, a relative's opinion, or a blanket rule about lump sums versus keeping cash. Those shortcuts destroy value.

A sound decision weighs:

- Liquidity needs: How much cash must stay available for the spouse or partner at home?

- Income sustainability: Will ongoing payments put retirement income under pressure?

- Asset sales: Are you forcing the sale of the wrong asset at the wrong time?

- Estate intent: Do you want to preserve flexibility for beneficiaries?

- Timing: Is this a permanent move now, or part of a staged path from home care?

The most expensive aged care decision is often the rushed one.

If you have not tested the effect on cash flow, tax, pension position, and estate outcomes, you are not planning. You are guessing.

Your Home and Assets in Aged Care Planning

For most WA families, the hardest question is simple: what do we do with the house?

That's also where poor aged care planning causes the most damage. Public discussion often focuses on care services. The bigger issue is funding strategy, including cash flow, liquidity, estate planning, accommodation deposits, and capital drawdowns, as noted in this guide on building a master plan for ageing.

The family home is emotional, but the decision must be strategic

Families often treat the home as untouchable. I understand why. It holds history, identity, and security. But if keeping it creates cash stress, complicates means-testing, or leaves a spouse financially exposed, sentiment has taken over strategy.

The right decision usually sits in one of three paths.

Keep the home

This can work when there's a strong reason to retain it, enough liquidity elsewhere, and a clear understanding of the ongoing holding costs. But keeping the property without a funding plan is lazy planning. Rates, insurance, maintenance, vacancy risk, and delayed decisions can slowly drain the estate.

Rent the home

Renting can create income and buy time. It can also change the financial picture in ways families don't expect. Before choosing this route, understand how rental income and property ownership fit into the broader structure of retirement planning and exemptions such as the main residence exemption.

Sell the home

Selling can solve a liquidity problem quickly and cleanly. It may fund accommodation, reduce admin, and simplify the estate. It can also be the wrong move if done in a panic or before the family understands the downstream effects.

Other assets matter too

The house gets all the attention, but it's rarely the only lever. Families also need to review:

- Superannuation balances: Especially when one spouse is still in a different retirement phase or structure.

- Investment accounts: These may be better liquidity sources than property in some cases.

- Cash reserves: Adequate cash can preserve choice.

- Estate intentions: Asset selection affects both current affordability and what's left later.

Aged care planning works best when assets are treated as a coordinated system, not a pile of unrelated accounts.

A house is not a strategy. It's an asset. The strategy is how and when you use it.

If you want a broader legal perspective on shielding wealth from care costs, this article on protecting assets from nursing home costs is worth reading for general context. The legal rules differ by country, but the core lesson holds: asset decisions need to be intentional, documented, and made before a crisis.

Securing Your Wishes with Legal Documents

Aged care planning fails when the money is organised but the authority isn't.

I've seen families with decent assets, clear intentions, and no valid documents giving anyone power to act. Then capacity changes, a health decision is needed, and everything slows down. Banks, providers, and relatives don't run on assumptions. They run on paperwork.

The three documents that matter most

You need to know the role of each document and keep them current.

Enduring Power of Attorney

This gives a trusted person authority to handle financial matters if you lose capacity. That can include banking, bills, property transactions, and other financial administration.

Choose this person carefully. Competence matters as much as trust. A loving but disorganised child can create real problems.

Enduring Power of Guardianship

This deals with personal, lifestyle, and certain health-related decisions when you can't make them yourself. It's about who speaks for you on care, living arrangements, and day-to-day welfare issues.

That role shouldn't be handed out lightly. The right person is calm, reliable, and capable of handling pressure from siblings and professionals.

Advance Care Directive

This records your treatment preferences. It helps doctors, carers, and family understand what you want if you can't communicate those wishes later.

This document is about control. It spares relatives from guessing and reduces conflict when emotions are high.

Review them regularly

Plans and preferences change. Reputable guidance recommends reviewing the plan after major health or life changes and at least annually, particularly to maintain role clarity and communication, as noted in this advance care planning resource.

A legal document signed years ago isn't automatically a good document today. Relationships change. Capacity changes. The person you appointed at 55 may be the wrong choice at 75.

Make the documents work together

The legal side should match the financial and care plan. If one child is named to act financially, another is handling care decisions informally, and nobody has discussed the arrangement, conflict is almost guaranteed.

Keep the structure aligned by asking:

- Does each appointed person understand the role?

- Do the documents reflect current wishes?

- Have the family discussed the practical plan?

- Does the legal setup match the estate plan?

For a general overview of incapacity planning concepts, this article on planning for incapacity in Texas gives a useful comparison point, even though Australian legal documents and rules are different. For local strategy, estate planning should be part of the same conversation, not a separate afterthought. This overview of what estate planning involves is a useful place to start.

Your Aged Care Planning Checklist and Next Steps

Most families don't need more information. They need a clear order of action.

Aged care planning becomes manageable when you stop treating it as one giant decision and start treating it as a short list of linked decisions. Care needs, costs, assets, and legal authority all need to line up. If one piece is missing, the whole plan weakens.

Your practical checklist

Use this as the baseline.

- Clarify care needs: Get specific about current support requirements, likely progression, and whether home remains safe and realistic.

- Complete the formal assessment process: Don't rely on family assumptions. Eligibility and care pathways need to be grounded in a proper assessment.

- Map the funding plan: Work out how ongoing care, accommodation choices, and cash flow will be funded without derailing retirement security.

- Decide how assets will be used: Review the home, super, investments, and cash reserves as one coordinated pool.

- Lock in legal authority: Put the right documents in place and make sure the right people are named.

- Review regularly: Revisit the plan after major health, family, or financial changes.

What good planning actually looks like

It's written down. It identifies who does what. It reflects real numbers, actual assets, and clear legal authority. It doesn't assume siblings will “sort it out later”.

The best aged care plans don't just fund care. They protect the spouse at home, reduce pressure on adult children, and preserve choice.

If you're in WA and you know this has been sitting in the too-hard basket, don't wait for a hospital event to force the issue. A short planning conversation now is far better than a rushed family meeting later.

If you want clarity on aged care planning, retirement cash flow, the family home, and the legal pieces that need to align, speak with Wealth Collective. Their Retirement Roadmap process is built for exactly these decisions. Start with a free 10-minute introductory call and get a clear view of your next step.