Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You might be sitting in a home that once made perfect sense. Four bedrooms, a big garden, room for Christmas, room for the kids, room for all the things that came with busy family life. Now the children have moved out, the stairs feel a bit less appealing, and the maintenance list seems to grow faster than the weekend disappears.

That doesn't automatically mean you should sell.

But it does mean it's worth asking a better question. Not “Should I leave the family home?” but “Is this home still helping the retirement I want?” For many West Australians, downsizing in retirement isn't about giving something up. It's about turning a large, under-used asset into something more flexible, more manageable, and better aligned with the next stage of life.

Some people downsize to free up cash flow. Others want less upkeep, a better location, or a home that will be easier to live in as they age. Some stay put and instead modify the home to make it safer and more practical. If that's where your thinking is heading, it can help to secure your home for independent living before making any big decisions.

Is It Time to Rethink the Family Home

A common Perth story goes like this. A couple in their sixties or seventies owns a long-held family home in a suburb they love. The mortgage is gone. The house holds decades of memories. But the spare rooms sit empty most of the year, the garden needs constant attention, and a growing share of retirement income goes into rates, repairs, insurance, and upkeep.

That tension is real. The home is emotional, but retirement planning is practical.

When the house starts shaping your retirement

A large home can influence major decisions. You might delay travel because the place needs watching. You might put off health or lifestyle upgrades because too much money stays tied up in bricks and land. You might also feel “asset rich and cash poor”, which is more common than many people realise.

Downsizing in retirement can change that equation. Instead of holding most of your wealth in an illiquid asset, you may be able to move into a home that better suits your current life and free up capital for spending, emergencies, aged care planning, or superannuation strategies.

The best downsizing decisions usually start with lifestyle, not property. The numbers matter, but they should support the life you want to live.

The question most people actually need to answer

The issue usually isn't whether the current home is too big. It's whether it still fits.

That means asking practical questions such as:

- How much of the home do you really use now

- What does it cost you to maintain each year

- Would a different home improve daily life

- Would released equity strengthen retirement income

- Would moving closer to family, medical services, or the coast make life easier

Those questions are especially important in WA, where lifestyle patterns vary widely. A retiree in inner Perth will often have different priorities from someone splitting time between Dunsborough and the metro area.

Understanding the Downsizing Opportunity

Downsizing gets talked about as if it means “sell the big house and buy a smaller one”. Financially, it's more useful to think of it as converting home equity into flexibility.

For many Australians, the family home is their largest asset. Australian Bureau of Statistics data show the national mean price of residential dwellings reached $976,800 in the March quarter 2024, and for people aged 65–74, the median dwelling had 6 rooms and the home ownership rate was 79.3% (Investopedia reference using ABS data). That helps explain why downsizing in retirement remains such a major planning issue rather than a niche lifestyle trend.

What “releasing equity” actually means

If you own a valuable home outright, much of your wealth may be locked inside it. That equity can't directly pay for groceries, travel, medical costs, or a buffer against market volatility unless you sell, borrow against it, or use another strategy.

Downsizing in retirement can release part of that value by:

- Selling the current home and turning the proceeds into cash

- Buying a lower-cost replacement home that may be easier to maintain

- Redirecting the remaining funds into super, investments, or reserves for future spending

That's why downsizing is often less about “moving smaller” and more about rearranging your balance sheet.

The opportunity is financial and practical

For some households, the biggest benefit is extra retirement capital. For others, it's lower maintenance and a simpler home that suits ageing better. Quite often, it's both.

A move can also reset how you use your space. A well-located villa, apartment, or smaller home may leave you with less gardening and fewer repair bills, while still keeping room for grandchildren, hobbies, or guests if chosen carefully.

If you're starting the process, this guide to planning a home downsize can help with the practical side of sorting, staging, and preparing for a move.

Practical rule: Don't judge a downsizing opportunity by square metres alone. Judge it by how much freedom it creates in your day-to-day life and your retirement plan.

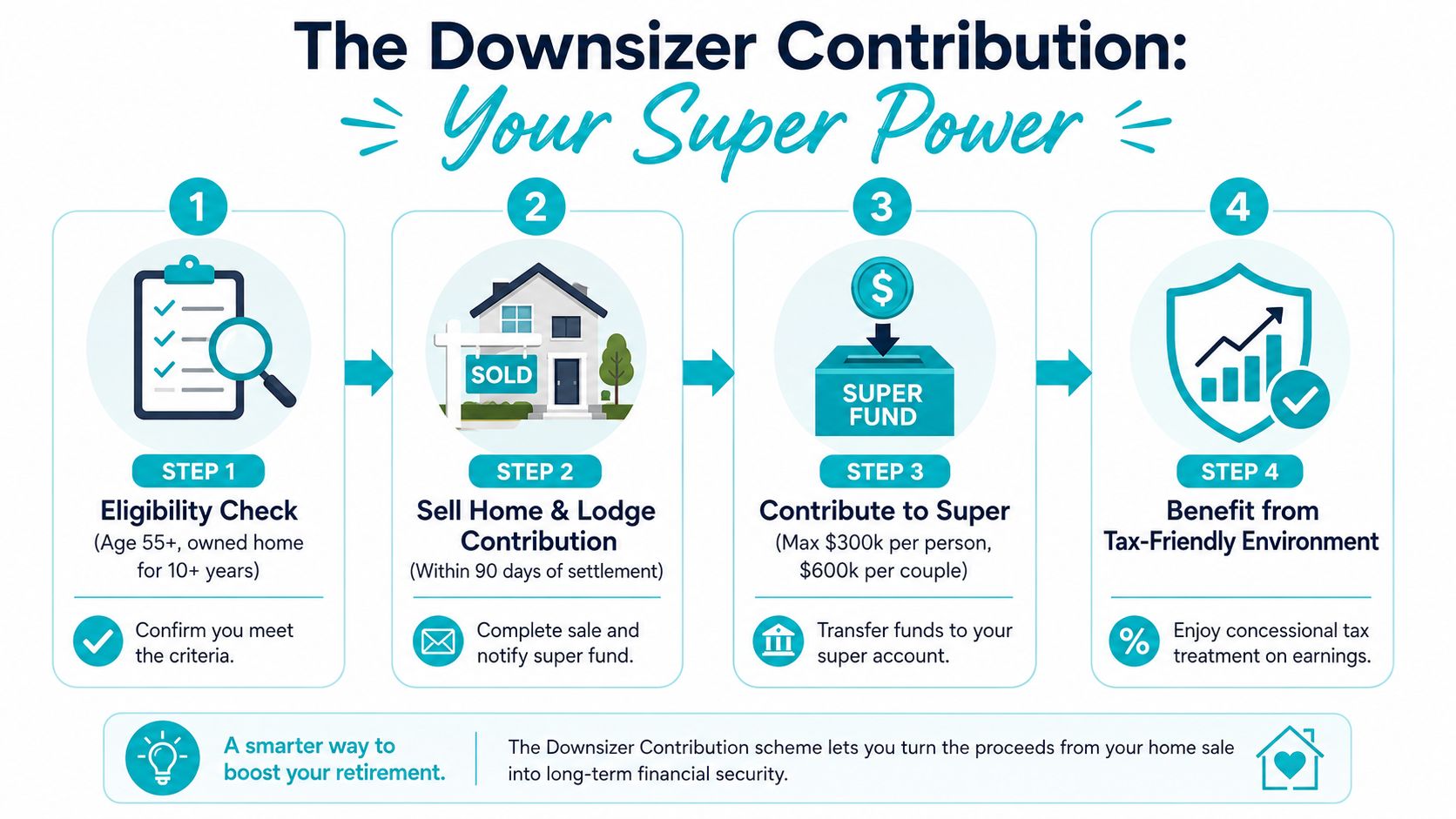

The Downsizer Contribution A Super Power

One of the most valuable parts of downsizing in retirement is the downsizer contribution. This is the rule many people have heard about, but fewer understand clearly.

The scheme was introduced in 2018–19 and expanded on 1 July 2022. It allows eligible Australians aged 60+ to contribute up to $300,000 per person, or $600,000 per couple, from the proceeds of a home sale into superannuation, outside the normal non-concessional caps (ACTS Retirement).

Why this rule matters

Normally, getting significant money into super later in life can be difficult because contribution rules can get tight. The downsizer contribution creates a separate pathway for eligible homeowners.

That matters because super can be a more tax-effective environment than holding funds personally. It also lets retirees reposition part of their wealth from the family home into an asset structure that may better support income planning.

You can read more detail on how the rules work through this downsizer contribution to super guide.

A simple example

John and Mary are both over the eligible age. They've owned their home long enough to meet the ownership requirement. They sell their long-held family property and buy something smaller and easier to manage.

If they qualify, they may each contribute up to $300,000 from the sale proceeds to super. That means up to $600,000 could move from home equity into superannuation.

That doesn't automatically make the strategy right for them. It means they have a powerful option that many retirees don't realise is available.

Where people get confused

The biggest misunderstandings usually sit in three areas:

Eligibility

You need to meet the age and home ownership rules. Not every sale qualifies.Timing

The contribution process needs to be handled correctly with your super fund and within the required timeframe.Strategy

Just because you can contribute doesn't mean you should contribute the maximum amount. The right figure depends on cash flow needs, Age Pension considerations, estate planning, and how much liquidity you want outside super.

A good strategy weighs all of those together. The house sale, the purchase of the new home, and the super contribution shouldn't be treated as separate decisions.

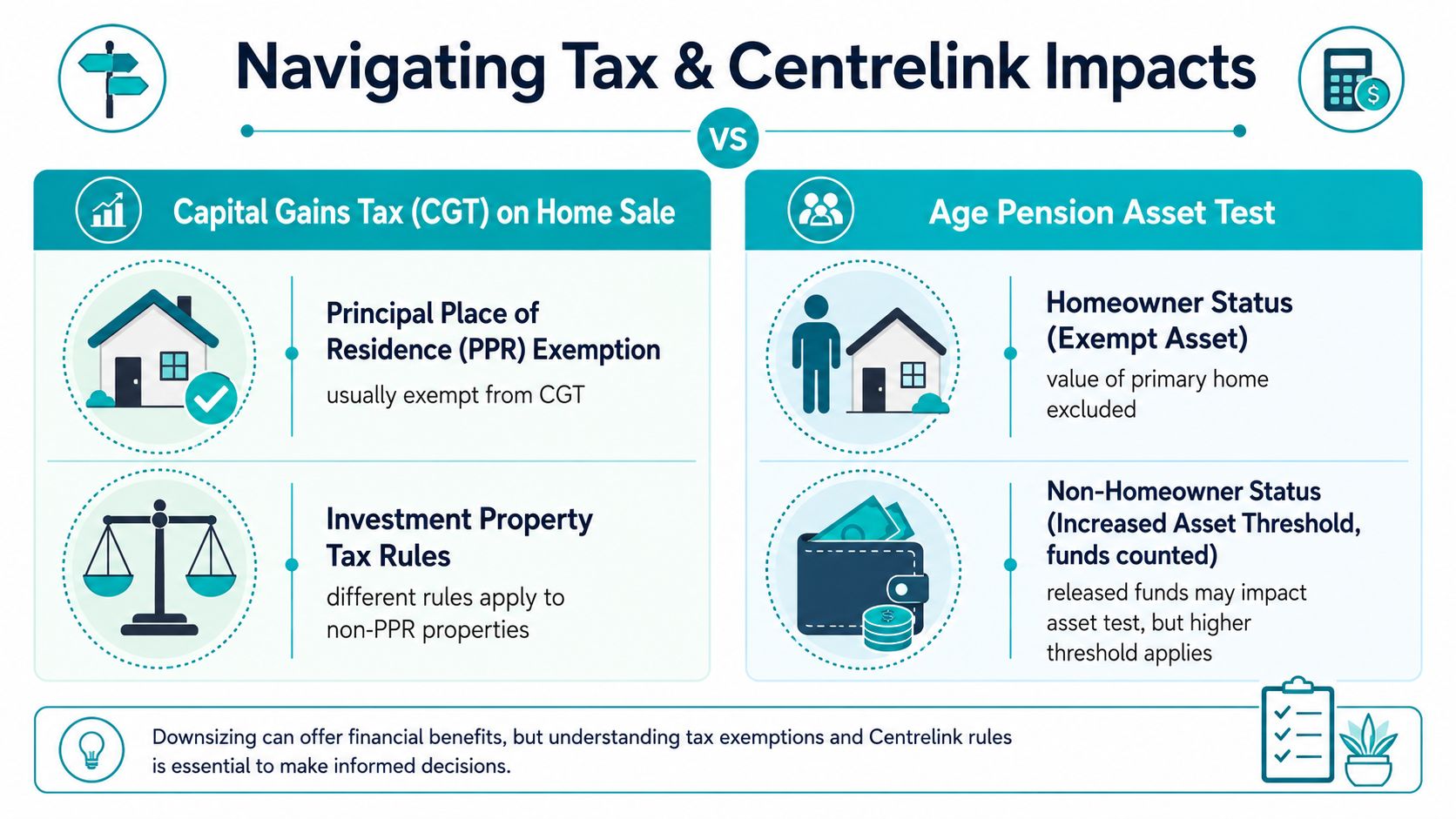

Navigating Tax and Centrelink Impacts

Downsizing in retirement often becomes more complicated than people expect. Selling the family home may feel straightforward, but the tax and Centrelink outcomes can be very different from what you assumed.

The tax side is often simpler than feared

For many retirees, the first relief is that a principal residence is generally CGT-exempt in Australia, so selling the family home doesn't usually trigger capital gains tax on the home itself. But the proceeds from the sale become assessable assets, and the downsizer contribution can help by allowing up to $300,000 per person to move into the concessionally taxed super environment (Gainbridge).

That distinction matters. The sale itself may not create CGT, but what you do with the money afterwards can still change your financial position in important ways.

For a broader explanation of how the home exemption works, this overview of the main residence exemption is a useful starting point.

Why Centrelink can change the picture

Your family home is often treated differently from cash and investments. Once you sell and bank the surplus, you've changed the form of your wealth.

Before downsizing, you may have a high-value home that doesn't affect your Age Pension in the same way. After downsizing, some of that value may sit in bank accounts, super, or other investments, which can affect your means testing.

Here's the simple version:

| Before selling | After selling |

|---|---|

| More wealth tied up in the home | More wealth may sit in assessable assets |

| Home may receive special treatment | Cash and investments are usually counted differently |

| Lower flexibility | Higher flexibility, but possible pension consequences |

This doesn't mean downsizing is a bad idea. It means you should model the result before committing.

The right question to ask

Many people ask, “Will I lose the pension if I downsize?”

A better question is, “After selling, buying, and repositioning the surplus, what will my overall cash flow and asset position look like?”

A lower Age Pension payment doesn't always mean you're worse off. If downsizing improves liquidity, reduces costs, and strengthens your long-term plan, the trade-off may still be worthwhile.

The key is to compare the full before-and-after position, not just one payment stream in isolation.

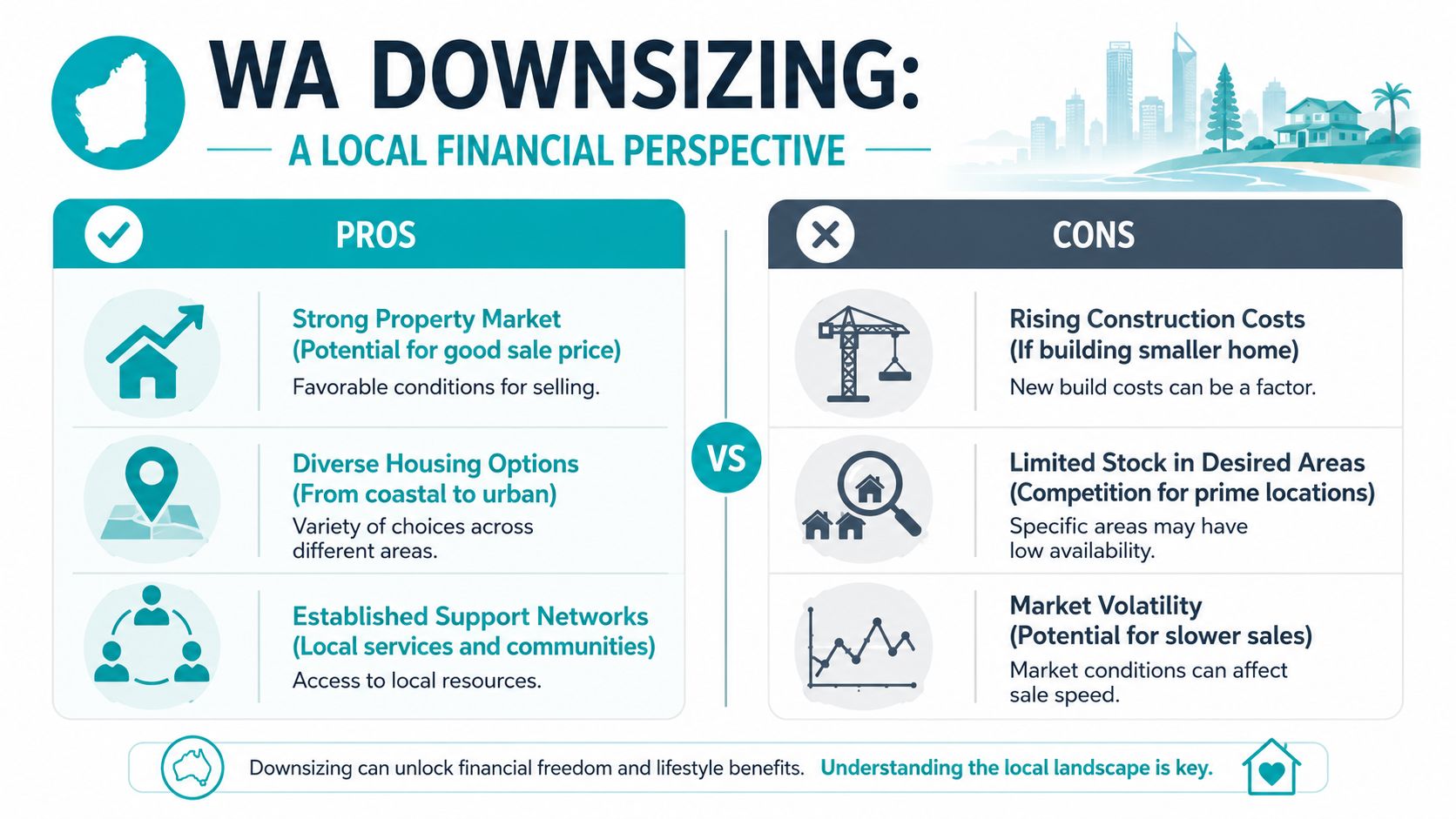

A Realistic Look at the Financials for West Australians

Generic advice often makes downsizing sound like a guaranteed financial win. In WA, it isn't always that clean.

Perth and South West retirees can run into what many locals informally think of as a premium trap. You sell a long-held, low-maintenance, paid-off home expecting a comfortable surplus, then discover that stamp duty, selling costs, moving costs, and ongoing strata or village fees narrow the benefit far more than expected.

Why headline price gaps can mislead

It's easy to compare sale price and purchase price and assume the difference is your gain. That shortcut misses the friction.

Downsizing decisions should be based on the equity release ratio, meaning net proceeds divided by home value, not just the headline price difference. In some markets, high transaction costs such as stamp duty can absorb a large share of the equity you hoped to realize (Blueprint Income).

What to include in your WA calculation

When clients look at downsizing in retirement, these are usually the costs that deserve attention:

Selling costs

Agent fees, styling, marketing, legal work, and settlement expenses.Buying costs

Purchase costs can include stamp duty and legal fees, which can materially change the outcome.Moving and setup costs

Removalists, storage, repairs, cleaning, and replacing furniture that no longer fits the new space.Ongoing housing costs

Some smaller properties come with strata fees, village charges, or maintenance structures that are very different from the old home.

Compare downsizing with other options

Sometimes the best answer isn't to move immediately. It may be to renovate for accessibility, to stage a later move, or to compare downsizing against other strategies such as drawing on existing assets more deliberately. For some households, it's also worth exploring how home equity alternatives stack up in principle, which is why people sometimes review tools like a reverse mortgage calculator in Australia before deciding.

The point isn't that reverse mortgages are better. It's that a good retirement decision should be compared against real alternatives, not against a generic idea that “smaller must be cheaper”.

If a move doesn't clearly improve both your lifestyle and your balance sheet, it may be the wrong move, or simply the wrong timing.

More Than Money The Emotional and Lifestyle Factors

The spreadsheet matters, but it won't tell you everything.

A home is where routines live. It's where family stays when they visit, where grandchildren sleep over, where the Christmas table already fits, and where you know which window catches the Fremantle Doctor in summer. Downsizing in retirement can improve life, but it can also create a genuine sense of loss if the move strips away things that mattered more than you first realised.

The WA lifestyle wrinkle many guides miss

This is particularly relevant in Western Australia. Many retirees move between Perth and the South West, host family for school holidays, or keep a larger home because children and grandchildren visit from interstate or overseas. National advice often treats extra space as waste. Locally, that extra room can be part of how family life still works.

A 2025 Murdoch University study found that 34% of WA retirees who downsized cited loss of family accommodation access as a primary regret. That local pattern is tied to the “Seasonal Migration” lifestyle often seen between places such as Perth and Dunsborough.

Questions worth asking before you sell

Some of the best downsizing decisions come from honest lifestyle planning rather than optimistic assumptions.

Who stays with you now

If family visits regularly, where will they sleep in the new home?How do you spend summers and holidays

A lock-and-leave apartment may be ideal. Or it may feel cramped when everyone visits at once.What parts of the current home still serve a purpose

A workshop, garden, art room, or guest suite can be more valuable than it looks on paper.What community are you leaving

Familiar neighbours, local clubs, medical providers, and routines often matter more in later life.

Downsizing works best when the new home supports your real lifestyle, not the simplified version of it.

A better way to define success

A successful move isn't just one that frees up money. It's one that still lets you live the way you want. That might mean keeping a second bedroom, choosing location over maximum equity release, or delaying a move until your needs are clearer.

That isn't indecision. It's good planning.

Your Downsizing Action Plan

If you're seriously considering downsizing in retirement, a calm sequence works far better than rushing from appraisal to listing.

Start with the life, not the property

Write down what you want the next phase of retirement to feel like. More travel. Less maintenance. Closer to family. Better walkability. Easier access to health services. Room for grandchildren. Once those priorities are clear, property choices become easier.

Then pressure-test the numbers

Build a simple decision file with these items:

Current position

Home value estimate, mortgage balance if any, and present living costs.Target property range

Look at realistic replacement options in the suburbs or towns you'd consider.Full transaction costs

Include selling costs, purchase costs, moving expenses, and likely ongoing fees.Retirement impacts

Consider super contribution opportunities, tax treatment, and possible Centrelink effects.Fallback options

If suitable properties aren't available, decide whether you'd wait, renovate, or explore another strategy.

Make the move manageable

The logistics can feel overwhelming long before the finances are resolved. That's normal. Breaking the process into stages helps. So does dealing with the contents of the home early. If you're staring at decades of accumulated furniture, paperwork, and sentimental items, this practical guide to streamline your move with decluttering can make the process feel far less daunting.

A good professional team also matters. Depending on your circumstances, that may include a financial adviser, real estate agent, conveyancer or solicitor, accountant, and buyer's advocate.

The key is coordination. A downsizing move affects cash flow, super, tax, housing, and lifestyle all at once. Treating it as a single integrated decision usually leads to a better outcome than handling each part in isolation.

If you want help assessing whether downsizing fits your retirement plans, Wealth Collective offers a simple first step. Book a free 10-minute introductory call to talk through your goals, your current position, and whether a personalised Retirement Roadmap could help you make the decision with more clarity and less stress.