Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Fuel costs hit your bank account long before they show up in your numbers. You fill the ute, top up the truck, refuel the generator, and keep the machinery moving because the job has to get done. Then the BAS rolls around and you're still feeling the squeeze.

A lot of small business owners accept that fuel is just one of those painful overheads. That's a mistake. If your business uses eligible fuel, fuel tax credits can put cash back into the business. Not eventually. Not in theory. In a real, claimable way that affects cash flow.

Are You Leaving Money on the Table at the Petrol Pump

You already know the routine. A staff member grabs fuel before heading to site. The excavator needs diesel. The generator burns through another tank. Nobody celebrates the spend, because fuel isn't optional. It's the cost of getting the work done.

What often gets missed is that part of that fuel cost may be recoverable when the fuel is used in eligible business activities. That's what fuel tax credits are. They're not a loophole and they're not a niche tax trick. They're a legitimate refund mechanism built into the system for businesses that use fuel in the right way.

If you run a trade business, farm, transport operation, civil crew, earthmoving business, or any setup with mixed vehicle and equipment use, there's a decent chance you've either underclaimed, delayed claiming, or never built a proper process around it. That's usually not because the entitlement isn't there. It's because the admin feels annoying enough to ignore.

That's where business owners lose money. Not through one dramatic error, but through repeated small misses. One forgotten quarter. One rough estimate. One pile of receipts no one reconciles properly.

Fuel tax credits matter most when you treat them as a cash flow system, not a once-a-year clean-up job.

If you're also trying to tighten field operations, improve job tracking, and drive sales team performance, it makes sense to connect fuel records with the way your team works on the road. Better operational visibility makes tax claims easier to defend.

And if your broader goal is to keep more of what the business earns, fuel credits should sit alongside the rest of your tax strategy, not outside it. That's why many owners start by reviewing their wider small business tax reduction options, then build fuel claims into that plan properly.

Understanding Fuel Tax Credits and Their Value

Fuel tax credits are easiest to understand if you think of them like claiming GST on a business purchase. You paid a tax component as part of the cost, and if the business use qualifies, you may be entitled to claim some of it back.

In this case, the claim relates to the fuel tax component included in eligible fuel used for business activities. The big point is simple. This is not one flat rate you memorise once and reuse forever.

Why the rate keeps changing

The ATO publishes current and historical fuel tax credit rates and makes clear that those rates are adjusted to reflect changes in fuel excise. That means you must use the correct rate for the exact tax period when calculating your claim. There isn't one static number that works for every BAS period or every fuel purchase. The ATO rates page is the authoritative reference point for this, and it also points users to a historical data file for rate history through the ATO fuel tax credit rates page.

That one fact changes how you should manage this.

If your team buys fuel across different dates, or if your business mixes equipment, heavy vehicles, and other operational uses, sloppy record-keeping doesn't just create compliance risk. It directly affects the amount you claim.

What that means in practice

The businesses that get this right do three things well:

- Match fuel purchases to the right period so each litre is claimed at the correct rate.

- Separate business use by activity because the operational use affects entitlement.

- Build the claim into regular reporting instead of leaving it as a year-end scramble.

A lot of owners assume their accountant will sort it out from the BAS totals alone. Usually, that's unrealistic. Your adviser can only work with the records you keep.

Practical rule: If your fuel records don't show when the fuel was bought and how it was used, you don't have a reliable claim. You have a guess.

That's why fuel credits belong inside a broader taxation and tax planning strategy, not on a spreadsheet someone updates when they remember.

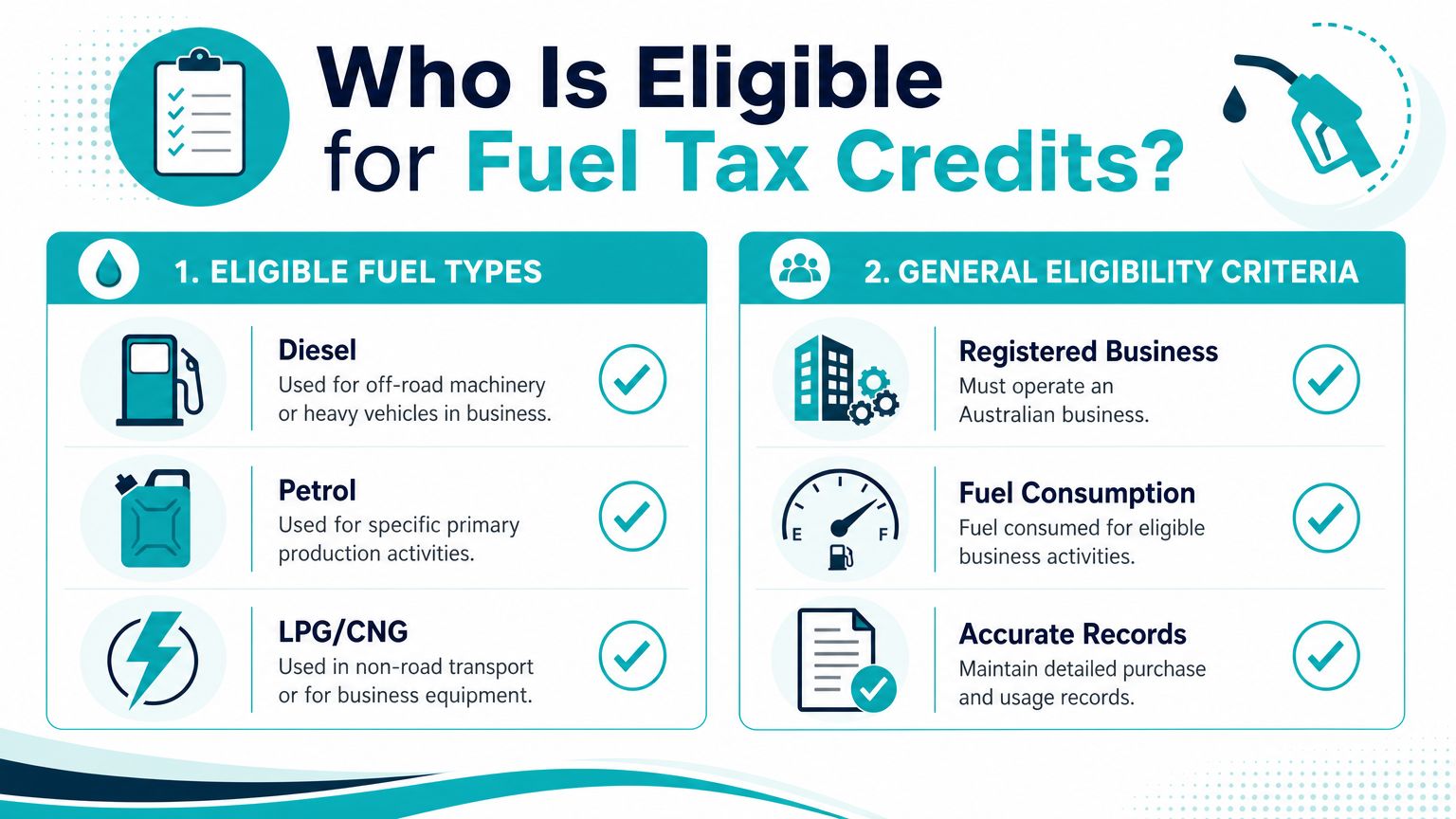

Who Is Eligible to Claim Fuel Tax Credits

Eligibility turns on how the fuel is used, not just the fact that your business bought it. That's where many claims go wrong. Owners look at the fuel bill, assume all business fuel is equal, and then either overclaim or miss value they were entitled to.

The cleanest way to think about fuel tax credit rates is by operational category.

Off-road business use

In Australia, where claims are often strongest, the off-road rate has historically matched the fuel excise component. Practitioner guidance gives a useful example of the difference this creates. As of December 2022, the off-road rate was 46.0 cents per litre, while the heavy-vehicle public-road rate was 18.8 cents per litre, showing how much operational use can change the entitlement through Teletrac Navman's fuel tax credit explainer.

If your business uses fuel in machinery, plant, generators, pumps, or equipment operating away from public roads, classification matters. Get it right and the refund can be materially better than a basic on-road assumption.

Heavy vehicles on public roads

Heavy vehicles can still attract fuel tax credits when used on public roads, but the rate is lower because the credit is reduced for road use. That's where many transport, logistics, and mixed-use operators need to be careful.

If one vehicle spends time on public roads and another part of your operation uses fuel off-road, you can't just throw everything into one pool and hope for the best. Different use cases can mean different rates.

Mixed-use businesses need stronger evidence

This is the most common real-world scenario. A construction business might have trucks travelling to site, machinery operating on site, and generators running for support equipment. A farming operation may have road travel, paddock work, and stationary equipment all in the same quarter.

That means you need records that can support apportionment.

- Vehicle records matter when part of the fuel relates to public-road travel.

- Equipment logs matter when fuel goes into plant or non-road machinery.

- Purchase records matter because you need to tie litres to real acquisitions.

- Usage records matter because entitlement depends on use, not intention.

For owners trying to organise the underlying paperwork better, it's worth reviewing practical systems that learn about expenses with Receipt Router. The principles around receipts, categorisation, and audit-ready evidence are useful even though fuel claims need their own specific treatment.

If your business uses fuel in more than one way, don't rely on memory. Build a method.

If you're not sure which parts of your operation belong in which category, start with cleaner bookkeeping and cost coding. That usually begins with a better accounting setup for small business, because poor classification upstream creates tax problems downstream.

How to Calculate Your Fuel Tax Credit Refund

The formula is simple.

Eligible litres × correct fuel tax credit rate = your claim

The hard part isn't the maths. It's making sure the litres are eligible and the rate is the right one for that use and period.

Start with litres, not guesses

Pull your fuel data from actual records. That may include supplier invoices, fuel card reports, tank logs, job records, and equipment usage summaries. Don't start with what you think the team used. Start with what you can prove.

Then split those litres into the correct categories based on use. If part of your diesel went into off-road machinery and part went into a heavy vehicle travelling on public roads, those litres should not be bundled together.

A practical example

Say you run a landscaping business. You have:

- a heavy vehicle that travels on public roads to jobs

- a diesel-powered generator used on-site

- equipment that operates away from public roads

You would identify how many litres fall into each use category for the BAS period, then apply the relevant rate for each category based on the ATO schedule for the period the fuel was acquired. After that, you total the results.

That's it. Simple structure. Precise inputs.

Sample fuel tax credit rates

Here's a small comparison table using the verified example rates already discussed.

| Fuel Type | Business Activity | Credit Rate (Cents/Litre) |

|---|---|---|

| Diesel | Off-road business use | 46.0 |

| Diesel | Heavy vehicle on public roads | 18.8 |

This table isn't a substitute for the current ATO rate schedule. It's a reminder that the use category changes the value of the claim.

The calculation discipline that saves money

Use this checklist before every claim period:

- Confirm the purchase date so you know which period's rate applies.

- Classify the fuel use by operational activity, not by convenience.

- Exclude non-eligible or private use before you calculate anything.

- Apply the matching rate to each litre pool.

- Retain the working papers so your claim can be explained later.

A surprising number of business owners only focus on the last step, lodging the figure. That's backwards. The value sits in the classification work.

The businesses that claim fuel tax credits well don't have better calculators. They have better records.

If you want one rule to keep front of mind, use this one. Never calculate from total fuel spend. Calculate from eligible litres linked to actual business use.

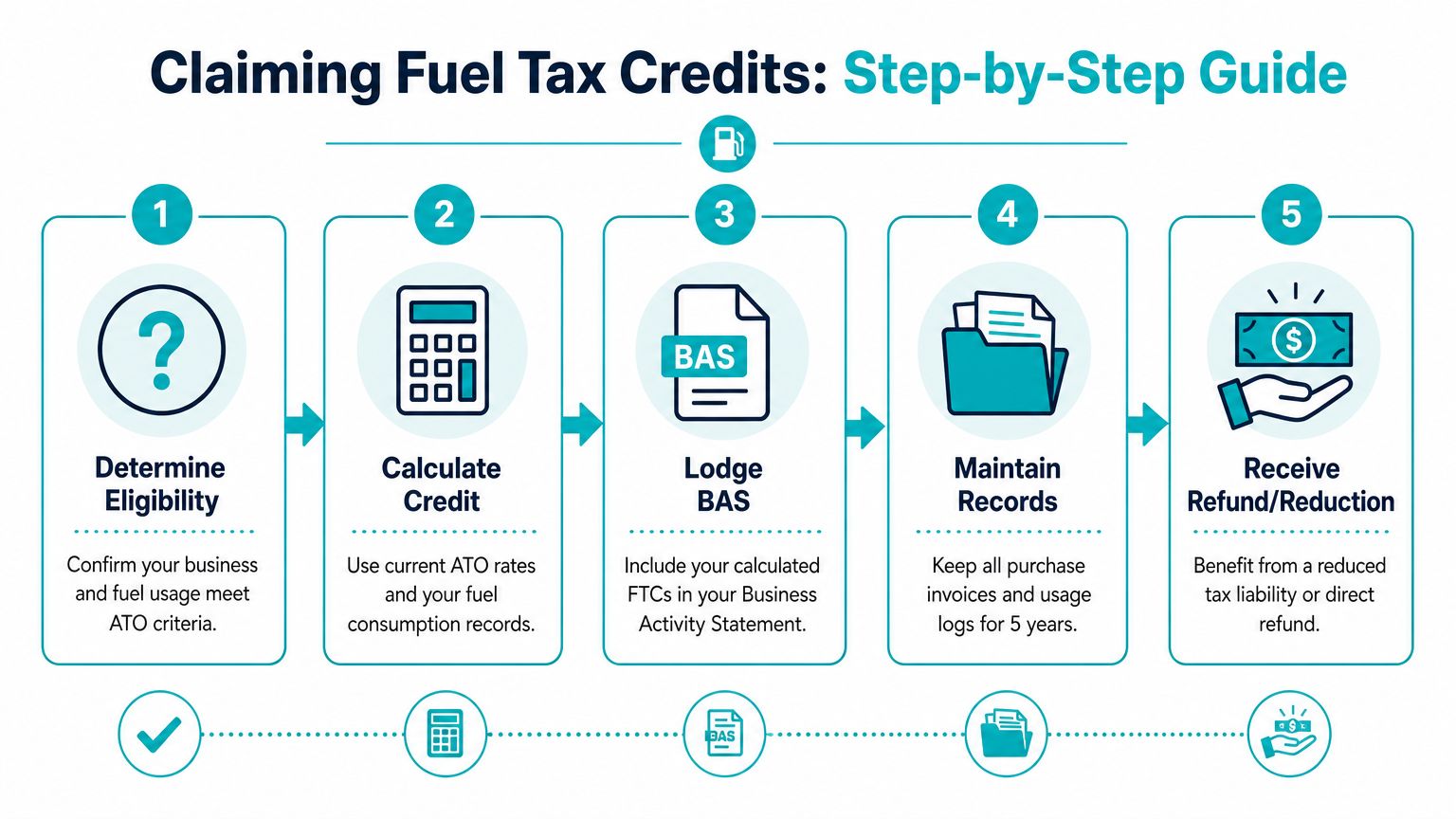

The Claiming Process and Record-Keeping Essentials

Most businesses claim fuel tax credits through the BAS. That part is familiar. The unfamiliar part is building records that can survive scrutiny without creating chaos in the office.

That's why I tell clients to stop treating this like a tax form issue. It's an evidence issue.

What you need to keep

A workable claim file usually includes a mix of purchase evidence and usage evidence. If one side is missing, the claim gets weaker.

- Fuel purchase invoices and receipts that show what was acquired and when.

- Fuel card statements or supplier summaries to support volume tracking.

- Logbooks, trip records, or GPS reports where road and off-road use needs to be separated.

- Equipment or machinery usage logs for plant, pumps, generators, and similar assets.

- Apportionment workings that show how you split business and non-business use, or one eligible category from another.

What usually goes wrong

The common failures aren't complicated.

One business keeps every fuel receipt but can't show what the fuel powered. Another has a clear equipment schedule but no reliable purchase trail. Another mixes private and business use in the same vehicle and never documents the split.

Those aren't minor admin issues. They affect the claim itself.

Build a repeatable process

You don't need a fancy system. You need a repeatable one.

| Task | Best habit |

|---|---|

| Capture purchases | Save invoices and fuel card reports by BAS period |

| Track usage | Record what asset or vehicle used the fuel |

| Split categories | Separate public-road, off-road, and non-eligible use |

| Prepare BAS claim | Use documented litre totals and supporting calculations |

Good records don't just protect you in an ATO review. They stop you underclaiming every quarter because no one wants to deal with the mess.

If you've got multiple vehicles, mobile crews, and site equipment, bring operations into the process. The office should not be guessing what happened in the field. Drivers, supervisors, and bookkeepers all need to feed the same record trail.

Smart Strategies and Future Trends

The smartest question around fuel tax credits isn't “Can I claim?” It's “Is the claim process worth the effort for my business, and how do I make it efficient enough to keep doing properly?”

That's the question more owners should ask.

Decide whether the claim is worth chasing

Practitioner guidance in the U.S. highlights a point that applies well to Australian small operators too. The compliance burden of tracking fuel use has to justify the refund, and the value often depends on having high off-road fuel volumes and solid records through the IRS fuel tax credit guidance.

That doesn't mean small claims aren't worth doing. It means you should be honest about the workload.

Use a basic decision test:

- High fuel volume and mixed operations usually justify a proper system.

- Low volume and poor records often mean the process needs fixing before the claim becomes worthwhile.

- Growing businesses should set the system early, before fuel usage becomes too messy to unwind.

If you're tightening the rest of your deductions at the same time, it helps to compare your approach with broader expert tips on business expenses. The principle is the same. A deduction or credit only helps if your records can support it without draining management time.

Use operations data, not memory

Fuel claims get easier when the business captures activity as it happens. Telematics, GPS logs, fuel cards, job management tools, and equipment registers can all make the claim more defensible.

I'm opinionated on this. If your business is scaling and still relies on a staff member's memory of which machine used which fuel, your process is already too weak.

Watch policy, not just receipts

Fuel-related tax settings don't stand still. In the U.S., policy changes have expanded and extended the Section 45Z Clean Fuel Production Credit through 2029, while policy commentary notes the maximum sustainable aviation fuel credit was reduced from $1.75 per gallon to $1.00 per gallon under the 2025 amendments, according to IRA Tracker's Section 45Z summary.

That isn't an Australian fuel tax credit rule. It is, however, a strong signal that fuel incentives can shift quickly as governments push different priorities.

Advisor view: If your business has exposure to fleet upgrades, alternative fuels, or long-term operating cost planning, treat fuel credits as part of a moving policy landscape, not a fixed entitlement forever.

The practical takeaway is simple. Review fuel claims regularly, but also keep one eye on the direction of transport and energy policy. Businesses that wait for change to become obvious usually react too late.

Turn Your Tax Credits into Business Growth

Fuel tax credits are easy to dismiss because they look administrative. They aren't. They're a cash flow lever.

If your business uses eligible fuel, every correct claim can free up money that would otherwise stay buried in operating costs. That cash can help cover debt repayments, improve working capital, support equipment purchases, or make the quarter less tight.

The owners who benefit most don't chase fuel credits in isolation. They connect them to a bigger financial plan. They know what the business is trying to build, and they make tax decisions that support that outcome.

That's the right way to think about this. Not as paperwork. As reclaimed capital.

If you've never reviewed your fuel position properly, or if your current process feels messy, late, or unreliable, fix it now. Don't wait until another BAS goes through with a rough estimate or no claim at all. Small leaks in cash flow become big frustrations over time.

If you want help turning fuel tax credits into a smarter business cash flow strategy, book a free introductory call with Wealth Collective. Their Guided Growth approach helps business owners connect tax decisions, cash flow, debt reduction, and long-term wealth planning into one clear plan.