Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You’ve probably done this already. You open a property portal, shortlist a few suburbs, check the asking prices, then start doing rough maths in your head. The rent looks decent. The area feels promising. The idea of building wealth through property makes sense.

Then the doubts start.

Will the rent cover enough? How much deposit do you need? What happens if rates stay high, the property sits vacant, or the costs are worse than expected? That’s usually the point where enthusiasm gets replaced by hesitation.

That hesitation is healthy. An investment property is a major financial commitment. It deserves more than a quick yield estimate and a hopeful assumption about capital growth. It needs numbers you can trust.

An investment property calculator in Australia is where that process should start. Not because a calculator can tell you whether to buy. It can’t. But it can turn a vague idea into a model you can test. It gives you a way to check whether a property is workable before you commit real money.

Used properly, a calculator helps you move from “this looks good” to “this is how it performs under pressure”. That’s a very different standard.

For Australian investors, and especially for buyers in WA, that distinction matters. Local taxes, acquisition costs, finance structure, and holding expenses can change the outcome far more than most generic tools suggest. The gap between a simple online result and a sound investment decision is wider than many people realise.

Your First Step Towards Investing with Confidence

A Perth investor sees a property leased at a decent weekly rent, runs a quick online estimate, and the deal looks fine. Then the key questions emerge. How much cash is tied up on day one, what does the shortfall look like after all holding costs, and does the loan structure still make sense if rates stay higher for longer?

That gap between a quick result and a sound decision is where many buyers get caught.

A calculator gives you a disciplined starting point. It turns a property from a sales pitch into a set of assumptions you can test against your own position. Price, rent, deposit, finance costs, purchase costs, and ongoing expenses all need to work together. If one part is off, the outcome changes.

The calculator turns interest into analysis

The first benefit is simple. It forces you to stop asking whether a property feels promising and start measuring whether it fits.

The useful questions are practical:

- Can the expected rent carry enough of the debt and expenses?

- What does the property cost you to hold each month?

- How much cash is required upfront, not just for the deposit but for purchase costs as well?

- What happens if the rent is lower than expected or vacancy runs longer?

- Does this property support your broader borrowing and investment plan?

That last point gets missed. A property can look acceptable in a generic calculator and still be the wrong move for your circumstances. I see this often with WA buyers who focus on headline yield but underestimate how loan structure, buffers, and cash reserves affect the quality of the decision.

Practical rule: If you cannot explain a property in numbers, you are not ready to buy it.

Confidence comes from clarity

Good investors do not use a calculator to confirm a hopeful story. They use it to test the weak points before they commit.

A generic tool can give you a rough snapshot. That has value. It helps you narrow the field and avoid wasting time on properties that clearly do not stack up. But a rough snapshot is not enough to decide whether to proceed, especially in Australia where stamp duty, lending policy, tax position, ownership structure, and local holding costs can materially change the result.

That is why the calculator should be treated as the first pass, not the final answer. It helps you identify the trade-offs early, compare options properly, and walk into a conversation with an adviser or broker prepared. If you want a broader framework for assessing returns, this guide to smarter real estate deals is a useful companion to the numbers.

Used properly, a calculator gives you something more useful than optimism. It gives you a clear basis for judgment.

What Is an Investment Property Calculator Really For

An investment property calculator is a financial flight simulator.

You use it to test conditions before you’re in the air with real money on the line. It doesn’t predict the future. It shows how the deal behaves when key inputs change.

A calculator is for scenarios, not certainty

Too many investors treat the output as an answer. It’s better to treat it as a range of possible outcomes.

If the rent comes in lower than expected, the calculator should show the impact. If the property is vacant for longer than planned, the model should react. If finance costs remain high, you should see what that does to your annual holding position.

That’s why the better Australian tools look beyond a single year. Guided Investor says its projection tool can model year-by-year outcomes across 30 years, including equity growth, cash flow before and after tax, return on equity, and LVR. It also notes local assumptions such as 3 to 8% annual property growth, 3 to 4% rent growth, management fees of 6 to 8% of rent, and insurance around $1,500 per year. Those settings make Australian calculators far more useful than generic overseas versions when you’re modelling a local property over time through its investment property projection tool.

What good investors actually use it for

In practice, the calculator is most useful for comparison and stress-testing.

A good process usually looks like this:

- Model the base case with realistic rent, loan terms, and recurring costs.

- Run a tougher case with less favourable assumptions.

- Check holding strength across the short term and the long term.

- Compare multiple properties on the same assumptions, not the selling agent’s assumptions.

The calculator’s real job is to show you where a deal breaks, not just where it looks good.

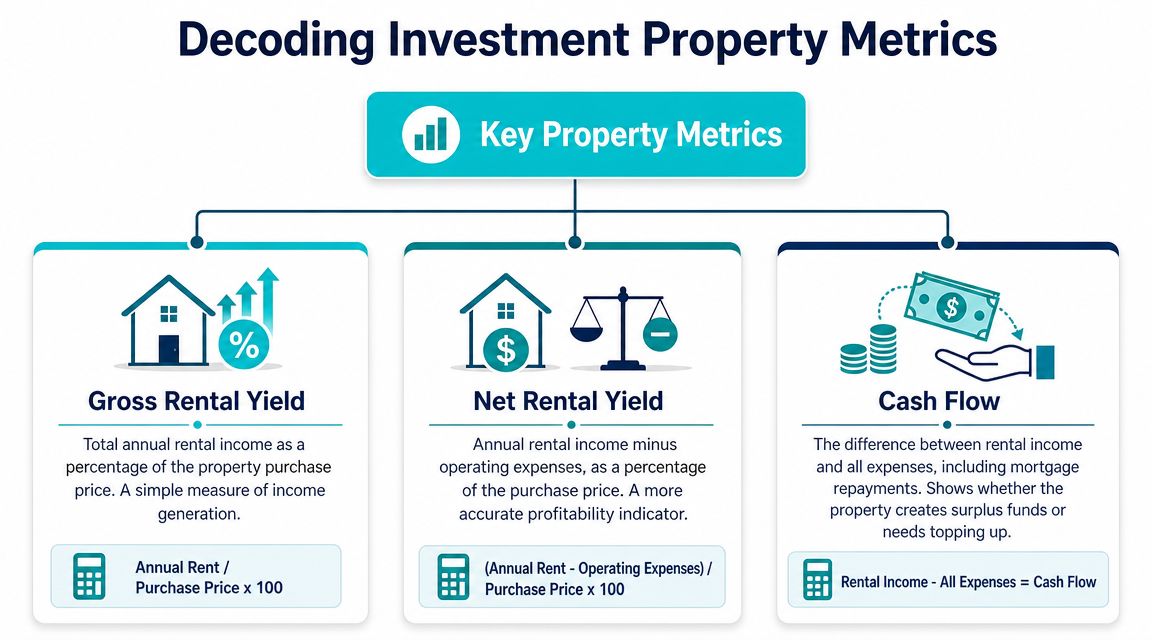

Decoding the Numbers Key Metrics Explained

A calculator can spit out neat percentages and dollar figures in seconds. The harder part is knowing which numbers deserve your attention, which ones can mislead you, and what they mean for a real Australian investment property.

Generic calculators usually stop at the headline figures. A sound investment decision in WA needs more than that. You need to know how each metric behaves once finance, tax, and ownership costs start interacting.

Gross rental yield

Gross rental yield is the quick screening metric.

It compares annual rent to the purchase price. That makes it useful when you are sorting through listings and trying to work out which properties deserve a closer look.

It also leaves out most of the costs that affect your holding position. Management fees, insurance, rates, maintenance, vacancy, and loan repayments do not appear in gross yield. A property can show a strong gross yield on paper and still be a poor fit once actual costs are layered in.

Net rental yield

Net rental yield is the more useful operating number because it accounts for the ongoing expenses of owning the property, before tax and before your personal borrowing structure are applied.

This metric gives a clearer read on whether the asset can carry itself reasonably well. For Perth investors, that matters. Two properties can have similar rent and similar price, yet one can produce a much weaker net result because strata fees, maintenance, or management costs are heavier.

Gross yield gets attention. Net yield gives context.

Cash flow

Cash flow answers the practical question most investors ask after the excitement of the listing wears off. How much money will this property require from me each month, or how much will it contribute?

That number matters because a property that is hard to hold can force bad decisions later. Selling too early, passing on other opportunities, or carrying unnecessary financial pressure usually starts with weak cash flow management, not with the suburb itself.

There are two cash flow views worth separating:

- Pre-tax cash flow shows the result after rent and property costs, but before tax effects.

- After-tax cash flow shows the result after deductions and tax benefits are considered in your own circumstances.

That second figure is where generic calculators often fall short. They can estimate a property result, but they do not know your income, ownership structure, borrowing position, or how deductions apply to you. That is also why understanding the tax benefits of rental property can materially change how you assess the same deal.

Return on investment

Return on investment, or ROI, is the broader scorecard. Depending on the calculator, it may combine rental income, expenses, loan reduction, and projected capital growth over time.

Used properly, ROI helps compare one strategy against another. Used carelessly, it can give false confidence. If the projected return depends on optimistic growth, low vacancy, and minimal repair costs, the output looks precise without being dependable.

That is the gap many buyers miss. The calculator is doing arithmetic. It is not judging whether the assumptions suit the property, the suburb, or your balance sheet.

A quick way to read the story behind the numbers

Here is the practical read on the main metrics:

| Metric | What it tells you | What it doesn’t tell you |

|---|---|---|

| Gross yield | How hard the rent is working relative to price | Whether the property is affordable to hold |

| Net yield | How much income remains after operating costs | How your finance and tax position change the result |

| Cash flow | Whether the property adds to or drains your monthly budget | Whether the asset is a good long-term buy |

| ROI | The combined return picture over time | Whether the assumptions behind the projection are sensible |

No single metric should drive the decision.

The better approach is to read them together. Gross yield helps you screen. Net yield shows operating reality. Cash flow shows holding pressure. ROI helps you compare the bigger picture. Once those numbers are on the table, you can start asking the questions a generic calculator cannot answer for you.

Garbage In Garbage Out Realistic Inputs for Australian Investors

A Perth buyer plugs a property into an online calculator, sees a neat cash flow figure, and feels ready to move. Then a different set of numbers emerges. Stamp duty, rates, management fees, maintenance, and a tighter lending structure can change the result fast.

That is the problem with generic calculators. They handle arithmetic well. They do not protect you from weak assumptions.

The inputs that matter most

A useful model starts with the obvious figures, then adds the costs that decide whether the property is comfortable to hold.

Start with:

- Purchase price based on the likely contract price, not the listing headline.

- Rental income based on comparable leased properties, not the best-case appraisal.

- Loan amount and interest rate because finance settings shape monthly pressure.

- Recurring ownership costs such as council rates, insurance, maintenance, and property management.

Those numbers need to reflect the property you are buying, the suburb it sits in, and the way you plan to finance it. A calculator can only work with what you put in.

Where Australian modelling usually breaks down

The weak point is rarely the purchase price. It is the costs investors leave out or soften to make the deal look cleaner than it is.

A sound assessment should include:

- Stamp duty and acquisition costs so the upfront cash requirement is realistic.

- Legal and settlement costs because they affect your true entry price.

- Land tax where applicable, especially if you already hold other property.

- Council and water rates which are easy to underestimate on a first purchase.

- Strata or body corporate fees for units, townhouses, and some villas.

- Property management fees if the property will be professionally managed, which is the right assumption for many investors.

- Maintenance allowance for routine wear, minor repairs, and the jobs that always seem to arrive at the wrong time.

- Vacancy allowance because even well-located rentals do not stay occupied every week of every year.

A polished result with missing costs is still a poor result.

Deposit size changes the whole structure

Deposit size is not a side issue. It changes the loan, the repayment burden, the interest bill, and the level of buffer you have if the property underperforms for a period.

As noted earlier, many investors use a 20% deposit as a working benchmark because it usually creates a cleaner lending position. Lower deposits may still be possible, but they need more careful testing. A property can look manageable at one loan-to-value ratio and become tight very quickly at another.

This is also where strategy matters more than a generic tool can show. Some buyers are aiming for lower holding costs. Others are prepared to carry a shortfall in exchange for growth potential or a path toward positive geared property strategies. The calculator can show the pressure points. It cannot decide which trade-off suits your income, tax position, and risk tolerance.

WA investors need local judgement

WA investors should be especially careful with imported assumptions. Many online calculators are built to give a broad national estimate, not a decision-ready view for a buyer in Perth or regional WA.

State duties, land tax settings, ownership structure, borrowing strategy, and your marginal tax rate can all change the holding picture. Pre-tax yield and headline cash flow are a starting point. They are not enough to decide whether the property fits your plan.

Good modelling is not about making the property look attractive. It is about stress-testing the purchase before you commit.

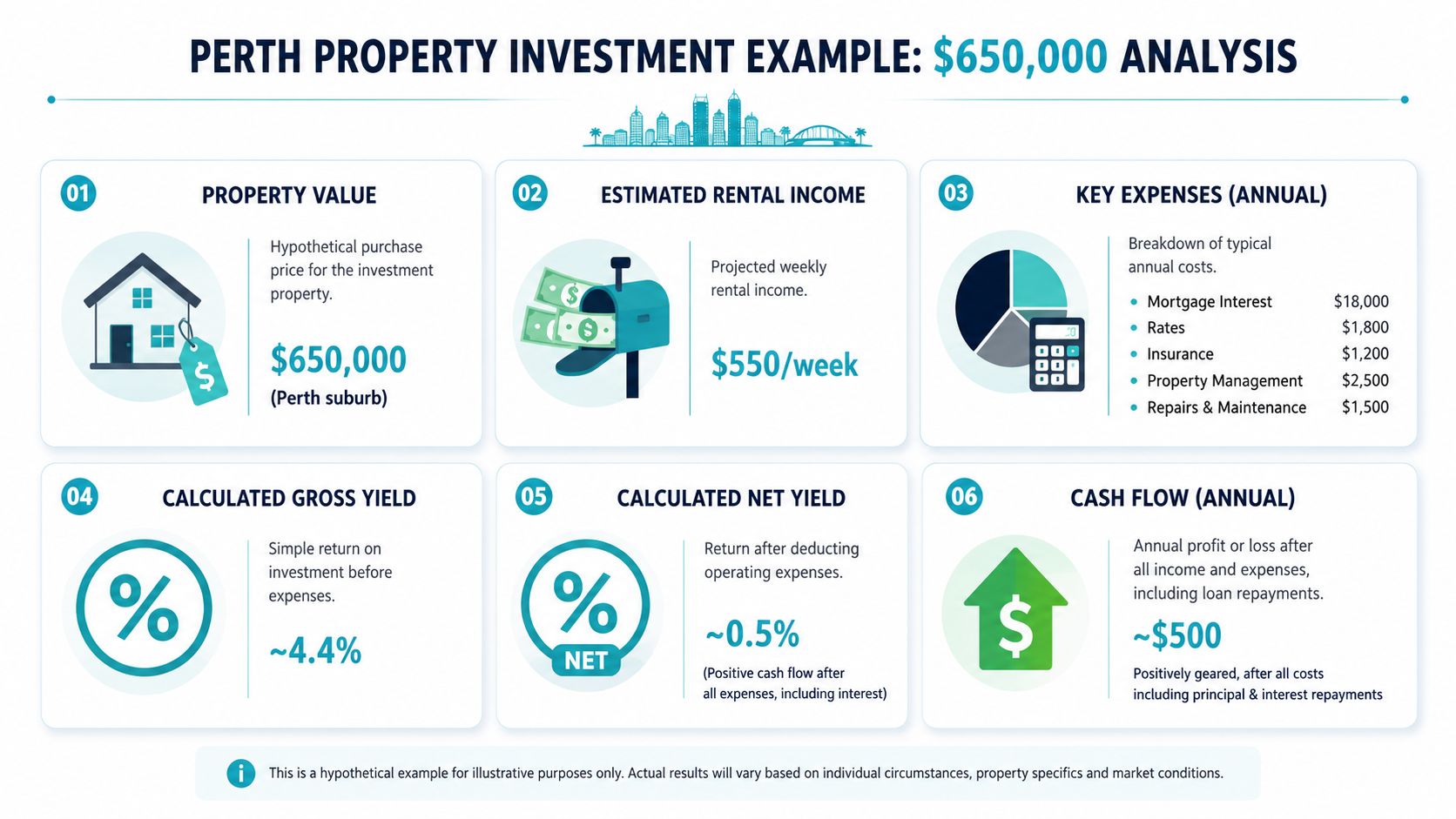

A Worked Example Analysing a Perth Investment Property

A Perth buyer is looking at a property listed at $650,000. The online calculator says the deal is roughly cash flow neutral, maybe slightly positive. That sounds encouraging. It is also the point where generic modelling stops being enough.

Used properly, a calculator gives you a first pass on whether the numbers deserve more attention. It does not tell you whether the property suits your borrowing position, tax settings, or risk tolerance in WA.

Start with the core inputs

For a practical pre-tax cash flow check, I would start with the same basic inputs any investor should test. Purchase price, expected rent, loan amount, interest rate, and recurring costs such as management fees, rates, insurance, and maintenance.

This example visual uses:

| Item | Example figure |

|---|---|

| Property value | $650,000 |

| Estimated rental income | $550 per week |

| Key annual expenses | Approximately $25,000 |

| Gross yield | About 4.4% |

| Net yield | About 0.5% |

| Annual cash flow | About $500 |

At face value, the property sits close to breakeven. That makes it a useful example because small changes matter.

What these numbers actually mean

The gross yield of about 4.4% gives a quick read on rent relative to price. It is a screening metric, not a decision metric.

The more important line is the net yield of about 0.5%. After interest and operating costs, there is very little margin for error. If the rent is overstated, if repairs run high, or if the loan cost shifts, the result changes quickly.

The annual cash flow of about $500 suggests a slim surplus before tax. Some investors will look at that and classify the property as positive cash flow. I would call it fragile positive cash flow until the assumptions have been tested properly.

How I would pressure-test this deal

For a WA investor, the next step is not to admire the output. It is to challenge it.

- Check the rent against current local evidence. An optimistic rental estimate can make a breakeven property look safer than it is.

- Review every recurring cost line. Water rates, landlord insurance, maintenance allowances, property management, and vacancy assumptions all matter when the surplus is thin.

- Run the loan at more than one interest rate. A property that works comfortably at one rate can become a monthly drag at another.

- Model the after-tax position. Pre-tax cash flow is only part of the picture, especially if depreciation, marginal tax rate, or ownership structure changes the result.

- Test the property against the investor’s broader plan. A deal can pass a calculator test and still be poor strategy if it limits future borrowing capacity or adds too much concentration.

That is the gap many generic online calculators leave open. They show a headline result. They do not tell you how stable that result is, or whether it still makes sense once the deal is placed inside an actual Australian household balance sheet.

If your goal is stronger income rather than pure growth, it helps to compare this kind of near-breakeven scenario with established positive geared property strategies. The comparison usually makes one point clear. A small projected surplus is not the same as a forgiving investment.

A worked example like this is useful because it shows where the core judgement sits. The calculator gives you a starting number. Sound advice decides whether that number is good enough to act on.

Beyond the Calculator Your Next Step to a Wildly Successful Investment

A calculator can test a property. It can’t build a strategy.

That distinction matters more than most investors expect. The calculator can estimate repayments, yields, and holding costs. It can’t tell you whether the investment suits your risk tolerance, whether the ownership structure is sensible, or how the property fits alongside super, debt, insurance, and retirement goals.

The gap most online calculators leave open

This is the issue many WA investors run into. Most calculators stop at the point where actual decision-making should begin.

The question investors usually need answered is not just whether a property has acceptable yield. It’s whether the after-tax cash flow still works once tax, depreciation, land tax, stamp duty, and state-specific settings are included. That gap is especially relevant in WA, where state-based costs and tax settings can materially change the outcome. The source material behind this point makes the limitation clear: many Australian calculators rarely answer the question investors need to know about after-tax cash flow in their state.

What advice adds that a calculator can’t

A proper advice process helps answer questions like these:

- Should you buy in your own name or another structure?

- How much investment debt is appropriate given your income and family commitments?

- Would a cash-flow-positive property help, or distract from a better long-term strategy?

- How does this purchase affect retirement planning, borrowing capacity, and risk exposure?

- What happens if rates, vacancy, or personal income change?

Those aren’t calculator questions. They’re judgement questions.

Where the next step becomes practical

For many investors, the smartest move after using an investment property calculator in Australia is to take the model into a personalised advice conversation.

That doesn’t mean abandoning the calculator. It means using it for what it’s good at, then bringing the output into a broader strategy discussion. One option is Wealth Collective, which works with Australians on advice across debt reduction, investment strategy, superannuation, and long-term planning. If you’re still at the stage of weighing up the purchase process itself, their guide on how to buy an investment property is a sensible next read.

A good adviser won’t replace the numbers. They’ll challenge the assumptions behind them and place the property in the context of your full financial life.

That’s where confidence becomes durable. Not because a calculator gave you a neat answer, but because the decision holds up when the numbers, the strategy, and your real life all line up.

If you want to turn a rough property idea into a decision you can stand behind, book a short introductory call with Wealth Collective. It’s a practical way to talk through your numbers, your WA-specific considerations, and whether an investment property fits your broader plan before you commit.