Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Australians are sitting on just over $18.9 billion in lost and ATO-held super across about 7.3 million inactive accounts as at 30 June 2025, according to the ATO's lost and ATO-held super data. That's not a quirky admin issue. It's retirement money that's gone off the radar.

If you live in Perth, Bunbury, Mandurah, Dunsborough or anywhere else in WA, the fix is usually less about “finding” a hidden account and more about cleaning up old records, making a smart consolidation decision, and avoiding mistakes that cost you later. That's where the difficulty often lies.

Missing super funds are rarely missing in the dramatic sense. They're usually sitting with a fund or the ATO while your details no longer line up. People change jobs, move house, change names, forget old employer defaults, and leave small balances behind. Then they assume it'll sort itself out. It often doesn't.

The Multi-Billion Dollar Treasure Hunt You Need to Join

Roughly one in three super accounts in Australia is a multiple account, lost, or ATO-held account. That should stop you in your tracks. Missing super is common, expensive, and usually fixable.

The problem isn't that the money has vanished. It is that old records, stale contact details, name changes, and forgotten employer funds push your super out of sight until fees, poor investment settings, or the wrong insurance setup start working against you. In WA, I see this after FIFO job changes, public sector moves, small business closures, divorce, and interstate relocations that leave old paperwork behind.

A small forgotten account causes bigger problems than people expect:

- Fees keep draining the balance: even modest admin and insurance costs can chew through a small account fast.

- Your retirement picture becomes inaccurate: you cannot make good contribution, investment, or drawdown decisions if part of your super is sitting off the radar.

- Insurance mistakes become more likely: one old account may still hold cover you need, while another may be charging for cover that no longer fits your life.

- Bad records block recovery: if your TFN, name, date of birth, or address do not match, the money can sit there for years.

That last point is where many people get stuck. Standard search guides tell you where to click. They do not tell you what to do when the account exists but your details do not line up cleanly. Fixing that often means pulling together old employment records, payslips, and tax documents. If you need to track down older income paperwork first, start with these steps on how to get your PAYG summary.

There is also a bigger decision sitting behind the search. Finding an old super account does not automatically mean you should cash it out, leave it alone, or roll it over immediately. The right move depends on tax, preservation rules, insurance, and how close you are to retirement. That is the part people get wrong when they treat missing super as a simple admin clean-up.

Unclaimed money does not become harmless just because you ignore it. It can remain with a fund or move to the ATO, and if no one fixes the identity mismatch or claim issue, it stays disconnected from the retirement strategy you are trying to build. The same principle shows up in other financial investigations. Tracing what belongs to you often starts with records, inconsistencies, and old transactions, much like Lighthouse Consultants on hidden assets.

If you are in your 40s, 50s, or nearing retirement in Perth or regional WA, deal with this now. You have less time to recover from avoidable leakage, poor consolidation choices, and insurance errors. A quick search is the easy part. Getting the money back into the right structure is what protects your long-term plan.

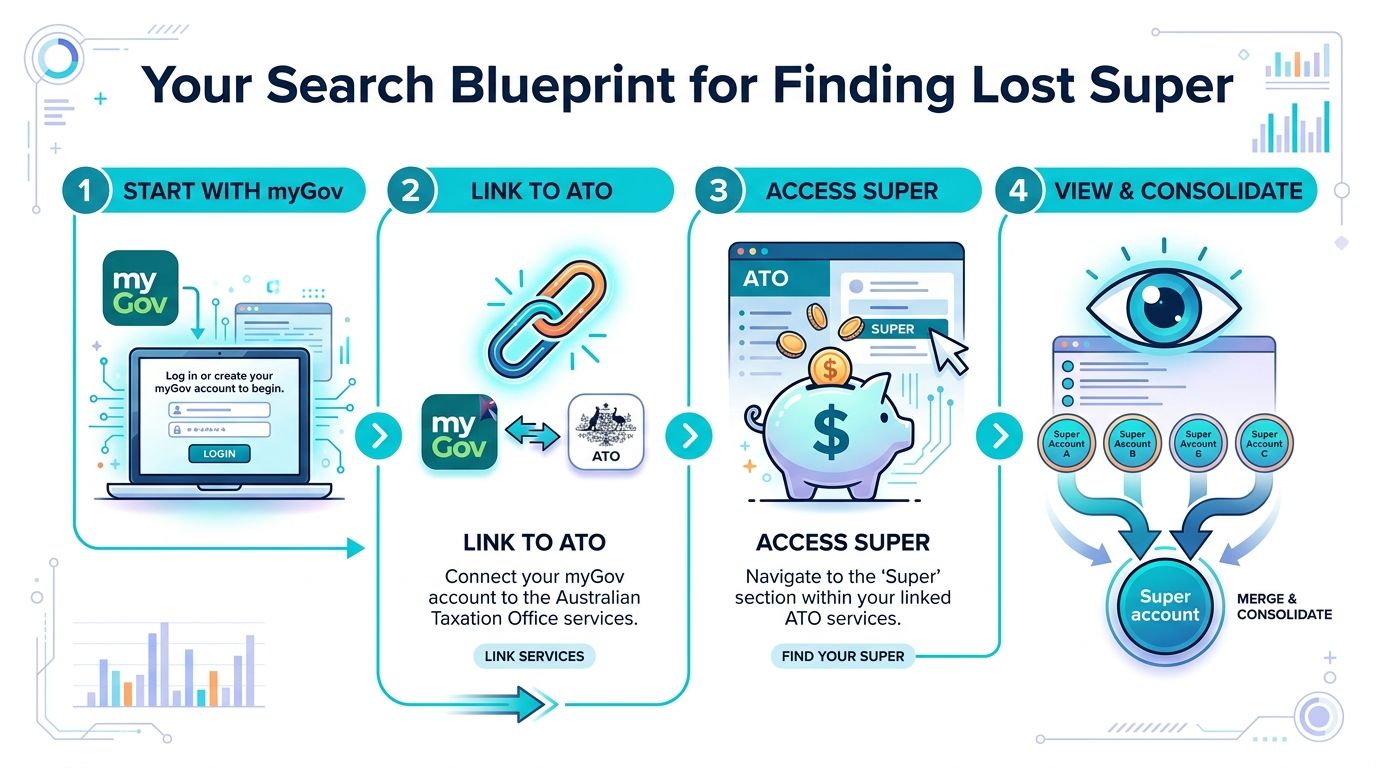

Your Search Blueprint for Finding Lost Super

A missing super search usually turns into an identity clean-up exercise. Start with the official system first, then fix the record gaps that stop the match from happening.

Start with myGov and the ATO

Log in to ATO online services through myGov. Go to Super, then Fund details. Look for balances marked Contact fund or ATO-held super.

Those labels tell you who controls the money right now.

- Contact fund means the account still sits with the super fund.

- ATO-held super means the balance has already been transferred to the ATO.

That distinction matters in practice. If the fund still holds the account, you may need to deal with older member records, outdated contact details, or a fund merger. If the ATO holds it, the claim process is usually cleaner, provided your identity details line up properly.

Why searches fail when the money is there

What most guides miss is that failed searches often come down to bad data, not missing money. If nothing shows up, assume the records are inconsistent before you assume the account has vanished.

Check these first:

- Your legal name across myGov, the ATO, and every fund you have used. Name changes and spelling variations cause problems constantly.

- Your date of birth. A single digit error can stop a match.

- Your address and contact details with current and former funds.

- Your TFN connection. Old accounts sometimes sit outside the system properly because the TFN was never matched correctly.

If the search result looks wrong, fix identity data first. Then run the search again.

This matters even more for Perth clients who have moved between mining, construction, government, and small business employers across WA. Job changes, regional work, payroll changes, and older default funds create messy records fast.

What to do when old systems are the problem

Older employer funds and pre-digital records can be hard to trace. Handle it like an audit. Work backwards through where you worked, when contributions were paid, and which fund was used at the time.

| Issue | What to do |

|---|---|

| Old surname or spelling variation | Ask the fund to update identity records using your current ID |

| Old residential address | Update details with every super fund you've ever used |

| Unknown employer default fund | Ask payroll or HR which fund received contributions |

| No visibility in myGov | Confirm your TFN is attached correctly across fund records |

If you are missing old payroll documents, rebuild the trail with this guide on how to get your PAYG summary. That gives you dates, employers, and income records you can use when a fund asks for proof.

The process is similar to tracing overlooked assets in other financial disputes. Lighthouse Consultants on hidden assets covers a different problem, but the lesson is the same. Records fail before money disappears.

Alternative paths when myGov does not solve it

Do not stop at one portal search.

- Call former employers and ask which default fund received your super contributions.

- Contact known super funds directly and provide your TFN plus updated ID.

- Check old emails, payslips, and onboarding packs for fund names or member numbers.

- Ask merged funds about predecessor accounts if a provider has changed names over time.

If you keep hitting dead ends, get advice before you make assumptions about withdrawing, merging, or ignoring the account. Finding the money is only useful if it ends up supporting your retirement plan, not sitting in the wrong place for another five years.

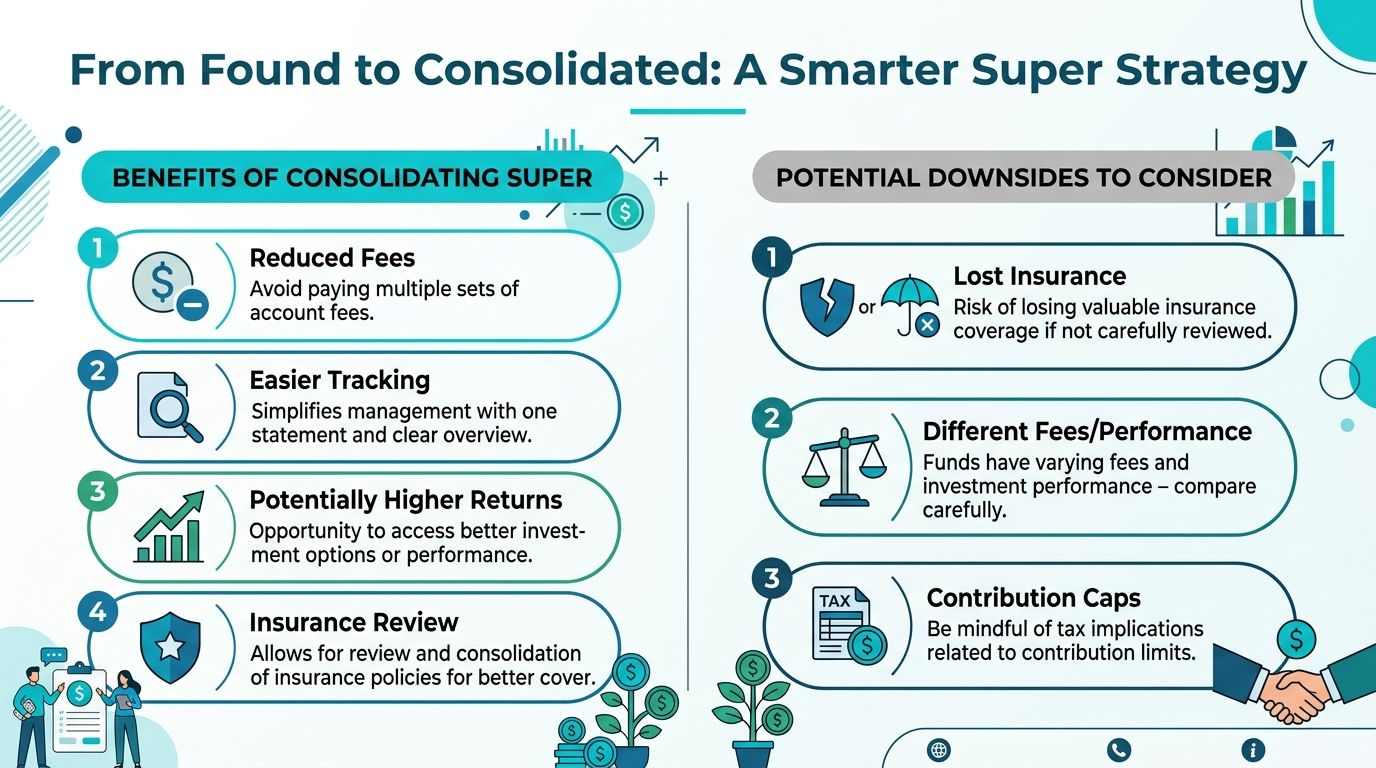

From Found to Consolidated A Smarter Strategy

Every extra super account creates another chance for fees, bad insurance decisions, and neglected investment settings to chip away at your retirement outcome.

Once you find old super, the next move is to decide whether it belongs in your long-term plan or whether it is still sitting there by accident. In Perth, I see the same pattern again and again. People track down forgotten balances, feel relieved, then stall. That delay costs money.

For most working Australians, consolidation into one suitable active fund is the right call. It gives you one balance to monitor, one investment strategy to review, one set of beneficiaries to keep current, and far less chance of money drifting out of sight again. If you want a practical process, this guide on consolidating your super lays it out clearly.

Do not merge accounts blindly.

The biggest mistake is treating consolidation like admin cleanup instead of a financial decision. Old accounts can hold insurance that is hard to replace under the same terms, especially if your health has changed since the cover started. Closing that fund first and asking questions later is how people lose Life, TPD, or Income Protection cover they needed.

Check these points before you roll anything over:

- Insurance cover: Confirm exactly what is attached to each account and whether you would lose it on closure.

- Underwriting history: Older cover may have been accepted on better terms than you could get now.

- Fees against value: Paying a premium can make sense if the policy is strong and relevant.

- Investment option: A forgotten account may be invested very differently from your main fund.

- Beneficiaries and administration: Make sure your chosen fund is the one you want managing your retirement money.

A larger balance is not automatically the best home for the rest of your super. Choose the fund with the better mix of fees, investment options, insurance, service, and fit for your retirement timeline. That matters more than which account happens to have the most money in it today.

This is also where the tax question starts to matter. Consolidating is usually straightforward. Accessing super is not. If part of your decision involves retirement timing, pension phase planning, or larger balances that may be affected by future rule changes, get across understanding the 2026 super tax before you act.

If your records are messy, your details have changed, or you are unsure whether an old policy should be kept, get advice before consolidating. The right move is usually simple once the facts are clear. The wrong move can be expensive and hard to reverse.

Understanding the Tax and Retirement Implications

People often assume that once they locate missing super funds, they can just pull the money out and use it. Usually, that's the wrong move. In many cases, it isn't even available that way.

Super is a retirement structure, not a savings account. Finding an old balance doesn't change the access rules. The better question is usually whether the money should stay in super and be consolidated into your active strategy, rather than whether it can be withdrawn.

Consolidating versus cashing out

Consolidating found super into the right active fund is cleaner than trying to take money out. It keeps retirement assets together and reduces the risk of making a short-term decision that weakens long-term security.

The tax side can also get murky fast, particularly for people nearing retirement, moving between work statuses, or trying to coordinate super with pension income. If you're trying to make sense of broader rule changes, this guide to understanding the 2026 super tax is a useful background read.

What happens if you never claim it

This is the question too many people leave until late in life. Some lost super doesn't just sit untouched forever in the same place. There's an Unclaimed Superannuation Fund mechanism that can transfer money to the government, and the process to reclaim it later can become more complex.

That matters because the standard “just search for it later” advice is lazy. Later is often harder.

A practical risk list looks like this:

- Records become older and harder to verify

- Fund history becomes less clear

- You may be dealing with retirement planning at the same time

- Administrative effort rises when you have less patience for it

Waiting until retirement to tidy super is like waiting until settlement day to read the contract. You can do it, but you've made the job harder than it needed to be.

A better retirement planning mindset

If you're in your fifties or approaching retirement, treat missing super as part of retirement planning, not an isolated admin chore. It affects the pool of assets you'll rely on, the timing of decisions, and the way your retirement income is structured.

That's especially true if you also need to think about:

- When to stop work

- Whether to keep insurance inside super

- How your super supports drawdown needs

- How to avoid avoidable tax friction

Recovered super is useful. Recovered and properly integrated super is far better.

Common Pitfalls and Perth-Specific Pointers

The assumption that missing super funds are easy to recover is wrong. Sometimes they are. Sometimes the process turns into a tangle of old addresses, inactive accounts, stale employer records, and bad decisions made in a hurry.

Australia holds an estimated $18.9 billion in lost and unclaimed superannuation, and the average amount of unclaimed super per individual is $2,590, according to AustralianSuper's lost super overview. That average is large enough to matter, especially if you're trying to tighten your retirement position or clean up household finances.

The mistakes that cause the most damage

Some errors are predictable. They keep showing up because people rush the process.

- Chasing unofficial recovery services: If someone contacts you out of the blue about lost super, be sceptical. Use official ATO and fund channels first.

- Ignoring insurance before consolidation: This mistake doesn't feel expensive until a claim is declined because the old cover is gone.

- Keeping multiple tiny accounts open: Admin clutter becomes financial drag.

- Treating every fund as interchangeable: Different funds suit different people.

One more issue deserves blunt treatment. The recent collapses around First Guardian and related investment options are a reminder that not every super-related decision is harmless. The ABC report hosted on YouTube about the First Guardian Master Fund collapse describes a $590 million investment vehicle affecting approximately 6,000 Australians, with $45 million paid to advisers and marketers. That's not “lost super” in the usual admin sense, but it proves a bigger point. You need to know where your retirement money sits and why.

WA context matters more than people admit

Super is governed nationally, but your financial life is local. WA workers often change roles across mining, construction, health, trades, government and small business. That means employer changes can be frequent, default funds can vary, and paperwork gets messy.

If you're based in Perth or regional WA, keep these points in mind:

- Job mobility creates account sprawl: Every employer change is a chance for another fund to appear.

- Address changes are a major risk: FIFO work, regional moves and rental changes can break contact trails.

- Pre-retirees need local context: Your super decision should fit your wider WA lifestyle plans, housing position and retirement timing.

For people who want personalized support rather than generic checklists, working with a Perth-based superannuation financial advisor can make the process far more deliberate.

A short checklist before you act

| Check | Why it matters |

|---|---|

| Confirm your identity details match | Mismatches block recovery |

| Review insurance first | Old cover can disappear on closure |

| Compare receiving funds properly | Convenience isn't the same as suitability |

| Use official channels | Scams thrive on confusion |

You don't need perfect paperwork to make progress. You do need discipline.

Take Control of Your Financial Future Today

Missing super funds are fixable. That's the good news. The bad news is that people leave them untouched for years because the issue feels annoying rather than urgent.

If your situation is simple, handle it yourself. One or two old accounts, straightforward employment history, and no major insurance attached. Log into myGov, clean up your details, locate the money, and consolidate carefully.

If your situation is not simple, get help early. That includes people nearing retirement, people with multiple old funds, anyone unsure about insurance, anyone considering withdrawal rather than consolidation, and anyone who's already hit a wall because the records don't match. In those cases, DIY can cost more than it saves.

The bigger picture matters. Finding super is not the goal. Building a retirement balance you can understand, control and use well is the goal. This is one of those jobs that feels administrative on the surface but quickly becomes strategic.

Take the first step now. Clean up the records. Find the accounts. Make a decision that supports your future self, not just today's inbox.

If you want a clear second opinion before making changes, Wealth Collective offers a practical starting point. A short introductory call can help you work out whether your missing super funds issue is a simple clean-up job or part of a bigger super, insurance, and retirement planning strategy.