Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

Starting a business in WA often feels straightforward until the first contract lands on your desk, the lease asks for certificates of currency, or you decide to hire someone for a few shifts a week. That's usually the moment small business insurance requirements stop feeling theoretical and start feeling personal.

For most owners, the concern isn't jargon. It's simpler than that. What do I legally need, what will clients demand, and what could put my business and personal wealth at risk if I get it wrong?

The answer in Western Australia is rarely a single policy. It's a mix of statutory obligations, vehicle rules, and commercial requirements that can change as your business grows. A sole trader working from home has one risk profile. The same person with a casual staff member, a delivery van, and a lease has a very different set of obligations.

Understanding Your Foundational Legal Obligations

If you're feeling unsure about whether you're “properly covered”, start with one question: Do you have employees? In Australia, that's the clearest trigger for mandatory insurance.

Across Australia, workers' compensation insurance is the clearest example of a mandatory small-business insurance requirement. Each state and territory runs its own scheme, and employers must insure when they hire staff, which makes it the first statutory checkpoint for many businesses, as noted in this national overview of workers' compensation obligations.

That matters because many owners still assume there's one national business insurance rule. There isn't. Australia uses separate state and territory systems, so compliance depends on where you operate and whether you've crossed an employment threshold by hiring staff.

The first trigger most owners miss

A lot of new owners focus on logo design, invoicing software, or getting their first client. Insurance only gets attention later. In practice, the first serious compliance issue usually appears when you bring someone in to help, even casually.

Once you employ staff, your obligations expand beyond just wages. You're also dealing with payroll, superannuation, and employment-related cover. That's one reason sound record-keeping matters from day one. If your business admin is already messy, the insurance side usually becomes messy with it. Good small business accounting support helps because insurance compliance rarely sits in a silo.

Practical rule: If you pay people to work in your business, check your workers' compensation position before their first shift, not after their first incident.

Legal minimums are only the floor

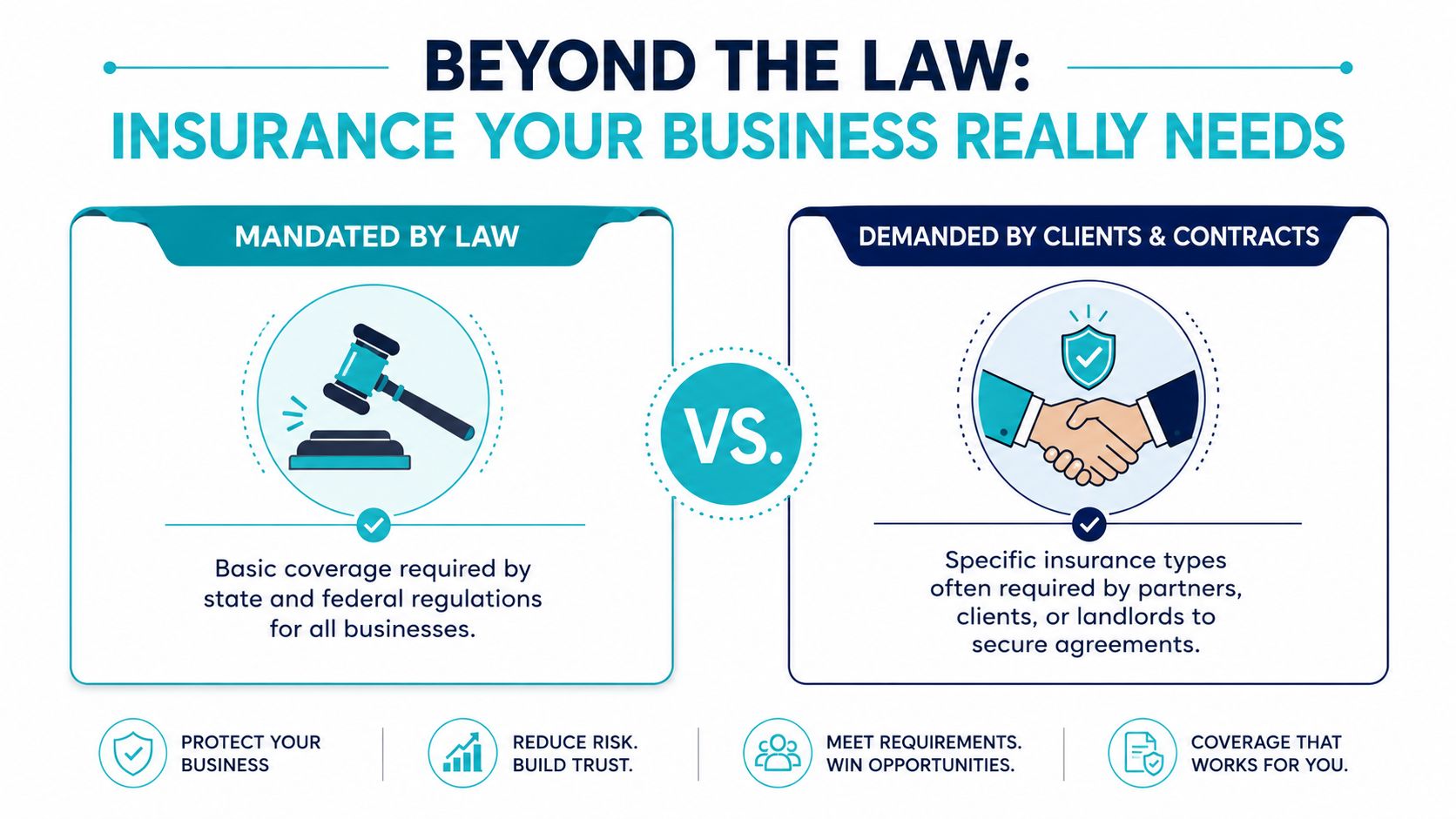

It helps to separate two ideas that owners often blend together:

- What the law requires: This is the mandatory cover tied to employment and other regulated activities.

- What prudent owners choose: This is the broader protection that keeps a setback from becoming a financial crisis.

- What commercial partners insist on: This sits somewhere in the middle. It may not be in legislation, but it can still stop you from trading if a landlord, lender, or client won't proceed without proof of cover.

That distinction keeps you from making two common mistakes. The first is buying too little because “it wasn't legally required”. The second is overbuying too early without understanding where the actual exposure sits.

A sensible starting point

For a new WA business owner, the foundational sequence is simple:

- Confirm whether you have employees. If yes, your insurance obligations likely begin immediately.

- Identify where you operate. State-based rules matter.

- Check whether your work involves vehicles, premises, or regulated activity.

- Review every lease and contract before signing. Insurance requirements often appear there first.

Most insurance problems in small business don't start with a claim. They start with an assumption.

Your Western Australia Specific Insurance Checklist

Western Australia has its own rules, and as a result broad advice stops being enough. If your business operates in Perth or elsewhere in WA, you need to work from WA obligations, not a generic Australian checklist.

Workers' compensation in WA

Under the WA Workers' Compensation and Injury Management Act 1981, any business with employees must hold workers' compensation insurance. That includes situations many owners wrongly treat as informal, including very small teams and casual arrangements. The WA framework also makes premiums highly sensitive to the nature of the work being done. The verified rate range is $0.50 to $12.00 per $1,000 of wages, depending on industry risk and wages assessment.

That's why a consulting business and a trade business can face very different premium outcomes even with similar payroll numbers. The law doesn't treat every business risk the same, and neither do insurers.

Here's a simple way to think about WA premium ranges:

| Industry Type | Risk Profile | Example Premium Rate |

|---|---|---|

| Office-based professional services | Lower risk | $0.50 per $1,000 of wages |

| Mixed operational business | Moderate risk | Within the statutory WA range |

| Higher-risk manual trade or labour work | Higher risk | Up to $12.00 per $1,000 of wages |

The exact premium depends on wages and industry classification. The practical point is clear. Small changes in staffing or business activity can change your insurance cost and your compliance position.

A business owner who says “it's only one casual” is often describing the very moment workers' compensation becomes compulsory.

Commercial vehicles in WA

The next issue is vehicle use. If your business owns, operates, or leases vehicles for commercial purposes, you need to treat that as a separate compliance category.

The verified data states that commercial auto insurance is a mandatory requirement for business vehicle use in Australia and notes a minimum liability coverage of $1 million per incident for third-party bodily injury and property damage, with WA legislation referenced through the Motor Vehicles Act 1959 and Road Traffic Act 1974. The same verified data also states that 94% of WA small businesses with commercial vehicles are compliant, while 6% fail because they use personal policies for business use.

That last point is where trouble starts. A personal policy may look cheaper, but if the vehicle is being used for deliveries, site visits, mobile services, or regular business errands, the insurer can treat that as the wrong classification.

The WA mistakes that create real exposure

A short checklist helps:

- Casual staff count too: In WA, even a single employee can trigger workers' compensation obligations.

- Wages affect premiums: Understating payroll or using the wrong classification can leave you underinsured.

- Business use changes vehicle insurance: A bakery van, mobile trade ute, or client-visit vehicle should be reviewed as a commercial risk.

- Proof matters: When builders, site managers, and principal contractors ask for evidence of cover, make sure you can quickly verify WorkCover insurance and produce current documents.

- Annual review is essential: A sole trader who hires one person, adds a vehicle, or changes contract structure can cross several compliance thresholds in one year.

If your business has moved beyond a simple sole trader setup, it usually makes sense to get broader WA business advisory support so insurance, payroll, structure, and tax decisions stay aligned.

Insurance Your Contracts And Clients Will Demand

Many of the most important small business insurance requirements never appear in an Act of Parliament. They show up in leases, council permits, procurement documents, lender terms, and client contracts.

That catches new owners off guard. They assume “required” means legally mandated. In business, “required” often means “produce the certificate or you don't get the job”.

Law versus commercial reality

Public liability insurance is the clearest example. It's frequently required by landlords, councils, or contract counterparties even when not mandated by statute. Many small businesses need it to rent premises or tender for work, as described in this guidance on business insurance needs and public liability expectations.

If you operate from a shop, studio, clinic, warehouse, market stall, or client-facing office, public liability is often the document someone asks for before they hand over the keys or approve your booking.

What each policy actually does

Use this comparison as a practical filter:

| Insurance type | Usually driven by | What it protects against |

|---|---|---|

| Workers' compensation | Law | Employee injury and related workplace liability |

| Public liability | Leases, councils, customer-facing activity, contracts | Third-party injury or property damage claims |

| Professional indemnity | Service agreements, licensed work, client terms | Claims arising from advice, errors, omissions, or professional service failures |

| Management liability | Governance needs, company structure, investor or director concerns | Claims involving directors, officers, employment practices, and management decisions |

Public liability is your “someone slipped, tripped, or was injured around your operations” cover. Professional indemnity is different. That's for the financial fallout from work that was wrong, late, incomplete, or relied on by a client to their detriment.

Why this matters before you sign

A lease might require public liability. A consulting contract may require professional indemnity. A board role or growing company structure can make management liability more relevant than many owners expect.

Commercial rule: If a contract creates risk for someone else, that contract often pushes the insurance burden back onto you.

This is why owners should review insurance clauses before signing anything significant. Don't wait until settlement, fit-out, or onboarding. By then, you're negotiating from a weak position.

For a broader plain-English look at how different exposures fit together, this guide to types of risk in insurance is a useful starting point.

How To Assess Your Unique Business Insurance Needs

The hardest part of small business insurance requirements isn't finding policy names. It's working out which risks apply to your business now, and which ones are likely to appear after your next hire, contract, or move.

Australian business obligations are fragmented across workers' compensation, compulsory third-party motor, and contract-based requirements. A key challenge for SMEs is mapping these overlapping obligations into a practical decision tree, especially for sole traders who cross new thresholds when they hire staff or take on bigger work, as noted in this discussion of fragmented business insurance obligations.

Start with operations, not products

A sensible assessment starts with how the business functions day to day.

Ask yourself:

- Who works in the business: Employees, contractors, family members, or just you?

- Where work happens: Home office, client sites, retail premises, warehouse, road, or mixed locations?

- What you provide: Physical goods, advice, design, trade work, health services, digital services, or data handling?

- What assets matter most: Vehicles, stock, equipment, fit-out, revenue continuity, or reputation?

- Which agreements bind you: Lease terms, franchise conditions, tender documents, finance covenants, or service contracts?

A café, a bookkeeper, an electrician, and an online consultant all face different exposures even if turnover is similar. Insurance should reflect operations, not just industry labels.

Build your decision tree

This is the process I'd use with a business owner who wants clarity fast:

- List every activity that creates obligation. Hiring staff, driving for work, inviting the public in, storing stock, giving advice, or handling client data all matter.

- Pull every contract into one place. Lease schedules, client MSAs, supplier contracts, subcontractor agreements, and finance documents often contain insurance clauses.

- Mark what would hurt most if it stopped. For some businesses it's premises access. For others it's revenue interruption, equipment loss, or one negligence claim.

- Match cover to the consequence. Insurance should protect the balance sheet, cash flow, and your ability to keep trading.

- Review after every meaningful change. New staff, a new vehicle, a larger contract, or a new location can all change the answer.

Most owners don't have an insurance problem. They have a mapping problem.

The questions that sharpen the answer

If you're stuck, these prompts usually expose the true need quickly:

- Would a client sue if your advice was wrong?

- Would a landlord ask for proof of cover before handing over the premises?

- Would your business stop trading if equipment was stolen or a fire closed the site?

- Would you still have cash flow if weather, theft, or a shutdown interrupted operations?

- Would one vehicle accident create a major personal financial problem?

When owners answer those accurately, the insurance shortlist becomes much clearer.

Avoiding Common Pitfalls And Managing Costs

The cheapest premium often looks smart on a comparison screen. It can be the most expensive mistake you make once a claim, renewal, or contract dispute exposes what the policy doesn't cover.

Recent commentary on the Australian insurance market emphasises that affordability and availability are major issues for small firms. The practical question isn't only what is mandatory. It's also what remains obtainable and sustainable at renewal, particularly where cyber exclusions, flood sub-limits, or higher excesses can leave an SME exposed, as discussed in this market commentary on insurance affordability and availability for small firms.

What doesn't work

These are the patterns that repeatedly create trouble:

- Buying on price alone: A low premium can hide tighter exclusions, lower sub-limits, or a larger excess than the business can comfortably absorb.

- Forgetting to update cover: Owners often insure the business they started, not the business they run now.

- Assuming one policy covers all business activity: It rarely does. Vehicles, advice, premises, stock, and management liability sit in different places.

- Ignoring renewal terms: A policy can continue with changed conditions that materially reduce protection.

- Treating risk control as optional: Poor documentation, weak security, and sloppy processes can make insurance harder to place or more expensive to keep.

Smarter ways to control cost

There are better ways to manage insurance spend than stripping out cover.

For premises-based businesses, practical risk controls can help. Better locks, alarm systems, staff procedures, and documented incident management don't replace insurance, but they support a stronger risk profile. If you're reviewing physical protection, examples of business security systems in Perth can help you think through how insurers may view site security.

A few cost disciplines usually pay off:

- Review sums insured properly: Don't guess. Base them on current replacement reality and contract commitments.

- Bundle where it makes sense: Sometimes combined policies simplify administration and reduce gaps between covers.

- Lift excesses carefully: Higher excesses can lower premiums, but only if the business can fund them during a claim.

- Clean up disclosures: Accurate payroll, vehicle use, staffing, and business activity details matter.

- Shop before renewal pressure hits: Waiting until the last minute weakens your options.

Cheap insurance is only cheap before you need it.

Watch the renewal trap

Renewal is where many underinsurance issues surface. An owner thinks the policy has rolled over, but the wording has changed, a sub-limit has tightened, or a risk is now subject to tougher terms.

That's especially relevant for businesses exposed to weather, theft, and cyber incidents. A policy that satisfied a landlord or lender last year may not adequately protect cash flow this year.

The better approach is to treat renewal as a risk review, not an admin task.

Integrating Insurance Into Your Broader Financial Plan

Business insurance is often filed mentally as overhead. That's too narrow. For a small business owner, it's part of the structure that protects income, assets, borrowing capacity, and long-term wealth.

A good insurance setup does more than satisfy a contract. It helps stop a business liability from spilling into personal finances. It supports continuity when trading is interrupted. It protects the value of what you're building, especially if the business is meant to fund lifestyle goals, debt reduction, school fees, or retirement.

Why owners should think bigger than compliance

If you're building a business in WA, the business probably sits at the centre of your financial life. It may support your household income, service debt, build super contributions, and eventually become a saleable asset or a retirement funding source.

That changes how insurance should be viewed.

- It protects cash flow: Claims don't just create legal cost. They interrupt operations and decision-making.

- It protects personal wealth: Inadequate cover can force owners to plug business losses with personal assets.

- It protects future options: A well-protected business is in a stronger position to borrow, grow, restructure, or transition.

The right lens for decision-making

Insurance decisions should sit alongside structure, tax, debt, and investment planning. They shouldn't be made in isolation.

That's also why it helps to look beyond the narrow wording of “mandatory cover” and think in terms of resilience. Some owners start by exploring broader small business coverage choices just to understand the range of protections available, then narrow that list down to what fits their actual risk and budget.

The right policy doesn't just pay a claim. It buys time, preserves options, and stops one bad event from undoing years of work.

When insurance is aligned with the bigger financial plan, it becomes easier to decide what to keep, what to increase, and what doesn't belong.

If you want a second opinion on whether your current cover protects your business and personal wealth, book a complimentary initial call with Wealth Collective. A clear review can help you sort legal obligations from commercial requirements, identify costly gaps, and make sure your insurance supports the broader financial life you're building.