Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You log in to your super fund, see the balance, and feel two things at once. Relief that something is building, and unease that you still don't know whether it will be enough.

That's where a Super Growth Calculator becomes useful. Not because it tells the future, but because it forces your retirement plan into numbers you can test.

These calculators are often used incorrectly. Users enter a few details, accept the defaults, and treat the final projection like a reliable answer. It isn't. It's a model. If the assumptions are weak, the output is weak. If the assumptions are realistic, the calculator becomes a strong decision tool.

Why Your Super Statement Is Only Half the Story

A super statement gives you a snapshot. It shows what you have now. It doesn't show whether your current settings are likely to get you where you want to go.

That gap matters most when retirement stops feeling abstract. You might be in your early 30s and starting to realise small changes today could have a big effect later. Or you might be in your late 50s, looking at a healthy balance on paper and wondering whether it will support the lifestyle you want.

What the statement tells you

Your statement is still valuable. It usually helps you identify the basics:

- Your current balance so you know your starting point

- Recent contributions from your employer and any personal top-ups

- Your investment option such as balanced, growth, or conservative

- Fund fees and insurance costs that may be reducing net growth

That's enough to understand the present. It's not enough to make a retirement decision.

What the calculator adds

A good super growth calculator gives you a forward view. It lets you test what happens if you retire earlier, contribute more, change investment options, or review your fees.

Practical rule: Treat a super growth calculator like a planning tool, not a prediction machine.

The problem is simple. Most calculators feel more precise than they really are. A polished graph can make weak assumptions look credible. That's why two people with similar balances can come away with very different outcomes, depending on the settings they use and the assumptions hidden inside the tool.

If you want a number that helps, you need to challenge the defaults. That starts with your own inputs before you start questioning the calculator's internal logic.

Gathering Your Inputs for an Accurate Projection

Most bad projections start with messy inputs. If your salary is wrong, your contributions are incomplete, or your fees are missing, the calculator can't rescue you.

Start by pulling together your latest super statement, your payslip, and a rough idea of your retirement timing. Don't guess when the information is sitting in front of you.

The core details to collect

These are the inputs that shape the projection most.

- Current super balance. This is your starting capital. Get it from your member dashboard or latest annual statement.

- Current age. This sets the timeframe for compounding and contributions.

- Target retirement age. Don't overthink it. Use the age you're aiming for now, then test alternative scenarios later.

- Salary. Use the figure the calculator asks for, and read the field carefully. Some tools want current salary, others focus on contribution amounts.

- Employer contributions. Check your payslip and fund transactions so you know what's being paid.

- Personal contributions. Include salary sacrifice and after-tax contributions if you make them.

- Investment option. Your current option affects the kind of return assumptions that make sense.

- Fees. Don't skip this. Fees are one of the easiest details to overlook and one of the most important to get right.

Why each input matters

A calculator doesn't just need data. It needs context.

Your age and retirement age tell the tool how long the money has to grow. Your salary and contributions determine how much new money will be added over time. Your investment option helps frame whether your return assumption is sensible or detached from reality.

Fees deserve special attention because they're easy to underestimate. A clean-looking balance can hide a mediocre structure underneath.

A projection built on estimated inputs often gives people false confidence. Accuracy at the start saves a lot of confusion later.

Where people usually get stuck

The confusion usually appears in three places:

| Input | Common mistake | Better approach |

|---|---|---|

| Salary | Using an outdated figure | Check your latest payslip |

| Contributions | Forgetting voluntary top-ups | Review fund transactions |

| Fees | Leaving default settings untouched | Compare against your actual fund statement |

If you like practical calculators, it's useful to see how assumptions affect other long-term financial decisions too. A good example is unlocking solar battery value, where the result depends heavily on what inputs you use and what defaults sit behind the model.

For readers making extra concessional contributions, a salary sacrifice check is worth doing alongside your retirement projection. Use the salary sacrifice super calculator to test whether boosting contributions now improves your longer-term position in a way that fits your cash flow.

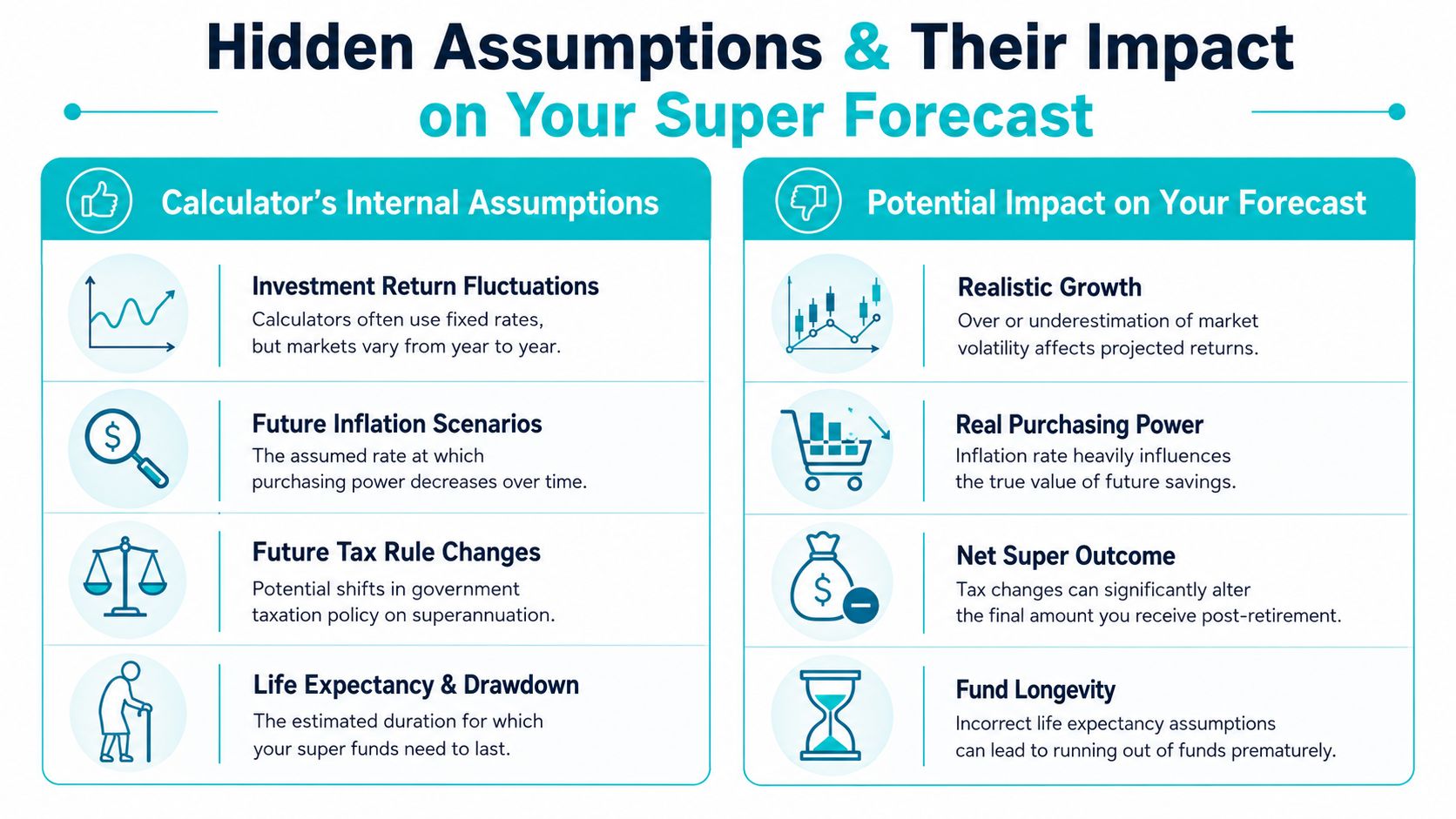

Uncovering Your Calculator's Hidden Assumptions

A calculator can show you a retirement balance that looks reassuring, then subtly build it on return, fee, and inflation settings you would never choose yourself.

That is the genuine risk.

Returns are only useful if they are realistic

Plenty of calculators produce generous outcomes because the default return setting is too high for the way people experience investing. The number may look reasonable in isolation, but your retirement outcome depends on what remains after investment tax, fees, inflation, and periods of weak performance.

A better approach is to test the projection with a tougher assumption and compare the gap. That single step tells you whether the result is sturdy or fragile.

Some financially engaged Australians make this exact point in a discussion in /r/fiaustralia, where they focus on reducing headline assumptions to something closer to real-world outcomes rather than accepting the calculator's first answer.

Treat any default return as a draft, not a fact.

Inflation changes what the final balance is worth

A future super balance can sound large and still fall short of the retirement lifestyle you want. The missing piece is purchasing power.

If inflation is understated, the projection flatters you. If inflation is ignored entirely, the number is close to useless. You need to know whether the tool is showing future dollars or today's buying power, because those are different answers to different questions.

This is why I tell clients to stop reacting to the headline figure. Focus on what that balance is expected to fund each year in retirement, not the size of the lump sum alone.

A retirement projection only helps if you understand what assumptions are doing the heavy lifting.

Fees deserve more scrutiny than the default setting gets

Many calculators use a generic fee estimate. That may be fine for a rough starting point, but it is weak advice if your own fund charges more through administration costs, investment fees, insurance premiums, or indirect costs.

Small fee differences matter because they reduce the amount left invested year after year. Over decades, that gap becomes material.

A simple comparison mindset works well here. If you have reviewed a broker fee comparison before choosing an investment platform, apply the same discipline to super. Net outcomes matter more than product labels.

Use scenarios, not a single forecast

One projection is not a plan. It is a guess built on one set of assumptions.

Run several versions instead:

- Current-settings case using your actual fund details

- Conservative-return case to test whether the result still holds up

- Higher-fee case if your costs are above the calculator default

- Earlier-retirement case if flexibility matters to you

- Extra-contribution case if you are weighing top-ups against current cash flow

That gives you a far better question to answer. Not “What number did the calculator produce?” but “Which assumptions change my decision?”

If you want a broader view of spending needs and retirement timing, compare your super estimate with this retirement calculator for Australia.

Two Real-World Super Growth Scenarios

The value of a super growth calculator becomes clearer when you stop thinking in abstract inputs and start looking at decisions real people face.

These scenarios show why the same calculator can lead to completely different priorities depending on your stage of life. The point isn't the exact output. The point is what the output tells you to do next.

The young professional

A client in their early 30s usually arrives with one main advantage. Time.

They might have a decent starting balance, regular employer contributions, and enough disposable income to make additional personal contributions if there's a strong reason to do it. Their biggest risk usually isn't market noise. It's inaction.

Here's what the calculator often reveals for this type of person:

- Small changes now can reshape the long-term path

- Contribution consistency matters more than trying to time markets

- Investment option selection deserves attention early, not later

- Career progression can do a lot of the heavy lifting if contributions rise with income

For this person, the calculator is less about retirement fear and more about advantage. If they increase contributions modestly, review their fund settings, and stay organised, they give compounding more years to work.

Young professionals don't need perfect certainty. They need a system they'll actually stick with.

The pre-retiree

A client in their late 50s uses the same calculator very differently.

They're not trying to maximise decades of compounding. They're trying to answer more immediate questions. Is the current balance enough? Are the fees too high for the balance size? Is the investment setting still appropriate? How exposed are they to a downturn near retirement?

Here, the projection becomes more sensitive.

| Focus area | Younger accumulator | Pre-retiree |

|---|---|---|

| Main lever | Ongoing contributions | Timing, risk, and drawdown readiness |

| Key concern | Momentum | Sustainability |

| Calculator use | Test growth pathways | Stress-test retirement readiness |

For a pre-retiree, the most useful calculator output often isn't a big final balance figure. It's the warning signal hidden underneath. A small adjustment to retirement age, fees, or investment risk can materially change the confidence level around the plan.

What these scenarios really tell you

A calculator doesn't give both people the same kind of answer.

The younger person gets a strategic prompt. Start early, contribute consistently, and don't drift into a poor default setup. The pre-retiree gets a planning prompt. Tighten assumptions, reduce blind spots, and stop relying on broad averages.

That's why generic calculator articles are often weak. They talk about fields and formulas, but they ignore context. A strong projection always depends on who's using it, what decisions they're facing, and how close they are to needing the money.

Common Super Calculator Mistakes to Avoid

A calculator can mislead you for two reasons. You entered weak inputs, or you trusted assumptions that were never right for you in the first place.

That second mistake catches people more often.

Leaving default settings untouched

Default fee, return, and inflation settings are placeholders. They are not personal advice, and they are rarely a clean match for your fund, investment option, or timeline. As noted earlier, even widely used calculators apply assumptions that can flatter the result if you do not replace them with your own figures.

Fix it: Use your latest super statement and fund disclosure documents to update fees, balance, insurance costs, and investment option details before you trust the projection.

Treating one projection like a plan

One result gives you a clean number. It does not give you a reliable decision.

Run the same calculator three ways. Use a conservative return, a middle case, and a tougher scenario with higher fees or later contribution increases. If the outcome only looks acceptable under the most optimistic settings, you have found a planning problem, not a reassuring forecast.

Fix it: Compare scenarios, then act on the range. If you need ideas, start with practical ways to maximise your superannuation before you rely on heroic assumptions.

Forgetting your career will change

Super calculators work in straight lines. Real working lives do not.

Pay rises, parental leave, part-time periods, bonuses, career breaks, and late-stage catch-up contributions all change the result. Leaving an old salary or contribution rate in place makes the projection stale fast.

Fix it: Update your numbers whenever your income, work pattern, or contribution strategy changes.

Ignoring what sits outside the calculator

A calculator does not know whether you plan to retire debt-free, support family members, sell an asset, or retire with a partner who has very different super. It also does not know how you react when markets fall. Those details matter because they shape how much risk you can carry and how much income you will need.

Fix it: Use the calculator for projection work only. Build retirement decisions around your full balance sheet, household goals, and risk tolerance.

Chasing the biggest balance instead of the most believable outcome

A large future balance can look impressive and still be useless. If the return assumption is too high, the fees are understated, or inflation is too soft, the number tells you very little about your real retirement position.

Good planning works the same way as strategies to reduce trading errors. Better results usually come from disciplined assumptions and regular review, not from optimistic forecasts.

Fix it: Judge the projection by how credible the inputs are and whether the outcome supports your intended lifestyle. Not by how big the final number looks.

Your Next Step From Projection to a Personal Plan

A super growth calculator is a starting point. It gives you a number. It does not give you a strategy.

That distinction matters. A retirement plan isn't just about reaching a target balance. It's about deciding how to get there efficiently, how much risk you should take, how to handle fees, when to adjust contributions, and how to turn a pool of super into dependable income later.

What a real plan adds

A proper plan answers questions calculators can't:

- What contribution approach fits your cash flow now

- Whether your current fund and investment option still suit your goals

- How your super interacts with debt, investments, insurance, and retirement timing

- What needs to change now so retirement feels controlled later

People who make fewer unforced mistakes usually have a better decision process, not better luck. The same lesson shows up in resources on strategies to reduce trading errors. The principle carries across. Good outcomes usually come from clear rules, realistic assumptions, and regular review.

When to get help

If your calculator results raised more questions than answers, that's normal. It usually means you've moved past DIY estimates and into real planning territory.

That point often arrives when:

| Situation | Why advice matters |

|---|---|

| You're nearing retirement | Small mistakes become harder to recover from |

| You have multiple super accounts or complex finances | Coordination matters more than rough estimates |

| You're making extra contributions | Strategy matters more than simply adding money |

| You want clarity on next steps | A calculator can't prioritise actions for you |

If you're reviewing contribution strategy or overall retirement readiness, it also helps to understand how to maximise superannuation in a broader sense rather than relying on one projection result.

The useful question isn't “What does the calculator say?” It's “What should I do with this information now?” That's where a personal plan earns its keep.

If you want help turning a calculator result into an actual strategy, book a free, no-obligation 10-minute call with Wealth Collective. The team can help you sense-check your assumptions, identify your next best move, and build a plan that fits your stage of life, whether you're building momentum or preparing for retirement.