Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

You open your super statement intending to spend two minutes on it. Then the questions start.

Why is the balance where it is? Is the investment option right for you? Are the insurance premiums sensible? Should you be adding more before retirement, or would that lock up money you might need sooner? Many aren't lazy about super. They're busy, and the system gives them just enough information to feel responsible, but not enough clarity to feel confident.

That's where good superannuation advice in Australia matters. It turns a pile of rules, tax settings, and fund choices into a practical decision-making process. Instead of reacting to whatever your fund sends you, you start making deliberate choices about contributions, investments, insurance, and retirement income.

For many Australians, super will become one of the biggest assets they ever own. It deserves more attention than a quick glance and a shrug.

Why Superannuation Advice Is Your Financial Secret Weapon

A lot of people first seek advice after a small shock. It might be a birthday that starts to feel close to retirement. It might be a job change. It might be a conversation with a friend who mentions salary sacrifice, transition planning, or whether their insurance inside super is still fit for purpose.

The pattern is familiar. Someone has done the right thing for years. Their employer has paid super. They've picked a fund, or stayed in the default one, and left it alone. On paper, they've been responsible. In practice, they're not sure whether the money is working as hard as it could.

Super often feels passive until it suddenly feels urgent

Super is designed to be long term, so it's easy to treat it like background admin. That works for a while. Then life changes and the questions become more personal.

A couple in their late fifties might realise one partner has a much smaller balance because of time out of the workforce. A business owner may wonder whether they've missed smart contribution opportunities. A professional on a higher income may suspect there are tax traps if they contribute more without planning first.

Most confusion around super doesn't come from a lack of discipline. It comes from trying to make important decisions with partial information.

Good advice changes the experience. You stop asking, “What does this statement mean?” and start asking, “What should I do next?”

Advice isn't only for the wealthy

That's one of the biggest myths in this space. Some people assume super advice only makes sense when retirement is right around the corner or when balances are very large. In reality, advice is often most useful when you're making decisions that compound over time.

That could mean:

- Early career choices that shape how much goes in and how it's invested

- Family-stage adjustments when cash flow, debt, and insurance all compete for attention

- Pre-retirement planning when contribution timing and structure become more important

- Retirement transition decisions when the wrong move can limit flexibility later

Value is clarity. When your super strategy matches your life, you feel less like you're hoping things will work out and more like you're steering the outcome.

Why this matters in Australia

Australians clearly place value on personalised guidance. In FY24, super funds paid nearly $1.7 billion for financial advice, and external advisers received 89 per cent, or $1.52 billion, according to Investment Magazine's reporting on APRA's Superannuation Fund Expenditure data. That tells you something important. When the decisions matter, many people want personalised advice rather than broad, fund-level information.

That's the shift worth making. Super doesn't need to remain a black box. With the right process, it becomes a strategic asset.

Decoding What Superannuation Advice Actually Involves

Super advice sounds vague until you break it into parts. The simplest way to think about it is this. A financial adviser acts like a personal trainer for your finances. A trainer doesn't just say “exercise more”. They assess where you are, ask what you want, identify weak spots, and build a program that fits your body and goals.

Super advice works the same way.

The four pillars most people actually need

For most households, superannuation advice in Australia sits across four practical areas:

- Contribution strategy. This is about how money gets into super, whether through employer contributions, salary sacrifice, or personal contributions.

- Investment selection. This focuses on how your super is invested and whether that matches your time frame and comfort with risk.

- Insurance review. Many people hold life, TPD, or income protection through super without ever checking the cover details or costs.

- Retirement planning. Retirement planning connects super to your broader plan for drawing income, managing tax, and supporting a preferred lifestyle.

Some people need help in just one area. Others need all four working together.

Information is not the same as personal advice

A fund website can explain what concessional contributions are. The ATO can explain the rules. Neither one tells you whether making an extra contribution this financial year is the right move for your income, tax position, cash flow, and retirement timing.

That's the difference.

Personal advice considers your circumstances and gives you a recommendation that's meant for you, not for a generic member profile. It also creates accountability. Someone has to test whether the recommendation fits your goals and whether the trade-offs are worth it.

Practical rule: If the answer depends on your age, balance, income, family situation, tax position, or retirement timeline, you're no longer dealing with general information. You're in advice territory.

Why people understand their super better after getting help

The process itself improves confidence. When someone explains why your fund is invested a certain way, how your contributions interact with your tax position, and what your insurance is doing, the fog lifts.

That shows up in engagement too. 73% of advised Australians reported strong or some understanding of how their super is invested, compared with 47% of unadvised Australians, according to Super Review's coverage of advised member engagement. That gap matters because people make better decisions when they understand what they own.

A good process doesn't drown you in jargon. It takes a complex system and makes the next decision feel manageable.

How Advice Can Optimise Your Super Contributions

Contributions are one of the few parts of super you can actively influence. Investment markets move when they move. Rules change when governments change them. But your contribution strategy is something you can plan around, adjust, and improve.

That's why advisers spend so much time here.

The two contribution buckets to understand

There are two broad categories to be aware of.

Concessional contributions are before-tax contributions. These include employer super guarantee payments and personal deductible contributions. They're often useful when you want to build super in a tax-aware way.

Non-concessional contributions are after-tax contributions. These can be useful when you have money outside super and want to move more of it into the super environment, subject to eligibility and balance limits.

The rules sound simple at first. The planning around them usually isn't.

The 2026 cap changes that affect strategy

From 1 July 2026, the concessional contributions cap increases to $32,500. The same ATO guidance also notes that Division 293 tax adds an extra 15% tax on concessional contributions if combined income and super contributions exceed $250,000, as set out by the Australian Taxation Office's contributions cap update.

That matters because the right contribution strategy isn't just “put in more”. It's “put in the right amount, at the right time, in the right way”.

For example:

- A salaried professional might use salary sacrifice, but only after checking how employer contributions already use part of the cap.

- A small business owner might prefer a personal deductible contribution because income can vary from year to year.

- A higher-income earner needs to weigh the value of concessional contributions against the impact of Division 293 tax.

If you've heard about using unused cap amounts from prior years, this guide on carry-forward concessional contributions gives useful context before acting.

After-tax contributions can also be powerful

For the 2026-27 financial year, the general non-concessional cap is $130,000, and eligible individuals under 75 may use the bring-forward rule to contribute up to $390,000 over a three-year period, provided their total superannuation balance is below the relevant threshold described by Nationwide Super's summary of current super thresholds.

People often get caught out when they hear a rule and assume it applies cleanly to them. But eligibility, timing, age, and existing balances all matter. Advice helps you check the sequence before money moves.

Getting contributions right isn't just about growing your balance. It's about avoiding preventable mistakes that are difficult to unwind later.

For pre-retirees in particular, this is often the area where individualised advice creates the most immediate clarity.

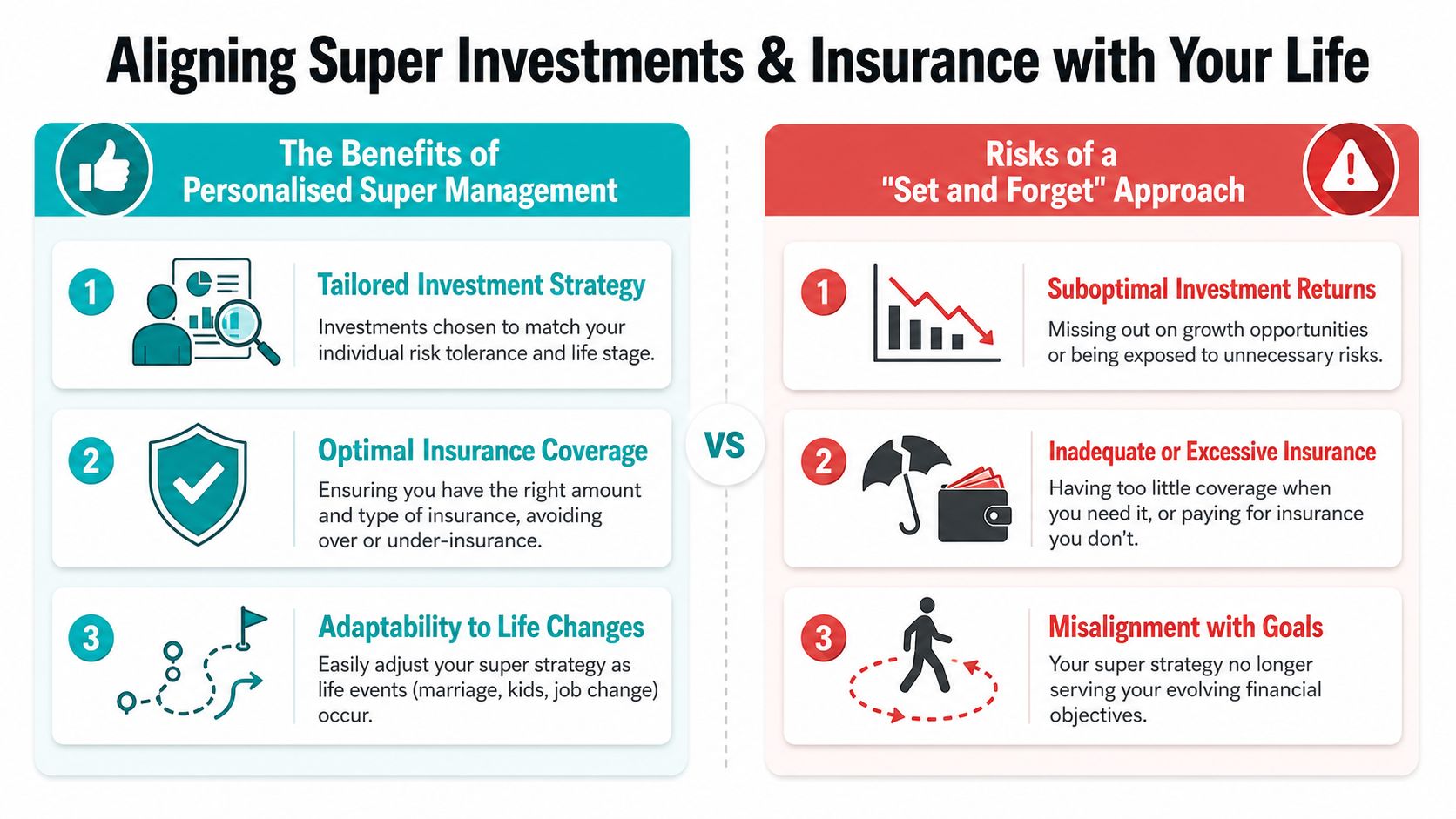

Aligning Super Investments and Insurance with Your Life

You join a super fund in your first full-time job, accept the default investment option, tick the insurance box, and get on with life. Ten or fifteen years later, your income is different, your family responsibilities may have changed, and retirement is no longer an abstract idea. Yet the settings inside your super can still be based on that earlier version of you.

That is often the primary reason people ask for superannuation advice. They do not just want to know the rules. They want someone to help check whether the pieces still fit together.

Why default settings can stop matching your life

Default investment options are built for a broad membership group. That makes them practical for a fund. It does not make them suited to your goals, time frame, or tolerance for market swings.

A person in their thirties who will not touch super for decades may accept more short-term volatility in exchange for higher long-term growth potential. Someone five years from retirement may care more about protecting the balance they have already built. The same logic applies to insurance. A single professional with no dependants usually needs to assess cover differently from a parent with a mortgage and children.

The issue is not that default settings are poor. The issue is that they are generic.

What an advice review usually looks at

This part of the advice process is less about finding a perfect product and more about asking the right questions in the right order. A good review usually works through three areas together, because changing one can affect the others.

- Your investment time frame. How long before you expect to start drawing on your super?

- Your ability to handle risk. If markets fall sharply, would you stay invested or feel pressure to switch at the wrong time?

- Your insurance purpose. Is the cover meant to clear debt, replace income, support children, or protect a business arrangement?

This is why seeking independent help is a common choice for Australians whose super has become more complex. Personal circumstances usually need personal recommendations, not general fund guidance.

Insurance inside super needs a side-by-side comparison

Insurance through super can be tax-effective and convenient, but convenience is only one part of the decision. You also need to compare policy definitions, who owns the cover, how premiums affect your retirement balance, and whether benefits can be paid in the way your family would expect.

People often mix up different types of cover before they even get to the super question. If you want a plain-English refresher first, My Policy Quote on insurance differences gives a useful overview. If you are weighing ownership, premiums, and access to benefits through a fund, this guide to life insurance through super explains the main trade-offs.

One simple test helps here. If you had to explain your current cover to your partner or family member, could you clearly say what it covers, what it does not cover, and why it sits inside super rather than outside it? If the answer is no, that is usually the point where advice becomes valuable.

A useful super review answers one practical question. “Does this setup still match the life I'm actually living?”

That question tends to surface after marriage, divorce, children, a new mortgage, business ownership, or a shift from accumulation to retirement planning. Wealth Collective Financial Advice typically reviews investments and insurance together because growth and protection are connected. A stronger investment setting can be undermined by unsuitable cover, and suitable cover can become too expensive if it gradually erodes long-term super growth.

Navigating Super Rules Regulations and Advice Costs

The cost question matters, and it should. Advice is a professional service, so you want to know what you're paying for, how the fee works, and whether the scope matches the complexity of your situation.

You also need to know when the rules are simple enough to handle yourself and when they're not.

Common fee structures for superannuation advice

Different advisers use different models. The right one depends on whether you need one-off advice, implementation help, or an ongoing relationship.

| Fee Model | How It Works | Best For |

|---|---|---|

| Fixed fee | You pay an agreed fee for a defined piece of advice or plan | People who want clarity on a specific super issue or a one-off strategy |

| Asset-based fee | The fee is linked to the assets being advised on | People who want ongoing management and regular strategic reviews |

| Ongoing service fee | You pay for continuing access, reviews, and advice over time | Households with evolving needs, retirement planning, or multiple moving parts |

None of these models is automatically right or wrong. What matters is transparency. You should understand what service is included, how often reviews happen, and what happens after the initial recommendations are delivered.

Regulation is there to protect you

In Australia, super and financial advice sit within a regulated environment. The ATO administers many of the tax and contribution rules. ASIC oversees parts of the advice framework and consumer protections. That doesn't remove complexity, but it does mean there are standards around how advice is provided.

The trouble is that regulation doesn't make the system easy to interpret. It makes it safer. Those are different things.

Complex rules are where advice becomes more valuable

Some super decisions are routine. Others carry more consequence.

A major example is the additional tax measure that commences on 1 July 2025, introducing an extra 15% tax on earnings related to the portion of a super balance above $3 million. The test date for being in scope is 30 June 2026, based on Treasury's consultation paper on the new super earnings tax measure.

That kind of change can affect contribution decisions, pension planning, asset location, and whether certain structures still make sense. The same is true for people considering an SMSF. Sometimes an SMSF is appropriate. Sometimes it adds cost and admin without solving the underlying problem.

There's also a practical gap in the market. The break-even point for paid super advice is often presented as lower than it really is, but some commentary suggests it may be closer to $1 million in super than $500,000, leaving many people in the middle unsure whether they need full advice or a narrower form of guidance, as discussed in this industry commentary on advice affordability and the mid-balance gap.

That's why a clear initial conversation matters. The key question isn't “Is advice cheap?” It's “What problem am I solving, and what level of help fits it?”

How to Choose the Right Financial Adviser in Australia

Choosing an adviser can feel harder than choosing a fund. The stakes are different. You're not just picking a product. You're choosing a person and a process.

That means technical competence matters, but fit matters too.

Start with the basics you can verify

Australia's super system is enormous. As of March 2026, Australians held $4.43 trillion in superannuation assets, and it is projected to become the world's second-largest retirement pool by 2031, according to Wikipedia's summary of Australian superannuation assets and projection data. With that much money involved, due diligence isn't overkill.

A practical first step is checking the Financial Adviser Register and confirming the adviser is authorised to provide advice. Then look at qualifications, areas of focus, and whether they regularly work with people in situations similar to yours.

Questions worth asking in an initial call

You don't need to interview an adviser like a regulator. You do need to ask enough to understand how they think.

Consider questions like:

- Who do you usually help? A pre-retiree, business owner, executive, or young family often needs a different style of advice.

- How do you charge? Ask for a clear explanation of initial and ongoing fees.

- What does your process look like? You want to know what happens after the first meeting.

- How do you explain recommendations? If they can't simplify a concept, that's a warning sign.

- What happens if I only need help with super, not a full financial plan? Scope should fit the problem.

For a more detailed checklist, this guide on how to choose a financial advisor is a helpful reference point.

Red flags people often miss

Some warning signs are obvious. Others are subtle.

- Rushed certainty. Be cautious if someone recommends a solution before understanding your goals and current setup.

- Foggy pricing. If the fee explanation feels slippery, keep asking questions.

- Product-first language. Good advice starts with your circumstances, not a pre-loaded answer.

- Poor communication. If you leave the conversation more confused than when you entered, that won't improve later.

The right adviser should make complex decisions feel clearer, not more intimidating.

The best working relationships feel collaborative. You should feel comfortable asking basic questions, challenging assumptions, and taking time before moving forward.

Your Next Step to a Wildly Successful Financial Life

The biggest shift needed with super isn't a new product. It's a better process.

When you understand what your super is doing, how contributions affect your position, whether the investments suit your time frame, and whether your insurance still belongs there, decision-making gets lighter. You stop carrying quiet uncertainty in the background.

Clarity comes from organised action

A strong advice process usually follows a simple path:

- Get clear on the issue. Not every person needs a full plan. Some need a contribution strategy. Others need retirement timing, pension planning, or an insurance review.

- Gather the right facts. Super advice gets better when account details, tax settings, and personal goals are on the table.

- Test the trade-offs. Every good strategy has upside and limits. Advice helps you see both before acting.

- Implement and review. Super isn't static. Life changes, legislation changes, and your strategy may need to change with them.

That same structured thinking is useful beyond retirement planning. If your workplace is also trying to support staff with money decisions, resources like this employee financial health roadmap show how financial confidence can improve when guidance becomes more practical and easier to access.

A good first step should feel easy

You shouldn't need to arrive with every answer. You also shouldn't feel pressured to commit before you understand whether the relationship is a fit.

That's why the best first conversation is usually short, clear, and low pressure. You explain what's on your mind. The adviser explains whether they can help, what the process would look like, and whether the scope makes sense for your situation.

Good advice doesn't begin with a sales pitch. It begins with a calm conversation about what's unclear and what matters most to you.

If your super has become one of those lingering tasks you know you should address, that's reason enough to act. You don't need a crisis. You just need a starting point.

Your super can play a major role in building and funding your wildly successful financial life. But guesswork won't get it there. A clear process will.

If you're ready for a simple starting point, book a complimentary introductory call with Wealth Collective. It's a short, no-pressure conversation to understand your goals, talk through what's unclear in your super, and see whether professional advice is the right next step for you.