Business hours

Monday to Friday (8.30AM - 5PM)

Weekend (Closed)

If you're in Perth, Busselton, Dunsborough, or anywhere else in WA and your finances feel more complicated than they did a few years ago, that's normal. The pressure usually doesn't come from one big problem. It comes from several decent-sized decisions landing at once. The mortgage is still there, super is building but not clearly organised, the kids are getting older, insurance needs a review, and retirement no longer feels abstract.

That's the point where many people start looking at wealth management advisors. Not because they want someone to “pick shares”, but because they want someone to help them make smart trade-offs across the whole picture. For the underserved affluent in Western Australia, that need is real. Dual-income families, small business owners, and pre-retirees often need integrated advice without paying for a family-office style service they don't need.

A good advisor should bring order to financial complexity. They should help you decide what matters now, what can wait, and how each financial choice affects the next one.

Is a Wealth Management Advisor Right for You

A lot of people wait too long to get advice because they assume wealth management is only for the very wealthy. That's outdated thinking.

If you're a couple earning solid incomes in Perth, carrying a mortgage, building super, and wondering whether to invest more, reduce debt faster, or improve your insurance, you're already in the zone where advice can make a material difference. The same applies if you run a business in WA and your personal and business finances keep bleeding into each other. It also applies if retirement is getting close and you need to make careful decisions around income, superannuation, tax, and risk.

The real trigger is complexity

The question isn't “Am I rich enough for an advisor?”

The better question is “Have my financial decisions become connected enough that getting one wrong will affect everything else?”

For many Australians, the answer is yes. There's a clear gap for people who need advice suited to complex situations without a family-office price tag. That underserved segment includes dual-income families, small business owners, and pre-retirees with superannuation, debt, and tax trade-offs who need thorough advice, not generic product-led planning, as discussed in this commentary on serving underserved advice clients.

A wealth advisor earns their place when your financial life stops being a set of separate tasks and starts acting like one connected system.

That's the practical value. You're not hiring someone to produce more paperwork. You're hiring someone to help you make cleaner decisions with less second-guessing.

Who usually benefits most

In my view, wealth management advisors are usually worth considering when you're dealing with issues like these:

- Super decisions with real consequences: You're unsure whether to consolidate, contribute more, change investment settings, or coordinate super with your retirement timeline.

- Debt versus investing trade-offs: You can save and invest, but you're not sure how aggressively to reduce non-deductible debt first.

- Insurance uncertainty: You know you need protection, but you don't know how much cover is appropriate or whether your current setup is full of gaps.

- Approaching retirement: You want clarity on how to convert assets into sustainable income without making rushed decisions.

- Business and household overlap: Your cash flow, tax position, borrowing, and succession plans all influence your personal strategy.

A clear rule of thumb

If your financial life has enough moving parts that you keep delaying decisions, you probably need advice. Not generic content. Not another calculator. Actual advice.

That's especially true in WA, where numerous individuals have built good incomes and meaningful assets but still don't feel fully organised. A capable advisor acts like a financial co-pilot. They bring structure, prioritisation, and accountability. For those in that position, that's far more valuable than market commentary.

What a Wealth Advisor Actually Does

A good wealth advisor fixes decision-making before they touch your portfolio.

For many affluent households in Western Australia, the main issue is not lack of income. It is competing priorities. You are earning well, building super, carrying a mortgage, possibly running a business, and trying to protect your family without wasting money on the wrong insurance or the wrong structure. An advisor's job is to turn those competing demands into a strategy that works together.

They connect the parts that usually get handled separately

Many people hear “wealth management advisors” and assume the work starts and ends with investments. That misses the point.

Value is found in coordination. Your investment settings affect your super strategy. Your debt position affects how aggressively you should invest. Your insurance cover affects how much risk your family can reasonably carry. Your tax structure affects what stays in your pocket. If those decisions are made in isolation, the plan gets expensive, clunky, and harder to stick to.

That is why the better benchmark is simple. Is this advisor helping you make stronger decisions across super, tax, debt, insurance, retirement planning, and personal wealth strategy, or are they just managing money?

The five jobs that matter

A capable advisor should be doing work across these areas:

Investment management

They build an investment approach that suits your goals, timeframe, and tolerance for risk. Good advice also answers what each pool of money is meant to do, because growth assets, emergency reserves, and retirement income should not all be treated the same way.Retirement planning

This includes super contributions, pension strategy, withdrawal planning, and the timing of major decisions. For pre-retirees in WA, this is often where small mistakes become expensive.Tax-aware structuring

A wealth advisor should work alongside your accountant so investment, entity, and contribution decisions fit your broader tax position. Advice that ignores tax is lazy advice.Estate and legacy planning

Beneficiary nominations, ownership structures, powers of attorney, and estate intentions need to line up. If they do not, your assets can end up in the wrong hands or tied up at the worst possible time.Risk management

This covers personal insurance, cash reserves, and the level of risk built into your portfolio and borrowing. Protection matters most for dual-income families and business owners because one health event or one disrupted income stream can derail years of progress.

Practical rule: If the conversation stays focused on products or market returns, you are not getting real wealth advice. You are getting a narrower service with a broader title.

What this looks like in real life

For the underserved affluent in WA, advice usually comes down to three practical outcomes.

- Protection Plus: setting up personal insurance and risk controls so one bad event does not wreck the household plan

- Guided Growth: aligning super, investments, and debt reduction with the goals you care about

- Retirement Roadmap: converting accumulated assets into a retirement income strategy you can use with confidence

That is the work Wealth Collective is built around. One lead advisor. One coordinated strategy. Clear trade-offs. Fewer blind spots.

If you want a plain-English explanation of how this broader advice model works, this guide to what financial planning covers is a useful place to start.

Comparing Advisor Types and Fee Structures

Many people get stuck, not because the concepts are hard, but because the industry often explains fees badly.

You should know exactly how an advisor gets paid, what service is included, and where conflicts might sit. If that isn't clear in the first conversation, walk away.

Advisor Fee Structure Comparison

| Fee Type | How It Works | Best For | Key Question to Ask |

|---|---|---|---|

| Asset-based fee | The fee is linked to the amount of money managed on your behalf | Ongoing advice relationships where investments are a major part of the work | What ongoing service will I receive beyond portfolio management? |

| Fixed fee | You pay an agreed dollar amount for defined advice or an ongoing service package | Clients who want cost clarity and a clearly scoped engagement | What exactly is included, and what triggers extra fees? |

| Hourly fee | You pay for the adviser's time | Specific one-off questions or limited strategy work | How many hours do you expect this work to take? |

| Insurance commission | The adviser may receive payment connected to insurance implementation | Clients needing personal risk advice, where cover design and underwriting support matter | How do you manage conflicts when recommending cover? |

What matters more than the label

The fee model matters, but transparency matters more.

An asset-based fee can be fair if the service is broad and ongoing. A fixed fee can be excellent if the scope is detailed and the follow-through is strong. An hourly model can work for focused advice, but it may not suit clients who need long-term coordination. Insurance commissions aren't automatically a problem, but they do require a frank discussion about recommendations and incentives.

Here's what I'd look for:

- Clarity before commitment: You should know how the adviser is paid before any work begins.

- Service matched to fee: If you're paying for ongoing advice, you should receive ongoing advice. Not just annual paperwork.

- Conflict awareness: Ask where product, platform, or implementation incentives could influence recommendations.

- Written scope: Verbal promises aren't enough. The engagement should state what's included.

Independent versus institutionally aligned

This part matters more than many people realise. Some advisors are independent in practice and philosophy. Others are tied, directly or indirectly, to a product provider, institution, or restricted menu of solutions.

That doesn't automatically make one bad and the other good. But it does change the questions you should ask.

Ask an advisor what they can recommend, what they can't recommend, and whether any commercial arrangement limits the strategy they can put in front of you.

For a more detailed breakdown of what Australian advice fees can look like in practice, this guide to financial advice fees in Australia is worth reading before your first meeting.

What to watch out for

The biggest red flags are usually simple:

- Vague pricing: If the explanation feels slippery, it probably is.

- Product-first conversations: If the adviser jumps to solutions before understanding your position, that's poor process.

- No clear review structure: Ongoing fees without a defined review rhythm are hard to justify.

- Overcomplication: Some advisors use complexity to make comparison difficult. Good advice should make things clearer, not murkier.

You don't need the cheapest advisor. You need one whose fee structure is understandable, defensible, and aligned with the service you need.

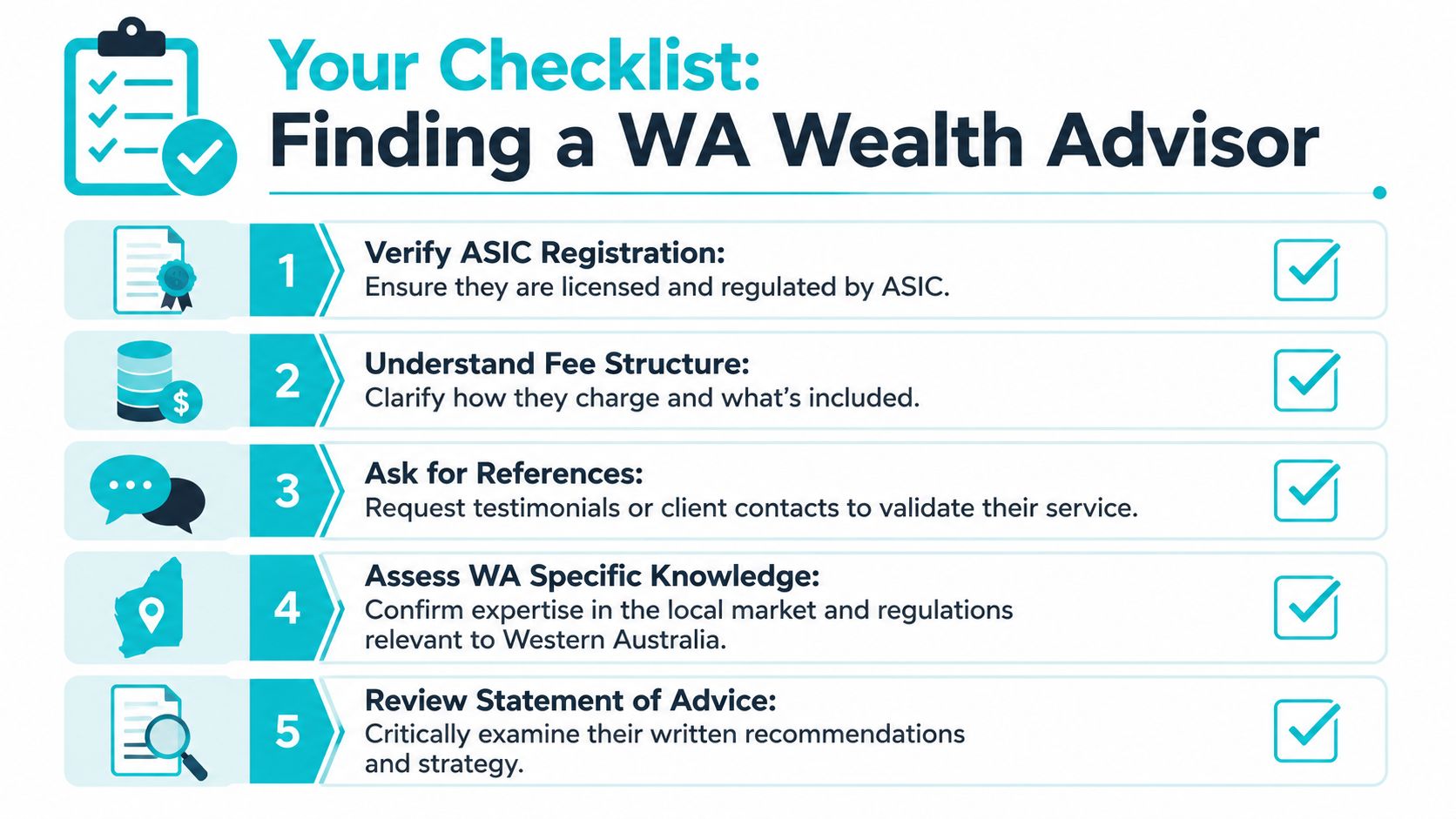

How to Choose the Right Advisor in Western Australia

Choosing an advisor in WA shouldn't be based on who has the slickest website or the most polished introduction meeting. It should be based on whether they can produce advice that fits your circumstances and clearly justify why it fits.

That standard matters in Australia because advice isn't supposed to be generic. Under ASIC's reforms and the best interests duty, advisers must base personal advice on the client's objectives, financial situation, and needs, and they must be able to demonstrate that the advice is appropriate and prioritises the client's interests, as outlined in this discussion of advice data, compliance, and best interests obligations.

Start with the non-negotiables

Before you worry about personality fit, verify the basics.

- ASIC registration: Confirm the adviser is properly authorised and appears on the relevant register.

- Clear advice process: They should be able to explain how they gather information, analyse it, and make recommendations.

- Documented recommendations: Statements of Advice, Records of Advice, and fee disclosures should be treated seriously, not brushed aside as admin.

- Relevant experience: If you're a pre-retiree, dual-income family, or business owner, ask whether they regularly advise clients in situations like yours.

- WA context: Local knowledge helps. Advice doesn't happen in a vacuum. Property decisions, lifestyle goals, and retirement patterns in Western Australia shape the work.

The best interests test in plain English

The best interests duty isn't legal decoration. It's the backbone of quality advice.

An advisor should be able to show why they recommended one path over another, what assumptions they used, what trade-offs they considered, and how the strategy connects to your goals. If they can't explain their reasoning clearly, I wouldn't trust the recommendation.

Good advice leaves a paper trail because good thinking can be explained.

Questions that reveal how an advisor really works

Individuals often ask soft questions and get polished answers. Ask better questions.

What information do you need from me before you'll make any recommendation?

This reveals whether they have a disciplined fact-finding process or a sales process.How do you prioritise competing goals like debt reduction, super contributions, and insurance?

This shows whether they think strategically or work from a template.What does ongoing service include over a normal year?

You want specifics. Reviews, implementation help, contact points, and proactive advice.How do you work with accountants and estate planning lawyers when a strategy crosses over?

Complex clients need coordination, not siloed advice.Can you explain a situation where you told a client not to do something?

Good advisors aren't there to approve every impulse. They should be willing to apply judgement.How will you show me that your advice remains suitable as my circumstances change?

This gets straight to process, review, and accountability.What type of client is not a good fit for your firm?

Honest answers here are valuable. Firms that work well with everyone usually work meaningfully with no one.

How to judge the first meeting

You're not just assessing competence. You're assessing whether the advisor can make complexity manageable.

Use this checklist after the meeting:

- Did they listen properly? Or did they rush to present a solution?

- Did they ask connected questions? Good advisors explore how super, debt, insurance, tax, and retirement plans affect each other.

- Did they explain trade-offs clearly? You want judgement, not jargon.

- Did the fee discussion feel direct? It should.

- Did you leave with more clarity? If you left more confused, that's a problem.

If you want a practical list of what to check before engaging anyone, this guide on choosing a financial advisor gives you a solid interview framework.

The Wealth Collective Process Explained

You book a first meeting because the numbers are getting bigger, but the decisions are getting harder. A Perth couple with two incomes might be weighing school fees against extra super contributions. A pre-retiree in Dunsborough might be asking whether to clear the mortgage faster or protect cash flow. A business owner might have solid revenue and weak personal structure. The trigger is complexity.

A good advice process should bring order to that quickly. You should come away with a clear picture of what matters now, what can wait, and what needs a firm decision.

What a straightforward advice journey should look like

The first step is a short introductory call. The purpose is simple. Clarify your situation, identify the pressure points, and decide whether the relationship makes sense.

Next comes discovery. During this stage, an adviser gathers the facts that drive good judgement. Income, assets, debts, super, insurance, tax position, business interests, family commitments, and retirement goals all need to be set out properly. For the underserved affluent in Western Australia, this stage matters because the trade-offs are rarely isolated. Extra cash can go to the home loan, concessional super contributions, investment accounts, or better cover. You need a framework for choosing, not a pile of disconnected suggestions.

Then the strategy is built. It should be specific and sequenced. First priority. Second priority. What to implement now. What to review later. If advice stays broad, it is not ready.

What that looks like in practice

For a WA couple in their fifties, the work often centres on decisions with direct consequences:

- whether their current super settings still fit their retirement timing

- how to split surplus cash between mortgage reduction and additional contributions

- whether their insurance still matches their income, debts, and family responsibilities

- how to build a retirement income plan that is realistic, tax-aware, and sustainable

- how future care costs may affect the plan, including understanding long-term care insurance

That is where advice earns its keep. It turns competing priorities into a decision order.

Wealth Collective works with clients across personal insurance, superannuation optimisation, investment strategy, debt reduction, and retirement planning. Its service pillars, Protection Plus, Guided Growth, and Retirement Roadmap, reflect the issues many affluent WA households are trying to sort out. Protect the downside. Use cash flow well. Build the next stage with intent.

A good process should leave you more organised after the first proper conversation.

What clients should expect

A capable firm should explain the process in plain language. You should know what happens first, what information is required, when advice will be presented, how implementation is handled, and what ongoing support involves.

If any of that stays vague, expect confusion later. Clear process is not a branding exercise. It shows the adviser can handle complexity, set priorities, and help you act with confidence.

Building Your Wildly Successful Financial Life

A Perth couple in their 40s can earn well, pay down a mortgage, build super, fund school fees, and still feel unsure whether they are making the right calls. A WA business owner can have strong profits and still wonder if too much of their wealth is tied up in the business. That is the gap a good advisor closes.

The households we see most often are not starting from zero. They have momentum. What they lack is a joined-up plan that puts each decision in the right order and connects today's cash flow with the life they want in 10, 20, or 30 years.

The outcome you're buying

You're buying clarity, structure, and follow-through.

For dual-income families, that usually means a clear plan for surplus cash, super, insurance, and lifestyle goals, without treating each decision in isolation. For pre-retirees, it means knowing what retirement can look like in Western Australia, what income is realistic, and where the tax traps sit. For small business owners, it means separating business success from personal financial security so one does not undermine the other.

There is also a broader family issue that often gets ignored until it becomes urgent. Later-life planning is not only about investments and pension balances. It can include aged care, support needs, and the cost of extended care. If that is starting to matter in your household, this guide to understanding long-term care insurance is worth reading.

The decision that matters now

Do not wait until the pressure becomes obvious.

The right time to get advice is when your financial life is getting more valuable and more complicated. That point often arrives earlier than people expect. A second property, rising income, equity in a business, older children, ageing parents, or a retirement date that no longer feels far away can all change the quality of the decisions you need to make.

Good advice gives you a plan you can use. It helps you protect what you have built, use cash flow deliberately, and make progress without second-guessing every major decision.

That is the value Wealth Collective is built to provide for affluent WA households who need integrated advice across super, investments, debt, insurance, retirement, and business-related personal planning. If you want a wildly successful financial life, get clear on what your money needs to do, then put the right advisor at the table.